Car Loans for Bad Credit No Credit Check: Your Ultimate Guide to Navigating Auto Financing with Confidence

Car Loans for Bad Credit No Credit Check: Your Ultimate Guide to Navigating Auto Financing with Confidence Carloan.Guidemechanic.com

Finding yourself in need of a car but facing the hurdle of bad credit or even no credit history at all can feel like navigating a maze blindfolded. The phrase "car loans for bad credit no credit check" often pops up as a beacon of hope, promising an easy solution to a complex problem. But is it truly the straightforward answer it appears to be? Or are there nuances and pitfalls you need to understand?

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing. Based on my experience, securing a car loan when your credit score isn’t ideal is absolutely possible. However, the "no credit check" part requires careful scrutiny. This comprehensive guide will demystify the process, explain your options, and equip you with the knowledge to make the best financial decisions, ensuring you drive away with a vehicle without getting taken for a ride.

Car Loans for Bad Credit No Credit Check: Your Ultimate Guide to Navigating Auto Financing with Confidence

Understanding the Landscape: The Reality of "No Credit Check" Car Loans

When you see "no credit check" advertised, it’s natural to feel a sense of relief, especially if your credit history is less than stellar. The reality, however, is often more complex than the simple phrase suggests. Traditional lenders, like major banks and credit unions, almost always perform a credit check to assess your financial risk. This check helps them determine your interest rate, loan terms, and ultimately, whether they’ll approve your application.

The concept of "no credit check" car loans primarily refers to specific types of lenders who operate outside the conventional banking system. These lenders often focus on factors other than your credit score, such as your income, employment stability, and the amount of your down payment. While this can be a lifeline for many, it’s crucial to understand the implications and potential trade-offs.

Why "No Credit Check" is Rarely What It Seems

Most legitimate financial institutions, even those specializing in subprime lending (loans for individuals with less-than-perfect credit), will conduct some form of credit assessment. This isn’t always a hard inquiry that significantly dings your score, but they will look at your financial history. The true "no credit check" scenario is usually limited to a very specific type of dealership, which we’ll explore in detail.

The reason lenders check credit is fundamental to their business model: risk management. Your credit report provides a snapshot of your past borrowing and repayment behavior. It tells them how likely you are to repay a new loan. Without this information, lenders face a higher risk, which they typically offset by charging higher interest rates or requiring more stringent terms.

Why Your Credit Score Matters (Even When It Seems Not To)

Before diving into the "no credit check" options, it’s vital to understand why your credit score holds so much weight in the financial world. Your credit score, typically a FICO or VantageScore, is a three-digit number that summarizes your creditworthiness. It’s built upon your payment history, the amounts you owe, the length of your credit history, new credit, and your credit mix.

A higher credit score signals to lenders that you are a responsible borrower, making you a lower risk. This translates directly into better loan terms, including lower interest rates and more flexible repayment schedules. Even if you’re exploring "no credit check" options, being aware of your credit score’s impact can help you understand the potential costs and prepare for the future.

The Real Impact on Your Wallet

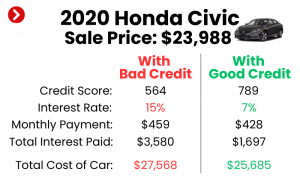

When your credit score is low, lenders perceive a higher risk of default. To compensate for this risk, they will offer loans with higher Annual Percentage Rates (APRs). A higher APR means you’ll pay significantly more interest over the life of the loan. For example, a difference of just a few percentage points in your interest rate can add thousands of dollars to the total cost of a car over a five-year loan term.

Beyond interest rates, a poor credit score can also affect other aspects of your loan. You might be required to make a larger down payment, accept a shorter loan term (leading to higher monthly payments), or even be limited in your choice of vehicles. Understanding this impact is the first step toward making an informed decision, even if you ultimately choose a "no credit check" path.

Navigating the Options: Where to Find Car Loans for Bad Credit

If traditional bank loans feel out of reach, don’t despair. Several avenues exist for individuals with bad credit or no credit history to secure vehicle financing. It’s about knowing where to look and what to expect from each option.

1. Buy-Here-Pay-Here (BHPH) Dealerships: The Closest to "No Credit Check"

Buy-here-pay-here dealerships are often the first place people turn when they explicitly search for "no credit check" car loans. These dealerships are unique because they act as both the car seller and the lender. Instead of arranging financing through a third-party bank or credit union, you make your payments directly to the dealership itself.

How They Work:

BHPH dealerships typically don’t rely on traditional credit scores to approve loans. Instead, they focus heavily on your income and employment stability. They want to ensure you have a consistent source of income that can cover the monthly payments. You’ll likely need to provide pay stubs, bank statements, and proof of residency.

Pros:

- High Approval Rates: For those with very poor credit or no credit history, BHPH dealerships offer a significantly higher chance of approval.

- Quick Process: The approval process can be very fast, sometimes allowing you to drive off the lot the same day.

- Focus on Income: If you have stable income but poor credit, this model can work in your favor.

Cons:

- Higher Interest Rates: This is the most significant drawback. To offset the increased risk, BHPH loans almost always come with much higher interest rates, often at the maximum legal limit in your state.

- Limited Vehicle Selection: You’re restricted to the inventory available on their lot, which may consist of older, higher-mileage vehicles.

- Less Flexible Terms: Loan terms can be rigid, and you might have less room for negotiation.

- Credit Reporting Varies: Some BHPH dealerships do not report your payments to major credit bureaus. While this might seem appealing initially (no credit check), it means making on-time payments won’t help you build or rebuild your credit score, which is a common mistake to avoid if your goal is long-term financial improvement. Pro tips from us: Always ask if they report to all three major credit bureaus.

When to Consider BHPH:

Based on my experience, BHPH dealerships should be considered a last resort. They can be a viable option if you absolutely need a car, have exhausted all other possibilities, and can comfortably afford the high payments. However, be prepared for a higher overall cost of ownership.

2. Subprime Lenders & Specialized Auto Financiers

These lenders specialize in providing car loans to individuals with less-than-perfect credit. While they do conduct credit checks, their approval criteria are more flexible than traditional banks. They understand that people can have financial setbacks and are willing to look beyond a low credit score.

What They Look For:

Subprime lenders take a holistic view of your financial situation. They’ll assess your:

- Income Stability: Proof of consistent employment and income.

- Debt-to-Income Ratio: How much of your income goes towards existing debt payments.

- Down Payment: A larger down payment significantly reduces their risk and can improve your chances of approval and secure a better rate.

- Credit History Details: They’ll examine your credit report not just for the score, but for patterns. Are there recent bankruptcies or foreclosures, or is it a history of missed credit card payments?

Pros:

- Wider Vehicle Selection: You’re not limited to a single dealership’s inventory; you can often get financing through these lenders at various dealerships.

- Credit Building Opportunity: Most subprime lenders report payments to credit bureaus, allowing you to improve your credit score with on-time payments.

- Potentially Better Rates: While still higher than prime rates, they are generally more competitive than BHPH dealerships.

Cons:

- Higher Interest Rates: Rates will still be higher than for borrowers with good credit.

- Stricter Requirements: You might need a significant down payment or a co-signer.

Pro tips from us: Research reputable subprime lenders online or ask trusted dealerships which subprime lenders they work with. Look for lenders with good customer reviews and transparent terms.

3. Credit Unions: A Member-Focused Approach

Credit unions are non-profit financial cooperatives owned by their members. Because of their member-focused structure, they often have more flexible lending criteria than traditional banks, especially for those with bad credit.

How They Help:

If you’re already a member of a credit union, or if you can join one, it’s worth exploring their auto loan options. They might be more willing to work with you, even with a lower credit score, particularly if you have a long-standing relationship with them or if you can demonstrate a commitment to improving your financial situation.

Pros:

- Potentially Lower Rates: Credit unions are known for offering competitive interest rates, even to those with less-than-perfect credit, as their goal isn’t profit maximization.

- Personalized Service: You might receive more personalized advice and support during the application process.

- Flexible Terms: They may be more open to negotiating terms or offering alternative solutions.

Cons:

- Membership Required: You typically need to be a member to qualify for a loan.

- Credit Check Still Likely: While flexible, they will still conduct a credit check.

4. Online Loan Marketplaces

Online platforms connect borrowers with multiple lenders, including those specializing in bad credit auto loans. These marketplaces allow you to submit one application and receive several offers, making it easier to compare rates and terms.

How They Work:

You fill out a single pre-qualification form, which often results in a soft credit inquiry (no impact on your credit score). Lenders then review your information and present conditional offers. This allows you to shop around without multiple hard inquiries hitting your credit report.

Pros:

- Convenience: Apply from home and compare offers easily.

- Multiple Offers: Get various loan options quickly.

- Pre-qualification: See potential rates without affecting your credit score initially.

Cons:

- Still a Credit Check for Final Approval: Once you choose a lender, they will perform a hard credit inquiry for final approval.

- Potential for Information Overload: You might receive many offers, requiring careful review.

Preparing for Your Car Loan Application (Even with Bad Credit)

Regardless of where you apply, being prepared can significantly improve your chances of approval and help you secure the best possible terms. This is especially true when dealing with bad credit.

1. Save for a Down Payment

This is perhaps the single most impactful step you can take. A substantial down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. It also shows the lender that you are financially committed to the purchase.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price. A larger down payment can often lead to lower interest rates and more favorable loan terms, even with bad credit. It also lowers your monthly payments, making the loan more affordable.

2. Create a Realistic Budget

Before you even look at cars, sit down and honestly assess your finances. How much can you truly afford each month for a car payment, insurance, fuel, and maintenance? Common mistakes to avoid are overestimating your budget and getting emotionally attached to a car you can’t afford.

Remember, a car loan isn’t just about the monthly payment; it’s about the total cost of ownership. Use a budget planner to track your income and expenses diligently.

3. Gather Necessary Documentation

Lenders will require proof of your financial stability. Prepare the following documents in advance:

- Proof of Income: Recent pay stubs (last 2-3 months), tax returns (if self-employed), bank statements.

- Proof of Residence: Utility bills, lease agreement, or mortgage statements.

- Proof of Identity: Driver’s license or state ID.

- References: Sometimes required, especially by BHPH dealerships.

4. Consider a Trade-In

If you have an existing vehicle, trading it in can act as a down payment. The value of your trade-in reduces the amount you need to finance, making your loan more manageable. Get an estimate of your car’s value beforehand using online tools like Kelley Blue Book or Edmunds.

5. Explore a Co-signer

If you have a trusted family member or friend with good credit who is willing to co-sign your loan, this can significantly increase your chances of approval and potentially secure a much lower interest rate. A co-signer’s creditworthiness provides an additional layer of security for the lender.

Important Note: A co-signer is equally responsible for the loan. If you miss payments, it negatively impacts their credit score, and they will be legally obligated to make the payments. Only consider this option if you are confident in your ability to repay the loan and have open communication with your co-signer.

6. Understand Loan Terms

Before signing anything, fully understand the loan’s Annual Percentage Rate (APR), the loan term (how many months you’ll be paying), and the total cost of the loan. Don’t just focus on the monthly payment. A longer loan term might mean lower monthly payments but will result in paying significantly more in interest over time.

Pro Tips for Securing the Best Possible Deal

Even with bad credit, you have leverage if you approach the car buying process strategically.

- Get Pre-Approved: Seek pre-approval from multiple lenders (credit unions, subprime lenders, online marketplaces) before stepping onto a dealership lot. Pre-approval gives you a clear idea of how much you can borrow, at what interest rate, and empowers you to negotiate the car price as a cash buyer. This separation of car price negotiation from financing negotiation is a powerful strategy.

- Shop Around for Loan Offers: Don’t take the first offer you receive. Compare interest rates, fees, and terms from at least three different lenders. This competition can save you a significant amount of money over the life of the loan.

- Negotiate the Car Price, Not Just the Loan: Remember, the dealership makes money on both the car sale and the financing. Focus on getting the best price for the vehicle first. Once you’ve agreed on a price, then discuss financing options, ideally with your pre-approved offer in hand.

- Avoid Unnecessary Add-ons: Dealerships often try to sell extended warranties, paint protection, or other add-ons. While some might be valuable, many are overpriced and can significantly increase your loan amount and total cost. Be firm in declining anything you don’t genuinely need or can’t afford.

- Read the Fine Print: Before signing any documents, read every line carefully. Understand all terms, conditions, and any hidden fees. If anything is unclear, ask for clarification until you fully grasp it. Common mistakes to avoid are rushing the paperwork and not understanding your obligations. For additional insights on consumer protection, you might find valuable resources at the Consumer Financial Protection Bureau (CFPB).

The Long-Term Game: Rebuilding Credit Through Your Car Loan

One of the most valuable aspects of securing a car loan, even with bad credit, is the opportunity it presents for credit rebuilding. If your lender reports your payment history to the major credit bureaus (Equifax, Experian, and TransUnion), making timely payments can significantly improve your credit score over time.

This improvement can open doors to better financial products in the future, such as lower interest rates on credit cards, mortgages, or even future car loans. It’s a powerful cycle: you get a car you need, and you simultaneously build a stronger financial foundation. Common mistakes to avoid are missing payments, paying late, or defaulting on the loan, as these actions will further damage your credit and can lead to vehicle repossession.

For more detailed strategies on improving your credit score, you might find our article, "How to Boost Your Credit Score: A Step-by-Step Guide," particularly helpful. (Internal Link Example)

Alternatives to "No Credit Check" Car Loans

While getting a loan for a car is often the goal, it’s worth considering alternatives, especially if the terms of available "no credit check" loans seem too burdensome.

- Save Up for a Cheaper Car: If you can delay your purchase, saving up cash for an older, reliable used car can prevent you from taking on high-interest debt.

- Public Transportation/Ridesharing: Explore if public transport or ridesharing services can meet your needs temporarily.

- Borrow from Family/Friends: If possible, borrowing from a trusted loved one can offer more flexible terms and potentially no interest, but ensure you have a clear repayment agreement in place to avoid damaging relationships.

Conclusion: Drive Smart, Not Just Drive

Navigating the world of car loans with bad credit or no credit history can be challenging, but it is far from impossible. While the allure of "no credit check" loans is strong, it’s essential to understand the underlying realities and potential costs. By exploring options like BHPH dealerships, specialized subprime lenders, credit unions, and online marketplaces, you can find a path to car ownership.

The key to success lies in preparation, informed decision-making, and a commitment to understanding all the terms and conditions. Focus on what you can afford, aim for a significant down payment, and always shop around for the best possible deal. Remember, a car loan isn’t just about getting a vehicle; it’s an opportunity to rebuild your financial standing. Make wise choices today, and you’ll not only drive away in a car but also on the road to a stronger financial future.

If you’re looking to delve deeper into understanding various loan types and their implications, our article on "Decoding Car Loan Interest Rates: What You Need to Know" could provide further valuable insights. (Internal Link Example) Take control of your financial journey, and make your car loan a stepping stone, not a stumbling block.