Car Loan Max: Unlock Your Best Auto Financing Potential

Car Loan Max: Unlock Your Best Auto Financing Potential Carloan.Guidemechanic.com

The dream of owning a new car, or even a reliable used one, often begins with a single question: how will I pay for it? For most, the answer lies in an auto loan. But simply getting a loan isn’t enough; the true goal is to achieve "Car Loan Max" – maximizing your potential for the best possible financing terms. This isn’t about securing the largest loan, but rather the smartest loan that aligns perfectly with your financial health and future goals.

Navigating the world of auto financing can feel like a complex maze, filled with jargon and hidden clauses. However, with the right knowledge and strategic preparation, you can transform this daunting process into a straightforward path toward optimal car ownership. This comprehensive guide will illuminate every corner of the car loan journey, empowering you to secure terms that save you money, reduce stress, and set you up for financial success.

Car Loan Max: Unlock Your Best Auto Financing Potential

Understanding "Car Loan Max": What Does It Truly Mean?

"Car Loan Max" isn’t a specific product or a magic button; it’s a strategic approach. It embodies the art and science of optimizing every aspect of your car loan to ensure you receive the most favorable interest rates, manageable monthly payments, and flexible terms tailored to your unique financial situation. It’s about leveraging your strengths and understanding the lending landscape to your advantage.

The core principle behind maximizing your car loan potential is simple: lenders assess risk. The less risk they perceive in lending to you, the better terms they are willing to offer. Therefore, our mission is to present ourselves as the least risky borrower possible. This involves meticulous preparation, understanding key financial indicators, and knowing where and how to apply for financing. Ultimately, achieving Car Loan Max means securing a loan that supports your lifestyle without becoming a financial burden.

The Pillars of Car Loan Max: Factors Influencing Your Approval & Terms

Lenders evaluate several critical factors when determining your eligibility and the terms of your auto loan. Understanding these pillars is the first step toward strategically positioning yourself for the best possible outcome.

1. Credit Score: Your Financial Report Card

Your credit score is arguably the most significant factor in securing favorable car loan terms. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. FICO and VantageScore are the most common models used by lenders.

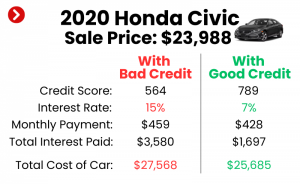

Based on my experience, a higher credit score isn’t just a number; it’s a gateway to significantly lower interest rates, which can save you thousands of dollars over the life of your loan. Lenders see a high score as an indicator of responsible financial behavior and a strong likelihood of on-time payments. A score above 700 is generally considered good, while scores above 750 often unlock the most competitive rates.

Pro tips from us: Before even thinking about a car, pull your credit report from all three major bureaus (Experian, Equifax, and TransUnion). You can do this annually for free at AnnualCreditReport.com. Scrutinize these reports for any errors or discrepancies. Incorrect information can unfairly depress your score, so dispute any inaccuracies immediately. Actively working to improve your credit score, even by a few points, can have a profound impact on your loan terms.

2. Income & Employment Stability

Lenders need assurance that you have a reliable income stream to meet your monthly loan obligations. They assess your gross monthly income and your employment history to gauge your ability to repay the loan. Consistent employment, ideally with the same employer for a year or more, demonstrates stability.

Your debt-to-income (DTI) ratio is also crucial. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates you have more disposable income available to cover new loan payments, making you a more attractive borrower. Lenders typically prefer a DTI ratio below 36%, though some may go higher depending on other factors.

3. Down Payment: Your Initial Investment

Making a substantial down payment is one of the most effective ways to maximize your car loan potential. A down payment reduces the total amount you need to borrow, directly lowering your monthly payments and the total interest paid over the life of the loan. It also significantly reduces the loan-to-value (LTV) ratio.

A lower LTV ratio means you owe less than the car is worth, which reduces the lender’s risk. If you were to default, they could more easily recover their investment by selling the vehicle. Common mistakes to avoid are skipping a down payment entirely or making a minimal one. Aim for at least 10-20% of the car’s purchase price if possible, as this demonstrates your financial commitment and can unlock better loan terms.

4. Vehicle Choice & Age

The type and age of the vehicle you intend to purchase also play a role in loan approval and terms. Newer cars generally qualify for lower interest rates and longer loan terms due to their higher resale value and lower likelihood of immediate mechanical issues. Lenders see them as less risky collateral.

Used cars, especially older models, might come with higher interest rates and shorter loan terms. This is because they depreciate faster and carry a higher risk of mechanical failure, which could impact your ability to repay the loan if unexpected repair costs arise. While a classic car might be your dream, a lender will likely view it differently than a new sedan.

5. Loan Term (Duration): Balancing Monthly Payments & Total Cost

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 48, 60, 72 months). A longer loan term results in lower monthly payments, making the car seem more affordable upfront. However, it also means you pay more in total interest over the life of the loan.

Conversely, a shorter loan term means higher monthly payments but significantly less total interest paid. Finding the "sweet spot" for your loan term is vital for achieving Car Loan Max. It’s about balancing a manageable monthly payment with minimizing the overall cost of the loan. Common mistakes to avoid include extending the term purely for a lower monthly payment, without considering the additional interest accumulation.

Preparing for Your Car Loan Max Journey: Essential Steps Before You Apply

Preparation is the bedrock of successful auto financing. By taking these proactive steps, you’ll approach lenders from a position of strength and clarity, greatly enhancing your chances of securing optimal terms.

1. Know Your Budget Inside Out

Before you even start browsing cars, establish a clear and realistic budget. This isn’t just about what you can afford for a monthly payment; it encompasses the total cost of car ownership. Factor in insurance premiums, fuel costs, routine maintenance, potential repairs, and even parking fees.

Creating a detailed budget will help you determine a maximum affordable purchase price for the car and a comfortable monthly payment. Remember, a car loan is a long-term commitment, so ensure it fits sustainably within your overall financial picture. For more insights on managing your budget effectively, check out our article on .

2. Check and Improve Your Credit Score

As discussed, your credit score is paramount. Obtain your free credit reports and carefully review them for accuracy. If you find errors, dispute them immediately with the respective credit bureau. This can take time, so start early.

Beyond error correction, actively work to improve your score. Pay down existing credit card balances to reduce your credit utilization ratio. Make all your payments on time, every time. Avoid opening new lines of credit in the months leading up to your car loan application, as new inquiries can temporarily ding your score. If you’re unsure about improving your credit, our detailed guide on can provide further assistance.

3. Gather Necessary Documentation

Being organized demonstrates responsibility and speeds up the application process. Have all your essential documents ready before you apply. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (recent pay stubs, W-2s, tax returns for self-employed individuals)

- Bank statements

- Social Security number

Having these documents readily available will streamline your application and prevent delays.

4. Pre-Approval: Your Secret Weapon

Pre-approval is arguably the most powerful tool in your Car Loan Max arsenal. It involves applying for a loan with a bank, credit union, or online lender before you step foot in a dealership. If approved, you receive a conditional offer outlining the maximum loan amount, interest rate, and terms you qualify for.

Why is pre-approval so crucial? It gives you concrete knowledge of your borrowing power, turning you into a cash buyer at the dealership. This shifts the negotiation leverage significantly in your favor, allowing you to focus on the car’s price rather than being swayed by monthly payment figures tied to potentially unfavorable financing. Common mistakes to avoid are only seeking financing through the dealership.

Where to Find Your Car Loan Max: Exploring Lender Options

The landscape of auto lenders is diverse, each offering different advantages. Exploring multiple avenues is key to uncovering the best possible rates and terms for your Car Loan Max.

1. Banks & Credit Unions

Traditional banks are a common source for auto loans, offering a range of products and competitive rates, especially for customers with strong credit. They provide stability and often have established relationships with local dealerships.

Credit unions, however, often stand out. As member-owned non-profits, they frequently offer lower interest rates and more flexible terms than traditional banks. If you’re a member or eligible to join one, a credit union should be high on your list for pre-approval. They tend to prioritize member benefits over profit, which can translate to better deals for you.

2. Dealership Financing

Most dealerships offer in-house financing or work with a network of lenders. This option provides immense convenience, allowing you to handle everything in one place. Dealerships can sometimes offer special promotions, such as 0% APR deals, often for highly qualified buyers on specific new models.

Pro tip: Always compare the dealership’s financing offer with your independent pre-approval. Use your pre-approval as leverage to negotiate a better rate from the dealership. If their offer can’t beat your pre-approval, you already have a solid alternative in hand. Never let convenience override your financial best interest.

3. Online Lenders

The rise of online lenders has added another layer of competition and convenience to the auto loan market. Companies like LightStream, Capital One Auto Finance, and many others offer quick applications, fast approvals, and often competitive rates. Their streamlined processes can be particularly appealing if you value speed and efficiency.

When considering online lenders, it’s essential to do your due diligence. Read reviews, check their reputation, and ensure they are legitimate. While convenient, some might have less personalized customer service compared to a local bank or credit union. However, their competitive rates often make them a strong contender for your Car Loan Max.

Navigating the Application Process for Car Loan Max

Once you’ve done your homework and chosen potential lenders, the application process itself requires careful attention to detail and a strategic mindset.

1. Filling Out the Application Accurately

Accuracy and honesty are paramount when completing loan applications. Provide all requested information truthfully and double-check for any typos or errors. Inconsistencies can raise red flags for lenders and potentially delay or even deny your application.

Make sure your reported income matches your documentation, and your employment history is clear. A complete and accurate application reflects positively on you as a borrower.

2. Understanding Loan Offers

When you receive loan offers, it’s crucial to look beyond just the monthly payment. Scrutinize every detail:

- APR (Annual Percentage Rate): This is the true cost of borrowing, encompassing the interest rate plus any fees. Always compare APRs, not just advertised interest rates.

- Total Loan Cost: Calculate the total amount you will pay over the life of the loan, including principal and all interest. A lower monthly payment over a longer term can often result in a much higher total cost.

- Fees: Look for origination fees, application fees, or prepayment penalties.

- Terms and Conditions: Understand clauses related to late payments, default, and early repayment.

Don’t hesitate to ask questions if anything is unclear. Your goal is to fully comprehend what you’re signing up for.

3. Negotiating Terms (Yes, You Can!)

Many people believe loan terms are non-negotiable, but this is a common misconception. Especially if you have a strong credit score and a pre-approval in hand, you have leverage. Use competing offers to negotiate for a better interest rate or more favorable terms.

Based on my experience, even a quarter-point reduction in APR can save you hundreds, if not thousands, over the life of the loan. Focus on the overall APR and the total cost of the loan, rather than just the monthly payment. Be polite but firm in your requests. Lenders want your business, and they may be willing to sweeten the deal to earn it.

Common Mistakes to Avoid on Your Car Loan Max Quest

Even with thorough preparation, it’s easy to stumble if you’re not aware of common pitfalls. Avoiding these mistakes will keep you firmly on the path to Car Loan Max.

- Not Checking Your Credit: Failing to review your credit reports for errors or understand your score before applying is a critical oversight. It leaves you vulnerable to unfair terms.

- Focusing Only on Monthly Payments: This is perhaps the most frequent mistake. A low monthly payment can disguise a long loan term and a high total interest cost. Always consider the total cost of the loan.

- Ignoring the Total Cost of the Loan: As mentioned, a longer loan term reduces monthly payments but drastically increases the amount of interest you pay over time. Calculate the overall expense.

- Accepting the First Offer: Never take the first loan offer you receive. Shopping around and getting multiple pre-approvals empowers you to compare and negotiate for better terms.

- Getting Emotionally Attached to a Car: Allowing emotions to override financial logic can lead to overspending or accepting unfavorable loan terms. Stick to your budget and walk away if the deal isn’t right.

- Extending Loan Terms Too Much: While a longer term means lower monthly payments, it also means you’ll be "underwater" (owing more than the car is worth) for a longer period, and you’ll pay significantly more in interest.

Life After Approval: Managing Your Car Loan Responsibly

Securing your Car Loan Max is a significant achievement, but the journey doesn’t end there. Responsible loan management is crucial for maintaining your financial health and protecting your credit score.

Making your payments on time, every single month, is paramount. Late payments can incur fees, damage your credit score, and potentially lead to default. Consider setting up automatic payments from your bank account to ensure you never miss a due date.

Understanding your loan statements is also important. These documents detail your payment history, remaining balance, and interest accrued. Regularly reviewing them helps you stay informed about your loan’s progress.

Pro tips: If your credit score significantly improves or interest rates drop after you’ve taken out your loan, consider refinancing. Refinancing can potentially lower your interest rate, reduce your monthly payments, or shorten your loan term, further maximizing your car loan potential even after the initial approval.

Conclusion: Drive Away with Confidence

Achieving "Car Loan Max" is about more than just getting approved for a loan; it’s about making an informed financial decision that serves your best interests. By understanding the key factors that influence your loan terms, diligently preparing, exploring all your lending options, and carefully navigating the application process, you empower yourself to secure the most advantageous financing possible.

Remember, knowledge is your most valuable asset in the world of auto financing. Armed with the insights from this guide, you are well-equipped to take control of your car buying journey, negotiate from a position of strength, and ultimately drive away with confidence, knowing you’ve made the smartest choice for your financial future. Don’t settle for just any loan; strive for your Car Loan Max and enjoy the road ahead. Start planning your optimized auto financing strategy today!