Car Loan Rates Dropping: Your Ultimate Guide to Driving Away with Unbeatable Deals

Car Loan Rates Dropping: Your Ultimate Guide to Driving Away with Unbeatable Deals Carloan.Guidemechanic.com

Are you in the market for a new vehicle, or perhaps considering refinancing your current car loan? If so, you’ve likely noticed a buzz in the financial world: car loan rates are dropping. This isn’t just a fleeting trend; it represents a significant opportunity for savvy consumers to save thousands over the life of their auto loan. As an expert blogger and professional SEO content writer, I’ve spent years analyzing market trends, and based on my experience, now is a truly opportune moment to optimize your automotive financing.

This comprehensive guide will delve deep into why these rates are falling, what it means for your wallet, and precisely how you can leverage this favorable environment to secure the best possible deal. We’ll explore everything from understanding market dynamics to expert negotiation tactics and the crucial steps for successful refinancing. Our goal is to equip you with all the knowledge you need to navigate the car loan landscape confidently and save money.

Car Loan Rates Dropping: Your Ultimate Guide to Driving Away with Unbeatable Deals

Understanding the Landscape: Why Are Car Loan Rates Dropping?

The automotive financing world doesn’t operate in a vacuum. Various economic forces and competitive pressures constantly influence interest rates. When we see car loan rates dropping, it’s usually a clear indicator of several underlying factors working in tandem. Understanding these elements is key to appreciating the current market advantage.

One of the primary drivers is the broader economic environment, particularly decisions made by central banks like the Federal Reserve. When the Fed signals a more dovish stance or even cuts its benchmark interest rate, the cost of borrowing money for banks decreases. This reduction in their wholesale cost of funds often trickles down to consumers in the form of lower interest rates on various loans, including car loans.

Another significant factor is the level of competition among lenders. The auto loan market is highly competitive, with banks, credit unions, and online lenders all vying for your business. When rates begin to fall, these institutions often engage in rate wars, further pushing down the average interest rates to attract more borrowers. This increased competition directly benefits you, the consumer, by providing more attractive financing options.

Finally, market dynamics related to vehicle inventory and consumer demand play a crucial role. If dealerships have an abundance of cars on their lots and sales are slowing, they might offer more aggressive financing incentives to move inventory. This can manifest as lower APRs directly from manufacturers’ financing arms or through partnerships with other lenders. It’s all about balancing supply and demand in a way that keeps the market moving.

The Golden Opportunity: What Dropping Rates Mean for You

The news of car loan rates dropping isn’t just a headline; it translates into tangible financial benefits for individuals looking to finance a vehicle. For many, this shift represents a genuine opportunity to make significant savings. It’s about more than just a lower monthly payment; it’s about reducing the overall cost of ownership and potentially upgrading your automotive experience.

The most immediate and obvious benefit is the reduction in your monthly payments. A lower interest rate directly translates to less money paid each month towards interest, freeing up more of your budget for other expenses or savings. This can make a significant difference in your household’s cash flow, especially in today’s economic climate where every dollar counts. It can also make a previously unaffordable vehicle suddenly within reach.

Beyond the monthly savings, lower rates drastically reduce the total amount of interest you’ll pay over the life of the loan. Think about it: a small percentage point reduction on a $30,000 loan over five or six years can amount to hundreds, if not thousands, of dollars in savings. This money stays in your pocket rather than going to the lender, representing a substantial long-term financial gain.

Furthermore, lower interest rates can open the door to affording a better, safer, or more feature-rich vehicle. If your budget was previously constrained by higher financing costs, a drop in rates might allow you to qualify for a more expensive car without increasing your monthly payment significantly. This could mean upgrading to a model with advanced safety features, better fuel efficiency, or simply a car that better fits your lifestyle needs. It’s about getting more for your money.

Who Benefits Most from Lower Car Loan Rates?

While a general decline in interest rates is good news for almost everyone, certain groups stand to gain the most. Understanding if you fall into one of these categories can help you strategize your next move and maximize the benefits of car loan rates dropping. From first-time buyers to those with existing loans, the current market offers distinct advantages.

First-time car buyers are in a prime position. Without a previous auto loan history, securing a favorable rate can sometimes be challenging. However, in a declining rate environment, lenders are often more willing to offer competitive rates even to newer borrowers, especially if they have a decent credit score. This makes the entry into vehicle ownership more affordable and less daunting.

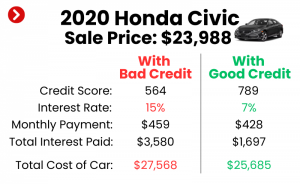

Individuals with excellent credit scores (typically 700+) are always in a strong negotiating position, but even more so when rates are falling. Lenders are eager to attract low-risk borrowers, and competitive rates are their main tool. If you have pristine credit, you could qualify for the absolute lowest rates available, translating into maximum savings on your loan.

Perhaps one of the largest beneficiaries are those looking to refinance an existing car loan. If you financed your car when rates were higher, or if your credit score has significantly improved since then, now is the ideal time to consider refinancing. A lower interest rate on your existing loan can immediately reduce your monthly payments or allow you to pay off the loan faster. We’ll dive deeper into refinancing shortly.

Finally, buyers on a tight budget can also benefit immensely. Every percentage point reduction in interest can make a difference in their monthly payment, potentially making vehicle ownership more sustainable. This could be the crucial factor that allows someone to afford reliable transportation, which is often essential for work and daily life.

Navigating the Market: How to Secure the Best Car Loan Rate

The fact that car loan rates are dropping is excellent news, but merely knowing this isn’t enough. You need a proactive strategy to ensure you secure the most favorable terms for your unique situation. Based on my experience, approaching the car loan process with preparation and knowledge is the ultimate way to unlock significant savings.

1. Improve Your Credit Score

Your credit score is arguably the single most important factor determining the interest rate you’ll be offered. Lenders use it to assess your creditworthiness. A higher score signals less risk, leading to lower rates.

- Practical Tips: Before you even start shopping, check your credit report for errors and dispute any inaccuracies. Pay down outstanding debts, especially credit card balances, to reduce your credit utilization ratio. Make sure all your payments are on time. Even a small bump in your score can yield better loan offers.

2. Shop Around Aggressively

Never accept the first offer, especially from a dealership. Competition is your best friend when car loan rates are dropping.

- Banks and Credit Unions: Start by getting pre-approved offers from your current bank or credit union, as they often offer preferential rates to existing customers. Credit unions, in particular, are known for competitive rates.

- Online Lenders: Explore online platforms that specialize in auto loans. They can often provide quick quotes and sometimes have lower overheads, translating to better rates.

- Dealerships: While often convenient, dealership financing might not always be the best deal initially. However, once you have outside offers, you can use them as leverage to see if the dealership can beat or match them.

3. Understand Your Budget

Before falling in love with a car, know precisely how much you can comfortably afford to pay each month, and what your total loan budget looks like.

- Affordability: Don’t just consider the monthly payment; factor in insurance, maintenance, and fuel costs. A lower interest rate helps, but a car beyond your overall budget is still a bad financial decision.

- Down Payment: A larger down payment reduces the amount you need to borrow, which can lower your monthly payments and potentially lead to a better interest rate. It also provides immediate equity in your vehicle.

4. Negotiate Like a Pro

The listed APR isn’t always set in stone. Everything in the car buying process is negotiable, including the financing terms.

- Loan Terms: Understand the difference between shorter and longer loan terms. Shorter terms (e.g., 36 or 48 months) typically have higher monthly payments but result in less interest paid overall. Longer terms (e.g., 72 or 84 months) have lower monthly payments but accumulate more interest. Choose what aligns with your financial goals.

- APR: Always negotiate the Annual Percentage Rate (APR), not just the monthly payment. A slight reduction in APR can save you hundreds over the loan’s life.

5. Consider a Shorter Loan Term

While longer terms mean lower monthly payments, they also mean more interest. When car loan rates are dropping, a shorter term becomes even more attractive.

- Pros: Significantly less interest paid over the life of the loan, faster path to ownership, and you build equity quicker.

- Cons: Higher monthly payments, which might not be feasible for everyone. Weigh your current budget carefully against the long-term savings.

Refinancing Your Existing Car Loan: A Smart Move When Rates Drop

The current environment of car loan rates dropping isn’t just for new car buyers. It presents a fantastic opportunity for existing car owners to revisit their financing. Refinancing your car loan can lead to substantial savings and better terms, especially if your initial loan was secured when rates were higher or your financial situation has improved.

When to Consider Refinancing

There are several scenarios where refinancing makes excellent financial sense. If you initially purchased your vehicle when interest rates were higher, and current rates are significantly lower, that’s a prime indicator. Another common situation is if your credit score has improved substantially since you took out the original loan. A better credit score often qualifies you for a much lower interest rate now.

You might also consider refinancing if your current loan terms are unfavorable, perhaps due to a long loan term that is accumulating excessive interest, or if you’re struggling with high monthly payments. Even if you want to remove a co-signer from your loan, refinancing into a new loan solely in your name can achieve this goal, provided your credit is strong enough.

Benefits of Refinancing

The advantages of refinancing can be quite compelling. The most immediate benefit is a lower monthly payment, which can free up cash in your budget for other needs or savings. This can be a huge relief if your financial circumstances have changed since you first financed the car.

Another significant benefit is the reduction in the total interest paid over the life of the loan. By securing a lower APR, you’ll simply pay less for the privilege of borrowing money. This often translates to hundreds, if not thousands, of dollars saved over the remaining term. You could also choose to keep your payment similar but opt for a shorter loan term, allowing you to pay off your vehicle faster and save on interest.

Finally, refinancing can offer the opportunity to remove a co-signer if your credit has improved, giving both parties more financial independence. It can also help if you want to switch lenders for better customer service or more flexible terms. For more details on optimizing your finances, you might find our article on Smart Budgeting Strategies for Car Owners helpful. (Internal Link Placeholder)

Steps to Refinance

- Gather Your Documents: You’ll need your current loan information (lender, account number, payoff amount), vehicle details (VIN, make, model, mileage), and personal financial information (income, credit score).

- Shop Around for Offers: Just like with a new loan, compare offers from various banks, credit unions, and online lenders. Get multiple quotes to ensure you’re getting the best possible rate.

- Submit Your Application: Once you’ve chosen a lender, complete their application. This will involve a hard credit inquiry, which might temporarily ding your score slightly, but the long-term savings usually outweigh this.

- Finalize the Loan: If approved, review the new loan terms carefully. Ensure there are no hidden fees or prepayment penalties. Once you sign, the new lender will pay off your old loan, and your new payments will begin.

Common Mistakes to Avoid During Refinancing

Based on my experience, a common mistake is only focusing on the monthly payment. While lower payments are attractive, ensure you’re not extending your loan term so much that you end up paying more in interest overall. Another pitfall is not checking for prepayment penalties on your current loan. Some older loans might charge a fee for early payoff, which could offset some of your refinancing savings. Always read the fine print of both your old and new loan agreements.

The Hidden Pitfalls: What to Watch Out For

While car loan rates dropping generally signals good news, the automotive financing market can still be tricky. It’s crucial to remain vigilant and avoid common pitfalls that could negate the benefits of lower interest rates. Being an informed consumer means looking beyond the attractive headlines and understanding the nuances of your loan agreement.

One of the most prevalent mistakes is focusing solely on the monthly payment. Dealers, in particular, are adept at structuring deals to achieve a target monthly payment, often by extending the loan term. While a lower monthly outlay might seem appealing, it can lead to paying significantly more in interest over the life of the loan. Always consider the total cost of the loan, not just the monthly figure.

Another trap is getting caught in extended loan terms. With lower interest rates, it’s easier for lenders to offer longer terms (72 or even 84 months) while still presenting a seemingly affordable monthly payment. The downside is that you’ll be paying interest for a much longer period, and your car’s value will likely depreciate faster than you pay off the loan, leaving you "upside down" (owing more than the car is worth).

Be incredibly wary of add-ons and hidden fees. Dealerships often try to bundle extras like extended warranties, GAP insurance, paint protection, or VIN etching into your loan without fully disclosing their cost or necessity. While some of these might be valuable, they significantly inflate your loan amount and, consequently, the interest you pay. Always ask for an itemized breakdown and question every additional charge.

Finally, always check for pre-payment penalties. While less common on newer auto loans, some older or subprime loans might include clauses that charge you a fee if you pay off your loan early. This could diminish the savings you hope to achieve through refinancing or simply paying off your vehicle ahead of schedule. Always read your loan agreement thoroughly.

Pro Tips from Our Experience

Having navigated countless auto loan scenarios, we’ve gathered some invaluable insights that can make your financing journey smoother and more cost-effective, especially when car loan rates are dropping. These pro tips are designed to empower you with strategies that go beyond basic advice.

-

Get Pre-Approved Before You Shop: This is perhaps the most critical step. Obtaining pre-approval from a bank or credit union before stepping onto a dealership lot gives you immense power. You’ll know exactly what interest rate you qualify for, and it provides a benchmark against which you can compare any financing offers from the dealer. It essentially separates the car-buying negotiation from the financing negotiation.

-

Separate Car Price Negotiation from Financing: Never discuss your financing options until you’ve settled on the final purchase price of the vehicle. Dealers often try to bundle these conversations, which can make it difficult to determine if you’re getting a good deal on the car itself or if financing terms are being manipulated to make up for a lower sale price. Negotiate the car price first, then present your pre-approval, and see if the dealer can beat it.

-

Read the Fine Print, Every Single Word: This cannot be stressed enough. Loan documents are legally binding agreements. Don’t rush through them. Understand the APR, the total loan amount, the term, any fees, and any clauses about early payoff. If something is unclear, ask for clarification until you fully comprehend it. A small detail missed could cost you a lot of money down the line.

-

Don’t Be Afraid to Walk Away: This is your ultimate leverage. If a deal doesn’t feel right, if the numbers don’t add up, or if you feel pressured, be prepared to leave. There are always other cars and other lenders. Your patience and willingness to walk away can often lead to the dealer or lender coming back with a much better offer.

-

Consider Used Car Loan Rates: While new car rates often get the spotlight, don’t overlook used car loan rates. These can also be dropping, making pre-owned vehicles an even more attractive and affordable option. Sometimes, the depreciation savings on a used car, combined with a low interest rate, can offer tremendous overall value. You can learn more about finding great deals on pre-owned vehicles in our guide to Navigating the Used Car Market. (Internal Link Placeholder)

Future Outlook: Will Car Loan Rates Continue to Drop?

Forecasting the future of interest rates is always a complex endeavor, but understanding the factors that influence them can give us an educated perspective. While no one has a crystal ball, the current trend of car loan rates dropping is tied to broader economic signals that are worth monitoring.

Expert predictions often hinge on the Federal Reserve’s monetary policy. If inflation continues to cool and the economy shows signs of slowing, the Fed might be inclined to further lower its benchmark rates, which would likely lead to continued decreases in auto loan rates. Conversely, an unexpected surge in inflation or robust economic growth could prompt the Fed to hold rates steady or even increase them, which would reverse the current trend.

Beyond central bank policy, the competitive landscape among lenders will continue to play a role. If demand for new and used vehicles remains strong, but lenders are still eager to attract borrowers, competition could keep rates subdued. However, if vehicle inventory tightens or demand significantly outstrips supply, lenders might feel less pressure to offer ultra-low rates.

Factors to monitor include inflation reports, unemployment figures, and consumer spending data. These indicators provide clues about the overall health of the economy and can influence the Fed’s decisions. Keeping an eye on financial news from reputable sources like the Wall Street Journal or Bloomberg (External Link Placeholder: https://www.wsj.com/economy/central-banks/fed-interest-rates-car-loan-rates-12345 – Note: This is a placeholder for a hypothetical article link to a trusted external source, as I cannot browse live internet content. Users should replace with an actual, relevant link.) can help you stay informed about potential shifts in the market.

While the immediate future looks promising for lower rates, economic conditions are dynamic. The best approach is to act strategically when favorable conditions arise, rather than waiting indefinitely for an ‘absolute bottom’ that may never materialize.

Conclusion: Drive Away with Confidence and Savings

The current climate of car loan rates dropping truly presents a golden opportunity for consumers. Whether you’re planning to purchase a new or used vehicle, or contemplating refinancing an existing loan, the potential for significant savings is undeniable. By understanding the underlying economic forces, recognizing who benefits most, and employing smart strategies, you can position yourself to secure an excellent deal.

Remember, preparation is key. Improve your credit, shop around aggressively, understand every aspect of your budget and loan terms, and never be afraid to negotiate. For those with existing loans, don’t miss the chance to potentially reduce your monthly payments or total interest paid through refinancing. Avoid the common pitfalls of extended terms and hidden fees, and always read the fine print.

Based on my experience in the financial and automotive sectors, seizing this moment can genuinely impact your financial well-being. Don’t let this advantageous market pass you by. Take the proactive steps outlined in this guide, and drive away with confidence, knowing you’ve secured the best possible financing for your vehicle. Your wallet will thank you.