Car Loan On Credit Card: Is It a Smart Move or a Financial Trap?

Car Loan On Credit Card: Is It a Smart Move or a Financial Trap? Carloan.Guidemechanic.com

The dream of a new car often comes with the practical challenge of financing it. For many, the immediate thought turns to traditional auto loans, but in a world brimming with credit options, a different question sometimes arises: "Can I use my credit card for a car loan?" It’s an intriguing idea, especially if you have a high credit limit or a tempting 0% APR offer. However, as an expert in personal finance and an advocate for smart money decisions, I can tell you that while technically possible in some limited scenarios, financing a car purchase with a credit card is almost always a path fraught with significant risks and financial downsides.

This comprehensive guide will meticulously unpack the complexities of using a credit card for a car, exploring the various ways people consider doing it, the hidden costs, the potential dangers, and, most importantly, the far smarter alternatives available. Our goal is to equip you with the knowledge to make an informed, financially sound decision for your next vehicle purchase, steering clear of common pitfalls that can lead to long-term debt.

Car Loan On Credit Card: Is It a Smart Move or a Financial Trap?

The Allure and The Reality: Can You Actually Get a Car Loan on a Credit Card?

The idea of swiping your credit card for a car purchase can seem appealing at first glance. Perhaps you’re chasing rewards points, hoping to leverage a promotional interest rate, or simply looking for a quick and easy financing solution without going through a separate loan application. The allure is understandable; credit cards offer convenience and immediate access to funds.

However, the reality is far more nuanced. While it’s technically possible to put a portion, or even in rare cases, the full price of a car on a credit card, it’s rarely a straightforward or financially advisable decision. Most car dealerships have strict limits on how much they’ll allow you to charge on a credit card, typically capping it at a few thousand dollars for a down payment, if at all. Beyond that, the fundamental structure of credit card debt makes it ill-suited for a large, long-term purchase like a car.

Unpacking the "How": Different Ways People Consider Using Credit Cards for Car Purchases

Let’s delve into the various methods individuals might contemplate when thinking about financing a car with a credit card. Each comes with its own set of mechanisms, limitations, and, crucially, significant financial implications. Understanding these pathways is the first step to recognizing why they are generally not recommended.

Cash Advance

One of the most direct ways to access funds from a credit card is through a cash advance. This involves withdrawing cash directly from your credit card limit, either at an ATM or a bank branch. The thought process here might be to take out a large cash advance and use that money to pay for the car.

Based on my experience, this is perhaps one of the riskiest and most expensive options available. Cash advances typically come with their own set of fees, often 3-5% of the amount withdrawn. What’s more, the interest rate on a cash advance is usually much higher than your standard purchase APR, and interest begins accruing immediately – there’s no grace period. This means you start paying high interest from day one, significantly inflating the total cost of your car.

Balance Transfer (for an existing car loan)

While not for a new car purchase, some might consider using a balance transfer to consolidate an existing car loan onto a credit card. This typically involves moving debt from one credit account (like an existing car loan, if eligible) to a credit card, often to take advantage of a 0% introductory APR offer. The goal here is usually to pay down the principal aggressively during the promotional period without accruing interest.

Common mistakes to avoid here include underestimating the balance transfer fee, which can be 3-5% of the transferred amount. More importantly, if you fail to pay off the entire balance before the promotional period ends, you’ll be hit with the card’s standard, often high, APR on the remaining balance, which can quickly negate any initial savings. Furthermore, most traditional car loans cannot be directly "balance transferred" to a credit card in the same way credit card debt can. This option is mostly relevant if you’re considering moving an existing personal loan that you used for a car.

Direct Purchase (if a dealer accepts)

In rare instances, a car dealership might allow you to put a significant portion, or even the entire purchase price, of a vehicle on your credit card. This is highly uncommon, as dealerships typically face substantial processing fees (interchange fees) from credit card companies, often 2-3% of the transaction value. For a large purchase like a car, these fees can quickly erode their profit margins.

Pro tips from us: Always ask the dealer about their credit card policy upfront. Many will cap the amount you can charge, usually to cover just the down payment or a few thousand dollars, to minimize their fees. Attempting to charge the full amount is almost always met with resistance or additional fees passed on to you, making it an economically unviable option.

Personal Loan from a Credit Card Issuer

It’s crucial to distinguish between using your credit card directly and taking out a personal loan from a credit card issuer. Many major credit card companies also offer personal loans, which are entirely separate products. These loans are typically unsecured, meaning they don’t require collateral like your car, and often come with fixed interest rates and repayment terms.

While a personal loan from a credit card issuer might offer better terms than a cash advance, it’s still a different beast than a traditional auto loan. The interest rates might be more competitive than a credit card’s APR, but they’re often higher than secured car loan rates because the lender has no asset (the car) to seize if you default. This is a distinct financing option, not a "car loan on credit card" in the direct sense.

The Hidden Costs and Significant Risks of Using Credit Cards for Car Financing

While the allure of using a credit card might be strong, the financial reality presents a stark contrast. The risks associated with financing a car, a substantial purchase, on a credit card are numerous and can lead to severe financial distress. Understanding these pitfalls is crucial for making responsible financial decisions.

Sky-High Interest Rates

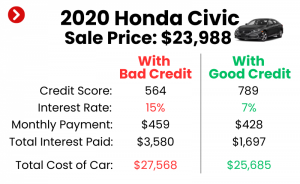

This is arguably the most significant drawback. Credit card interest rates, especially for cash advances, are notoriously high, often ranging from 18% to 25% APR or even more. Compare this to traditional auto loan rates, which for well-qualified buyers can be as low as 3-7% APR. The difference is astronomical.

Over the typical lifespan of a car loan, these high credit card interest rates can add thousands, if not tens of thousands, of dollars to the total cost of your vehicle. You end up paying far more for the car than its sticker price, essentially turning a reasonable purchase into a financial burden.

Punishing Fees

Beyond the exorbitant interest rates, credit cards come with various fees that can quickly add up. As discussed, cash advances incur immediate fees, typically 3-5% of the amount withdrawn. Balance transfers also carry fees, usually 3-5% of the transferred amount. Even if a dealership allows a direct purchase, you might find yourself paying an "administrative fee" to offset their interchange costs.

These fees, while seemingly small percentages, translate into hundreds or even thousands of dollars on a car-sized purchase. They are an immediate cost that reduces the effective value of your funds and contributes to the overall expense of your vehicle.

Damaging Your Credit Score

Financing a large purchase like a car on a credit card can severely impact your credit score, especially if it pushes your credit utilization ratio too high. Credit utilization, which is the amount of credit you’re using compared to your total available credit, is a major factor in your FICO score. Ideally, you want to keep this below 30%.

Charging a significant portion of a car’s price to your credit card could instantly push your utilization to 80%, 90%, or even 100%. This sends a red flag to credit bureaus, signaling higher risk and leading to a substantial drop in your score. A lower credit score can then hinder your ability to secure other loans (like a mortgage) or even impact insurance rates in the future.

Limited Credit Limits

Most personal credit cards have limits that are far below the cost of even a moderately priced used car, let alone a new one. Typical credit limits might range from a few thousand to maybe $20,000 or $30,000 for those with excellent credit. A new car, however, can easily cost $25,000 to $50,000 or more.

This inherent limitation means that using a credit card for a full car purchase is often simply not feasible. You might only be able to cover a small down payment, which then still leaves you needing alternative financing for the bulk of the cost.

No Collateral (for the lender)

Traditional car loans are "secured" loans, meaning the car itself acts as collateral. If you fail to make payments, the lender can repossess the vehicle to recoup their losses. This collateral is why auto loan interest rates are generally much lower than unsecured debt like credit cards.

When you use a credit card for a car, it’s considered unsecured debt. The credit card company has no claim on your car if you default on your payments. This lack of collateral is a primary reason why credit card companies charge such high interest rates – they’re taking on a greater risk.

Short Repayment Terms (implicitly)

While credit cards don’t have fixed repayment terms in the same way an installment loan does, the implicit expectation is to pay off balances quickly to avoid high interest. Many consumers, however, only make the minimum payments on credit card debt.

Based on my experience, making only minimum payments on a large credit card balance for a car can lead to a debt trap that lasts for decades, with the interest paid far exceeding the car’s value. The lack of a structured, manageable payment plan for a large sum is a recipe for long-term financial struggle.

When Might It Seem Like a Good Idea (and why it probably isn’t)

Despite the overwhelming downsides, there are a couple of scenarios where using a credit card for a car might briefly cross someone’s mind. Let’s examine these and understand why even in these situations, caution is paramount.

Emergency Down Payment

Imagine you’ve found the perfect car, but you’re a little short on the ideal down payment, and you need the car immediately. Using a credit card to cover a small portion of the down payment (e.g., $1,000-$2,000) might seem like a quick fix. This allows you to secure the car and potentially get a better interest rate on the remaining financed amount.

However, even in this scenario, it’s still risky. That small credit card balance needs to be paid off extremely quickly – ideally within one or two billing cycles – to avoid significant interest charges. If you can’t pay it off immediately, that "emergency" down payment could become a high-interest burden. Pro tips from us: It’s almost always better to save a little longer or opt for a slightly less expensive car than to incur high-interest credit card debt, even for a down payment.

Leveraging a 0% APR Offer

Perhaps you have a new credit card with a fantastic 0% introductory APR offer for 12, 18, or even 24 months on purchases. The thought might be to put a significant chunk of the car’s cost on this card and pay it off interest-free during the promotional period. This requires extreme financial discipline and a very clear repayment plan.

Common mistakes to avoid here are plentiful. Firstly, you’d still face the credit limit issue – most 0% APR cards won’t have a limit high enough for a full car purchase. Secondly, you must pay off the entire balance before the promotional period expires. If even $1 remains, the deferred interest (in some cases) or the standard high APR will kick in on the remaining balance, often retroactively. This strategy is only viable for a highly disciplined individual who has a guaranteed plan to repay the full amount well before the 0% APR period ends.

Smarter Paths to Your New Ride: Viable Car Financing Alternatives

Given the significant drawbacks of using a credit card for a car, it’s essential to explore the numerous, far more financially sound alternatives. These options are specifically designed for vehicle purchases and offer much better terms and conditions.

Traditional Car Loans

This is the most common and generally the best way to finance a car. Traditional car loans are offered by banks, credit unions, and even through dealership financing departments. They are secured loans, meaning the car serves as collateral, which allows lenders to offer significantly lower interest rates compared to unsecured debt.

Pro Tip: Always shop around for the best interest rates before you visit the dealership. Getting pre-approved from a bank or credit union gives you negotiating power and a benchmark rate to compare against the dealer’s offers. These loans typically come with fixed monthly payments and clear repayment schedules, making budgeting much easier.

Personal Loans (Unsecured)

If you have excellent credit but prefer not to use your car as collateral, an unsecured personal loan can be an option. These loans are typically offered by banks, credit unions, and online lenders. While their interest rates are generally higher than secured auto loans, they are almost always lower than credit card APRs, especially for cash advances.

Personal loans come with fixed interest rates and predictable monthly payments, making them easier to manage than revolving credit card debt. They can be a good alternative if you’re looking to avoid a lien on your vehicle, though you’ll likely pay a premium in interest for that flexibility.

Savings and Down Payments

The most financially sound approach to buying a car is to save up for it, or at least for a substantial down payment. The more cash you put down, the less you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan.

Based on my experience, aiming for a 20% down payment on a new car and 10% on a used car is a wise goal. This not only reduces your loan amount but can also help you avoid being "upside down" on your loan (owing more than the car is worth) early in its life.

Refinancing an Existing Car Loan

This option isn’t for a new car purchase, but it’s relevant if you’re looking to improve the terms of an existing auto loan. If your credit score has improved since you first bought your car, or if interest rates have dropped, refinancing could allow you to secure a lower interest rate or a more favorable repayment term.

Refinancing can significantly reduce your monthly payments or the total interest paid over the loan’s life. It’s a proactive step to manage your existing car debt more effectively, rather than incurring new, high-interest credit card debt.

Pro Tips for Smart Car Financing

Navigating the car buying process can be daunting, but with a few strategic tips, you can ensure you secure the best possible financing and avoid common pitfalls.

- Establish a Realistic Budget: Determine how much you can truly afford, including not just the car payment but also insurance, fuel, maintenance, and registration.

- Save for a Substantial Down Payment: The more you put down, the less you borrow, leading to lower interest costs and monthly payments.

- Check Your Credit Score: Know your credit standing before applying for loans. This helps you understand what rates you qualify for and spot any errors.

- Shop Around for Loan Rates: Don’t just accept the dealer’s first offer. Get pre-approved by several banks and credit unions to compare rates and terms.

- Understand All Terms and Conditions: Read the fine print of any loan agreement. Pay attention to the APR, loan term, total interest paid, and any fees.

- Consider a Used Car: Used cars often represent better value, as the steepest depreciation occurs in the first few years of ownership. This can make financing much more manageable.

Common Mistakes to Avoid When Financing a Car

Even with the best intentions, car buyers can fall into traps that cost them money and create financial stress. Here are some common mistakes to actively avoid:

- Focusing Only on the Monthly Payment: While important, fixating solely on the monthly payment can lead to longer loan terms and higher overall interest paid. Always consider the total cost of the loan.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approved loan makes you vulnerable to less favorable financing offers. Pre-approval gives you leverage.

- Ignoring the Total Cost of the Loan: Always ask for the total amount you will pay over the life of the loan, including all interest and fees. This provides a clearer picture than just the monthly payment.

- Skipping a Down Payment: While possible, not putting money down significantly increases your loan amount, interest paid, and the risk of being upside down on your loan.

- Impulse Buying: Rushing into a car purchase without proper research and financial planning can lead to buyer’s remorse and a costly financing mistake. Take your time.

For more in-depth advice on managing your budget effectively to save for large purchases, check out our detailed guide on .

Conclusion: Drive Smart, Not Sorry

The notion of using a credit card for a car loan, while superficially convenient, is almost universally a poor financial strategy. The astronomical interest rates, punishing fees, potential damage to your credit score, and inherent limitations make it a risky endeavor that can lead to long-term debt and financial strain. As we’ve explored, the "Car Loan On Credit Card" pathway is riddled with more pitfalls than perks.

Instead, prioritize the proven, financially responsible avenues for car financing: traditional auto loans from reputable lenders, personal loans with favorable terms, and, ideally, saving up for a significant down payment. By understanding the true costs and risks, and by exploring smarter alternatives, you can drive away in your new vehicle with peace of mind, knowing you’ve made a decision that supports your financial well-being. Make informed choices, plan ahead, and your journey to car ownership will be a smooth one. For additional insights on consumer finance and making smart borrowing decisions, consider resources like the Consumer Financial Protection Bureau (CFPB) at .