Car Loans 101: Your Ultimate Guide to Smart Vehicle Financing

Car Loans 101: Your Ultimate Guide to Smart Vehicle Financing Carloan.Guidemechanic.com

Buying a car is a significant life event for many, often marking a new chapter of independence or family convenience. While the excitement of a new set of wheels is palpable, the financial aspect – particularly securing a car loan – can feel daunting. This isn’t just about finding a vehicle; it’s about making a smart financial decision that impacts your budget for years to come.

As an expert blogger and professional SEO content writer, my goal with this comprehensive guide is to demystify the world of car loans. We’re going to break down every essential aspect, from understanding the basics to navigating complex terms, ensuring you’re empowered to make the best possible choice for your next vehicle purchase. Consider this your definitive "Car Loans 101" masterclass, designed to transform confusion into confidence.

Car Loans 101: Your Ultimate Guide to Smart Vehicle Financing

What Exactly is a Car Loan, and Why Does It Matter?

At its core, a car loan, also known as an auto loan or vehicle financing, is a secured loan specifically designed to help you purchase a car. When you take out a car loan, a lender provides you with the funds to buy the vehicle, and in return, you agree to repay that money, plus interest, over a predetermined period. The car itself typically serves as collateral for the loan. This means if you fail to make your payments, the lender has the legal right to repossess the vehicle.

Understanding this fundamental concept is crucial. It’s not just about getting the keys; it’s about entering into a serious financial agreement. Your ability to manage this loan will directly impact your financial health and credit score for years to come.

Most people rely on car loans because purchasing a vehicle outright with cash is often not feasible due to the significant cost involved. A car loan makes vehicle ownership accessible by spreading the expense over several months or years, making it manageable within a typical budget. It’s a tool that bridges the gap between your immediate cash availability and the price of your desired car.

Decoding the Language of Car Loans: Key Terminology You Must Know

Before diving into the application process, it’s essential to understand the jargon. Familiarity with these terms will not only help you comprehend loan offers but also empower you during negotiations.

- Principal: This is the initial amount of money you borrow to purchase the car. It’s the sticker price of the vehicle minus any down payment or trade-in value.

- Interest Rate: Expressed as a percentage, this is the cost of borrowing money. It’s what the lender charges you for the privilege of using their funds. A higher interest rate means you’ll pay more over the life of the loan.

- Annual Percentage Rate (APR): Often confused with the interest rate, the APR is a broader measure of the total cost of borrowing. It includes the interest rate plus any additional fees or charges associated with the loan, such as administrative fees. Always compare APRs when shopping for loans, as it gives you a more accurate picture of the total cost.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term usually results in lower monthly payments but often means you pay more in total interest over time.

- Down Payment: This is the upfront cash amount you pay towards the purchase of the car. A larger down payment reduces the principal you need to borrow, thereby lowering your monthly payments and the total interest paid.

- Trade-in Value: If you’re exchanging your current vehicle as part of the deal, its appraised value is deducted from the new car’s price, effectively acting like a down payment.

- Secured Loan: A car loan is a secured loan because the car itself acts as collateral. This provides security for the lender; if you default on the loan, they can repossess the vehicle.

Based on my experience, many people get caught off guard by the difference between interest rate and APR. Always ask for the APR to get the full picture of your borrowing cost.

Laying the Groundwork: Essential Preparations Before You Apply

The key to a successful car loan experience lies in thorough preparation. Don’t walk into a dealership or bank without doing your homework.

1. How Much Can You Truly Afford? Beyond the Monthly Payment

This is perhaps the most critical step. It’s tempting to focus solely on the monthly payment, but that’s a narrow view. You need to consider the total cost of vehicle ownership. This includes not just the loan payment, but also insurance, fuel, maintenance, registration fees, and potential repairs.

Pro tips from us: Create a detailed budget. Factor in your current income, fixed expenses (rent, utilities, existing loans), and variable expenses (groceries, entertainment). Once you have a clear picture of your disposable income, you can realistically determine a comfortable monthly car payment that won’t strain your finances. Aim for a payment that allows you to still save money and manage unexpected expenses.

2. Your Credit Score: The Ultimate Game Changer

Your credit score is a three-digit number that profoundly influences the interest rate you’ll be offered on a car loan. Lenders use it to assess your creditworthiness – essentially, how likely you are to repay your debts. A higher credit score (generally above 700) indicates less risk to lenders, often leading to significantly lower interest rates and more favorable loan terms. Conversely, a lower score can result in higher rates or even loan denial.

Before applying, check your credit report from all three major bureaus (Equifax, Experian, TransUnion). Look for any errors and dispute them promptly. If your score is lower than you’d like, focus on improving it by paying bills on time, reducing outstanding debt, and avoiding new credit applications for a few months. For a deeper dive into credit scores, consider reading our article on .

3. The Power of a Down Payment

Making a substantial down payment is one of the smartest moves you can make when financing a car. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. A larger down payment also builds immediate equity in the vehicle, reducing the risk of being "upside down" on your loan (owing more than the car is worth).

Common mistakes to avoid are skipping a down payment entirely or making a very small one. While it might seem appealing to preserve cash, it often costs you more in the long run. Aim for at least 10-20% of the car’s purchase price if possible.

4. Maximizing Your Trade-in Value

If you have an existing vehicle you plan to trade in, treat it like a separate transaction. Research its market value using reputable online tools like Kelley Blue Book (KBB) or Edmunds. Have your car cleaned, address minor repairs, and gather maintenance records. This preparation can significantly boost its trade-in value, which then acts as additional capital towards your new purchase, much like a down payment.

Don’t simply accept the first trade-in offer. Be prepared to negotiate, and even consider selling your old car privately if the dealership’s offer is too low.

5. Understanding Your Debt-to-Income Ratio (DTI)

Lenders look at your Debt-to-Income (DTI) ratio to gauge your ability to manage monthly payments. This ratio is calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your total monthly debt (including your prospective car payment) is $1,500 and your gross monthly income is $4,000, your DTI is 37.5%. Lenders generally prefer a DTI of 36% or lower, though some may approve loans with a DTI up to 43%.

A high DTI can signal to lenders that you might be overextended, potentially leading to higher interest rates or loan denial. If your DTI is high, consider paying down other debts before applying for a car loan.

Navigating Your Financing Options: Where to Get Your Loan

You have several avenues for securing a car loan, and it’s always wise to explore multiple options before committing.

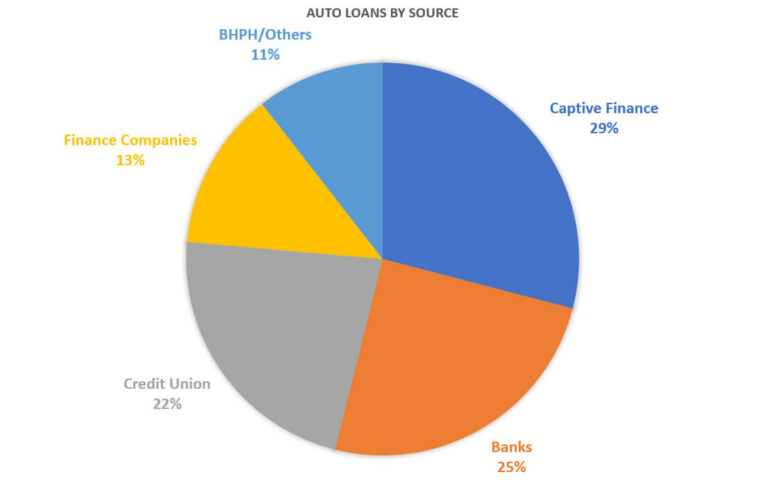

1. Dealership Financing

Most dealerships offer on-site financing, often through relationships with various banks and captive finance companies (e.g., Ford Credit, Toyota Financial Services). This can be convenient, as you can handle the car purchase and financing in one place. Dealerships might also offer special manufacturer incentives like 0% APR or low-interest rates on new cars.

However, be aware that dealership financing might not always be the best deal. They sometimes mark up interest rates to earn a profit, and the focus might be more on selling you the car than securing the absolute best loan terms for you. Always compare their offer with pre-approvals you’ve obtained elsewhere.

2. Banks and Credit Unions

Traditional banks and local credit unions are excellent sources for car loans. They often offer competitive interest rates, especially to their existing members or customers with strong credit. Credit unions, being not-for-profit, are particularly known for their favorable rates and personalized service.

Pro tips from us: Apply for pre-approval with your bank or credit union before you even step foot in a dealership. This gives you a clear understanding of the interest rate and loan terms you qualify for, providing a powerful negotiation tool.

3. Online Lenders

A growing number of online lenders specialize in auto loans. These platforms often offer quick application processes, competitive rates, and the convenience of applying from anywhere. They can be particularly useful for comparing multiple offers in a short amount of time. Websites like LightStream or Capital One Auto Finance are examples of reputable online options.

When considering online lenders, always ensure they are legitimate and have a strong reputation. Read reviews and verify their licensing.

4. Manufacturer Financing Incentives

Automakers frequently offer special financing deals, especially on new models or to clear out older inventory. These can include incredibly low-interest rates (sometimes 0% APR for qualified buyers) or cash-back rebates. While attractive, these offers often require excellent credit, and you might have to choose between a low APR and a cash rebate – you typically can’t have both.

Carefully evaluate if these incentives truly benefit you, or if a slightly higher interest rate from an independent lender, combined with a larger cash discount on the car, might be a better overall deal.

5. Options for Bad Credit Car Loans

Even if your credit score isn’t perfect, there are still options for securing a car loan. However, expect to pay a higher interest rate to offset the increased risk for the lender. Subprime lenders specialize in loans for individuals with lower credit scores.

In these situations, a larger down payment becomes even more crucial. Consider finding a co-signer with good credit, which can help you qualify for better terms. Be very cautious and read all the fine print, as these loans often come with stricter terms and higher fees. The goal should be to get a reliable car to rebuild your credit, then potentially refinance later.

The Application Process: Step-by-Step to Your New Car

Once you’ve done your homework and explored financing options, it’s time to apply.

1. The Power of Pre-Approval

Getting pre-approved for a car loan is perhaps the most strategic move you can make. It means a lender has already reviewed your financial information and approved you for a specific loan amount at a certain interest rate, contingent on the final car selection. This process involves a "soft" credit pull, which doesn’t negatively impact your credit score.

Why it’s crucial:

- Budget Clarity: You know exactly how much car you can afford before you start shopping.

- Negotiating Power: You walk into the dealership as a cash buyer, knowing you have your own financing. This shifts the focus from your monthly payment to the actual price of the car.

- Faster Process: It streamlines the buying experience at the dealership.

2. Gathering Your Documents

Whether you’re applying for pre-approval or a final loan, lenders will require specific documentation to verify your identity, income, and financial stability. Common documents include:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, tax returns if self-employed)

- Proof of residence (utility bill, lease agreement)

- Social Security number

- Information about the vehicle you intend to purchase (make, model, VIN if known)

Having these ready will significantly speed up the application process.

3. Understanding the Loan Offer: Beyond the Monthly Number

When you receive a loan offer, look beyond the attractive monthly payment. Scrutinize the APR, the loan term, and any associated fees. A lower monthly payment achieved by extending the loan term might seem appealing, but it often means paying significantly more in total interest over time.

Common mistakes to avoid: Don’t let a salesperson "stretch" the loan term just to hit a desired monthly payment. Always calculate the total cost of the loan (principal + total interest) for different terms.

4. Negotiating the Deal: Car Price AND Loan Terms

Remember, everything is negotiable – not just the car’s price, but also the loan terms. With a pre-approval in hand, you can negotiate the car price as if you’re paying cash. Once you’ve settled on a price, you can then compare your pre-approved loan offer with any financing options the dealership presents. If the dealership can beat your pre-approval’s APR, great! If not, stick with your external financing. For more negotiation tips, check out our article on .

Different Strokes for Different Folks: Types of Car Loans

The type of car you buy can also influence your loan options and terms.

1. New Car Loans

Loans for new vehicles generally come with the most favorable interest rates and longer terms. Lenders see new cars as less risky because they typically hold their value better initially and are less prone to immediate mechanical issues. Manufacturer incentives are also more common with new car purchases.

2. Used Car Loans

Used car loans typically have slightly higher interest rates than new car loans, and sometimes shorter loan terms. This is because used cars are considered a higher risk by lenders; their value depreciates more rapidly, and they may have a higher likelihood of mechanical problems. The age and mileage of the used car can also impact the loan terms.

3. Refinancing Your Car Loan

Refinancing means taking out a new loan to pay off your existing car loan. People typically refinance to get a lower interest rate, reduce their monthly payment, or change the loan term. This can be a smart move if your credit score has improved since you initially took out the loan, if interest rates have dropped, or if you simply found a better offer elsewhere.

When to consider refinancing:

- Your credit score has significantly improved.

- Market interest rates have decreased.

- You initially got a high-interest loan (e.g., with bad credit).

- You want to lower your monthly payment (though beware of extending the term too much).

Before refinancing, compare potential savings against any fees associated with the new loan.

Common Mistakes to Avoid on Your Car Loan Journey

Navigating the car loan process can be tricky, and many common pitfalls can lead to costly errors. Based on my experience, these are the most frequent mistakes:

- Focusing Only on the Monthly Payment: As discussed, this is a dangerous trap. A low monthly payment can hide a high interest rate or an excessively long loan term, leading to you paying much more overall. Always look at the total cost.

- Not Getting Pre-Approved: Without a pre-approval, you lose significant negotiation leverage at the dealership and might accept whatever financing they offer, which may not be the best for you.

- Skipping a Down Payment: While not always possible, avoiding a down payment means borrowing more, paying more interest, and increasing the risk of being upside down on your loan.

- Ignoring the Total Cost of the Loan: Always calculate the total amount you will pay over the loan’s life (principal + total interest). A slight difference in APR can translate to thousands of dollars.

- Falling for Unnecessary Add-ons: Dealerships often try to sell extended warranties, GAP insurance (Guaranteed Asset Protection), paint protection, and other add-ons. While some might be beneficial (like GAP insurance if you make a small down payment), many are overpriced or unnecessary. Research each add-on carefully and don’t be pressured into buying them.

Pro Tips for a Smooth and Smart Car Loan Journey

Here are some additional insights to ensure your car loan experience is as positive and cost-effective as possible:

- Read the Fine Print, Every Single Word: Before signing any document, thoroughly read the entire loan agreement. Understand all clauses, fees, and penalties for late payments or early payoff. If something is unclear, ask for clarification. Don’t be rushed.

- Shop Around for Rates (Within a Short Window): When getting pre-approvals, apply to multiple lenders within a 14-45 day window. Credit bureaus typically count all "hard inquiries" for the same type of loan within this period as a single inquiry, minimizing the impact on your credit score. This allows you to compare offers without penalty.

- Consider a Shorter Loan Term if Possible: While a longer term means lower monthly payments, a shorter term (e.g., 48 or 60 months instead of 72 or 84) will save you significant money in interest. If your budget allows for the higher monthly payment, it’s almost always the financially smarter choice.

- Build an Emergency Fund: Unexpected car repairs can derail your budget. Having an emergency fund specifically for vehicle-related issues can prevent you from missing loan payments or incurring additional debt.

- Understand GAP Insurance: If you make a small down payment or no down payment, your car might depreciate faster than you pay off the loan. In case of a total loss (theft or accident), your insurance payout might be less than what you still owe. GAP insurance covers this "gap." Decide if it’s necessary for your situation; you might be able to get it cheaper from your auto insurer than the dealership. For more general financial guidance, the Consumer Financial Protection Bureau (CFPB) offers excellent resources on auto loans: https://www.consumerfinance.gov/consumer-tools/auto-loans/

The Road Ahead: Empowered Car Buying

Securing a car loan doesn’t have to be a stressful ordeal. By understanding the fundamentals, preparing thoroughly, exploring your options, and avoiding common pitfalls, you can navigate the process with confidence. This "Car Loans 101" guide has provided you with the knowledge to make informed decisions, ensuring your next vehicle purchase is not just exciting, but also financially sound.

Remember, the goal isn’t just to get approved for a loan, but to secure the best possible terms that align with your financial health. Armed with this comprehensive information, you’re now ready to drive off into the sunset, knowing you’ve made a smart choice for your future. Happy driving!