Capital One Car Loan Credit Score: Your Definitive Guide to Approval and Smarter Auto Financing

Capital One Car Loan Credit Score: Your Definitive Guide to Approval and Smarter Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. For many, securing the right financing is a critical step, and Capital One has emerged as a prominent player in the auto loan landscape. They’re known for their accessibility, often catering to a broader spectrum of credit profiles than some traditional lenders. But what exactly does Capital One look for when it comes to your credit score?

Understanding the nuances of the Capital One car loan credit score requirements is paramount to navigating the application process successfully. This comprehensive guide will demystify Capital One’s lending criteria, explore the credit score ranges they consider, and provide actionable strategies to boost your chances of approval. Whether you have excellent credit, fair credit, or are working to rebuild your credit, we’ll equip you with the knowledge to approach your Capital One auto loan application with confidence.

Capital One Car Loan Credit Score: Your Definitive Guide to Approval and Smarter Auto Financing

Understanding Capital One’s Approach to Auto Loans

Capital One has carved a significant niche in the auto financing market by offering solutions to a wide range of consumers. Unlike some lenders that exclusively target prime borrowers, Capital One is often recognized for its willingness to work with individuals across the credit spectrum, including those with less-than-perfect credit histories. This inclusive approach makes them a popular choice for many car buyers.

Their primary goal, like any lender, is to assess risk. While your credit score is a major indicator of this risk, it’s certainly not the only factor. Capital One utilizes a sophisticated underwriting process that considers multiple aspects of your financial health to determine your eligibility and the terms of your loan. This holistic view is crucial to understanding why one applicant might be approved with a particular score while another might face different outcomes.

Based on my experience working with countless individuals navigating auto loans, Capital One truly stands out for its flexibility. They understand that life happens, and a past financial misstep shouldn’t necessarily bar you from vehicle ownership. Their "sweet spot" for approval often extends beyond the highest credit tiers, making auto financing accessible to more people.

The Credit Score Spectrum: What Capital One Looks For

When it comes to securing a Capital One car loan, your credit score plays a pivotal role. However, it’s not a one-size-fits-all scenario. Capital One evaluates applicants across various credit ranges, understanding that each score tells a different story about a borrower’s financial reliability. Let’s break down what you can expect based on your credit profile.

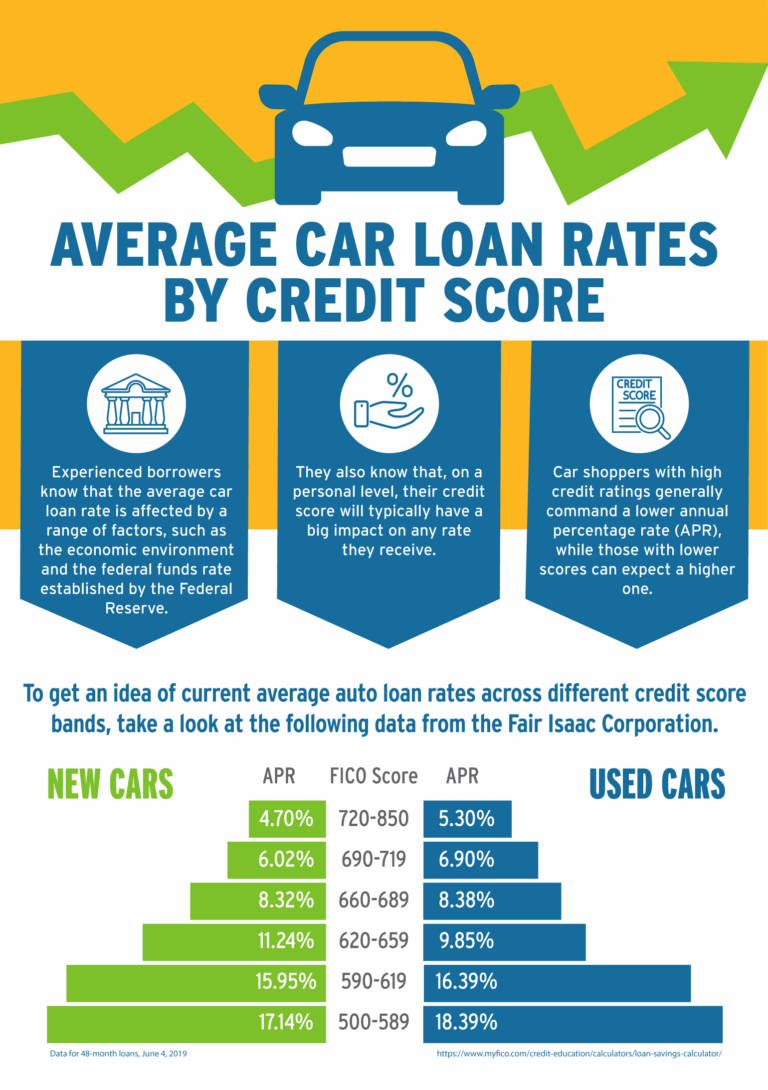

Excellent to Good Credit (700+ FICO Score)

If your FICO score falls into the excellent (800-850) or good (700-799) range, you are in an enviable position. Borrowers with strong credit scores are generally seen as low-risk, responsible payers. For these individuals, securing a Capital One auto loan is typically a smooth process, often accompanied by the most favorable interest rates and flexible loan terms.

With a high credit score, you’ll likely qualify for the lowest Annual Percentage Rates (APRs), which translates to significantly lower monthly payments and less money paid over the life of the loan. Capital One will view your application favorably, and you’ll have strong leverage to negotiate terms, whether it’s for a new or used car loan. This credit tier offers the best opportunity for a cost-effective financing solution.

Fair Credit (600-699 FICO Score)

The fair credit range is where many individuals find themselves, and Capital One is particularly active in this segment. If your credit score is between 600 and 699, you still have a very good chance of approval for a Capital One car loan. However, the terms might not be as attractive as those offered to borrowers with excellent credit.

Applicants in this range may encounter slightly higher interest rates. This is because lenders perceive a moderate level of risk associated with fair credit scores. Despite this, Capital One’s willingness to lend to this group is a significant advantage. You might be asked for a larger down payment or offered a slightly shorter loan term to mitigate some of the perceived risk, but approval is certainly within reach.

Subprime/Poor Credit (Under 600 FICO Score)

This is where Capital One truly differentiates itself. While many traditional lenders shy away from applicants with credit scores below 600, Capital One often provides viable options for those with subprime or poor credit. This doesn’t mean it will be easy, but it does mean there’s a possibility.

For applicants in this range, the interest rates will undoubtedly be higher to compensate for the increased risk. Capital One will be looking for other indicators of your ability to repay, such as a stable income, a substantial down payment, and a reasonable debt-to-income ratio. Securing a car loan with bad credit from Capital One is possible, but it requires careful preparation and realistic expectations regarding the loan terms. The key is to demonstrate stability and a clear plan for repayment.

No Credit History

If you’re new to credit and have no established credit history, securing a loan can be challenging with any lender. Capital One, however, might still consider your application. They often look at alternative data points, such as your income stability, employment history, and banking relationships.

In cases of no credit, having a co-signer with good credit can significantly improve your chances of approval and help you secure more favorable terms. A co-signer essentially shares the responsibility for the loan, reducing the lender’s risk. This can be an excellent way to get your foot in the door and begin building your credit history.

Beyond the Score: Other Factors Capital One Considers

While your credit score is a major piece of the puzzle, Capital One, like all savvy lenders, looks at a broader picture of your financial health. Your score provides a snapshot, but several other elements contribute to your overall loan eligibility and the terms you’ll receive for a Capital One auto loan.

Income and Debt-to-Income (DTI) Ratio

Your income is a crucial factor. Capital One needs assurance that you have a steady and sufficient income to comfortably make your monthly car loan payments. They will typically look at your gross monthly income and your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. A lower DTI ratio indicates you have more disposable income to handle new debt, making you a more attractive borrower. Lenders generally prefer a DTI ratio below 43%, though it can vary.

Down Payment Size

A significant down payment can dramatically improve your chances of approval, especially if your credit score is not stellar. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your commitment and financial responsibility. Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price, if possible. For used car loans, a larger down payment can be even more impactful.

Vehicle Choice

The type of vehicle you intend to purchase also plays a role. Capital One evaluates the vehicle’s age, mileage, and overall value. Newer, lower-mileage vehicles tend to be seen as less risky collateral. Lenders are more comfortable financing a vehicle that retains its value well, as it can be repossessed and sold to recover losses if you default. Be realistic about the vehicle you can afford based on your financial situation.

Loan Term

The length of your loan, or the loan term, directly impacts your monthly payment and the total interest paid. Longer terms mean lower monthly payments but higher total interest over time. Capital One will assess whether your chosen loan term is appropriate for your income and the vehicle’s expected lifespan. They want to ensure the loan isn’t "upside down" (where you owe more than the car is worth) for an extended period.

Employment Stability

A stable employment history signals reliability. Capital One will typically review your job history to see if you have consistent employment, preferably for several years with the same employer or in the same industry. Frequent job changes can sometimes be a red flag, suggesting potential income instability.

Payment History on Other Debts

Beyond just your credit score, Capital One will delve into the specifics of your credit report. They’ll examine your payment history on other loans and credit cards. A consistent record of on-time payments, even on small debts, builds trust and demonstrates your ability to manage financial obligations responsibly. Conversely, a history of late payments or collections will be a significant concern.

Navigating the Capital One Auto Loan Process

Securing a Capital One car loan can be a streamlined experience, especially if you understand their process. Capital One has invested heavily in digital tools to make car buying more transparent and efficient for consumers.

Pre-qualification with Capital One Auto Navigator

One of the most valuable tools Capital One offers is the Capital One Auto Navigator. This platform allows you to get pre-qualified for an auto loan without impacting your credit score. When you use Auto Navigator, Capital One performs a soft credit pull, which doesn’t show up on your credit report to other lenders and has no effect on your score.

Pre-qualification gives you real loan terms, including your estimated interest rate and monthly payment, based on your credit profile. It also shows you which vehicles you’re likely to be approved for within their network of participating dealerships. This step is incredibly empowering, as it allows you to shop for a car with confidence, knowing your financing is already largely in place.

Application Process

Once you’ve found a vehicle and are ready to finalize your purchase, the full application process begins. This typically happens at a participating dealership. You’ll provide more detailed personal and financial information, which will lead to a hard credit inquiry. This hard pull will temporarily lower your credit score by a few points, but the impact is usually minor and short-lived.

The dealership will submit your information to Capital One, leveraging the pre-qualification details you already have. Having your pre-qualification offer in hand significantly speeds up this stage, as much of the initial assessment has already been completed.

Dealership Experience

Having a pre-qualification offer from Capital One before stepping onto the lot puts you in a much stronger negotiating position. You’re no longer just a shopper; you’re a pre-approved buyer. This means you can focus more on negotiating the vehicle price rather than worrying about loan approval. The dealership will work with Capital One directly to finalize the loan, often making the entire transaction smoother and more efficient. For a deeper dive into optimizing your dealership visit, you might find our guide on "Maximizing Your Dealership Experience with Pre-Approved Loans" helpful.

Strategies for Improving Your Chances of Capital One Car Loan Approval

Even if your credit score isn’t perfect, there are proactive steps you can take to significantly improve your chances of getting approved for a Capital One car loan and securing more favorable terms. These strategies focus on enhancing your financial profile and presenting yourself as a reliable borrower.

Boost Your Credit Score

This is often the most impactful strategy. Even a modest improvement in your credit score can unlock better interest rates and terms.

- Pay Bills on Time: This is the single most important factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date on any of your accounts, from credit cards to utility bills.

- Reduce Existing Debt: Lowering your credit card balances is particularly effective. Aim to keep your credit utilization (the amount of credit you’re using compared to your total available credit) below 30%. This shows lenders you’re not over-reliant on credit.

- Check Your Credit Report for Errors: Regularly review your credit reports from all three major bureaus (Equifax, Experian, TransUnion). Mistakes can unfairly drag down your score. Dispute any inaccuracies immediately.

- Avoid New Credit Applications: In the months leading up to a car loan application, refrain from applying for new credit cards or other loans. Each application results in a hard inquiry, which can temporarily lower your score.

Save for a Larger Down Payment

As discussed, a substantial down payment reduces the loan amount and lowers the lender’s risk. It also demonstrates your financial discipline. A larger down payment can also lead to a better loan-to-value (LTV) ratio, which is attractive to lenders. Even an extra few hundred dollars can make a difference in your loan terms.

Consider a Co-signer

If your credit score is on the lower side or you have limited credit history, a co-signer with good credit can be a game-changer. A co-signer shares the legal responsibility for the loan, which reassures Capital One that the loan will be repaid. However, understand that a co-signer is equally responsible for the debt, so choose someone you trust and who understands the commitment.

Choose the Right Vehicle

Being realistic about the vehicle you’re applying to finance is crucial. Capital One evaluates the car as collateral. Opting for a reasonably priced, reliable vehicle that aligns with your income can make your application more appealing. Avoid overspending on a luxury vehicle if your financial profile suggests otherwise. Common mistakes to avoid are applying for a loan on a vehicle that’s significantly more expensive than your financial situation can comfortably handle, as this often leads to denial or unmanageable payments.

Understanding Loan Terms and Interest Rates

Securing a Capital One car loan isn’t just about approval; it’s about understanding the terms you’re agreeing to. The interest rate is arguably the most significant factor impacting the total cost of your loan, and it’s directly tied to your credit score.

A higher credit score typically qualifies you for a lower interest rate. This means you’ll pay less in interest over the life of the loan, resulting in lower monthly payments and a reduced overall cost for your vehicle. Conversely, a lower credit score will likely result in a higher interest rate, increasing both your monthly payments and the total amount you pay back.

It’s crucial to compare offers, even if you’re pre-qualified with Capital One. While their Auto Navigator provides excellent transparency, checking rates from other lenders, credit unions, or even your existing bank can help you ensure you’re getting the most competitive deal. Remember, a difference of even one or two percentage points in your interest rate can save you thousands of dollars over a typical five-year car loan. For more detailed insights into how interest rates are calculated and how they affect your auto loan, consider exploring resources from trusted financial education sites like the Consumer Financial Protection Bureau (CFPB).

What to Do If Your Application Is Denied (or Approved with Unfavorable Terms)

Even with careful preparation, sometimes a Capital One auto loan application might not go as planned. Don’t be discouraged if your application is denied or if the approved terms aren’t what you hoped for. This is an opportunity to learn and improve.

Understand the Reason for Denial

By law, if your credit application is denied, the lender must provide you with a specific reason. Capital One will send you an adverse action notice explaining why your application was not approved. This notice is invaluable. It might point to a low credit score, high debt-to-income ratio, insufficient income, or even an error on your credit report. Understanding the exact reason allows you to address the specific issue.

Rebuilding Credit

If a low credit score was the primary reason, focus on the strategies mentioned earlier: paying bills on time, reducing debt, and reviewing your credit report. It takes time, but consistent positive financial behavior will gradually improve your score. Consider secured credit cards or small credit-builder loans as stepping stones.

Exploring Alternatives

If Capital One isn’t the right fit at this moment, explore other options. Some lenders specialize in subprime auto loans, although their rates will likely be higher. Credit unions often have more flexible lending criteria and may offer competitive rates to their members. You could also consider saving up a larger down payment or opting for a less expensive vehicle to reduce the loan amount needed. Sometimes, taking a few months to save and improve your credit can open up better financing opportunities in the near future.

Capital One Auto Navigator: A Closer Look

We’ve touched upon the Capital One Auto Navigator already, but its significance in the car buying process for a Capital One car loan warrants a closer examination. This digital tool is more than just a pre-qualification service; it’s a comprehensive resource designed to empower consumers.

The Auto Navigator allows you to:

- Get Pre-qualified: As discussed, this involves a soft credit pull, providing you with personalized loan terms without affecting your credit score.

- Shop for Cars: You can browse millions of new and used vehicles from participating dealerships within the Capital One network. The platform shows you cars that fit your pre-qualified financing, making your search highly efficient.

- Calculate Payments: For each vehicle you consider, the Auto Navigator provides estimated monthly payments based on your pre-qualified terms, down payment, and chosen loan length. This real-time calculation helps you stay within your budget.

- Compare Options: You can easily compare different vehicles and their associated financing costs side-by-side.

This tool significantly streamlines the car buying process by bringing financing transparency upfront. It eliminates much of the guesswork and stress associated with securing an auto loan, allowing you to focus on finding the right vehicle. By understanding your financing options before stepping foot in a dealership, you gain significant leverage and can make a more informed purchase decision. If you want to dive deeper into leveraging digital tools for car buying, our article on "Smart Car Buying: How Online Tools Can Save You Time and Money" provides further insights.

Conclusion: Your Path to a Capital One Car Loan

Navigating the world of auto financing, especially concerning your credit score, can seem daunting. However, with Capital One, the path to a car loan is often more accessible than with many other lenders, catering to a broad spectrum of credit profiles. Understanding the role of your Capital One car loan credit score, alongside other crucial financial factors like income and down payment, is the first step toward securing favorable financing.

Whether you possess excellent credit, are in the fair credit range, or are working to rebuild your credit, Capital One offers options. By utilizing tools like the Capital One Auto Navigator for pre-qualification, diligently improving your credit score, and preparing a solid financial presentation, you significantly enhance your chances of approval. Remember, securing a car loan isn’t just about getting the keys; it’s about doing so on terms that fit your budget and contribute positively to your financial well-being. Take control of your car buying journey with informed decisions and confident steps.