Car Loan With Bankruptcy On Credit: Your Ultimate Roadmap to Auto Financing Success

Car Loan With Bankruptcy On Credit: Your Ultimate Roadmap to Auto Financing Success Carloan.Guidemechanic.com

Navigating the financial landscape after a bankruptcy can feel like traversing a dense fog. Many assume that getting a car loan with bankruptcy on credit is an impossible feat. However, we’re here to tell you that it’s not only possible but, with the right strategy, it can also be a significant step towards rebuilding your financial stability.

This comprehensive guide is designed to be your ultimate roadmap. We’ll demystify the process, share expert insights, and provide actionable steps to help you secure a car loan even after bankruptcy. Our goal is to empower you with the knowledge and confidence to drive away in your next vehicle, all while setting yourself on a path to a stronger financial future.

Car Loan With Bankruptcy On Credit: Your Ultimate Roadmap to Auto Financing Success

Understanding Bankruptcy and Its Impact on Your Credit

Before diving into car loans, it’s crucial to understand what bankruptcy entails and how it affects your credit. Bankruptcy provides a legal "fresh start" for individuals burdened by insurmountable debt. However, this fresh start comes with a significant, albeit temporary, impact on your credit report.

There are primarily two types of personal bankruptcy relevant to most consumers: Chapter 7 and Chapter 13. Chapter 7, often called "liquidation" bankruptcy, discharges most unsecured debts quickly, typically within a few months. Chapter 13, or "reorganization" bankruptcy, involves a court-approved repayment plan over three to five years.

Regardless of the chapter, a bankruptcy filing will appear on your credit report for a considerable period. Chapter 7 stays for 10 years, while Chapter 13 remains for 7 years from the filing date. During this time, your credit score will drop significantly, and lenders will view you as a higher risk. This doesn’t mean you’re unlendable, but it does mean you’ll need to approach financing strategically.

The Reality of Getting a Car Loan With Bankruptcy On Credit

The immediate aftermath of a bankruptcy can feel daunting when you need to finance a significant purchase like a car. Many people assume they are simply out of options. However, the reality is more nuanced. While challenging, obtaining a car loan after bankruptcy is a common scenario that lenders are prepared to address.

From our professional perspective, many lenders specialize in what’s known as "subprime" lending. These are loans offered to borrowers with less-than-perfect credit, including those with a bankruptcy history. These lenders understand that life happens and people deserve a second chance.

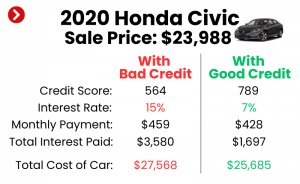

The key difference you’ll encounter is in the terms of the loan. Expect higher interest rates compared to someone with excellent credit. This higher rate compensates the lender for the increased risk they are taking. Additionally, loan terms might be shorter, or you might need to provide a larger down payment.

Pro tips from us: Don’t get discouraged by initial rejections. The market for bad credit car loans is competitive, and finding the right lender who understands your situation is paramount. Persistence and preparation are your greatest allies in this journey.

Key Factors Lenders Consider After Bankruptcy

When you apply for a car loan with bankruptcy on credit, lenders will scrutinize several aspects of your financial situation. Understanding these factors will help you prepare a stronger application and increase your chances of approval.

Time Since Discharge

The amount of time that has passed since your bankruptcy was discharged is a critical factor. The further you are from the bankruptcy filing date, the better. Lenders typically prefer to see at least a year or two pass, as it demonstrates that you’ve had time to stabilize your finances post-bankruptcy.

A longer period allows you to demonstrate responsible financial behavior. It gives lenders confidence that you are moving forward and not likely to repeat past financial difficulties. Every month that passes without new negative entries on your credit report works in your favor.

Re-established Credit History

While your bankruptcy is still on your report, lenders want to see evidence that you’ve started rebuilding your credit. This doesn’t mean accumulating new debt but rather demonstrating responsible use of new, small credit lines.

Perhaps you’ve opened a secured credit card and made timely payments, or secured a small credit-builder loan. These actions show lenders that you are capable of managing credit responsibly. It’s about demonstrating a positive trend after the bankruptcy.

Income and Employment Stability

Lenders need assurance that you have the consistent ability to make your car loan payments. Your income and employment stability are therefore heavily weighed. They want to see a steady job history, ideally with the same employer for a significant period.

Proof of consistent income, such as recent pay stubs or bank statements, will be essential. This demonstrates your capacity to meet your financial obligations and reduces the perceived risk for the lender.

Down Payment Amount

A substantial down payment can significantly improve your chances of approval and secure better loan terms. When you put down a larger amount, you reduce the lender’s risk. It also means you’ll be borrowing less, leading to lower monthly payments and less interest paid over the life of the loan.

Based on my experience, a down payment shows your commitment and financial discipline. It signals to lenders that you have some equity in the vehicle from day one, which makes the loan less risky for them. Aim for at least 10-20% of the car’s value if possible.

Vehicle Choice and Price

The type of vehicle you choose also plays a role. Lenders are more inclined to approve loans for reliable, reasonably priced used cars rather than brand-new luxury models. A modest, affordable car presents less risk for both you and the lender.

Opting for a vehicle that fits comfortably within your budget, even after accounting for insurance and maintenance, is a smart move. It demonstrates financial prudence and increases the likelihood that you can sustain the payments without strain.

Co-signer Option

If you’re struggling to get approved on your own, having a co-signer with good credit can be a significant advantage. A co-signer essentially guarantees the loan, promising to make payments if you default. This greatly reduces the lender’s risk.

However, choosing a co-signer is a serious decision. It impacts their credit and financial future if you fail to pay. Ensure both parties fully understand the responsibilities involved before pursuing this option.

Steps to Prepare for a Car Loan Application Post-Bankruptcy

Preparation is key when seeking a car loan after bankruptcy. A well-prepared application can make all the difference in securing approval and favorable terms. Follow these steps to put yourself in the best possible position.

1. Check Your Credit Report and Score

Your first and most crucial step is to obtain copies of your credit reports from all three major bureaus (Experian, Equifax, TransUnion). Review them meticulously for any errors or inaccuracies. Bankruptcy information should be correctly reported.

Dispute any discrepancies immediately, as even small errors can negatively impact your score. Understanding exactly what lenders will see helps you anticipate questions and address potential issues proactively. You can get free copies of your reports annually from AnnualCreditReport.com.

2. Understand Your Budget

Before you even look at cars, determine what you can truly afford. This isn’t just about the monthly car payment. Factor in insurance, fuel, maintenance, and potential repair costs.

A common mistake to avoid is focusing solely on the monthly payment. Look at the total cost of ownership and ensure it fits comfortably within your overall budget. Overextending yourself now could lead to future financial strain.

3. Save for a Down Payment

As discussed, a larger down payment is incredibly beneficial. Start saving as much as you can. Even a few hundred dollars can make a difference, but aiming for 10-20% of the vehicle’s price will significantly improve your loan prospects and terms.

A substantial down payment reduces the loan amount, lowers your monthly payments, and shows lenders your commitment. It’s one of the most impactful steps you can take to strengthen your application.

4. Gather Necessary Documents

Lenders will require various documents to verify your identity, income, and financial history. Have these ready before you apply. This typically includes:

- Government-issued ID (driver’s license)

- Proof of residence (utility bill)

- Proof of income (recent pay stubs, bank statements, tax returns if self-employed)

- Bankruptcy discharge papers or proof of Chapter 13 filing and trustee approval.

- Trade-in vehicle title (if applicable).

Having everything organized demonstrates your seriousness and efficiency, streamlining the application process.

5. Build a Small Credit History (Carefully)

If some time has passed since your bankruptcy, focus on responsibly building a positive credit history. This could involve a secured credit card, where your credit limit is backed by a cash deposit, or a credit-builder loan from a credit union.

Make sure to use these new credit lines sparingly and pay them off in full and on time every single month. Consistent, positive payment history is the fastest way to show lenders you are a responsible borrower post-bankruptcy. For a deeper dive into improving your credit score, explore our detailed guide on .

Finding the Right Lenders for Car Loans After Bankruptcy

Not all lenders are created equal, especially when it comes to financing a car loan with bankruptcy on credit. Knowing where to look can save you time and frustration.

Subprime Auto Lenders

These lenders specialize in working with borrowers who have less-than-perfect credit scores. Their business model is built around assessing higher-risk applicants. They understand that a bankruptcy doesn’t define your entire financial future.

Many large dealerships work with a network of subprime lenders, making them a good starting point. Be prepared for potentially higher interest rates, but also for a greater willingness to work with your specific situation.

Dealership Financing

Most car dealerships have finance departments that work with multiple lenders, including subprime ones. They can often submit your application to several institutions simultaneously, increasing your chances of finding an approval.

However, always compare their offers with pre-approvals you might receive elsewhere. While convenient, dealership financing isn’t always the cheapest option.

Credit Unions

Credit unions are member-owned financial institutions often known for more flexible lending criteria and lower interest rates compared to traditional banks. If you’re a member, or eligible to join one, it’s worth exploring their auto loan options.

They may be more willing to consider your individual circumstances beyond just your credit score. Building a relationship with a credit union can be beneficial for future financial needs as well.

Online Lenders

A growing number of online lenders specialize in bad credit auto loans. Many offer pre-qualification processes that allow you to see potential loan terms without impacting your credit score. This can be a great way to compare offers from various lenders from the comfort of your home.

Be cautious and only use reputable online lenders. Read reviews and ensure they are transparent about their terms and fees.

Beware of "Buy Here, Pay Here" Lots

"Buy Here, Pay Here" dealerships lend you money directly, often without a credit check. While this seems convenient, these loans typically come with extremely high interest rates, short repayment terms, and limited vehicle choices.

From our professional observation, while they can be a last resort, they are rarely the best option for long-term financial recovery. Always explore other avenues first before considering a "Buy Here, Pay Here" lot.

The Application Process: What to Expect

Once you’ve done your homework and found potential lenders, it’s time to apply. The process might seem intimidating, but honesty and preparation will guide you through.

When you submit your application, be completely transparent about your bankruptcy. Trying to hide it will only lead to distrust and rejection. Lenders appreciate honesty and a clear explanation of your current financial situation.

Expect lenders to thoroughly review your income, employment history, and the time elapsed since your bankruptcy discharge. They will also assess your current debt-to-income ratio to ensure you can comfortably manage new payments.

Understanding the terms of your loan is crucial. Pay close attention to the Annual Percentage Rate (APR), the loan term (how long you have to pay it back), and any associated fees. A higher APR means more interest paid over time, and a longer loan term, while lowering monthly payments, also increases total interest.

Pro tip: Don’t be afraid to negotiate, even with bad credit. If you have multiple pre-approvals, use them as leverage to get the best possible terms. Ensure you read all the fine print before signing any agreement.

Chapter 7 vs. Chapter 13: Specific Considerations

The type of bankruptcy you filed significantly impacts when and how you can obtain a car loan. Understanding these distinctions is vital.

Car Loan After Chapter 7 Bankruptcy

With Chapter 7, your debts are typically discharged within a few months. Once the bankruptcy is officially discharged, you are generally free to take on new debt. This is often the "fresh start" lenders look for.

Lenders will still be cautious, but they know you’re no longer burdened by the previous debts. The main focus will be on your post-bankruptcy financial behavior, such as income stability and any credit rebuilding efforts you’ve made. The longer it has been since your discharge, the better your chances of approval. You will need to provide your discharge papers as proof.

Car Loan During or After Chapter 13 Bankruptcy

Chapter 13 bankruptcy is more complex because you are actively in a repayment plan for three to five years. Getting a car loan during an active Chapter 13 plan requires court approval. This is not a simple process.

You will typically need to file a motion with the bankruptcy court, demonstrating that the car is a necessity (e.g., for work or medical appointments) and that the proposed loan payments are affordable within your existing repayment plan. Your bankruptcy trustee will review the request and make a recommendation to the judge. This process can add several weeks to your car buying journey.

If you are seeking a car loan after your Chapter 13 plan has been successfully completed and discharged, the process becomes more similar to that of a Chapter 7 discharge. The bankruptcy will still be on your credit report, but the successful completion of the repayment plan demonstrates a strong commitment to financial responsibility, which lenders will view positively.

Rebuilding Your Credit Score While Paying Off Your Car Loan

Securing a car loan after bankruptcy isn’t just about getting a vehicle; it’s a powerful tool for rebuilding your credit. How you manage this loan will profoundly impact your financial future.

Make Payments On Time, Every Time

This is non-negotiable. Your car loan payments will be reported to credit bureaus. Consistent, on-time payments are the single most effective way to demonstrate creditworthiness and improve your score. Set up automatic payments to avoid missing due dates.

Even a single late payment can set back your credit rebuilding efforts significantly. Treat your car loan as a priority payment.

Keep Credit Utilization Low on Other Accounts

If you have any other credit accounts, such as a secured credit card, strive to keep your credit utilization ratio low. This means not maxing out your credit limit. Ideally, keep balances below 30% of your available credit.

Low utilization signals to lenders that you’re not overly reliant on credit and can manage your finances responsibly.

Avoid New Unnecessary Debt

While you’re working to rebuild, resist the temptation to take on new, unnecessary debt. Focus on your current obligations, especially your car loan. Each new debt adds more financial pressure and can slow your credit recovery.

Patience and discipline are key. Allow your credit score to improve steadily by managing your existing accounts well.

Monitor Your Credit Regularly

Regularly check your credit reports and scores. You can use free credit monitoring services provided by many banks or credit card companies. This allows you to track your progress, spot any errors, and ensure all your payments are being reported correctly.

Monitoring your credit empowers you to take control of your financial health. To understand more about navigating personal finances after a major life event, you might find our article on helpful.

Common Mistakes to Avoid When Seeking a Car Loan After Bankruptcy

Even with the best intentions, certain pitfalls can derail your efforts to secure a car loan after bankruptcy. Being aware of these common mistakes can help you steer clear of them.

- Not Checking Your Credit Report First: Failing to review your credit report for accuracy before applying is a significant oversight. Errors can unfairly lower your score and lead to rejections.

- Applying to Too Many Lenders Simultaneously: Each hard inquiry on your credit report can slightly lower your score. Applying to numerous lenders at once can be detrimental. Stick to a few well-researched options within a short window (typically 14-45 days for rate shopping) to minimize the impact.

- Ignoring Your Budget: Getting approved for a loan doesn’t mean you can truly afford it. Overcommitting to a high monthly payment can lead to financial stress and potentially another default.

- Settling for the First Offer: Even with bankruptcy on your credit, comparing offers is crucial. The first offer you receive might not be the best one. Shop around to ensure you’re getting competitive rates and terms.

- Not Reading the Fine Print: Auto loan contracts can be complex. Always read every line, understand all fees, and clarify any ambiguities before signing. From my professional observation, overlooking details can lead to unexpected costs.

- Buying an Unreliable Car: A car with a low purchase price but high maintenance costs can quickly become a financial burden. Focus on reliable, affordable used vehicles that won’t drain your budget with repairs.

Pro Tips for Success

Securing a car loan after bankruptcy is a journey, not a sprint. Here are some final pro tips to ensure your success and set you up for long-term financial health.

- Start Small: Your first car after bankruptcy doesn’t need to be your dream car. Aim for a reliable, affordable used car that meets your immediate transportation needs. This allows you to successfully make payments and build positive credit.

- Consider a Shorter Loan Term: While a longer loan term means lower monthly payments, it also means you pay significantly more in interest over time. If your budget allows, opt for the shortest loan term you can comfortably afford.

- Focus on Consistency: The most powerful tool for credit rebuilding is consistent, on-time payments. Every single payment contributes to your recovery.

- Don’t Be Afraid to Negotiate: Even with bad credit, there’s often room for negotiation on the car price, trade-in value, and potentially even loan terms if you have multiple offers.

- Educate Yourself Continually: Stay informed about personal finance and credit management. The more you know, the better decisions you can make. You can learn more about understanding your credit report from trusted sources like the Consumer Financial Protection Bureau (CFPB).

Conclusion: Driving Towards a Brighter Financial Future

Obtaining a car loan with bankruptcy on credit is a significant step towards rebuilding your financial life. It demonstrates resilience and a commitment to moving forward. While the path may present challenges, it is absolutely achievable with diligent preparation, realistic expectations, and a strategic approach.

Remember, bankruptcy is not the end of your financial story; it’s often a new beginning. By following the guidance in this comprehensive roadmap, you can secure the transportation you need, responsibly manage your new debt, and effectively use your car loan as a powerful tool to rebuild your credit score. Start preparing today, and soon you’ll be driving towards a brighter, more stable financial future.