Car Loan Years: How to Choose the Perfect Loan Term for Your New Ride (And Save Thousands!)

Car Loan Years: How to Choose the Perfect Loan Term for Your New Ride (And Save Thousands!) Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but the financing aspect can often feel like navigating a maze. One of the most critical decisions you’ll make, beyond the make and model, is determining the right car loan years – also known as the loan term or duration. This choice profoundly impacts your monthly payments, the total cost of your vehicle, and your overall financial well-being.

As an expert in automotive financing, I’ve seen firsthand how choosing the wrong car loan term can lead to unnecessary financial strain or even trap buyers in a cycle of debt. My mission with this comprehensive guide is to empower you with the knowledge and insights needed to make an informed decision, ensuring your car purchase is a source of joy, not stress. Let’s dive deep into understanding car loan years and how to pick the perfect fit for your financial situation.

Car Loan Years: How to Choose the Perfect Loan Term for Your New Ride (And Save Thousands!)

Understanding Car Loan Years: The Core Concept

At its heart, the "car loan years" refers to the period over which you agree to repay the money borrowed to purchase your vehicle. This duration is typically expressed in months, such as 36, 48, 60, 72, or even 84 months. Each month represents a payment installment, and the total number of months dictates how long you’ll be making those payments.

This choice is far from trivial. It’s a fundamental lever that influences two critical aspects of your car loan: your monthly payment amount and the total amount of interest you’ll pay over the life of the loan. A longer loan term generally means lower monthly payments but higher total interest paid, while a shorter term means the opposite.

Why Your Loan Term Choice Matters So Much

The loan term isn’t just a number; it’s a financial commitment that can affect your budget for years to come. Opting for a shorter term might mean higher monthly outflows, but it frees you from debt faster and often saves you a significant amount in interest. Conversely, a longer term offers the allure of lower monthly payments, making a more expensive car seem affordable, but it comes with its own set of risks and higher overall costs.

Based on my experience, many buyers focus solely on the monthly payment figure. While this is certainly important for budgeting, it’s a common mistake to overlook the total cost of the loan and the long-term implications of stretching payments over many years. This article will help you look beyond the immediate monthly cost and consider the bigger financial picture.

The Spectrum of Car Loan Terms: A Deep Dive

Car loan terms typically range from three years (36 months) to seven years (84 months), with some lenders even offering longer options. Each bracket comes with its unique set of pros and cons, catering to different financial situations and priorities.

Short-Term Loans: 36 to 48 Months

Short-term loans, typically spanning 36 to 48 months, are often considered the most financially prudent choice for those who can afford the higher monthly payments. These terms allow you to pay off your vehicle quickly and minimize the amount of interest you accrue.

The Advantages of Shorter Car Loan Years

One of the biggest benefits of a shorter loan term is the substantial savings on total interest paid. Because you’re repaying the principal more quickly, there’s less time for interest to accumulate, resulting in a lower overall cost for the car. You’ll also build equity in your vehicle faster, meaning you’ll own more of the car’s value sooner. This reduces the risk of being "upside down" on your loan, where you owe more than the car is worth.

From an expert perspective, shorter terms are fantastic for financial discipline. They free up your budget sooner for other financial goals, like saving for a house, retirement, or another significant purchase. It’s a powerful way to reduce your debt burden quickly.

The Disadvantages of Shorter Car Loan Years

The primary drawback of a shorter loan term is the higher monthly payment. For some budgets, this increased monthly outflow can be a significant hurdle, potentially making certain vehicles unaffordable. It requires a robust and stable income to comfortably manage these larger payments.

Common mistakes to avoid here include underestimating the monthly payment burden. Ensure your budget can comfortably accommodate the higher payment without straining your finances, leaving room for unexpected expenses or other financial obligations.

Who Are Short-Term Loans Best For?

Short-term loans are ideal for individuals with a strong, stable income who prioritize minimizing total interest paid and achieving debt freedom quickly. If you have excellent credit, which often qualifies you for lower interest rates on shorter terms, and you’re disciplined with your budget, a 36-to-48-month loan can be an excellent financial move.

Mid-Term Loans: 60 to 72 Months

Mid-range terms, particularly 60-month (five-year) and 72-month (six-year) loans, represent the most popular choice for car buyers. These terms strike a balance between manageable monthly payments and a reasonable total interest cost, making them accessible to a wider range of budgets.

The Appeal of Mid-Range Car Loan Years

The main advantage of a 60-to-72-month loan is the reduced monthly payment compared to shorter terms. This makes a wider selection of vehicles more financially accessible without requiring an overly burdensome monthly commitment. It’s often the "sweet spot" where affordability and total cost meet a comfortable medium.

Pro tips from us: This is often the ideal term for many buyers as it allows for a decent car without completely breaking the bank each month, while still keeping the total interest somewhat in check. It’s a pragmatic approach for balancing immediate cash flow with long-term financial health.

The Trade-offs of Mid-Range Car Loan Years

While more affordable monthly, mid-term loans will result in paying more interest over the life of the loan compared to their shorter counterparts. You’ll also build equity at a slower pace, increasing the potential for negative equity, especially in the early years of the loan. This means the car might depreciate faster than you pay down the principal.

A common mistake is focusing only on the monthly payment and neglecting to calculate the total interest paid over 60 or 72 months. Always compare the full cost, not just the monthly figure, across different loan terms.

Who Are Mid-Term Loans Best For?

Mid-term loans are suitable for the majority of car buyers who need a balance between affordable monthly payments and a manageable total cost. If you have a stable income but don’t want the financial pressure of a very high monthly payment, or if you’re financing a moderately priced vehicle, a 60- or 72-month term is often a sensible choice.

Long-Term Loans: 84 Months and Beyond

Long-term loans, particularly those stretching to 84 months (seven years) or even longer, have become increasingly common, especially for more expensive vehicles. They offer the lowest possible monthly payments, but this comes at a significant financial cost.

The Allure of Extended Car Loan Years

The primary benefit of an 84-month loan is the significantly lower monthly payment. This can make higher-priced vehicles, like luxury cars or large SUVs, appear more affordable on a month-to-month basis. For some, it’s the only way to fit a desired vehicle into their budget.

From an expert perspective, while the low monthly payment can be tempting, long-term loans come with substantial risks that buyers often overlook in the excitement of a new car. It’s crucial to understand these risks before committing to such a lengthy term.

The Serious Drawbacks of Extended Car Loan Years

The most significant disadvantage of an 84-month loan is the dramatically higher total interest paid. Over such a long period, interest compounds, adding thousands, sometimes tens of thousands, to the overall cost of the vehicle. You’ll also be in debt for a much longer time, potentially tying up your budget for nearly a decade.

A critical risk is negative equity, often referred to as being "upside down" on your loan. Cars depreciate rapidly, especially in the first few years. With an 84-month loan, you’ll likely owe more than your car is worth for a significant portion of the loan term. This becomes a major problem if you need to sell the car or if it’s totaled in an accident, as your insurance payout might not cover the outstanding loan amount. Furthermore, the car will likely require significant maintenance and repairs towards the end of an 84-month term, potentially while you’re still making payments.

Common mistakes include falling into the trap of low monthly payments without considering the astronomical total cost or the high likelihood of being upside down. It’s a common strategy for dealerships to "stretch" the loan to make any car fit a buyer’s desired monthly payment, often to the buyer’s detriment.

Who Are Long-Term Loans Best For?

Frankly, long-term loans are rarely the "best" choice from a purely financial standpoint. They should be approached with extreme caution. They might be considered in very specific, limited scenarios, such as when financing a highly reliable vehicle with a substantial down payment, and you absolutely need the lowest monthly payment possible, understanding the higher overall cost and risks. Even then, I would strongly advise exploring all other options first.

Factors Influencing Your Ideal Car Loan Term

Choosing the perfect car loan years isn’t a one-size-fits-all decision. It’s a personal financial strategy that should be tailored to your unique circumstances. Several key factors will influence what loan term makes the most sense for you.

1. Budget & Monthly Payment Affordability

Your monthly budget is arguably the most critical factor. Before you even start looking at cars, you need to determine how much you can comfortably afford to pay each month without straining your finances. This isn’t just about the car payment; it includes insurance, fuel, maintenance, and any other car-related expenses.

Calculate your available funds and set a strict limit for your total monthly car expenses. Remember, a lower monthly payment on a longer term might seem appealing, but it can lead to financial regret down the road.

2. Interest Rates

Interest rates play a pivotal role in the total cost of your loan. Generally, shorter loan terms often come with slightly lower interest rates, as lenders perceive less risk over a shorter period. Conversely, longer terms might have higher interest rates, compounding the effect of the extended duration.

Even a small difference in interest rate can save or cost you hundreds, if not thousands, over the life of the loan. Always compare the Annual Percentage Rate (APR) across different loan terms and lenders.

3. Total Cost of the Loan

This is where many buyers make a crucial error. Focusing solely on the monthly payment blinds you to the true cost of your car. The total cost includes the principal amount borrowed plus all the accumulated interest.

Always calculate the total amount you will pay over the entire loan term for various options. This helps you visualize the real financial impact of choosing a 72-month loan over a 48-month one, even if the monthly payment difference seems small.

4. Vehicle Depreciation

Cars begin to depreciate the moment they leave the dealership lot, losing a significant portion of their value in the first few years. Depreciation is the silent killer in long-term loans.

With a long loan term, your car’s value can drop faster than you pay down the principal, putting you in a state of negative equity. This means you owe more on the car than it’s worth, which can be financially disastrous if you need to sell or if the car is totaled.

5. Your Financial Goals

Consider your broader financial goals. Are you saving for a down payment on a house, planning for retirement, or aiming to be debt-free quickly? A shorter car loan aligns better with rapid debt repayment and freeing up cash flow for other investments.

A longer loan, while offering lower monthly payments, keeps you in debt for an extended period, potentially delaying other important financial milestones. Align your car loan choice with your overarching financial strategy.

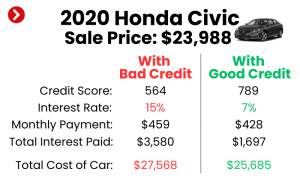

6. Credit Score

Your credit score significantly impacts the interest rate you qualify for, which in turn influences the affordability of different loan terms. Borrowers with excellent credit typically qualify for the lowest rates, making shorter terms more palatable.

A strong credit score gives you more flexibility and power in negotiating terms and rates. If your credit score is less than ideal, focusing on a shorter term might still be beneficial if you can manage the payments, as it reduces the overall interest burden that higher rates would impose.

7. Age of the Vehicle

Lenders often have restrictions on loan terms, particularly for used vehicles. It’s common for an 84-month loan to only be available for brand-new cars, or for used car loan terms to be capped at 60 or 72 months, depending on the car’s age and mileage.

The older the car, the less likely a lender is to offer an extended loan term due to increased risk of mechanical failure and further depreciation. Always check lender-specific policies.

8. Down Payment

A larger down payment directly reduces the amount you need to borrow, which can significantly impact your loan term options. A substantial down payment can enable you to choose a shorter loan term with a manageable monthly payment, or simply reduce your overall interest costs on any term.

Based on my experience, aiming for a down payment of at least 10-20% is a solid financial move. It immediately puts you in a better equity position and reduces the risk of being upside down.

Strategies for Choosing the Best Car Loan Years

Making an informed decision about your car loan years requires a strategic approach. Don’t rush into a decision based solely on the first monthly payment quoted by a dealer.

1. Calculate Everything

Don’t rely on mental math. Use online car loan calculators to compare different loan terms, interest rates, and down payment amounts. Input various scenarios (e.g., 48, 60, 72 months) to see how your monthly payment and total interest paid change.

This hands-on calculation empowers you to see the real numbers and understand the long-term financial implications of each choice.

2. Prioritize Total Cost Over Monthly Payment

This is perhaps the most crucial piece of advice. While the monthly payment is important for your budget, the total cost of the loan (principal + total interest) reveals the true expense of your car. Always aim to minimize this figure whenever possible.

A lower total cost means more money stays in your pocket, rather than going to the lender in interest payments.

3. Consider Your Lifestyle & Future Plans

Think beyond the immediate car purchase. How stable is your job? Are you planning to start a family, move, or make another large purchase in the next few years? A car loan is a multi-year commitment.

Ensure your chosen loan term fits comfortably within your expected financial stability and life plans. You don’t want a car payment to hinder future opportunities or create stress during life changes.

4. Build a Strong Down Payment

As discussed, a significant down payment is one of the best ways to improve your loan terms. It reduces your principal, lessens your monthly payments, and can even help you qualify for better interest rates.

Pro tip: Aim for at least 20% down, especially on new cars. This helps mitigate the impact of initial depreciation and reduces your time in negative equity.

5. Shop Around for Lenders

Never take the first loan offer you receive, especially from a dealership. Dealers often have preferred lenders, but they might not offer you the best rates or terms. Get pre-approved with several banks, credit unions, and online lenders before you even step foot in a dealership.

Shopping around for the best interest rate and loan terms can save you thousands over the life of the loan. For more detailed guidance, check out our article on How to Secure the Best Car Loan Rates (Internal Link Example).

6. Understand Add-ons

Be wary of add-ons like extended warranties, GAP insurance, or service contracts being rolled into your car loan. While some, like GAP insurance, might be wise for long terms, financing them increases your loan amount and thus your total interest paid.

Consider purchasing these separately or paying for them upfront if possible, to avoid adding to your principal balance and the interest you’ll pay on them over years.

7. The "Rule of 20/4/10"

A useful guideline to keep your car purchase financially sound is the "20/4/10 Rule." This suggests:

- 20% Down Payment: Put down at least 20% of the car’s purchase price.

- 4-Year Maximum Loan Term: Aim for a maximum loan term of four years (48 months).

- 10% of Gross Income for Car Expenses: Your total monthly car expenses (payment, insurance, fuel, maintenance) should not exceed 10% of your gross monthly income.

While not everyone can strictly adhere to this rule, it serves as an excellent benchmark for healthy car ownership. For more insights into this rule, you can check out financial resources like Investopedia’s explanation on car loan best practices.

Common Mistakes to Avoid When Choosing Car Loan Years

Even with the best intentions, car buyers often fall into common traps when selecting their loan term. Being aware of these pitfalls can help you steer clear of financial regret.

1. Focusing Solely on Monthly Payment

As emphasized, this is the biggest and most frequent mistake. A low monthly payment on an 84-month loan might seem affordable, but it masks a much higher total cost and extended debt. Always consider the total financial picture.

2. Ignoring Total Interest Paid

Many buyers don’t bother to calculate the total interest paid over the life of the loan. This oversight can lead to shock when they realize how much extra they’ve paid just for the privilege of stretching out payments.

3. Not Considering Depreciation

Failing to account for how quickly a car loses value is a recipe for negative equity. If your loan term is too long, you’ll be paying for a car that’s worth less than what you owe on it for an extended period.

4. Extending the Loan Term to Afford a More Expensive Car

This is a dangerous cycle. If you need to extend the loan term significantly just to afford the monthly payment of a particular car, it’s a clear sign that you’re buying more car than you can truly afford. Resist the temptation to stretch your budget this way.

5. Skipping the Down Payment

While some "no money down" offers are appealing, a zero down payment increases your principal, your monthly payments, and your total interest. It also puts you immediately into a negative equity position.

6. Not Shopping for Rates

Assuming your bank or the dealership offers the best rate is a common and costly mistake. Always compare offers from multiple lenders to ensure you’re getting the most competitive interest rate and terms.

7. Overlooking Additional Car Costs

Beyond the loan payment, remember to budget for insurance, fuel, routine maintenance, and potential repairs. A low monthly car payment won’t help if the total cost of ownership is unsustainable.

When to Reconsider Your Current Car Loan Term (Refinancing)

Even after choosing your initial car loan years, your financial situation or market conditions might change, making your original term less ideal. This is where refinancing comes in. Refinancing means taking out a new loan to pay off your existing car loan, potentially with new terms.

You might consider refinancing if:

- Interest Rates Have Dropped: If market rates have fallen since you took out your original loan, you could qualify for a lower APR.

- Your Credit Score Has Improved: A significantly better credit score can open doors to more favorable rates and terms.

- You Need to Lower Monthly Payments (with caution): If your financial situation has changed and you need to reduce your monthly outflow, refinancing to a longer term can lower payments. However, be mindful of the increased total interest.

- You Want to Shorten the Term and Save on Interest: If your income has increased, you might want to refinance to a shorter term to pay off the loan faster and save on interest.

Refinancing can be a powerful tool for optimizing your car loan. To learn more about this option, explore our guide: Is Refinancing Your Car Loan Right for You? (Internal Link Example).

Conclusion: Making Your Car Loan Years Work for You

Choosing the right car loan years is a pivotal decision that impacts your financial health for years to come. It’s a balance between managing your monthly budget and minimizing the total cost of your vehicle. While the allure of low monthly payments on long-term loans can be strong, exercising caution and prioritizing your long-term financial well-being is paramount.

By understanding the pros and cons of different loan terms, considering all influencing factors, and avoiding common mistakes, you can make an informed choice that aligns with your financial goals. Remember to always calculate the total cost, shop around for the best rates, and build a strong down payment. Your car purchase should be a source of convenience and enjoyment, not a financial burden. Drive smart, not just for show!