Car Loan Length By Year: Your Ultimate Guide to Smart Auto Financing Decisions

Car Loan Length By Year: Your Ultimate Guide to Smart Auto Financing Decisions Carloan.Guidemechanic.com

Deciding on a car loan isn’t just about the monthly payment; it’s profoundly about the car loan length by year. This seemingly simple choice can dramatically impact your financial well-being for years to come, influencing everything from the total amount you pay to your flexibility for future purchases. As an expert in auto financing, I’ve seen firsthand how understanding these nuances can save drivers thousands of dollars and countless headaches.

In this comprehensive guide, we’ll dive deep into the world of auto loan durations, exploring the critical factors, common pitfalls, and expert strategies to help you choose the best term for your unique situation. Our goal is to equip you with the knowledge to make an informed decision, ensuring your next car purchase is a step forward, not a financial burden.

Car Loan Length By Year: Your Ultimate Guide to Smart Auto Financing Decisions

Understanding Car Loan Length: What Does "By Year" Really Mean?

When we talk about car loan length by year, we’re referring to the duration, or term, over which you agree to repay the money borrowed to purchase your vehicle. While often quoted in months (e.g., 36, 48, 60, 72, 84 months), it’s more intuitive for many to think of these in years: 3 years, 4 years, 5 years, 6 years, or even 7 years. This timeframe dictates how long you’ll be making regular payments.

Choosing the right loan term is one of the most significant decisions you’ll make in the car buying process. It’s not merely a number; it’s a financial commitment that shapes your budget, affects your overall interest expense, and even influences your car’s resale value over time. A common misconception is that a lower monthly payment always equates to a better deal, but as we’ll explore, this isn’t always the case.

The Immediate Impact of Car Loan Length on Your Monthly Payments

The most apparent effect of your chosen car loan length by year is on your monthly payment. This is where most car buyers focus their attention, often for understandable reasons related to immediate budget constraints. A longer loan term typically results in a lower monthly payment, while a shorter term leads to a higher one.

Let’s consider a hypothetical example. Imagine you’re financing $25,000 for a car at an interest rate of 5%.

- With a 3-year (36-month) loan, your monthly payment might be around $749.

- Extend that to a 5-year (60-month) loan, and your payment could drop to approximately $472.

- Go further to a 7-year (84-month) loan, and you might see payments around $357.

This clear difference in monthly outflow makes longer terms very attractive, especially for those looking to stretch their budget to afford a more expensive vehicle or simply keep their fixed expenses low. However, this immediate relief often comes at a hidden cost, which we’ll uncover next.

The True Cost: How Loan Length Affects Total Interest Paid

While longer loan terms offer the appeal of lower monthly payments, they almost always result in significantly higher total interest paid over the life of the loan. This is a crucial point that many car buyers overlook, focusing instead on the more tangible monthly figure. The longer you take to repay a loan, the more time the principal amount has to accrue interest.

Let’s revisit our $25,000 loan at 5% interest:

- Over 3 years (36 months), the total interest paid would be approximately $1,960.

- Over 5 years (60 months), the total interest could jump to about $3,332.

- Over 7 years (84 months), you might pay as much as $4,989 in interest alone.

Based on my experience, this difference of over $3,000 in interest between a 3-year and a 7-year loan on the same principal is a substantial sum. It’s money that could have gone towards savings, investments, or simply enjoying life. Always remember: the longer your car loan length by year, the more you’ll pay for the privilege of borrowing that money. This is the true financial trade-off for lower monthly payments.

Pros and Cons of Shorter Car Loan Terms (e.g., 3-5 Years)

Choosing a shorter car loan length by year, typically ranging from 3 to 5 years (36 to 60 months), has distinct advantages and disadvantages. This approach is often favored by financially savvy individuals who prioritize long-term savings and quicker debt freedom.

Pros of Shorter Car Loan Terms:

- Significantly Lower Total Interest Paid: This is the most compelling benefit. By paying off the loan quicker, you minimize the time interest can accumulate, leading to substantial savings over the life of the loan.

- Faster Equity Build-Up: Your car depreciates rapidly, especially in the first few years. With a shorter loan, you pay down the principal faster, increasing your equity in the vehicle more quickly. This reduces the risk of being "upside down" or having negative equity.

- Quicker Path to Debt Freedom: Imagine the relief of having one less major monthly payment! A shorter term gets you to this point much faster, freeing up cash flow for other financial goals like saving for a house, retirement, or a new investment.

- Less Risk of Negative Equity: As mentioned, you’re less likely to owe more than your car is worth. This is particularly beneficial if you need to sell or trade in your car sooner than expected.

- Potentially Better Interest Rates: Lenders often view shorter terms as less risky, which can sometimes translate into slightly lower interest rates for well-qualified borrowers.

Cons of Shorter Car Loan Terms:

- Higher Monthly Payments: This is the primary hurdle for many. The larger monthly outflow can strain budgets, especially for those with other significant financial commitments.

- May Limit Car Choice: Higher payments might force you to choose a less expensive vehicle than you initially desired, or require a larger down payment to make the payments manageable.

Pro tips from us: If your budget allows, opting for the shortest loan term you can comfortably afford is almost always the financially smarter move. It drastically reduces your overall cost and puts you in a better financial position sooner.

Pros and Cons of Longer Car Loan Terms (e.g., 6-7 Years, Even 8 Years)

On the other end of the spectrum, longer car loan length by year options, typically 6, 7, or even 8 years (72, 84, or 96 months), have become increasingly common. These terms appeal to a different set of priorities, often driven by affordability and access to pricier vehicles.

Pros of Longer Car Loan Terms:

- Lower Monthly Payments: This is the undeniable draw. Spreading the cost over more years makes each individual payment smaller, making it easier to fit into a tight budget.

- Greater Affordability for More Expensive Cars: Lower payments can make a higher-priced vehicle seem more accessible, allowing buyers to purchase a car with more features or a higher trim level.

- Increased Cash Flow: By keeping car payments low, you theoretically have more discretionary income each month for other expenses, savings, or investments.

Cons of Longer Car Loan Terms:

- Significantly Higher Total Interest Paid: As detailed earlier, this is the biggest drawback. You’ll pay thousands more in interest over the life of the loan compared to a shorter term.

- Prolonged Debt: You’re tied to a car payment for a much longer period, potentially outliving the car’s most reliable years. This can hinder your ability to save or take on other financial commitments.

- Higher Risk of Negative Equity (Upside Down): Cars depreciate rapidly. With a longer loan term, your car’s value can drop faster than you pay down the principal, leaving you owing more than the car is worth. This makes selling or trading in the vehicle problematic.

- Higher Maintenance Costs as Car Ages: By the time you finish paying off a 7-year loan, your car will be 7-8 years old. At this age, maintenance and repair costs typically begin to climb significantly, creating a scenario where you’re paying for a loan and expensive repairs.

- "Car Poor" Syndrome: You might be able to afford the monthly payment, but the total cost and the duration of the debt can severely limit your other financial aspirations.

Common mistakes to avoid are extending your loan term solely to afford a more expensive car than you truly need or can afford long-term. This often leads to a cycle of debt and financial strain.

Key Factors to Consider When Choosing Your Car Loan Length

Selecting the optimal car loan length by year is a personal decision that should be based on a thorough evaluation of several key factors. There’s no one-size-fits-all answer, so it’s essential to assess your individual financial situation and priorities.

-

Your Budget and Monthly Affordability: This is paramount. Don’t just consider what the bank approves you for; determine what you can comfortably afford each month without stretching yourself thin. Account for insurance, fuel, and maintenance costs in addition to the loan payment. A general rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 10-15% of your net income.

-

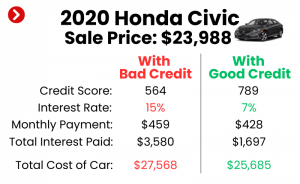

The Interest Rate You Qualify For: A lower interest rate can make a longer term slightly more palatable, but it won’t eliminate the increased total interest paid. Your credit score heavily influences the rate you receive. A higher credit score typically means access to lower rates, making any loan term more affordable.

-

Your Down Payment: A larger down payment reduces the principal amount you need to borrow. This, in turn, lowers both your monthly payments and the total interest paid, regardless of the loan term. It also immediately builds equity and reduces the risk of negative equity.

-

Your Credit Score: A strong credit score is your best asset when securing an auto loan. It directly impacts the interest rate offered by lenders. A low score might limit your options, pushing you towards longer terms with higher rates to achieve an "affordable" monthly payment. Improving your credit before applying can save you thousands.

-

The Car’s Depreciation Rate: Different vehicles depreciate at different rates. Luxury cars and some SUVs tend to depreciate faster than economy cars. If you opt for a long loan term on a fast-depreciating car, you’re at a higher risk of being upside down for a significant portion of the loan. Research your chosen car’s typical depreciation.

-

Your Financial Goals: Are you aiming to be debt-free quickly? Do you have other significant financial goals like buying a house or saving for retirement? If so, a shorter car loan aligns better with these objectives. If your priority is absolute lowest monthly outflow to maximize other investments, a longer term might be considered, but with caution.

The "Sweet Spot" for Car Loan Length: Is There One?

Many financial experts and consumers often point to a 60-month (5-year) car loan length by year as a "sweet spot." This term length often strikes a balance between manageable monthly payments and a reasonable total interest cost. It’s short enough to avoid excessive interest accumulation and prolonged debt, yet long enough to keep payments from being prohibitively high for many budgets.

However, it’s crucial to reiterate that the "sweet spot" is ultimately personal. What works for one individual might not work for another. For some, a 36-month (3-year) loan might be perfectly comfortable and is financially superior. For others, with tighter budgets or higher income, a 72-month (6-year) loan might be the only viable option to afford reliable transportation. The key is to find the balance that aligns with your financial capacity and long-term goals without compromising your financial health.

Navigating Negative Equity (Being "Upside Down")

One of the most significant risks associated with longer car loan length by year is negative equity, often referred to as being "upside down" on your loan. This occurs when the outstanding balance of your car loan is greater than the current market value of your vehicle. It’s a common and financially frustrating situation.

How do long terms increase this risk? Cars depreciate most rapidly in their first few years. If you’re stretching your payments over 6, 7, or even 8 years, you’re paying down the principal much slower than the car is losing value. This gap means you’re likely to be upside down for a considerable period. If you need to sell or trade in the car while in negative equity, you’ll have to pay the difference out of pocket or roll it into a new loan, which is a dangerous financial cycle.

Tips to Avoid Negative Equity:

- Make a Larger Down Payment: This is the most effective strategy. A substantial down payment immediately creates equity and reduces the amount you need to finance.

- Choose a Shorter Loan Term: By paying down the principal faster, you outpace the depreciation curve, building equity quicker.

- Consider Gap Insurance: This type of insurance covers the difference between what you owe on your loan and the car’s actual cash value if your vehicle is totaled or stolen. It’s particularly useful for those with small down payments or longer loan terms.

- Avoid Rolling Over Old Loan Balances: If you have negative equity on your current car, avoid rolling that balance into a new car loan. This starts you off upside down on your new vehicle and compounds the problem.

Strategies for Smarter Car Financing, Regardless of Term

No matter your chosen car loan length by year, there are universal strategies that can help you secure better terms and save money over the life of your loan. Applying these principles will make your auto financing experience much smoother and more affordable.

-

Shop Around for Rates: Do not simply accept the financing offered by the dealership. Obtain pre-approvals from multiple banks, credit unions, and online lenders before you step onto the lot. This gives you leverage and a benchmark rate to compare against. For more insights into managing your car budget, check out our guide on .

-

Get Pre-Approved: A pre-approval tells you exactly how much you can borrow and at what interest rate, based on your creditworthiness. This not only gives you confidence but also allows you to focus on negotiating the car price as a separate transaction.

-

Negotiate the Car Price Before Financing: Dealerships often try to combine the car price and financing into one confusing negotiation. Always agree on the final purchase price of the vehicle first, independent of the financing terms. This prevents them from manipulating numbers to make a less favorable deal seem good.

-

Make Extra Payments (If Possible): If your loan agreement allows for it without penalty, making even small extra payments can significantly reduce your principal balance and, consequently, the total interest paid. Even an extra $50 a month can make a big difference over time.

-

Refinance if Rates Drop or Your Credit Improves: Keep an eye on interest rates. If market rates fall or your credit score improves significantly after you’ve secured your initial loan, consider refinancing. A lower interest rate on the remaining balance can save you a substantial amount of money. If you’re considering refinancing, our article on offers valuable advice.

-

Understand All Fees: Be aware of any origination fees, documentation fees, or other charges associated with your loan. These can add to your overall cost. Always ask for a clear breakdown of all expenses. For more general financial guidance, you can consult trusted sources like the Consumer Financial Protection Bureau.

Conclusion: Making an Informed Decision About Your Car Loan Length By Year

The choice of your car loan length by year is far more impactful than just the monthly payment. It’s a critical financial decision that dictates how much you’ll ultimately pay for your vehicle, how quickly you’ll build equity, and how long you’ll remain in debt. While longer terms offer immediate budget relief through lower monthly payments, they come at the significant cost of higher total interest and increased risk of negative equity. Shorter terms, conversely, save you money in the long run but demand a higher monthly commitment.

By carefully considering your budget, credit score, down payment, and long-term financial goals, you can make an informed decision that aligns with your financial health. Don’t fall into the trap of focusing solely on the lowest monthly payment. Instead, look at the big picture: the total cost of the loan and how it fits into your broader financial strategy. Choose wisely, and drive confidently, knowing you’ve made a smart choice for your wallet and your future.