Car Loan vs. Cash: The Ultimate Guide to Buying Your Next Vehicle

Car Loan vs. Cash: The Ultimate Guide to Buying Your Next Vehicle Carloan.Guidemechanic.com

Buying a car is a significant financial decision, often ranking as one of the largest purchases most people make after a home. The excitement of a new set of wheels can quickly turn into a headache if you don’t approach the payment method strategically. Should you drain your savings and pay with cash, or take out a car loan and spread the cost over time?

This isn’t just a simple yes or no question; it’s a nuanced financial puzzle with implications for your budget, credit, and long-term financial health. As an expert blogger and professional SEO content writer, I’ve seen countless individuals grapple with this very choice. Based on my experience, understanding the intricacies of both options is paramount to making a smart decision.

Car Loan vs. Cash: The Ultimate Guide to Buying Your Next Vehicle

In this comprehensive guide, we’ll dive deep into the world of car purchases, meticulously comparing the advantages and disadvantages of paying with cash versus financing with a car loan. Our goal is to equip you with the knowledge and insights needed to confidently choose the path that best aligns with your personal financial situation and goals. Let’s get started and demystify this critical decision.

The Allure of Cash: A Deep Dive into Upfront Payment

Paying for a car with cash feels incredibly liberating. There’s a certain satisfaction that comes from handing over a check or making a wire transfer and knowing that vehicle is 100% yours, free and clear. This approach appeals to many for its simplicity and the immediate sense of ownership it provides.

However, the decision to pay cash is more than just an emotional one; it has tangible financial benefits and potential drawbacks that warrant careful consideration. Let’s explore what it truly means to buy a car with your hard-earned cash.

Pros of Paying with Cash

Opting to pay cash for your vehicle brings a host of compelling advantages, primarily centered around financial freedom and reduced long-term costs. Many financial experts, including myself, often lean towards this method when it’s genuinely feasible without compromising other critical financial aspects.

1. No Interest Payments, Significant Savings

This is arguably the most significant advantage of paying with cash. When you take out a car loan, you’re essentially renting money from a lender, and that rental fee is called interest. Over the life of a typical 3-5 year car loan, these interest payments can add up to thousands of dollars, significantly increasing the total cost of your vehicle.

By paying cash, you completely bypass these interest charges. The price you agree upon with the dealer is the final price you pay, excluding taxes and fees. This direct saving goes straight back into your pocket, making the car a much more affordable purchase in the long run.

2. No Monthly Payments, Financial Freedom

Imagine not having a car payment looming over your head every month. This newfound financial freedom can be incredibly powerful. It frees up a significant portion of your monthly budget, allowing you to allocate those funds towards other financial goals, such as saving for a down payment on a house, investing, or building your emergency fund.

This reduction in fixed expenses also lowers your overall financial stress. You won’t have to worry about missing a payment or the consequences of late fees, providing a greater sense of security and control over your finances.

3. Immediate Ownership and No Liens

When you pay cash, you immediately become the sole owner of the vehicle. There’s no lienholder listed on your title, meaning no bank or financial institution has a claim on your car. This provides a clear and straightforward ownership experience.

Should you decide to sell the car in the future, the process is much simpler. You don’t need to involve a lender to release the title, making transactions quicker and less complicated.

4. Potential for Better Negotiation

While not always guaranteed, paying cash can sometimes give you a slight edge in negotiations with a dealership. Dealers make money on financing, so they might not prefer cash buyers, but the simplicity of the transaction can sometimes lead to a quicker sale for them.

In certain scenarios, particularly with private sellers, cash is king. It simplifies the transaction immensely, and the immediate nature of the payment can sometimes be leveraged for a slightly better price.

5. Avoidance of Debt

In a world where many people are burdened by various forms of debt, avoiding another significant debt obligation is a huge win. A car loan is a liability that ties up your future income and can impact your debt-to-income ratio.

By paying cash, you keep your personal balance sheet cleaner, which can be beneficial if you plan to apply for other loans (like a mortgage) in the near future. It aligns with a debt-free lifestyle, which many strive for.

Cons of Paying with Cash

While the benefits of cash are compelling, it’s not always the best option for everyone. There are significant downsides that could potentially put your financial well-being at risk if not carefully considered.

1. Depletion of Savings/Emergency Fund

The most critical drawback of paying cash for a car is the potential to deplete your hard-earned savings. For many, a car purchase represents a substantial sum of money. Using all or most of your liquid assets can leave you financially vulnerable in the face of unexpected emergencies.

Pro tips from us: Always maintain a robust emergency fund – typically 3-6 months of living expenses – separate from your car-buying fund. Draining this critical safety net for a car is a common mistake to avoid.

2. Opportunity Cost of Cash

Every dollar you spend on a car is a dollar that can’t be used for something else. This is known as opportunity cost. If you have the option to invest that cash where it could earn a higher rate of return than the interest rate on a car loan, then paying cash might not be the most financially optimal decision.

For instance, if your car loan rate is 5% but you could invest that money and reasonably expect an 8% return, then financing the car and investing your cash might make more sense. This requires a strong understanding of investment risks and returns.

3. Lack of Credit Building

For younger buyers or those looking to establish or improve their credit score, a car loan can be a valuable tool. Making consistent, on-time payments on a secured loan like a car loan demonstrates financial responsibility and contributes positively to your credit history.

If you pay cash, you miss out on this opportunity to build credit. While not a deal-breaker for those with established credit, it’s a factor to consider for those who need to strengthen their credit profile.

4. Tying Up a Large Sum of Capital

A car is a depreciating asset, meaning its value decreases over time. When you pay cash for a car, you’re essentially tying up a large amount of liquid capital in an asset that is guaranteed to lose value. This cash could potentially be used for other investments that appreciate or provide greater financial returns.

Consider how much liquidity you need for other life events or investments. Is tying up tens of thousands of dollars in a depreciating asset the best use of your capital at this moment?

When Cash is King

Based on my experience, paying cash is the optimal choice when:

- You have ample savings beyond your emergency fund and other short-term financial goals.

- The interest rate on a car loan is higher than what you can reasonably earn on your investments.

- You prioritize being debt-free and the psychological comfort that comes with it.

- You’re buying an older, less expensive used car where financing costs might disproportionately add to the total price.

Navigating the World of Car Loans: A Comprehensive Look

For many, financing a car through a loan is the most practical and common method of purchase. It allows individuals to acquire a necessary vehicle without liquidating their entire savings or waiting years to save up the full amount. However, entering into a loan agreement requires a clear understanding of its structure, costs, and commitments.

Let’s explore the advantages and disadvantages of taking out a car loan, offering a balanced perspective for your decision-making process.

Pros of Taking a Car Loan

Car loans, when managed responsibly, can be a powerful financial tool that offers flexibility, preserves capital, and can even bolster your financial standing. They are a lifeline for many who need reliable transportation but don’t have the immediate cash reserves.

1. Preservation of Savings/Emergency Fund

One of the most compelling reasons to take out a car loan is the ability to preserve your savings. Instead of depleting your emergency fund or investment accounts, you can make a down payment (if desired) and spread the remaining cost over several years. This ensures you maintain a financial safety net for unexpected life events, which is crucial for financial stability.

Having readily accessible cash provides peace of mind and the ability to handle emergencies without resorting to high-interest credit cards or further loans. This is a critical aspect of sound financial planning.

2. Opportunity for Higher Return Investments

As touched upon earlier, financing your car frees up capital that can potentially be invested elsewhere. If you have investment opportunities that offer a higher rate of return than the interest rate on your car loan, then financing could be a financially savvy move. This concept is often referred to as "arbitrage" in a simplified context.

For example, if your car loan carries a 4% interest rate, but you have an investment vehicle (like a diversified stock portfolio or real estate) that historically yields 7-10% annually, it makes more sense to invest your cash and pay the car loan. This strategy, however, requires comfort with investment risk.

3. Building Credit History

For individuals with limited or developing credit history, a car loan can be an excellent way to build a strong credit profile. Making consistent, on-time monthly payments on a car loan demonstrates to credit bureaus that you are a reliable borrower. This positively impacts your credit score.

A good credit score is invaluable, opening doors to better interest rates on future loans (mortgages, personal loans) and even impacting insurance premiums or rental applications. Responsible loan management is a cornerstone of good credit.

4. Ability to Afford a Newer/More Reliable Car

Let’s be realistic: not everyone can afford to pay cash for a brand-new or even a late-model used car. A car loan makes these vehicles accessible, allowing buyers to get into a safer, more reliable, and often more fuel-efficient car than they could afford outright with cash.

This can be particularly important for families or individuals who rely heavily on their vehicle for work or daily commutes. Investing in a more dependable car can reduce maintenance headaches and provide greater peace of mind.

5. Fixed Monthly Payments for Budgeting

Most car loans come with fixed monthly payments, meaning the amount you pay each month remains consistent throughout the loan term. This predictability is a huge advantage for budgeting. You know exactly how much you need to allocate for your car payment each month, making financial planning much simpler.

This contrasts with variable expenses and helps you maintain control over your cash flow. It allows for better long-term financial planning and goal setting.

Cons of Taking a Car Loan

While beneficial in many respects, car loans come with their own set of challenges and financial obligations. It’s crucial to be aware of these potential pitfalls before committing to a financing agreement.

1. Interest Payments (Adds to Total Cost)

The most obvious downside to a car loan is the interest. While you get to drive the car now, you end up paying more than its sticker price over the loan’s duration. This additional cost can be substantial, especially with longer loan terms or higher interest rates.

It’s vital to calculate the total cost of the loan, including all interest, before signing. Don’t just focus on the monthly payment; understand the true financial commitment you’re making.

2. Monthly Payment Commitment (Financial Burden)

A car loan introduces a recurring fixed expense into your budget. This monthly payment can feel like a significant burden, especially if your income is unstable or if you encounter unexpected financial difficulties. Missing payments can lead to late fees, damage to your credit score, and even repossession.

Before taking on a loan, carefully assess your ability to comfortably make these payments throughout the entire loan term, even if your financial circumstances change slightly.

3. Debt Obligation

A car loan is a form of debt, and carrying debt can have psychological and financial consequences. It ties up a portion of your future income and can limit your flexibility for other financial endeavors. Your debt-to-income ratio increases, which can affect your ability to qualify for other loans in the future.

Being mindful of your overall debt burden is crucial. While some debt is manageable, too much can lead to financial strain and reduced options.

4. Risk of Negative Equity

Negative equity, or being "upside down" on your loan, occurs when you owe more on your car than its current market value. This is a common issue because cars depreciate rapidly, especially in the first few years. If you need to sell the car or it’s totaled in an accident, you could find yourself still owing money to the lender even after the sale or insurance payout.

Common mistakes to avoid are taking a very long loan term (e.g., 72 or 84 months) with a small down payment, as this significantly increases the risk of negative equity. Always consider gap insurance to protect yourself in such scenarios.

5. Loan Application Process and Potential Rejections

Securing a car loan involves an application process that can be time-consuming and sometimes stressful. Lenders will review your credit history, income, and debt-to-income ratio. If your credit score is low or your financial situation is not ideal, you might face higher interest rates or even outright rejection.

This means you might not get the terms you desire, or you might have to settle for a less favorable loan, increasing your overall cost. It’s wise to get pre-approved before heading to the dealership.

When a Car Loan Makes Sense

Based on my experience, taking a car loan is a smart move when:

- You need to preserve your emergency fund and other liquid assets.

- You have a good to excellent credit score, qualifying you for low interest rates.

- You can comfortably afford the monthly payments without straining your budget.

- You want to build or improve your credit history.

- You have investment opportunities that promise returns higher than your loan’s interest rate.

Key Factors to Consider Before Deciding

The choice between a car loan and cash isn’t one-size-fits-all. It requires a thoughtful assessment of your personal financial landscape and priorities. Here are several critical factors you must consider before making your final decision.

1. Your Financial Health

Before anything else, take a hard look at your overall financial situation. Do you have a stable income? How large is your emergency fund? What other debts do you currently carry (credit cards, student loans, mortgage)?

Pro tips from us: If your emergency fund is not fully stocked (ideally 3-6 months of living expenses), or if you have high-interest debt, paying cash for a car might not be the best move, even if you have the funds. Your financial safety net and debt reduction should often take precedence.

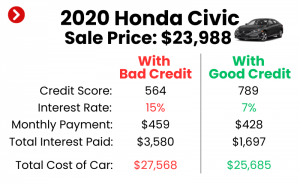

2. Interest Rates & APR

If you’re considering a loan, the interest rate (and more importantly, the Annual Percentage Rate or APR, which includes fees) is paramount. A low interest rate significantly reduces the total cost of borrowing, making a loan more attractive. Conversely, a high interest rate can make paying cash far more appealing.

Shop around for the best rates from multiple lenders – banks, credit unions, and online lenders – before stepping into a dealership. A difference of even one or two percentage points can save you hundreds, if not thousands, of dollars over the loan term.

3. Opportunity Cost

This concept cannot be stressed enough. What else could you do with the cash you’re considering spending on a car? Could it be invested for retirement, used for a down payment on a house, or to start a business?

Weigh the guaranteed savings from avoiding interest payments against the potential returns from investing that money. This calculation will be unique to your financial goals and risk tolerance.

4. Credit Score

Your credit score directly influences the interest rate you’ll be offered on a car loan. A high credit score (generally 700+) can unlock the most favorable rates, making financing a very attractive option. A lower score, however, will result in higher rates, increasing the total cost of the loan significantly.

If your credit isn’t great, consider improving it before applying for a car loan, or explore options like secured loans or a larger down payment. For external reference, you can learn more about understanding your credit score from trusted sources like the Consumer Financial Protection Bureau (CFPB) .

5. Car Depreciation

Cars are depreciating assets. They lose value from the moment you drive them off the lot. While this is true regardless of how you pay, it’s a critical consideration. If you pay cash, you’re tying up capital in an asset that is steadily losing value.

If you finance, you run the risk of negative equity if the car depreciates faster than you pay down the loan. Understanding typical depreciation rates for the vehicle you’re interested in can help inform your decision.

6. Down Payment

Even if you opt for a loan, a substantial down payment can significantly improve your financial standing. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

It also helps mitigate the risk of negative equity. Pro tips from us: Aim for at least 20% down, especially on a new car, to start with positive equity.

7. Your Risk Tolerance

How comfortable are you with debt? How comfortable are you with a smaller emergency fund? Your personal tolerance for financial risk plays a huge role. Some people prefer the absolute certainty of no debt, while others are comfortable leveraging loans to preserve liquidity or pursue investment opportunities.

There’s no right or wrong answer here, but honest self-assessment is key.

8. Long-Term Financial Goals

Consider how this car purchase fits into your broader financial plan. Is a car loan going to delay your ability to save for a house, retirement, or your children’s education? Or will paying cash leave you too exposed to unexpected expenses?

Align your car buying decision with your overarching financial objectives. A car is a tool; ensure its purchase doesn’t derail your ultimate destination.

Hybrid Approaches and Smart Strategies

The decision isn’t always black and white. There are nuanced approaches that can blend the benefits of both cash and loans, alongside smart strategies that apply regardless of your payment method.

1. Large Down Payment with a Small Loan

This is often the "best of both worlds" strategy. By making a significant down payment (e.g., 30-50% or more), you drastically reduce the amount you need to finance. This results in much lower monthly payments, less interest paid overall, and a reduced risk of negative equity.

You preserve some of your cash for emergencies or investments, while still benefiting from building credit and spreading a manageable cost over time. This approach is highly recommended for those who have substantial savings but don’t want to completely deplete them.

2. Negotiating Like a Pro

Regardless of whether you pay cash or finance, never skip the negotiation process. Research the market value of the car you want, understand all fees, and be prepared to walk away. Dealerships often try to focus on the monthly payment; always negotiate the total price of the car first.

Pro tips from us: Keep your payment method to yourself until you’ve agreed on the vehicle’s price. Disclosing you’re a cash buyer too early might mean missing out on potential dealer incentives tied to financing.

3. Refinancing Options

If you initially took out a car loan with a higher interest rate (perhaps due to a lower credit score at the time), you might be able to refinance it later. If your credit score has improved or interest rates have dropped, refinancing can secure you a lower rate, reducing your monthly payments and total interest paid.

This is a valuable strategy for those who used a loan to build credit and are now in a stronger financial position. Don’t be afraid to revisit your loan terms down the line.

4. Pre-approval: A Powerful Tool for Loan Seekers

Before you even step foot in a dealership, get pre-approved for a car loan from your bank, credit union, or an online lender. This provides you with a clear understanding of the interest rate and loan amount you qualify for, essentially giving you "cash in hand" leverage.

With a pre-approval in hand, you can negotiate with the dealership as if you were a cash buyer, as you already have your financing secured. This allows you to focus solely on the car price, without the pressure of in-house financing discussions.

Common Mistakes to Avoid (E-E-A-T)

Having guided countless individuals through this process, I’ve observed several recurring pitfalls. Avoiding these common mistakes can save you significant money and stress.

1. Draining Your Emergency Fund

As emphasized earlier, this is perhaps the biggest mistake. Your emergency fund is your financial safety net, designed to protect you from job loss, medical emergencies, or unforeseen home repairs. Draining it for a depreciating asset like a car leaves you vulnerable. Always prioritize your emergency savings.

2. Focusing Only on Monthly Payments

Dealerships love to talk about monthly payments because it makes expensive cars seem more affordable. However, a low monthly payment often comes with a longer loan term and a higher total interest paid. Always ask for the total price of the vehicle, including all fees and interest, over the life of the loan.

3. Ignoring the Total Cost of Ownership

Beyond the purchase price or loan payments, remember to factor in other costs: insurance, maintenance, fuel, and potential repairs. A cheaper car upfront might be more expensive to own in the long run. Research reliability ratings and insurance costs before committing.

4. Not Shopping Around for Loans

Never take the first loan offer you receive, especially not from the dealership’s finance department without comparing. Always shop around with multiple banks and credit unions before you go to the dealership. This empowers you with the best rate and allows you to negotiate from a position of strength.

5. Buying More Car Than You Can Afford

It’s easy to get swept up in the excitement and desire for a fancier car. However, purchasing a vehicle that strains your budget can lead to financial stress and regret. Be realistic about what you can comfortably afford, not just in terms of monthly payments, but also overall cost and impact on your other financial goals.

Conclusion: Making Your Informed Decision

The journey to buying a new or used car is exciting, but the decision of whether to pay with a car loan or cash is a critical one that impacts your financial well-being for years to come. There is no single "best" answer; the optimal choice depends entirely on your unique financial situation, goals, and risk tolerance.

We’ve explored the myriad benefits of paying cash – the freedom from interest, monthly payments, and debt – alongside its potential drawbacks, such as depleting vital savings. Conversely, we’ve examined how car loans can preserve liquidity, build credit, and make more reliable vehicles accessible, while also highlighting the costs of interest and the burden of debt.

Pro tips from us: Take the time to honestly assess your financial health, calculate the total cost of each option, and consider how this purchase aligns with your long-term aspirations. Whether you choose the immediate satisfaction of paying cash, the strategic flexibility of a loan, or a smart hybrid approach, make sure it’s a decision rooted in knowledge and foresight.

By carefully weighing these factors and avoiding common pitfalls, you’ll be well-equipped to drive away in your next vehicle, confident that you’ve made a financially sound choice.

What’s your experience? Did you pay cash or take a loan for your last car? Share your insights and questions in the comments below! And for more insights on managing your finances, check out our other articles on or .