Car Loan vs. Hire Purchase: The Ultimate Guide to Funding Your Dream Car

Car Loan vs. Hire Purchase: The Ultimate Guide to Funding Your Dream Car Carloan.Guidemechanic.com

Driving your own car offers unparalleled freedom, convenience, and a sense of accomplishment. But before you hit the open road, a crucial decision awaits: how will you finance your new (or new-to-you) vehicle? For many, the choice boils down to a Car Loan or a Hire Purchase (HP) agreement. While both options allow you to drive away with a car without paying the full price upfront, they are fundamentally different, each with its own set of advantages and disadvantages.

Understanding these distinctions is paramount. Making the right financial choice can save you thousands in interest, avoid unexpected penalties, and ensure your car ownership journey is a smooth one. This comprehensive guide will dissect Car Loans and Hire Purchase, helping you navigate the complexities and empowering you to make the best decision for your unique financial situation. Let’s embark on this journey to decode vehicle financing!

Car Loan vs. Hire Purchase: The Ultimate Guide to Funding Your Dream Car

Understanding the Core Differences: Car Loan vs. Hire Purchase

At a glance, both car loans and hire purchase agreements might seem similar – you make regular payments and eventually get to keep the car. However, the legal structure and implications, particularly concerning ownership, set them miles apart. Grasping this fundamental difference is the first step towards an informed decision.

What Exactly is a Car Loan?

A Car Loan, often referred to as an auto loan, is a sum of money borrowed from a financial institution, like a bank or credit union, specifically for the purpose of purchasing a vehicle. When you take out a car loan, the lender provides you with the funds, and you then use this money to buy the car outright from the dealership or private seller.

The key characteristic here is that you become the legal owner of the car immediately upon purchase. The car serves as collateral for the loan, meaning if you fail to make your payments, the lender has the right to repossess the vehicle to recover their money. You will then repay the borrowed amount, plus interest, over a predetermined period through fixed monthly installments.

What is a Hire Purchase (HP) Agreement?

A Hire Purchase (HP) agreement, on the other hand, is a financing method where you effectively rent the car for a set period, with an option to purchase it at the end of the agreement. With HP, the finance company legally owns the car throughout the repayment term. You, as the hirer, gain possession and use of the vehicle, but you do not become the outright owner until you have made all the scheduled payments and typically paid an "option to purchase" fee.

This distinction in ownership is critical. Until the final payment is made and the option fee is settled, you are not the car’s legal proprietor. This means you cannot sell, extensively modify, or make certain decisions about the vehicle without the finance company’s permission. HP agreements are often arranged directly through car dealerships, who act as intermediaries for the finance company.

Deep Dive into Car Loans: Pros, Cons, and Key Considerations

When you opt for a car loan, you’re essentially taking on a personal debt that is secured against the vehicle itself. This approach has distinct advantages, but it also comes with its own set of responsibilities.

How a Car Loan Works

The process typically begins with you applying for a loan with a bank, credit union, or online lender. They will assess your creditworthiness, income, and debt-to-income ratio. Once approved, you receive the funds, which you then use to pay the car seller. The car’s title is issued in your name, often with the lender noted as a lienholder until the loan is fully repaid.

You then make regular, fixed monthly payments over the agreed loan term, which can range from a few months to several years (commonly 3 to 7 years). Each payment covers a portion of the principal amount borrowed and the accrued interest. Once the final payment is made, the lender removes their lien, and you own the car free and clear.

Advantages of a Car Loan

- Immediate Ownership: This is perhaps the biggest draw. From day one, the car is legally yours. You hold the title (though a lienholder may be noted). This gives you full control over the vehicle.

- Flexibility and Freedom: Because you own the car, you’re free to sell it at any time, modify it as you wish (within legal limits), or even use it as collateral for another loan if needed. There are no mileage restrictions often found in other financing types.

- Potential for Lower Interest Rates: If you have a strong credit score, you might qualify for very competitive interest rates from banks or credit unions, potentially leading to a lower overall cost compared to some HP agreements.

- Refinancing Options: Should interest rates drop, or your credit score improve, you might be able to refinance your car loan to secure a better rate or different terms, potentially reducing your monthly payments or total interest paid.

Disadvantages of a Car Loan

- Higher Initial Payments (Potentially): While not always the case, car loan monthly payments can sometimes be higher than HP, especially if you opt for a shorter loan term to minimize interest, or if a significant down payment isn’t made.

- Credit Score Dependency: Securing a good car loan rate heavily relies on your credit history and score. Individuals with poor credit may struggle to get approved or face very high interest rates.

- Depreciation Risk is Yours: As the owner, you bear the full brunt of depreciation. Cars lose value rapidly, particularly in the first few years. If you need to sell the car early, you might find its market value is less than the outstanding loan balance, putting you in a negative equity situation.

- Collateral Requirement: The car itself acts as collateral. Defaulting on your payments can lead to repossession, meaning you lose the vehicle and still might owe money if the sale of the repossessed car doesn’t cover the full outstanding balance.

Based on my experience, securing a direct car loan from a bank often gives you more negotiating power at the dealership. You walk in as a cash buyer, which can sometimes lead to a better purchase price for the car itself, separating the car purchase from the financing decision.

Deep Dive into Hire Purchase (HP) Agreements: Pros, Cons, and Key Considerations

Hire Purchase offers a different route to car ownership, one where the finance company plays a more direct role throughout the repayment period. It’s particularly common for new and used cars bought from dealerships.

How a Hire Purchase Agreement Works

With HP, you typically pay an initial deposit, and then make fixed monthly payments over an agreed term, usually between 1 and 5 years. The finance company purchases the car from the dealership, and you "hire" it from them. During this period, you have possession and use of the vehicle, but it remains legally owned by the finance company.

Once all the scheduled monthly payments have been made, and you pay a small "option to purchase" fee (which finalizes the transfer of ownership), the car legally becomes yours. Until that point, you are effectively a renter with an option to buy.

Advantages of a Hire Purchase Agreement

- Lower Initial Deposit (Often): HP agreements often require a smaller upfront deposit compared to what might be needed for a traditional car loan, making it easier to get behind the wheel if your savings are limited. Some agreements even offer zero-deposit options.

- Predictable Fixed Payments: Your monthly payments are fixed throughout the agreement, making budgeting straightforward and predictable. You know exactly how much you need to pay each month, which can be reassuring.

- Easier Approval for Some: For individuals with a less-than-perfect credit history, HP agreements can sometimes be easier to secure than a traditional car loan, as the finance company retains ownership of the vehicle as security.

- Structured Path to Ownership: It provides a clear, disciplined path to owning the car. As long as you keep up with payments, you know the car will eventually be yours.

Disadvantages of a Hire Purchase Agreement

- No Immediate Ownership: This is the most significant drawback. You don’t own the car until the very end of the agreement. This means you cannot sell the car, part-exchange it, or make significant modifications without the finance company’s explicit permission.

- Less Flexibility: Breaking an HP agreement early can be costly. You might face early settlement penalties or still owe a significant portion of the outstanding balance, especially if you’re early in the term and the car’s value has dropped considerably.

- Potentially Higher Overall Cost: While monthly payments might seem lower, the total amount paid over the term, including interest and the option to purchase fee, can sometimes be higher than a competitive car loan, especially for those with excellent credit.

- "Option to Purchase" Fee: Don’t forget this final fee. While usually a small amount (e.g., £100), it’s a mandatory payment at the end of the term to transfer ownership and should be factored into your total cost calculation.

Pro tips from us: Always scrutinize the "option to purchase" fee and any early settlement clauses within an HP agreement. These details can significantly impact the overall cost and your flexibility.

Car Loan vs. Hire Purchase: A Head-to-Head Comparison

To further clarify the distinctions, let’s compare these two financing options on several key criteria.

| Feature | Car Loan (Auto Loan) | Hire Purchase (HP) |

|---|---|---|

| Ownership | You own the car from day one. | Finance company owns the car until final payment + fee. |

| Collateral/Security | The car acts as collateral for the loan. | The finance company owns the car as security. |

| Initial Deposit | Varies, often optional or a strong recommendation. | Often required, can be lower than a car loan’s down payment. |

| Interest Calculation | Based on the outstanding loan balance. | Often calculated on the initial amount borrowed. |

| Flexibility | High. Can sell, modify, or refinance the car easily. | Low. Cannot sell or modify without permission until owned. |

| Early Settlement | Generally possible with varying penalties/savings. | Possible, but often incurs significant penalties. |

| Depreciation Risk | Fully borne by you. | Borne by the finance company initially, then by you upon ownership. |

| Credit Impact | Strong credit usually yields better rates. | Can be more accessible for varied credit profiles. |

| End of Agreement | You own the car outright. | You pay an "option to purchase" fee to gain ownership. |

Factors to Consider When Choosing Your Car Financing

The "best" option isn’t universal; it depends entirely on your personal circumstances, financial goals, and preferences. Here are the critical factors to weigh before making your decision.

Your Financial Situation

Your current financial health is perhaps the most important determinant. Lenders will assess your credit score, income stability, existing debts, and overall financial history.

- Credit Score: If you have an excellent credit score, you’re likely to qualify for the most competitive interest rates on a car loan. If your credit is fair or poor, an HP agreement might be more accessible, though often at a higher effective interest rate.

- Income Stability: Lenders want to see a consistent income that demonstrates your ability to make regular payments. Both options require this, but car loans might have stricter income-to-debt ratios.

- Existing Debts: High existing debt levels can impact your ability to secure either type of financing or push you towards less favorable terms.

Ownership Preference

Do you value immediate ownership and the freedom that comes with it, or are you comfortable waiting until the end of the term?

- Immediate Control: If you want the ability to sell, trade-in, or extensively customize your vehicle without seeking permission, a car loan aligns better with this preference.

- Gradual Ownership: If you prefer a structured path where you gradually work towards ownership and are less concerned with immediate control, HP can be a suitable choice.

Future Plans for the Car

Consider how long you intend to keep the vehicle and what your plans might be.

- Long-Term Keeper: If you plan to keep the car for many years beyond the financing term, a car loan might be more cost-effective in the long run, especially with a good interest rate.

- Potential Early Sale/Trade-in: If you foresee needing to sell or trade-in the car within a few years, understand the implications. With a car loan, you can sell anytime (though you must settle the loan). With HP, selling early means settling the agreement, which can be expensive.

Your Budget: Monthly Payment vs. Total Cost

It’s crucial to look beyond just the monthly payment. While a lower monthly payment might seem appealing, it could mean a longer term and more interest paid overall.

- Monthly Affordability: Calculate what you can comfortably afford each month without straining your finances. Use online calculators to compare payment scenarios for different loan amounts, terms, and interest rates.

- Total Cost of Financing: Sum up all payments, interest, fees (like the HP option to purchase fee), and any initial deposits to determine the true overall cost of each option. This holistic view helps you identify the most financially sound choice.

Interest Rates and Fees

These are the core financial components that determine how much you’ll pay beyond the car’s price.

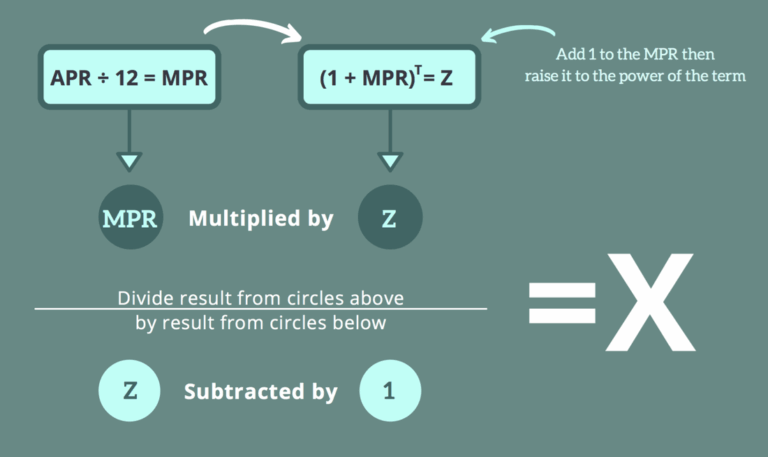

- Annual Percentage Rate (APR): Always compare the APR, not just the advertised interest rate. APR includes all mandatory fees and charges, giving you a truer picture of the loan’s annual cost.

- Hidden Fees: Look out for processing fees, administration charges, early settlement penalties, and the "option to purchase" fee in HP agreements. These can add up.

Down Payment or Initial Deposit

How much cash do you have available upfront?

- Car Loan: A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

- Hire Purchase: HP often requires a deposit, but it can sometimes be smaller, or even zero, making it accessible even if you have limited upfront cash.

Common Mistakes to Avoid in Car Financing

Based on my experience in the automotive and finance sectors, many individuals fall prey to common pitfalls when financing a car. Avoiding these can save you stress and money.

- Focusing Only on Monthly Payments: This is perhaps the most prevalent mistake. While affordable monthly payments are important, fixating solely on them can lead to longer loan terms, higher overall interest, and ultimately, a more expensive car. Always consider the total cost of the financing.

- Not Reading the Fine Print: Every contract, whether a car loan agreement or an HP agreement, contains crucial details. Pay close attention to interest rates, fees, penalties for early settlement, and any clauses regarding modifications or mileage. Don’t be afraid to ask questions until you fully understand every term.

- Neglecting Your Credit Score: Your credit score is your financial passport. Not knowing or working to improve your score before seeking financing can lead to higher interest rates or even rejection. Check your credit report well in advance.

- Not Shopping Around: Never take the first offer presented to you, especially at a dealership. Compare offers from multiple banks, credit unions, and finance providers for both car loans and HP. Different lenders have different criteria and rates.

- Forgetting About Additional Costs: The monthly payment is just one piece of the puzzle. Factor in insurance, road tax, maintenance, servicing, and fuel costs into your overall budget. A car that seems affordable on paper can become a burden if these running costs are overlooked.

- Underestimating Depreciation: Cars lose value. Understanding how quickly your chosen vehicle depreciates can help you avoid negative equity, where you owe more on the car than it’s worth. This is particularly relevant if you plan to sell or trade in the car before the financing term ends.

Pro Tips for a Smooth Car Financing Journey

Navigating the world of car financing can be daunting, but with a few strategic approaches, you can secure a great deal and drive away confidently.

- Get Pre-Approved for a Loan: Before you even step foot in a dealership, get pre-approved for a car loan from your bank or credit union. This gives you a clear budget, acts as leverage when negotiating the car price, and allows you to compare the dealership’s financing offers against your pre-approval.

- Understand Your Credit Report: Obtain a copy of your credit report and check it for any errors. Rectifying mistakes can significantly improve your score. A higher score translates directly to better interest rates. For more insights into managing your credit score effectively, check out our guide on .

- Negotiate Fiercely (But Fairly): Everything is negotiable – the car’s price, your trade-in value, and even financing terms. Be prepared to walk away if the deal isn’t right. Knowledge is power here.

- Budget for More Than Just the Payment: Create a comprehensive budget that includes not only your monthly financing payment but also insurance, fuel, maintenance, and potential repair costs. A good rule of thumb is to allocate an additional 10-15% of your car payment towards these running costs.

- Consider the Car’s Resale Value: Some cars hold their value better than others. Researching depreciation trends for the models you’re considering can be a smart move, especially if you anticipate selling or trading in the car in the future.

- Don’t Be Pressured: Car dealerships can be high-pressure environments. Take your time, ask questions, and never sign anything you don’t fully understand or are uncomfortable with. If you’re still weighing your options for vehicle acquisition, explore our article on .

- Seek External Advice: If you’re unsure, consult a financial advisor or a trusted, independent source. For official guidelines and consumer rights regarding vehicle financing, a trusted resource like the Consumer Financial Protection Bureau (CFPB) in the US or similar national financial regulatory bodies can provide invaluable information. You can find more details on their official website, for example, at www.consumerfinance.gov (External Link Simulation to a reputable financial advice site).

Conclusion: Making Your Informed Decision

The choice between a Car Loan and a Hire Purchase agreement is a significant financial decision that should not be taken lightly. There’s no universal "best" option; the ideal choice is the one that best aligns with your personal financial situation, your comfort level with ownership, and your long-term plans for the vehicle.

A car loan offers immediate ownership, greater flexibility, and potentially lower overall costs for those with strong credit. Hire Purchase, on the other hand, can provide easier access to a vehicle with lower upfront costs and predictable payments, particularly for those with a less established credit history, albeit with delayed ownership and less flexibility.

Before committing, take the time to thoroughly evaluate your financial standing, compare multiple offers, understand all the terms and conditions, and ask every question you have. By doing your homework and considering all the factors discussed in this guide, you will be well-equipped to make an informed decision that puts you in the driver’s seat of your dream car, with peace of mind. Drive smart, finance wisely!