Car Loan Calculator With Trade In And Payoff: Your Ultimate Guide to Smart Car Financing

Car Loan Calculator With Trade In And Payoff: Your Ultimate Guide to Smart Car Financing Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone for many, but the financial aspects can often feel like navigating a complex maze. From deciphering interest rates to understanding trade-in values and existing loan payoffs, it’s easy to feel overwhelmed. Many car buyers walk into a dealership feeling unprepared, potentially leaving money on the table or agreeing to less favorable terms.

This is precisely where a powerful tool like a Car Loan Calculator With Trade In And Payoff becomes your indispensable co-pilot. It’s more than just a simple math tool; it’s your strategic advantage, empowering you to make informed decisions and secure the best possible deal. In this comprehensive guide, we’ll demystify the process, explain every crucial component, and show you how to leverage this calculator for a smoother, more financially savvy car purchase.

Car Loan Calculator With Trade In And Payoff: Your Ultimate Guide to Smart Car Financing

Understanding the Core Components of Your Car Loan

Before we dive into the mechanics of the calculator, let’s break down the essential elements that shape your car financing experience. Each piece plays a significant role in determining your final loan amount and monthly payments.

What is a Car Loan Calculator and Why Is It Crucial?

At its heart, a car loan calculator is a digital tool designed to estimate your potential monthly car payments. You input variables like the vehicle price, down payment, interest rate, and loan term, and it instantly provides an estimated payment figure. This basic function is invaluable for setting a realistic budget before you even start shopping.

However, a truly advanced car loan calculator goes a step further. It integrates crucial real-world scenarios, like accounting for your trade-in vehicle and any outstanding loan on it. This comprehensive approach is what transforms it from a simple estimation tool into a powerful financial planning instrument. It helps you understand the true cost of your new vehicle and how your current one impacts that figure.

The Power of Your Trade-In Value

Your current vehicle, if you plan to trade it in, isn’t just an old car; it’s a valuable asset that can significantly reduce the cost of your next purchase. The "trade-in value" is the amount a dealership is willing to offer you for your existing car, which is then typically applied towards the purchase price of your new vehicle.

Several factors influence this value. These include the car’s make, model, year, mileage, overall condition (both mechanical and cosmetic), and current market demand. A well-maintained car with low mileage will naturally command a higher trade-in value than one that has seen better days.

Pro tips from us: To maximize your trade-in value, consider getting your car detailed, fixing minor dents or scratches, and ensuring all routine maintenance is up to date. Gather appraisals from multiple sources – not just the dealership you’re buying from – to ensure you’re getting a fair offer. Websites like Kelley Blue Book or Edmunds can provide excellent starting points for estimating your car’s worth.

Navigating Your Current Car’s Payoff

If you still owe money on your current vehicle, understanding its "payoff amount" is absolutely critical. This is the exact amount of money you need to pay your lender to completely satisfy your existing car loan. It includes the principal balance, any accrued interest, and sometimes small administrative fees.

You can typically obtain your precise payoff amount by contacting your current loan provider directly. They will provide a "10-day payoff quote," which is valid for a specific period, accounting for interest that will accrue during that time. This figure is non-negotiable and must be accurate for any trade-in scenario. Knowing this number empowers you to calculate your equity, which is arguably the most important piece of the puzzle.

Positive vs. Negative Equity: A Deep Dive

The relationship between your car’s trade-in value and its payoff amount determines your equity position. This position can profoundly impact your next car loan.

Understanding Positive Equity

Positive equity occurs when your car’s market value (what it’s worth on trade-in) is greater than the amount you still owe on your loan. For example, if your car is appraised for $15,000 and you only owe $10,000, you have $5,000 in positive equity.

This is the ideal scenario. Your positive equity acts just like an additional down payment on your new vehicle. It directly reduces the amount you need to finance, leading to lower monthly payments and less interest paid over the life of your new loan. It provides a significant financial advantage, making your next car more affordable.

Dealing with Negative Equity (Being "Upside Down")

Conversely, negative equity, often referred to as being "upside down" or "underwater" on your loan, means you owe more on your car than its current market value. If your car is worth $10,000 but you still owe $12,000, you have $2,000 in negative equity.

This situation presents a challenge. When you trade in a car with negative equity, the dealership will typically roll that outstanding balance into your new car loan. This means your new loan amount will be inflated by the negative equity, leading to higher monthly payments and potentially extending the loan term. It’s a common mistake to ignore this, as it can snowball into a cycle of being perpetually upside down on your vehicle loans.

Common mistakes to avoid are: Not knowing your equity position before you start negotiating. Walking into a dealership without this crucial information puts you at a disadvantage. You might unknowingly agree to roll over a substantial negative equity, making your new car far more expensive than anticipated.

If you find yourself with negative equity, consider your options carefully. You might pay off the negative balance out-of-pocket, sell the car privately (which often yields a higher price than trade-in, allowing you to cover the deficit), or wait until your loan balance drops below the car’s value before trading in.

How the Car Loan Calculator With Trade In And Payoff Works (Step-by-Step)

Now that we understand the core components, let’s walk through how a comprehensive Car Loan Calculator With Trade In And Payoff brings it all together. This structured approach empowers you to see the complete financial picture.

Step 1: Gather Your Data

Before you even touch the calculator, collect all the necessary information. This accuracy is paramount for reliable results.

- New Car Price: The sticker price or negotiated price of the vehicle you intend to purchase.

- Trade-In Value: The estimated or appraised value of your current car. Get multiple quotes if possible.

- Current Loan Payoff: The precise, up-to-date amount you owe on your existing vehicle.

- Additional Down Payment: Any extra cash you plan to put down, separate from your trade-in equity.

- Desired Loan Term: How long you want to take to repay the loan (e.g., 36, 48, 60, 72 months).

- Estimated Interest Rate (APR): This is crucial. Your credit score and market conditions will heavily influence this. Based on my experience, getting pre-approved for a loan before visiting the dealership provides you with a solid interest rate estimate to use in the calculator.

Step 2: Calculate Your Net Trade-In Value (Equity)

This is where the trade-in and payoff figures merge. Subtract your current loan payoff amount from your trade-in value.

- Trade-In Value – Current Loan Payoff = Net Equity

If the result is positive, you have positive equity that reduces your new loan. If it’s negative, you have negative equity that will be added to your new loan.

Step 3: Determine Your Total Amount to Finance

Now, combine all the elements to find out how much you actually need to borrow.

- New Car Price – Additional Down Payment – Net Positive Equity = Total Amount to Finance

- OR

- New Car Price – Additional Down Payment + Absolute Value of Net Negative Equity = Total Amount to Finance

This final number is the principal amount of your new car loan. It’s the most critical input for the next step.

Step 4: Input into the Calculator and Analyze Results

With your total amount to finance in hand, input it along with your desired loan term and estimated interest rate into the car loan calculator. The calculator will then provide:

- Estimated Monthly Payment: This is the figure you’ll be paying each month.

- Total Interest Paid: The total amount of interest you’ll pay over the life of the loan.

- Total Cost of the Loan: The sum of the principal and total interest.

Run multiple scenarios by adjusting the down payment, loan term, or even the estimated interest rate (if you’re comparing different lenders). This allows you to see how each variable impacts your monthly payment and the overall cost.

Beyond the Basics: Factors Influencing Your Car Loan

While the calculator provides a solid framework, several other factors can significantly sway your final loan terms and costs. Understanding these empowers you to negotiate more effectively.

The Impact of Interest Rates

The interest rate, expressed as an Annual Percentage Rate (APR), is essentially the cost of borrowing money. A higher interest rate means you pay more for the privilege of borrowing, increasing both your monthly payments and the total cost of the loan.

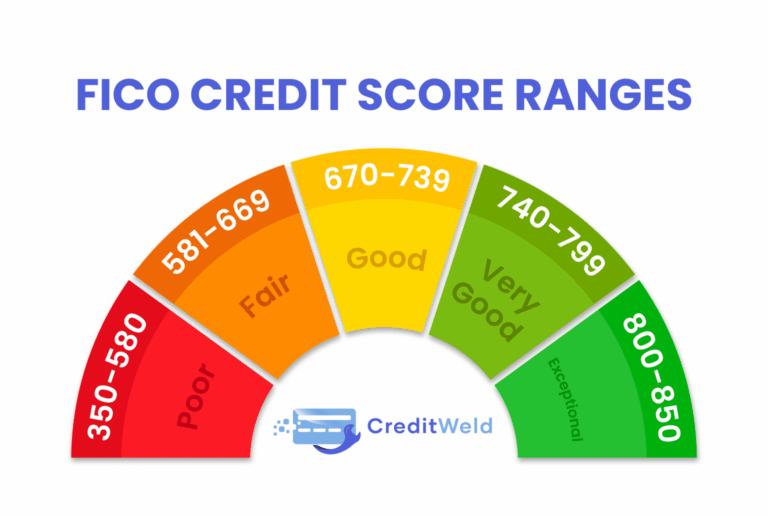

Your credit score is the primary determinant of the interest rate you’ll be offered. Borrowers with excellent credit scores typically qualify for the lowest rates, while those with lower scores will face higher rates. Market conditions, such as the Federal Reserve’s prime rate, also play a role, influencing the general availability and cost of credit. This is why it’s so important to check your credit score and history well before applying for a loan.

Choosing the Right Loan Terms

The "loan term" refers to the duration over which you will repay your loan, typically expressed in months (e.g., 60 months, 72 months). Shorter loan terms generally result in higher monthly payments but lower total interest paid over the life of the loan. Conversely, longer loan terms offer lower monthly payments but accumulate more interest over time, making the car more expensive overall.

Finding the right balance depends on your budget and financial goals. While a 72-month or even 84-month loan might seem appealing due to lower monthly payments, carefully consider the long-term cost. Pro tips from us: Aim for the shortest loan term you can comfortably afford, as this minimizes the total interest you pay and helps you build equity faster.

The Value of a Down Payment

A down payment is the initial sum of money you pay upfront for a vehicle, reducing the amount you need to borrow. A larger down payment has several significant benefits. It directly lowers your principal loan amount, which in turn reduces your monthly payments and the total interest you’ll accrue.

Furthermore, a substantial down payment can sometimes help you qualify for a better interest rate, as it signals to lenders that you’re a lower-risk borrower. It also helps you build positive equity in your car more quickly, making future trade-ins more advantageous.

Don’t Forget Additional Costs

The sticker price of the car isn’t the only expense you’ll encounter. Various additional costs can significantly impact your total outlay. These include:

- Sales Tax: Varies by state and can be a substantial amount.

- Registration Fees: Charges to register your vehicle with the state, also varying by location.

- Documentation Fees ("Doc Fees"): Fees charged by the dealership for processing paperwork. These can often be negotiable to some extent.

- License Plate Fees: The cost for your vehicle’s license plates.

- Optional Add-ons: Extended warranties, GAP insurance, paint protection, etc., which can be rolled into your loan or paid separately.

Always factor these into your overall budget. While some can be financed, paying them out-of-pocket upfront prevents them from accruing interest over the loan term.

Pro Tips for Using Your Car Loan Calculator Effectively

Leveraging your Car Loan Calculator With Trade In And Payoff to its full potential requires a strategic approach. Here are some expert tips to guide you:

- Get Multiple Trade-In Appraisals: Don’t just rely on the first offer. Visit several dealerships or use online appraisal tools to get a realistic range for your car’s value. This empowers you during negotiations.

- Know Your Payoff Amount Accurately: Contact your current lender for an official 10-day payoff quote. This ensures you’re working with precise numbers, avoiding any surprises.

- Understand Your Credit Score: Check your credit report and score well in advance of car shopping. This gives you time to address any inaccuracies and provides an expectation of the interest rates you might qualify for. For tips on improving your credit, consider reading our article on Improving Your Credit Score Before a Major Purchase.

- Shop Around for Interest Rates (Get Pre-Approved): Don’t wait until you’re at the dealership to think about financing. Get pre-approved by your bank, credit union, or online lenders. This gives you a benchmark rate to compare against dealership financing offers.

- Factor In All Additional Costs: As discussed, sales tax, registration, and other fees can add thousands to the total. Include these in your budget to avoid unexpected financial strain.

- Run Multiple Scenarios: Experiment with different down payment amounts, loan terms, and even slightly varied interest rates. This helps you understand the flexibility you have and find the payment structure that best fits your budget.

- Don’t Just Focus on the Monthly Payment: While important, a low monthly payment achieved by extending the loan term too long can lead to paying significantly more in interest overall. Always consider the total cost of the loan.

- Be Prepared to Walk Away: Having all your numbers calculated gives you confidence. If a deal doesn’t align with your pre-calculated budget, be ready to walk away and explore other options.

When to Use This Powerful Tool

The Car Loan Calculator With Trade In And Payoff isn’t just for the final stages of a purchase; it’s a tool you should use throughout your car buying journey:

- Before Stepping into a Dealership: Arm yourself with knowledge. Knowing your budget, trade-in equity, and potential monthly payments gives you immense negotiating power.

- Comparing Different Vehicles: Use the calculator to compare the financial impact of various cars you’re considering. A slightly more expensive car might have a better resale value, affecting future trade-in potential.

- Deciding Between Trading In or Selling Privately: Run the numbers for both scenarios. Sometimes, selling your car privately can yield a higher return, which you can then use as a larger down payment.

- Budgeting for a Future Car Purchase: If you’re planning a car purchase months or years down the line, use the calculator to set savings goals for a down payment or to pay down your current loan to achieve positive equity.

Common Pitfalls and How to Avoid Them

Even with the best tools, car buying can have its traps. Here are some common mistakes and how to sidestep them:

- Ignoring Negative Equity: Rolling negative equity into a new loan is a common pitfall that can lead to being perpetually "upside down" on your vehicles. Address it upfront or postpone your purchase.

- Not Getting Pre-Approved: Without a pre-approval, you’re negotiating blindly on interest rates. The dealership might not offer you the best rate available, and you won’t know it.

- Focusing Only on Monthly Payments: Dealerships often try to steer conversations toward monthly payments. Always ask for the "out-the-door price" and consider the total cost of the loan, including all fees and interest.

- Underestimating Additional Costs: Forgetting about sales tax, registration, and other fees can lead to a rude awakening. Factor them into your initial calculations. For more on managing car ownership costs, check out our guide on Understanding Car Insurance Options.

- Not Negotiating Trade-In Value: Your trade-in is a separate transaction from your new car purchase. Negotiate it independently. Don’t let the dealership lowball you, especially if you’ve done your research.

The Road Ahead: Financial Planning and Car Ownership

The journey doesn’t end when you drive off the lot. Smart car ownership extends to ongoing financial planning. Remember to budget for insurance, routine maintenance, fuel, and unexpected repairs. Regularly review your financial health and loan terms. Making informed decisions at every stage ensures long-term financial stability and a more enjoyable car ownership experience.

The Car Loan Calculator With Trade In And Payoff is more than just a convenience; it’s an empowering tool for financial literacy. By meticulously calculating your options, understanding the nuances of equity, and preparing for every financial angle, you transform the often-stressful process of car buying into a strategic, confident, and ultimately rewarding experience. Drive smart, not just far.

External Resource: For additional guidance on car buying and financial planning, consider exploring resources from the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.