Car Loans For Everyone: Your Ultimate Guide to Driving Away with Confidence

Car Loans For Everyone: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

The dream of owning a car is a universal one, offering freedom, convenience, and access to opportunities. However, for many, the path to car ownership often feels paved with complex financial hurdles, particularly when it comes to securing a car loan. It’s a common misconception that only those with pristine credit scores and substantial savings can qualify.

But what if we told you that car loans are truly for everyone, regardless of your financial background? This comprehensive guide will demystify the world of auto financing, providing you with the knowledge and strategies needed to secure the best possible car loan, even if you have bad credit, no credit, or a unique financial situation. Our ultimate goal is to empower you to drive away with confidence, knowing you’ve made an informed decision.

Car Loans For Everyone: Your Ultimate Guide to Driving Away with Confidence

Why Car Ownership Remains a Cornerstone of Modern Life

Having a personal vehicle isn’t just a luxury; for many, it’s a necessity. It provides reliable transportation for work, allows you to manage family responsibilities, and opens up possibilities for leisure and travel that public transport simply can’t match. The ability to commute independently can significantly impact your career prospects and overall quality of life.

Beyond daily commutes, a car offers unparalleled flexibility. Imagine spontaneous road trips, weekend adventures, or simply the peace of mind knowing you can get where you need to go, whenever you need to. This foundational role in daily life makes understanding car financing incredibly important for a vast majority of people.

Demystifying Car Loans: The Basics You Need to Know

Before diving into the specifics of qualifying, let’s establish a clear understanding of what a car loan entails. At its core, a car loan is an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that money, plus interest, over a set period.

Key Terms Explained

Understanding the terminology is crucial. The principal is the actual amount of money you borrow for the car. The interest rate is the cost of borrowing that money, expressed as a percentage. This rate directly impacts how much you’ll pay back in total.

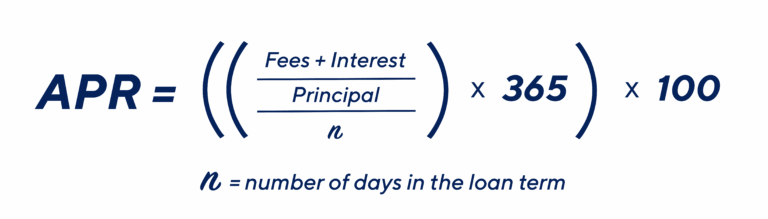

The loan term refers to the duration over which you’ll repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). Finally, the Annual Percentage Rate (APR) is the true annual cost of your loan, including not just the interest rate but also any additional fees. Based on my experience, focusing solely on the interest rate can be misleading; always compare APRs for an accurate picture.

Who Can Get a Car Loan? Dispelling Common Myths

The notion that car loans are exclusive to a select few is simply untrue. While having excellent credit certainly makes the process smoother and often leads to better terms, there are viable options for almost everyone. This section will break down the possibilities for various financial profiles.

For Good Credit Borrowers: The Easiest Path

If you have a strong credit history, typically a FICO score of 670 or above, you’re in an excellent position. Lenders view you as a low-risk borrower, making you eligible for the lowest interest rates and most flexible loan terms. Your application process will likely be straightforward, with quick approvals.

Even with good credit, it’s vital to shop around. Don’t settle for the first offer. Pro tips from us include comparing offers from multiple lenders to ensure you’re getting the most competitive rate available.

For Bad Credit Borrowers: Hope is Not Lost!

Having a low credit score (typically below 580) can make securing a car loan more challenging, but it is absolutely possible. Many lenders specialize in bad credit car loans, understanding that financial setbacks happen. These loans might come with higher interest rates to offset the increased risk for the lender, but they serve as a crucial pathway to car ownership and, more importantly, an opportunity to rebuild your credit.

Common mistakes to avoid are feeling discouraged and not exploring all your options. Focus on demonstrating stability in other areas of your finances.

For No Credit History Borrowers: First-Time Buyers Welcome

If you’re young, new to the country, or simply haven’t had the need for credit before, you might find yourself with no credit history. This "thin file" can be just as tricky as bad credit, as lenders have no track record to assess your repayment reliability. However, no credit car loans are specifically designed for this demographic.

Many lenders offer first-time car buyer loans or programs. These often require a larger down payment or a co-signer, but they provide an essential entry point into the credit world. This is your chance to establish a positive credit history.

For Self-Employed Borrowers: Navigating Income Verification

Being self-employed brings unique challenges when applying for a loan, primarily around income verification. Lenders prefer stable, predictable income, which can be harder to demonstrate for freelancers or business owners. However, with the right documentation, such as tax returns, bank statements, and profit and loss statements, you can prove your financial stability.

It’s crucial to be organized and transparent with your financial records. Showing consistent income over several years will significantly strengthen your application.

Factors Lenders Consider for Car Loan Approval

Lenders assess several key indicators to determine your eligibility and the terms of your car loan. Understanding these factors can help you prepare your application and improve your chances of approval.

Your Credit Score: The Big One

Your credit score is often the first thing lenders look at. It’s a numerical representation of your creditworthiness, based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score indicates a lower risk.

It’s highly recommended to check your credit score and report before applying. You can get a free copy of your credit report annually from each of the three major credit bureaus. Addressing any inaccuracies beforehand is a pro tip that can save you a lot of hassle. (Internal Link Placeholder)

Debt-to-Income Ratio (DTI)

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to take on additional debt. A lower DTI ratio indicates you have more disposable income to cover your car loan payments.

Generally, lenders prefer a DTI ratio of 43% or lower, though this can vary. A high DTI might signal that you’re already stretched thin financially.

Employment Stability

Lenders want to see a consistent employment history. Long-term employment with the same employer demonstrates stability and a reliable income stream, which reassures lenders of your ability to make regular payments. Frequent job changes or gaps in employment might raise red flags.

If you’ve recently started a new job, be prepared to provide pay stubs or an offer letter confirming your new income.

Down Payment: Your Upfront Investment

Making a significant down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. It also signals to lenders that you are serious about your purchase and have some financial discipline.

Based on my experience, a down payment of at least 10-20% is ideal, especially for those with less-than-perfect credit, as it can significantly improve your chances of approval and secure better terms.

Vehicle Type and Age

The type and age of the vehicle you wish to purchase can also influence loan approval. Newer, more reliable vehicles often qualify for better loan terms because they hold their value longer and are less likely to require costly repairs that could jeopardize your ability to make payments. Older, higher-mileage vehicles are considered higher risk.

Lenders also consider the resale value of the car as collateral. If you default, they want to ensure they can recoup their losses.

Co-signer: A Helping Hand

If you have bad credit or no credit, a co-signer with good credit can significantly boost your application. A co-signer agrees to be legally responsible for the loan if you fail to make payments. This reduces the risk for the lender, potentially allowing you to get approved or secure a lower interest rate.

However, it’s crucial for both parties to understand the implications. If you default, your co-signer’s credit will also be negatively impacted.

Types of Car Loans and Where to Find Them

The landscape of car loans is diverse, offering various avenues to financing. Knowing where to look and what each option entails is key to finding the right fit for your needs.

Direct Lenders: Banks, Credit Unions, and Online Lenders

Direct lenders are financial institutions that lend money directly to consumers. This category includes traditional banks, local credit unions, and modern online lenders.

- Banks: Offer competitive rates for borrowers with good credit. They have established processes and often provide personalized service.

- Credit Unions: Known for their member-focused approach and often lower interest rates, especially for those with average credit. They prioritize their members’ financial well-being.

- Online Lenders: Have revolutionized the lending space. They offer quick applications, fast approvals, and often cater to a wider range of credit scores, including those with bad or no credit. Their streamlined process can be very appealing.

Pro tips from us suggest getting pre-approved from a direct lender before visiting a dealership. This gives you negotiating power and a clear budget.

Dealership Financing: Convenience vs. Cost

Many car dealerships offer financing options directly through their sales departments. They act as intermediaries, working with a network of lenders to find you a loan. This can be incredibly convenient, allowing you to complete the car purchase and financing in one place.

However, convenience can sometimes come at a cost. Dealerships might mark up interest rates to earn a commission. While they can sometimes offer special manufacturer incentives, it’s always wise to compare their offer with pre-approvals you’ve obtained elsewhere.

Specialty Lenders: For Unique Financial Situations

For individuals with particularly challenging credit histories, specialty lenders or subprime lenders exist. These lenders focus specifically on bad credit car loans and no credit car loans. They are often more flexible with their lending criteria but typically charge higher interest rates to compensate for the increased risk.

While the rates might be higher, these lenders provide a valuable service, enabling car ownership for those who might otherwise be denied. Always read the terms and conditions carefully with any lender, but especially with specialty lenders.

The Step-by-Step Process to Secure a Car Loan

Navigating the car loan process can seem daunting, but breaking it down into manageable steps makes it much simpler. Follow this guide for a smooth journey.

Step 1: Assess Your Financial Health

Before you even look at cars, take a good, hard look at your finances. What’s your income? What are your fixed expenses? What’s your current debt load? This will help you understand how much you can realistically afford for a monthly car payment, insurance, and maintenance.

Checking your credit report and score at this stage is also crucial. Knowing where you stand financially is the first and most important step.

Step 2: Determine Your Budget

Once you know your financial capacity, set a realistic budget for the car itself. Remember, the car loan payment is only one part of car ownership. Factor in insurance, fuel, maintenance, and potential repair costs. (Internal Link Placeholder)

Common mistakes to avoid are focusing solely on the monthly payment and overlooking the total cost of ownership. A lower monthly payment spread over a longer term can mean paying significantly more in interest.

Step 3: Get Pre-Approved (Crucial Step!)

This is perhaps the most powerful step in the entire process. Getting pre-approved for a car loan means a lender has provisionally agreed to lend you a certain amount at a specific interest rate, subject to final verification. This gives you a clear budget and turns you into a cash buyer at the dealership.

You’ll know exactly what you can afford, and you won’t be swayed by dealer financing tactics. Based on my experience, walking into a dealership with a pre-approval in hand gives you immense negotiating leverage.

Step 4: Shop for a Car

With your pre-approval in hand and a clear budget, you can now confidently shop for your vehicle. Focus on cars that fit within your pre-approved amount. Remember to factor in taxes, registration, and any additional fees into the total cost.

Don’t rush this process. Take your time, test drive multiple vehicles, and ensure the car meets your needs and expectations.

Step 5: Finalize the Loan and Purchase

Once you’ve found the perfect car, you’ll finalize the loan. If the dealership offers a better rate than your pre-approval, great! But always compare the APR, not just the interest rate. Read all documents carefully before signing.

Ensure you understand every clause, including any prepayment penalties or late payment fees. This final review prevents any unwelcome surprises down the road.

Strategies for Getting Approved, Even with Challenges

Securing a car loan isn’t always straightforward. If you’re facing obstacles like bad credit, no credit, or low income, these strategies can significantly improve your approval chances.

For Bad Credit: Improving Your Odds

- Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and the lender’s risk.

- Co-signer: A reliable co-signer with good credit can be a game-changer.

- Secured Loan: Some lenders offer secured car loans where the car itself acts as collateral. This can be an option for those with very poor credit.

- Improve Credit Score: While it takes time, making timely payments on existing debts, reducing credit card balances, and disputing errors on your credit report can gradually boost your score.

For No Credit: Building Your Financial Foundation

- Secured Credit Card: Obtain a secured credit card and use it responsibly to start building a credit history.

- First-Time Buyer Programs: Many lenders and manufacturers offer specific programs for first-time buyers. Inquire about these.

- Co-signer: Similar to bad credit situations, a co-signer can provide the necessary backing.

- Smaller Loan Amount: Start with a less expensive, reliable used car to keep the loan amount manageable.

For Low Income: Making It Work

- Realistic Budgeting: Be incredibly disciplined with your budget. Don’t overextend yourself.

- Smaller Loan Amount: Focus on more affordable vehicles. A reliable used car is often a smarter choice than a brand-new one.

- Longer Loan Terms (with caution): While longer terms mean lower monthly payments, they also mean more interest paid over time. Use this strategy judiciously and only if absolutely necessary.

- Demonstrate Stability: Even with low income, consistent employment and a low DTI can show lenders you’re a responsible borrower.

Navigating Interest Rates and Loan Terms

The interest rate and loan term are two of the most critical components of your car loan, directly impacting your monthly payments and the total cost of the loan. Understanding how they work is paramount.

How Interest Rates Are Determined

Interest rates are influenced by several factors: your credit score, the current economic climate (federal interest rates), the loan term, the down payment, and the lender’s risk assessment. Borrowers with excellent credit will typically secure the lowest rates.

It’s important to differentiate between fixed interest rates and variable interest rates. Most car loans are fixed, meaning your interest rate remains the same throughout the loan term, providing predictable monthly payments. Variable rates can change, which introduces an element of uncertainty, though they are less common for auto loans.

Short vs. Long Loan Terms: The Impact on Total Cost

The loan term dictates how long you have to repay the loan. Shorter terms (e.g., 36 or 48 months) mean higher monthly payments but significantly less interest paid over the life of the loan. This results in a lower total cost for the car.

Longer terms (e.g., 60, 72, or even 84 months) lead to lower monthly payments, making the car seem more affordable upfront. However, you’ll pay substantially more in interest over the extended period, increasing the overall cost of the vehicle. Pro tips from us: Always prioritize the shortest term you can comfortably afford to minimize interest expenses.

Common Mistakes to Avoid When Applying for a Car Loan

Even experienced buyers can fall prey to common pitfalls. Being aware of these mistakes can save you money and stress.

Not Checking Your Credit Report

Failing to review your credit report for errors or outdated information can lead to a lower credit score than you deserve, resulting in higher interest rates or even loan denial. Always check it thoroughly.

Accepting the First Offer

Whether from a dealership or a direct lender, never accept the first loan offer without comparing it to others. Competition among lenders can drive down rates, so shop around aggressively.

Applying to Too Many Lenders at Once

While shopping around is good, applying to numerous lenders within a short period can negatively impact your credit score due to multiple "hard inquiries." Aim to complete your rate shopping within a 14-45 day window to have them count as a single inquiry.

Buying More Car Than You Can Afford

It’s easy to get caught up in the excitement of a new car and stretch your budget. Stick to your pre-determined budget. Remember, the loan payment is just one piece of the financial puzzle.

Ignoring the Total Cost of the Loan

Focusing solely on the monthly payment can be deceptive. Always look at the total amount you’ll pay over the life of the loan, including all interest and fees. A lower monthly payment often means a longer term and a higher total cost.

Refinancing Your Car Loan: When and Why?

Securing a car loan is just the beginning. Circumstances change, and you might find yourself in a position to improve your existing loan terms by refinancing.

Why Consider Refinancing?

- Lower Interest Rates: If your credit score has improved significantly since you first got the loan, or if market rates have dropped, you could qualify for a much lower interest rate, saving you a substantial amount over time.

- Reduce Monthly Payments: Refinancing to a lower interest rate or extending the loan term can decrease your monthly payment, freeing up cash flow. Be mindful of extending the term, as it increases total interest paid.

- Change Loan Terms: You might want to switch from a variable to a fixed rate, or vice versa, depending on your financial strategy.

- Remove a Co-signer: If your credit has improved, you might be able to refinance the loan solely in your name, releasing your co-signer from their obligation.

Based on my experience, it’s always worth exploring refinancing options if your financial situation has improved or if you’re struggling with your current payments. Many online lenders specialize in car loan refinancing, making the process straightforward. (External Link: For more information on car loan refinancing, consider visiting the Consumer Financial Protection Bureau’s guide on auto loans.)

Beyond the Loan: Understanding Car Ownership Costs

Securing a car loan is a significant step, but it’s just one piece of the larger car ownership puzzle. To truly be confident in your purchase, you must account for all associated costs.

Insurance, Maintenance, and Fuel

These are ongoing expenses that can quickly add up. Car insurance is legally required and varies widely based on your vehicle, driving history, and location. Maintenance, such as oil changes, tire rotations, and unexpected repairs, is inevitable. Fuel costs fluctuate but are a constant factor in your budget.

Ignoring these can lead to financial strain, even if your car loan payment is manageable. Always factor these into your overall budget before committing to a car purchase.

Depreciation: The Hidden Cost

Cars begin to depreciate, or lose value, the moment they are driven off the lot. This is a significant, yet often overlooked, cost of ownership. While it doesn’t come out of your pocket monthly, it affects the resale value of your vehicle.

Understanding depreciation helps in making smarter purchasing decisions, especially if you plan to sell or trade in your car in the future. New cars depreciate faster than used cars in their initial years.

Pro Tips for a Smooth Car Loan Journey

Throughout my career in finance and content creation, I’ve observed patterns that lead to successful outcomes. Here are some actionable pro tips to make your car loan experience as smooth as possible.

- Negotiate, Don’t Just Accept: Everything is negotiable – the car price, the trade-in value, and especially the loan terms. Don’t be afraid to haggle for a better deal.

- Read the Fine Print: Before signing any document, read it meticulously. Understand all terms, conditions, fees, and penalties. If something isn’t clear, ask for clarification.

- Budget for More Than Just the Payment: Always remember the additional costs of ownership: insurance, fuel, maintenance, and potential repairs. Create a comprehensive budget that includes all these elements.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or if the terms aren’t favorable, be prepared to walk away. There will always be another car and another loan.

Conclusion: Driving Towards Financial Freedom

Securing a car loan doesn’t have to be a daunting task reserved for a select few. As we’ve explored, car loans for everyone are a reality, with options available for a wide spectrum of financial situations, from excellent credit to bad credit or no credit history. The key lies in understanding the process, knowing your options, and approaching the journey with careful planning and informed decision-making.

By assessing your financial health, getting pre-approved, shopping wisely, and avoiding common pitfalls, you can navigate the complexities of auto financing with confidence. Remember, a car loan is not just about getting a vehicle; it’s an opportunity to manage a significant financial responsibility effectively, potentially building or rebuilding your credit along the way. Drive forward with knowledge, and the open road awaits!