Car Loan Singapore: Your Ultimate Expert Guide to Smart Car Financing & Ownership

Car Loan Singapore: Your Ultimate Expert Guide to Smart Car Financing & Ownership Carloan.Guidemechanic.com

Car ownership in Singapore is a unique journey, often seen as a significant milestone and a substantial investment. Unlike many other parts of the world, acquiring a vehicle here involves navigating a complex landscape of Certificate of Entitlement (COE), high taxes, and stringent financing regulations. For most, securing a car loan is an indispensable step towards turning that dream into a reality.

This comprehensive guide is designed to demystify the process of obtaining a car loan in Singapore. We’ll delve deep into everything you need to know, from understanding the regulatory framework to securing the best possible rates, ensuring you make informed decisions every step of the way. Our goal is to equip you with the knowledge to approach car financing with confidence and financial prudence.

Car Loan Singapore: Your Ultimate Expert Guide to Smart Car Financing & Ownership

Understanding the Singaporean Car Market: More Than Just a Purchase

Before diving into loans, it’s crucial to grasp what makes car ownership in Singapore distinct. The government implements various measures to manage vehicle population, most notably through the Certificate of Entitlement (COE) system. A COE is essentially a right to own and use a vehicle for 10 years, and its price can often exceed that of the car itself.

This unique system directly impacts your car loan. When you finance a car, you’re not just borrowing for the vehicle’s Open Market Value (OMV) but also for the hefty COE premium, registration fees, and other associated costs. Therefore, understanding the COE bidding process and its current trends is fundamental to budgeting for your car.

Fluctuations in COE prices can significantly alter the total cost of your car, directly affecting the loan amount you need. A higher COE means a larger principal sum to borrow, which in turn influences your monthly repayments and total interest paid over the loan tenure. Being aware of these market dynamics allows for better financial planning.

Decoding the Different Types of Car Loans in Singapore

Not all car loans are created equal, and understanding the distinctions is vital for making the right choice. In Singapore, the primary categories revolve around the age of the vehicle you intend to purchase. Each type comes with its own set of considerations and eligibility criteria.

1. New Car Loans

These loans are specifically for brand-new vehicles purchased directly from dealerships. They typically offer the most favourable terms, including potentially lower interest rates and the maximum allowed loan tenure. Lenders generally view new cars as lower risk due to their predictable depreciation and condition.

When considering a new car loan, you’ll often find promotional packages from banks working in conjunction with car dealerships. These can sometimes include attractive bundled deals or slightly better rates, though it’s always wise to compare them with independent bank offers. The maximum loan quantum for new cars is often higher, subject to MAS regulations.

2. Used Car Loans

Financing a pre-owned vehicle involves a slightly different set of rules. Used car loans are subject to stricter limits on loan tenure and the maximum loan amount, primarily due to the vehicle’s age. The older the car, the shorter the maximum loan tenure and the lower the loan-to-value (LTV) ratio allowed.

For instance, a car that is already five years old might only qualify for a maximum loan tenure of two years, given the overall seven-year MAS limit. Interest rates for used car loans can also be marginally higher than those for new cars, reflecting the increased risk associated with older vehicles. It’s crucial to assess the car’s remaining COE life when planning a used car loan.

3. Car Loan Refinancing

Refinancing your existing car loan involves taking out a new loan to pay off your current one, often with the aim of securing better terms. This could mean a lower interest rate, reduced monthly payments, or a different loan tenure. It’s a strategy many car owners explore, especially if interest rates have dropped or their credit score has improved since their initial loan.

Based on my experience, refinancing can be particularly beneficial if you initially took out a loan with a high interest rate, perhaps due to a less-than-ideal credit score at the time. However, be mindful of any early repayment penalties on your existing loan, as these can sometimes outweigh the benefits of refinancing. Always calculate the total cost savings before committing.

Key Factors Influencing Your Car Loan in Singapore

Several critical elements will shape the terms and affordability of your car loan. Understanding these factors will empower you to navigate the application process more effectively and potentially secure a more favourable deal.

1. Interest Rates

The interest rate is perhaps the most significant factor determining the total cost of your loan. In Singapore, car loan interest rates are typically expressed as a flat rate, meaning the interest is calculated on the original loan amount throughout the entire tenure. This differs from reducing balance rates seen in home loans, where interest is calculated on the outstanding balance.

Even a seemingly small difference in interest rates can translate into thousands of dollars over a seven-year loan tenure. For example, a 0.5% difference on a $100,000 loan can save you a substantial sum. Always compare rates from multiple lenders and understand whether the rate is fixed for the entire period or subject to change.

2. Loan Tenure

Loan tenure refers to the period over which you will repay your loan. In Singapore, the Monetary Authority of Singapore (MAS) imposes a maximum loan tenure of seven years for car loans. While a longer tenure means lower monthly repayments, it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter tenure will result in higher monthly instalments but significantly reduce the total interest paid. Our professional experience reveals that choosing the shortest tenure you can comfortably afford is often the most financially prudent decision. It helps minimise interest costs and speeds up your path to debt-free car ownership.

3. Down Payment

MAS regulations also stipulate a minimum down payment for car loans, which varies based on the Open Market Value (OMV) of the vehicle. For cars with an OMV of up to $20,000, the maximum loan-to-value (LTV) is 70%, meaning a minimum 30% down payment. For cars with an OMV exceeding $20,000, the maximum LTV is 60%, requiring a minimum 40% down payment.

Making a larger down payment than the minimum required can offer significant advantages. It reduces the principal loan amount, which in turn lowers your monthly repayments and the total interest you’ll pay. Furthermore, a substantial down payment can sometimes make you a more attractive borrower to lenders, potentially unlocking better interest rates.

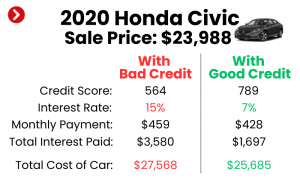

4. Your Credit Score

Your credit score is a crucial indicator of your financial health and repayment capability. Lenders in Singapore, like elsewhere, rely heavily on your credit report from the Credit Bureau Singapore (CBS) to assess your risk profile. A strong credit score signals responsible financial behaviour and can significantly improve your chances of loan approval at favourable rates.

Pro tips from us: Regularly check your credit report for inaccuracies and work on improving your score by paying bills on time, keeping credit utilisation low, and avoiding excessive new credit applications. A good credit history is your passport to better car loan terms.

5. Debt-to-Income (DTI) Ratio

Lenders will also look at your Debt-to-Income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have sufficient income to manage additional debt obligations, making you a more attractive borrower. Lenders typically prefer a DTI ratio below a certain threshold, often around 35-40%.

While there isn’t a strict regulatory limit on DTI for car loans in Singapore, individual banks and financial institutions apply their own internal guidelines. Ensuring your DTI is healthy before applying can boost your approval chances.

6. Vehicle Age

For used cars, the age of the vehicle plays a direct role in determining the maximum loan quantum and tenure. As mentioned, the combined age of the car and the loan tenure cannot exceed a certain limit (typically around 10 years, aligning with COE validity, but lenders often have stricter internal caps like 7 years for the loan itself). An older car will naturally have a shorter maximum loan tenure and potentially a lower LTV, impacting your financing options.

The Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan can seem daunting, but breaking it down into manageable steps makes it straightforward. Follow this process to ensure a smooth and efficient application.

Step 1: Research and Compare Lenders

Before you even decide on a car, research the various car loan providers in Singapore. This includes major banks, in-house financing options from car dealerships, and licensed finance companies. Compare their advertised interest rates, processing fees, repayment flexibility, and customer service. Don’t just look at the headline rate; understand the total cost.

Step 2: Determine Your Affordability

Based on your income, existing debts, and living expenses, calculate how much you can realistically afford for a monthly car loan repayment. Remember to factor in other car ownership costs like insurance, road tax, petrol, parking, and maintenance. Overstretching your budget for a car is a common mistake to avoid.

Step 3: Gather Necessary Documents

Once you’ve narrowed down your choices, prepare all the required documentation. Common documents include your NRIC, proof of income (payslips, income tax statements), bank statements, and details of the car you intend to purchase (if already chosen). For self-employed individuals, more extensive financial records will be needed.

Step 4: Submit Your Application

With your documents in hand, submit your loan application to your chosen lender. This can often be done online, in person at a branch, or through a car dealership’s finance department. Be transparent and accurate with all the information you provide.

Step 5: Await Approval and Review Offer

The lender will assess your application, creditworthiness, and the vehicle details. If approved, they will provide you with a loan offer detailing the interest rate, monthly repayment, total loan amount, and any associated terms and conditions. Review this offer meticulously before signing.

Step 6: Loan Disbursement

Once you accept the offer and sign the loan agreement, the funds will be disbursed. Typically, the loan amount is paid directly to the car dealership or seller, and you will begin your monthly repayments according to the agreed schedule.

Where to Get Your Car Loan in Singapore

In Singapore, you primarily have three avenues for securing a car loan, each with its own set of advantages and disadvantages.

1. Banks

Major banks like DBS, OCBC, and UOB are prominent providers of car loans. They often offer competitive interest rates, transparent terms, and a wide range of financial products. Banks are generally a good option for those with a strong credit history seeking straightforward loan terms.

However, bank approval processes can sometimes be more stringent, and they might require more extensive documentation compared to other options. They typically focus solely on the financing aspect, leaving car purchase negotiations separate.

2. In-House Dealership Financing

Many car dealerships offer their own financing options, often in partnership with specific banks or finance companies. This can be very convenient, as the entire purchase and financing process is handled under one roof. Dealerships might also offer special promotions or bundled deals, especially for new cars.

A common mistake to avoid, based on my experience, is accepting the first financing offer from a dealership without comparing it to external bank offers. While convenient, dealership rates are not always the most competitive. Always do your due diligence and compare.

3. Licensed Finance Companies

Beyond traditional banks, there are licensed finance companies in Singapore that specialise in vehicle financing. These companies can sometimes be more flexible with their lending criteria, particularly for used cars or applicants who might not meet strict bank requirements.

However, the trade-off for this flexibility can sometimes be slightly higher interest rates or different terms compared to major banks. It’s crucial to ensure any finance company you consider is licensed by MAS to protect your interests.

MAS Regulations on Car Loans in Singapore: What You Must Know

The Monetary Authority of Singapore (MAS) plays a pivotal role in regulating car loans to promote financial prudence and stability. These regulations are designed to prevent over-leveraging and ensure borrowers can comfortably manage their repayments. Understanding these rules is not just good practice; it’s essential for any car buyer.

1. Loan-to-Value (LTV) Limits

MAS imposes strict Loan-to-Value (LTV) limits, which determine the maximum percentage of the car’s purchase price (including COE) that you can borrow.

- For cars with an Open Market Value (OMV) of $20,000 or less, the maximum LTV is 70%. This means you must make a minimum down payment of 30%.

- For cars with an OMV above $20,000, the maximum LTV is 60%. This requires a minimum down payment of 40%.

These limits directly impact how much upfront cash you need. The higher the OMV of your desired car, the larger your initial cash outlay will be. These regulations aim to ensure borrowers have a significant stake in their purchase, reducing default risks.

2. Loan Tenure Limit

MAS also caps the maximum loan tenure for car loans at seven years. This applies to all new and used car loans. This regulation ensures that borrowers do not stretch their repayment period excessively, which would lead to higher total interest paid and potentially greater exposure to financial market changes.

For used cars, it’s important to remember that this seven-year limit is often combined with the car’s age. For instance, if you’re buying a five-year-old car, your maximum loan tenure might effectively be shorter than seven years, depending on the lender’s internal policies and the car’s remaining COE life.

These regulations are crucial for maintaining a healthy and sustainable car market. They protect consumers from taking on unmanageable debt and encourage responsible borrowing. For official details on these regulations, you can always refer to the Monetary Authority of Singapore (MAS) website. (External link example)

Calculating Your Car Loan: Beyond the Monthly Payment

While the monthly instalment is often the first number car buyers look at, it’s only one piece of the puzzle. A truly smart financial decision requires a holistic view of all costs involved.

Start by using online car loan calculators, which are widely available on bank websites and financial portals. Input the loan amount, interest rate, and tenure to get an estimate of your monthly repayment and the total interest over the loan period. This helps you compare different scenarios quickly.

However, don’t stop there. Factor in all upfront costs not covered by the loan, such as a larger-than-minimum down payment, car insurance, road tax, and any initial servicing costs. Then, consider ongoing expenses like petrol, parking fees, maintenance, and potential repair costs. A comprehensive budget ensures no hidden surprises.

Smart Strategies for Securing the Best Car Loan in Singapore

Navigating the car loan landscape can be challenging, but with the right strategies, you can significantly improve your chances of securing the most favourable terms.

-

Improve Your Credit Score: As highlighted earlier, a strong credit score is your biggest asset. Pay all your bills on time, keep your credit utilisation low, and avoid opening too many new credit accounts simultaneously. This demonstrates financial responsibility to lenders.

-

Save for a Larger Down Payment: Exceeding the minimum MAS down payment requirements can lower your overall loan amount, reduce your monthly instalments, and decrease the total interest paid. It also signals to lenders that you are a serious and financially stable borrower.

-

Shop Around and Compare: Never settle for the first loan offer you receive. Contact multiple banks and finance companies, and get quotes from each. Compare not just the interest rates but also any processing fees, early repayment penalties, and other terms.

-

Negotiate: Don’t be afraid to negotiate, especially if you have a strong credit profile. Some lenders might be willing to offer slightly better rates or waive certain fees to win your business, particularly if you present a competing offer.

-

Understand the Fine Print: Before signing any loan agreement, read and understand every clause. Pay close attention to terms regarding late payment fees, early repayment penalties, and what happens in case of default. Clarity prevents future disputes.

-

Consider Your Financial Health: A car is a depreciating asset and a significant liability. Ensure that taking on a car loan aligns with your broader financial goals and does not compromise your ability to save, invest, or handle unexpected expenses. For more tips on managing your personal finances, check out our article on . (Internal link example)

Common Mistakes to Avoid When Taking a Car Loan

Even the most informed buyers can sometimes fall prey to common pitfalls. Being aware of these can save you a lot of headache and money.

-

Not Understanding the Total Cost: Focusing solely on the monthly repayment without considering the total interest paid over the tenure, upfront costs, and ongoing expenses is a major oversight. This can lead to financial strain down the line.

-

Ignoring Your Credit Score: Many buyers neglect their credit health until they need a loan. A poor credit score can result in higher interest rates or even loan rejection, costing you more in the long run.

-

Rushing into a Decision: The excitement of buying a car can lead to hasty decisions regarding financing. Take your time to compare offers, understand the terms, and ensure it fits your budget comfortably.

-

Not Comparing Offers: Assuming all lenders offer similar rates is a costly mistake. Even a small difference in interest can accumulate significantly over several years. Always get at least three to four quotes.

-

Overstretching Your Budget: Buying a car that is beyond your financial means just because you can secure a loan for it is a recipe for financial stress. Remember, the loan needs to be serviced consistently for years. From years of observing car buyers, this is one of the most frequent pitfalls leading to regret.

Conclusion: Drive Smart, Finance Smarter

Securing a car loan in Singapore is a significant financial commitment that demands careful consideration and thorough research. By understanding the unique market dynamics, the different types of loans available, and the crucial factors that influence your terms, you can navigate the process with confidence.

Remember to leverage smart strategies like improving your credit score and shopping around for the best rates, while vigilantly avoiding common mistakes. Your goal should not just be to get a car loan, but to secure the most advantageous Car Loan Singapore has to offer, aligning with your financial well-being. With this comprehensive guide, you are now well-equipped to make informed decisions and embark on your car ownership journey with peace of mind. Drive smart, finance smarter!