Car Loan Through Bank Or Dealer: Your Ultimate Guide to Smart Car Financing

Car Loan Through Bank Or Dealer: Your Ultimate Guide to Smart Car Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but the process of securing the right financing can often feel daunting. One of the biggest questions car buyers face is whether to get a car loan through a traditional bank or opt for dealer financing. This isn’t just a minor detail; it’s a pivotal financial decision that can save or cost you thousands of dollars over the life of your loan.

As an expert in automotive finance, I’ve guided countless individuals through this complex landscape. My goal today is to provide you with a super comprehensive, in-depth guide that demystifies car loans, empowering you to make the best choice for your financial future. We’ll explore every facet of car financing, ensuring you understand the pros and cons of both avenues.

Car Loan Through Bank Or Dealer: Your Ultimate Guide to Smart Car Financing

Understanding the Fundamentals of Car Loans

Before we dive into the specifics of bank versus dealer financing, let’s establish a solid understanding of what a car loan entails. At its core, a car loan, also known as an auto loan, is borrowed money specifically for the purchase of a vehicle. You agree to repay this money, plus an additional cost called interest, over a set period.

The three primary components of any car loan are the principal, the interest rate (often expressed as APR), and the loan term. The principal is the amount of money you borrow to buy the car. The interest rate is the percentage charged by the lender for the use of their money, and the loan term is the duration, typically in months, over which you will repay the loan.

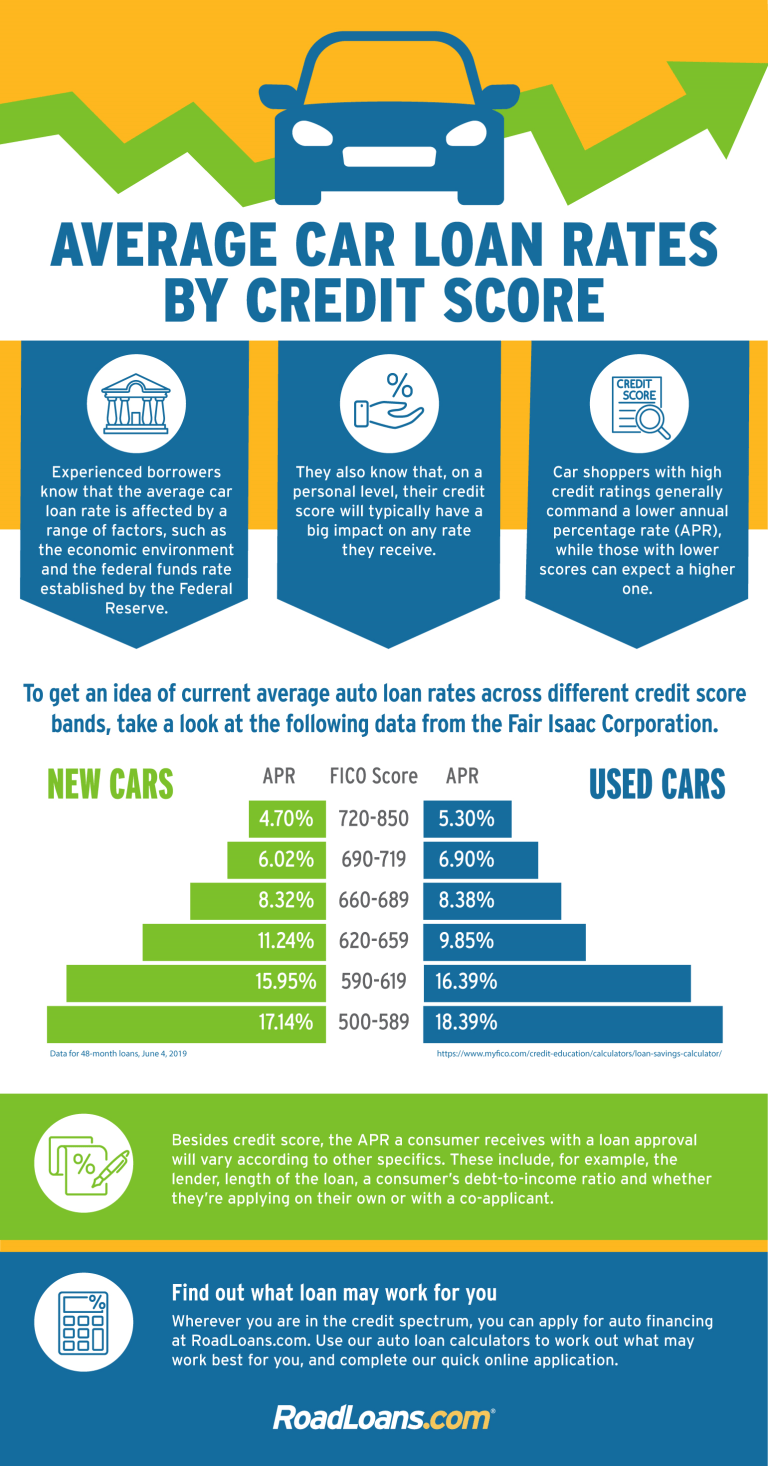

Your credit score plays an absolutely crucial role in determining the interest rate you’ll be offered. A higher credit score signals less risk to lenders, often resulting in more favorable loan terms and lower monthly payments. Conversely, a lower credit score might lead to higher interest rates, increasing the overall cost of your car.

The Bank Loan Advantage: Going Independent for Better Control

Many financial experts, myself included, often recommend exploring bank loans as your first step in the car buying journey. This proactive approach can give you a significant advantage, transforming you into a more powerful negotiator at the dealership. Securing pre-approval from a bank or credit union before you even step foot on a car lot is a game-changer.

Proactive Approach: Getting Pre-Approved

Getting pre-approval for a car loan means a bank or credit union has reviewed your financial information and tentatively agreed to lend you a specific amount of money at a particular interest rate. This isn’t a final loan, but it gives you a concrete offer in hand. You’ll know exactly how much you can afford, what your potential monthly payments will look like, and the interest rate you qualify for.

This pre-approval acts like a golden ticket. It sets a baseline for comparison and gives you immense confidence. You’re no longer just dreaming about a new car; you have a clear financial path laid out.

Potential for Better Rates and Transparency

Based on my experience, banks and credit unions often offer more competitive interest rates (APR) compared to dealer financing. This is primarily because their core business is lending, and they have a broader range of financial products and services. They compete fiercely for your business, which can translate into better deals for you.

Dealing directly with a bank also typically offers greater transparency. You’re working solely with the lender, making it easier to understand all the fees, terms, and conditions without the added layer of the dealership. This direct communication can prevent misunderstandings and ensure you’re fully aware of your financial commitment.

Empowering Your Negotiation

Walking into a dealership with a pre-approved bank loan means you’re effectively a cash buyer. You’ve already secured your financing, so your focus can solely be on negotiating the best possible price for the car itself. This separates the car price negotiation from the financing negotiation, simplifying the process and often leading to a better overall deal.

Dealers know that if you have your own financing, they can’t mark up the interest rate to increase their profit. This puts the ball firmly in your court, allowing you to drive a harder bargain on the vehicle’s sticker price. It’s a powerful position to be in.

Common Mistakes to Avoid with Bank Loans

A common mistake when pursuing a bank loan is only checking with one institution. Always compare offers from at least three different banks or credit unions. Even a half-percentage point difference in your APR can save you hundreds, if not thousands, over the loan term. Don’t settle for the first offer; shop around diligently.

Another pitfall is not fully understanding the pre-approval letter. Make sure you know if it’s a "soft" or "hard" credit pull and if the rate is truly locked in. Some pre-approvals are subject to final verification, so read all the fine print carefully.

The Dealer Financing Convenience: Your One-Stop Shop

While independent bank loans offer significant advantages, dealer financing remains a popular option for many car buyers, primarily due to its convenience. Dealers often act as intermediaries, connecting you with multiple lenders they partner with. This can streamline the entire car buying process into a single, efficient transaction.

Simplicity and Speed

One of the biggest draws of dealer financing is its sheer simplicity. You select your car, fill out one application, and the dealership handles the rest. They submit your information to various lenders in their network, often providing you with multiple financing options within minutes. This can be incredibly appealing if you’re short on time or prefer a less hands-on approach to securing your loan.

The quick approval process means you can often drive off the lot with your new car the same day. For buyers who value speed and minimal paperwork, this seamless experience is a major benefit.

Special Offers and Manufacturer Incentives

Dealers sometimes offer promotional interest rates or special financing deals, especially on new car models. These incentives might include 0% APR for a limited term or significantly reduced rates, directly from the manufacturer. These offers are usually designed to boost sales of specific models and can be incredibly attractive if you qualify.

Such promotional rates can be difficult to find through traditional banks. If you have excellent credit, you might be able to take advantage of these deals, potentially saving a substantial amount on interest.

Convenience and Building Relationships

Having all your paperwork handled at one location – from the purchase agreement to the car loan documents – simplifies the process immensely. You don’t have to juggle appointments with different banks or coordinate between multiple entities. This integrated approach saves time and reduces stress.

Furthermore, building a relationship with a dealership can sometimes lead to future benefits, such as preferred service appointments or special discounts on maintenance. While not a primary factor for everyone, it’s an added layer of convenience for some buyers.

Pro Tips for Dealer Financing

To ensure you’re getting a good deal with dealer financing, always ask the dealer to show you all the financing options they received from their lenders, not just the one they recommend. This forces transparency and allows you to compare rates. Also, be prepared to walk away if the dealer’s financing terms are significantly worse than what you could get independently.

It’s crucial to understand that while a dealer can offer attractive rates, they also have a profit motive. They might mark up the interest rate they receive from their lending partners to earn a commission. This is a common practice, so always be vigilant and compare their offer with your pre-approved rate.

Deep Dive: Key Factors to Consider When Choosing Your Path

Making an informed decision about your car loan requires a thorough evaluation of several critical factors. Each element plays a significant role in the total cost and overall experience of borrowing money for your vehicle.

Interest Rates (APR): The True Cost of Borrowing

The interest rate, specifically the Annual Percentage Rate (APR), is arguably the most important factor. It represents the total cost of borrowing, including certain fees, expressed as a yearly percentage. A lower APR means less money paid in interest over the life of the loan.

Based on my experience, even a small difference in APR can have a substantial impact. For example, on a $30,000 loan over five years, a 0.5% difference in APR could mean hundreds of dollars in extra payments. Always focus on the APR, not just the monthly payment, to understand the true cost.

Loan Terms: Balancing Payments and Total Cost

The loan term dictates how long you have to repay the loan. Common terms range from 36 to 84 months. A shorter loan term typically means higher monthly payments but less interest paid overall. Conversely, a longer term reduces your monthly payments but increases the total interest you’ll pay.

It’s a delicate balance. While a lower monthly payment might seem appealing, extending your loan term too much can lead to "upside down" equity (owing more than the car is worth) and significantly higher total costs. Pro tips from us: Aim for the shortest loan term you can comfortably afford without straining your budget.

Your Credit Score: The Ultimate Deciding Factor

As mentioned earlier, your credit score is paramount. Lenders use it to assess your creditworthiness and determine the risk associated with lending you money. A strong credit history and a high score (generally 700+) will open doors to the most competitive interest rates and favorable loan terms.

If your credit score isn’t where you’d like it to be, taking steps to improve it before applying for a car loan can save you a significant amount. For a deeper dive into managing your credit score, check out our comprehensive guide on .

Down Payment: Reducing Your Burden

Making a substantial down payment is one of the smartest financial moves you can make when buying a car. A larger down payment reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan.

Furthermore, a significant down payment helps you build equity in the car faster, reducing the risk of being upside down on your loan. It also signals financial stability to lenders, potentially qualifying you for better rates. Aim for at least 10-20% of the car’s purchase price, if possible.

Fees and Charges: Unmasking Hidden Costs

Beyond the interest rate, be vigilant for various fees and charges that can inflate the total cost of your loan. These can include origination fees, documentation fees, processing fees, or even prepayment penalties. Some lenders charge a fee if you pay off your loan early, so always ask about this.

Common mistakes to avoid are signing loan documents without thoroughly reviewing every line item. Demand a clear breakdown of all costs. Transparency is key, and if a lender or dealer is hesitant to provide it, consider that a red flag.

Flexibility: Prepayment and Refinancing Options

Consider the flexibility of the loan. Can you make extra payments without penalty? Is there an option to refinance the loan later if interest rates drop or your credit score improves? These flexibilities can offer significant advantages down the line.

A good loan agreement will not penalize you for wanting to pay it off early. Ensure you understand the terms regarding early repayment before you commit.

The Pre-Approval Power Play: A Strategy for Success

Securing pre-approval is more than just getting an estimate; it’s a strategic move that fundamentally shifts the power dynamic in your favor. It transforms you from a hopeful shopper into a qualified buyer, armed with concrete financial terms.

What Pre-Approval Means in Practice

When you get pre-approved, a bank or credit union performs a credit check and assesses your financial health. They then provide you with a written offer stating the maximum loan amount, the interest rate (APR), and the loan term they are willing to extend to you. This is a real, albeit conditional, offer.

This means you know your budget before you start looking at cars. You won’t fall in love with a vehicle only to find out you can’t afford it or the financing is too expensive.

How to Get Pre-Approved

The process is straightforward. You can apply online, over the phone, or in person at banks, credit unions, and even online lenders. You’ll typically need to provide personal information, employment details, income verification, and consent for a credit check.

Credit unions, in particular, often offer highly competitive rates due to their member-focused structure. It’s always worth exploring their options.

Benefits of Pre-Approval: Confidence and Negotiation

The benefits of pre-approval are multifaceted. Firstly, it provides immense confidence. You know your spending limit, preventing impulse decisions. Secondly, it gives you incredible negotiating power. When a dealer asks about your financing, you can confidently state you have your own financing secured.

This allows you to focus solely on negotiating the car’s purchase price. You can compare the dealer’s financing offer directly against your pre-approval, often forcing the dealer to match or beat your existing rate if they want your business.

Common Mistakes to Avoid with Pre-Approval

A common mistake is assuming pre-approval is a guarantee. It’s usually conditional, meaning the final approval depends on the specific car you choose meeting the lender’s criteria (e.g., age, mileage for a used car) and a final review of your documents. Always confirm the conditions.

Another error is letting multiple pre-approval inquiries impact your credit score. While multiple hard inquiries within a short period (typically 14-45 days, depending on the credit bureau) for the same type of loan are often grouped as one, spreading them out too much can lower your score. Get all your pre-approvals within a focused timeframe.

Negotiation Strategies for Both Scenarios

Mastering the art of negotiation is crucial, regardless of whether you choose a bank loan or dealer financing. Your approach, however, will differ slightly.

Negotiating with a Bank Loan in Hand

When you arrive at the dealership with a pre-approved bank loan, your negotiation strategy becomes incredibly focused: negotiate only the price of the car. Since your financing is already secured, you’re effectively a cash buyer in the dealer’s eyes.

Resist any attempts by the dealer to shift the conversation to financing until you’ve agreed on a final purchase price for the vehicle. If they offer to beat your pre-approved rate, that’s a bonus, but it should never be the primary negotiation point initially.

Negotiating with Dealer Financing

If you’re relying on dealer financing, you’ll need to negotiate both the car’s price and the loan terms simultaneously, or sequentially. Pro tips from us: Always try to settle on the car’s price first, before discussing trade-ins or financing. Separating these elements prevents the dealer from shifting numbers around to make it seem like you’re getting a good deal on one aspect while losing out on another.

Once the car price is fixed, then you can discuss the interest rate, loan term, and any additional fees. Be firm, compare their offers to what you might expect based on your credit score, and don’t be afraid to walk away if the terms aren’t favorable.

Beyond the Loan: Other Critical Considerations

Your car buying journey extends beyond just the car loan. Several other factors deserve your attention to ensure a smooth and financially sound purchase.

Insurance Implications

The type of car you buy and how you finance it will directly impact your auto insurance premiums. Lenders typically require full coverage insurance (collision and comprehensive) for the duration of your loan to protect their asset. This can be more expensive than liability-only coverage.

Always get insurance quotes for specific models before finalizing your purchase. A higher insurance premium can significantly increase your overall monthly car expenses.

Warranty Options

New cars come with a manufacturer’s warranty, but for used car purchases, extended warranties or service contracts are often offered by dealers. While these can provide peace of mind, they also add to the total cost. Carefully evaluate if an extended warranty is necessary and if the coverage justifies the price.

For more advice on inspecting used cars, our article on offers invaluable guidance.

Long-Term Financial Planning

Consider how this car loan fits into your broader financial picture. Does it align with your budget? Will it hinder other financial goals like saving for a home or retirement? A car is a depreciating asset, so ensure you’re not overextending yourself for a vehicle that will lose value over time.

Think about the total cost of ownership, including fuel, maintenance, and insurance, not just the monthly loan payment.

Which Path Is Right For You? A Decision Matrix

The choice between a car loan through bank or dealer ultimately depends on your individual circumstances, financial discipline, and comfort with negotiation.

| Feature | Bank Loan (Independent Financing) | Dealer Financing (Captive/Partner Lenders) |

|---|---|---|

| Control | High; direct communication with lender, pre-approval power. | Moderate; dealer acts as intermediary, less direct control. |

| Interest Rates | Often more competitive due to direct competition. | Potentially higher (dealer markup) or lower (special manufacturer offers). |

| Convenience | Requires separate application process; more steps. | One-stop shop; quick approval at dealership. |

| Transparency | Generally high; all terms from one lender. | Can be complex; multiple lenders, potential for hidden fees. |

| Negotiation | Focus solely on car price; stronger buyer position. | Negotiate car price and loan terms simultaneously. |

| Speed | Pre-approval takes time; final loan paperwork separate. | Can be very fast; drive away same day. |

| Best For | Savvy shoppers, those with good credit, who value control and savings. | Buyers prioritizing convenience, those with excellent credit for promos. |

If you have excellent credit, are comfortable with a bit more legwork, and want to ensure you get the absolute best rate, pursuing a bank loan first is usually the smartest move. It empowers you with a strong negotiating position.

However, if you prioritize convenience, have a tight timeline, or qualify for a compelling manufacturer’s promotional APR, then dealer financing might be a viable and attractive option. Just be sure to do your homework and compare all offers diligently.

Conclusion: Drive Away with Confidence and the Right Loan

Navigating the world of car loans doesn’t have to be a confusing ordeal. By understanding the distinct advantages and disadvantages of securing a car loan through bank or dealer, you equip yourself with the knowledge needed to make a smart, informed decision. Remember, the ultimate goal is to find financing that fits your budget, offers competitive terms, and aligns with your financial goals.

Whether you choose the independent route of a pre-approved bank loan or the streamlined process of dealer financing, the key is thorough research, diligent comparison, and a willingness to negotiate. Don’t rush the process; take your time to evaluate all your options. To understand your rights as a consumer and get unbiased information on financial products, resources like the Consumer Financial Protection Bureau (CFPB) or the Federal Trade Commission (FTC) are excellent starting points. For example, the FTC provides valuable information on car buying and financing at .

By taking these steps, you won’t just drive away with a new car; you’ll drive away with confidence, knowing you’ve made a financially sound choice that serves your best interests for years to come. Happy car buying!