Car Loans For First Time Car Buyers: Your Ultimate Guide to Navigating the Road Ahead

Car Loans For First Time Car Buyers: Your Ultimate Guide to Navigating the Road Ahead Carloan.Guidemechanic.com

Embarking on the journey to buy your very first car is an incredibly exciting milestone. The prospect of newfound independence, open roads, and personal freedom is truly exhilarating. However, for many first-time car buyers, the path to ownership can feel daunting, especially when it comes to securing a car loan.

Navigating the world of automotive financing, credit scores, interest rates, and loan terms can be confusing. It’s a significant financial decision that requires careful consideration and a solid understanding of the process. That’s precisely why we’ve crafted this comprehensive guide: to empower you, the first-time car buyer, with the knowledge and confidence needed to secure a smart, affordable car loan and drive away happy.

Car Loans For First Time Car Buyers: Your Ultimate Guide to Navigating the Road Ahead

This article will break down every essential step, from preparing your finances to understanding the loan agreement. Our goal is to make the complex simple, ensuring you make informed decisions that benefit your financial future. Let’s hit the road!

Understanding the Landscape: What First-Time Car Buyers Need to Know

The excitement of getting your first set of wheels is palpable. Yet, it’s crucial to balance this enthusiasm with a healthy dose of financial reality. For first-time car buyers, the loan process often presents unique challenges and opportunities compared to seasoned borrowers.

One of the primary differences is the lack of an established credit history. Lenders rely heavily on your credit score and history to assess your risk profile. Without a lengthy track record of managing debt responsibly, you might find initial loan offers less favorable. This doesn’t mean securing a loan is impossible; it just means you need to be strategic and well-prepared.

Based on my experience, many first-time buyers jump into car shopping before understanding their financial standing. This can lead to disappointment or, worse, taking on a loan with unfavorable terms. Our pro tip from us is to always start with your finances, not with the car of your dreams.

The Foundation: Getting Your Finances in Order Before You Look at Cars

Before you even start browsing car models online or stepping onto a dealership lot, the most critical step is to get your financial house in order. This foundational work will not only save you stress but also potentially thousands of dollars over the life of your first car loan.

Budgeting: How Much Can You Truly Afford?

This isn’t just about the monthly payment; it’s about the total cost of car ownership. Many first-time car buyers mistakenly focus solely on the monthly installment, which can be a grave error. A car comes with numerous ongoing expenses beyond the loan itself.

Consider fuel costs, insurance premiums, routine maintenance, potential repairs, registration fees, and even parking. These can quickly add up and significantly impact your monthly budget. A good rule of thumb is to allocate no more than 10-15% of your net monthly income towards all car-related expenses.

Pro tips from us: Create a detailed budget. Track your income and all your current expenses for a month or two. This exercise will give you a clear picture of how much disposable income you genuinely have available for a car. Don’t forget to factor in an emergency fund for unexpected repairs.

Your Credit Score: The Key to Unlocking Better Rates

For first-time car buyers, understanding and improving your credit score is paramount. Your credit score is a three-digit number that summarizes your creditworthiness to lenders. A higher score typically translates to lower interest rates on your car loan, saving you a substantial amount of money over time.

Common mistakes to avoid are not checking your credit score before applying for a loan. You can get free copies of your credit report from AnnualCreditReport.com once a year from each of the three major credit bureaus (Experian, Equifax, and TransUnion). Review these reports for any errors that could be negatively impacting your score. If you find discrepancies, dispute them immediately.

If you have little to no credit history, don’t despair. There are strategies to build credit. Consider applying for a secured credit card or becoming an authorized user on a trusted family member’s credit card (provided they have good credit). Making small, on-time payments consistently will help establish a positive credit history.

The Power of a Down Payment

A significant down payment is one of the most powerful tools in a first-time car buyer’s arsenal. It immediately reduces the amount you need to borrow, which means lower monthly payments and less interest paid over the life of the loan. Lenders also view borrowers with larger down payments as less risky, potentially leading to better loan terms.

How much is ideal? While there’s no magic number, aiming for at least 10-20% of the car’s purchase price is a strong starting point. For used cars, a larger down payment might be even more beneficial due to potentially higher interest rates. From years of observing successful first-time buyers, those who prioritize saving for a substantial down payment consistently secure better deals.

Debt-to-Income Ratio (DTI): A Lender’s Perspective

Your debt-to-income (DTI) ratio is another crucial metric lenders evaluate. It compares your total monthly debt payments to your gross monthly income. For example, if your total monthly debt (student loans, credit cards, rent, etc.) is $1,000 and your gross monthly income is $3,000, your DTI is 33%.

Lenders prefer a DTI ratio below 36%, though some may approve loans with a DTI up to 43%. A lower DTI indicates that you have sufficient income to manage additional debt, like a car loan. If your DTI is high, consider paying down existing debts before applying for a car loan to improve your chances of approval and secure better terms.

Navigating the Loan Process: From Pre-Approval to Paperwork

Once your finances are in order, it’s time to delve into the actual process of securing a car loan for first-time car buyers. This stage involves understanding your options, getting pre-approved, and comparing offers.

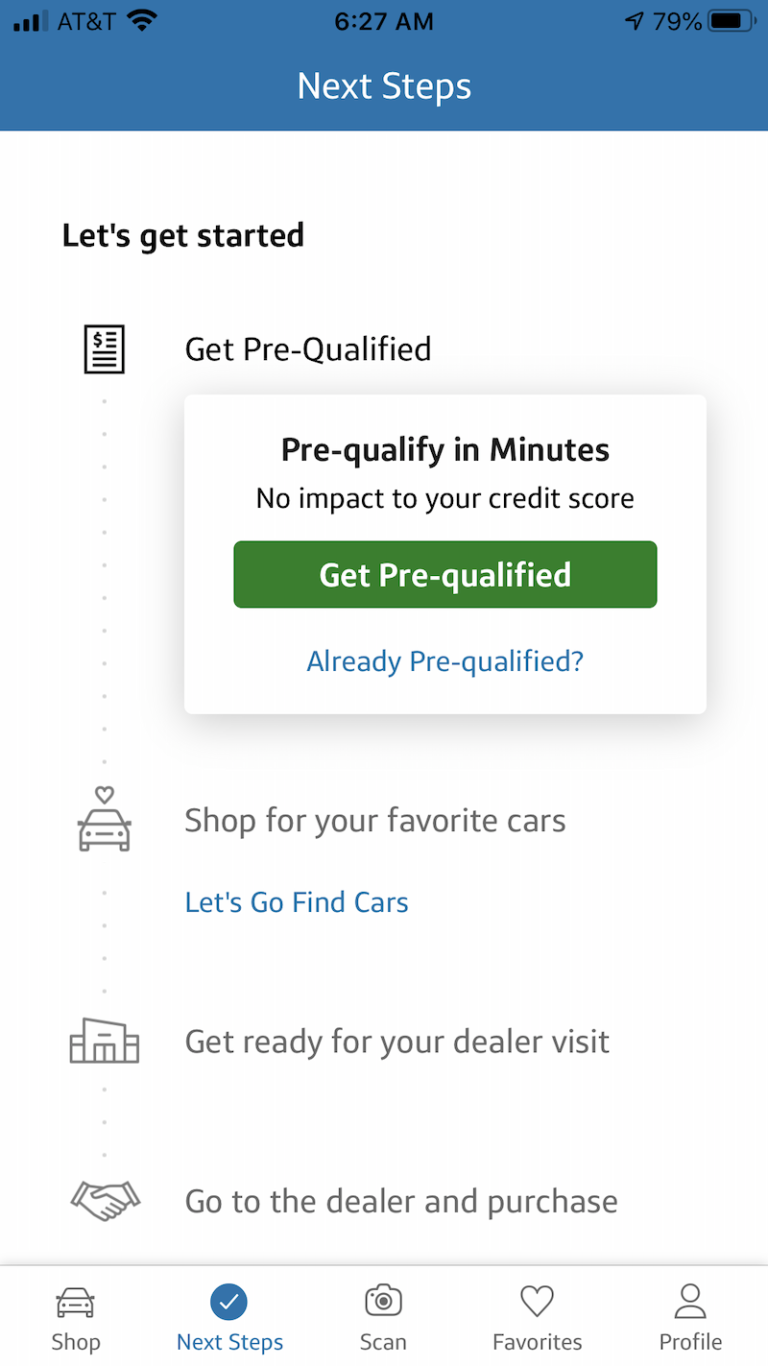

Pre-Approval: Your Secret Weapon

Getting pre-approval for a car loan is perhaps the most crucial step a first-time buyer can take. What is it? Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount of money at a particular interest rate, before you’ve even chosen a car.

Why is it crucial for first-time car buyers? It provides clarity on how much you can truly afford, giving you a firm budget. More importantly, it transforms you into a cash buyer at the dealership. You’re no longer negotiating two things at once (car price and loan terms); you’re simply negotiating the car’s price. This significantly enhances your negotiation power and helps you avoid inflated interest rates often offered by dealership financing.

Benefits include:

- Clear Budget: You know your maximum loan amount.

- Negotiation Power: You can focus solely on the car’s price.

- Rate Comparison: You can compare the pre-approved rate with any offers the dealership might present.

- Avoid Pressure: You won’t feel rushed into accepting a dealership’s financing offer.

Where to Get a Loan: Exploring Your Options

As a first-time car buyer, you have several avenues for obtaining a loan. It’s wise to explore all of them to find the best possible terms.

- Banks: Traditional banks offer a variety of auto loan products. If you have an existing relationship with a bank, they might offer competitive rates.

- Credit Unions: Based on my experience, credit unions often provide some of the most competitive interest rates and personalized service, especially for members. They are member-owned and tend to prioritize their members’ financial well-being.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others offer convenient online applications and competitive rates. They can be a great option for comparing multiple offers quickly.

- Dealership Financing: While convenient, dealership financing often involves a markup on interest rates. However, dealerships sometimes offer special promotions or incentives from manufacturers that can be appealing. Always compare their offer with your pre-approval.

Pro tips from us: Apply to several lenders (banks, credit unions, online) within a short window (typically 14-45 days, depending on the credit scoring model). This will be treated as a single hard inquiry on your credit report, allowing you to compare offers without negatively impacting your score multiple times.

Understanding Loan Terms: Interest Rate, Loan Term, and Total Cost

When reviewing loan offers, pay close attention to these key terms:

- Interest Rate (APR): The Annual Percentage Rate (APR) is the true cost of borrowing, including interest and certain fees. A lower APR means less money paid over the life of the loan. For first-time car buyers with limited credit, rates might be higher, making it even more important to shop around.

- Loan Term: This is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term means lower monthly payments but results in paying more interest over time. Common mistakes to avoid are stretching the loan term too long (e.g., 72 or 84 months) just to get a lower monthly payment, as this significantly increases the total cost of the loan and means you might owe more than the car is worth (negative equity) for a longer period.

- Total Cost of Loan: Always calculate the total amount you will pay over the life of the loan, including the principal and all interest. This gives you the clearest picture of the true expense.

The Car Search: Smart Choices for First-Time Buyers

With your financing pre-approved, you can now focus on the exciting part: finding the right car! For first-time car buyers, making a smart vehicle choice is just as important as securing a good loan.

New vs. Used: What’s Best for You?

- New Cars:

- Advantages: Latest features, full warranty, no prior owner history, often attractive financing deals from manufacturers.

- Disadvantages: Rapid depreciation (a new car loses a significant portion of its value in the first year), higher purchase price, potentially higher insurance premiums.

- Used Cars:

- Advantages: Lower purchase price, less depreciation, potentially lower insurance costs, wider selection within your budget.

- Disadvantages: Potential for unknown mechanical issues (though mitigated by inspections), shorter or no warranty, may lack the latest features.

Pro tips from us: For many first-time car buyers, a reliable used car (3-5 years old) offers the best value. It has already gone through its steepest depreciation curve but is still relatively new and reliable.

What Kind of Car? Practicality Over Flash

It’s tempting to opt for a flashy sports car or a huge SUV. However, as a first-time owner, prioritize reliability, fuel efficiency, and safety. A compact sedan or a small SUV often makes a great first car.

Consider your daily commute, typical passenger needs, and the cost of fuel. A reliable vehicle with a strong safety rating will serve you well and likely keep your insurance costs down.

Test Driving & Inspection: Essential Steps

Never buy a car without a thorough test drive. Pay attention to how the car handles, brakes, and accelerates. Listen for any unusual noises. Test all features: air conditioning, radio, windows, lights.

For a used car, a pre-purchase inspection by an independent mechanic is non-negotiable. This small investment (typically $100-$200) can save you thousands by uncovering hidden issues. A trusted external source like Consumer Reports provides excellent guides on car reliability and what to look for during an inspection. (Example External Link: Consumer Reports Used Car Buying Guide)

Finalizing the Deal: Don’t Rush It!

You’ve found the perfect car and secured your pre-approval. Now comes the final stage: negotiating and signing the contract. This is where patience and attention to detail are paramount.

Negotiation: Tips for First-Time Buyers

- Focus on the Out-the-Door Price: This is the total price, including the car, taxes, registration, and any fees. Avoid getting sidetracked by monthly payment discussions initially.

- Be Prepared to Walk Away: This is your most powerful negotiating tool. If the deal isn’t right, don’t be afraid to leave.

- Know Your Trade-In Value (if applicable): If you have a trade-in, research its value beforehand using sites like Kelley Blue Book or Edmunds. Negotiate the car price first, then discuss the trade-in.

We’ve seen countless first-time buyers get swayed by emotion. Stay firm, stick to your budget, and remember your pre-approval rate.

Understanding the Contract: Read Everything

This is arguably the most critical part. Do not sign anything until you have thoroughly read and understood every single line of the purchase agreement and the loan contract. Take your time. Ask questions about anything you don’t understand.

Look out for:

- Hidden Fees: Are there any charges you weren’t expecting?

- Add-ons: Dealerships often try to sell extended warranties, GAP insurance, paint protection, and other services. While some, like GAP insurance, might be beneficial (especially if you have a small down payment), others might be overpriced or unnecessary. Carefully evaluate each add-on and decline anything you don’t need or can get cheaper elsewhere.

Common mistakes to avoid are feeling pressured to sign quickly. You have the right to understand what you’re agreeing to.

Car Insurance: A Non-Negotiable Necessity

Before you can legally drive your new car off the lot, you must have car insurance. For first-time car buyers, this is an essential but often overlooked expense that needs to be factored into the budget early on. Insurance premiums can vary significantly based on your age, driving record, the type of car, and where you live.

Pro tips from us: Get multiple insurance quotes before you finalize your car purchase. This way, you’ll know the exact cost and can ensure it fits within your budget. Some cars are significantly more expensive to insure than others. Understanding Car Insurance for New Drivers provides more detailed guidance on this topic.

Post-Purchase: Responsible Car Ownership

Congratulations! You’ve successfully navigated the process and are now a proud car owner. But the journey doesn’t end there. Responsible car ownership is key to maintaining your investment and building good financial habits.

- Making Payments on Time: This is crucial for building a positive credit history. Every on-time payment strengthens your credit score, which will benefit you for future loans (e.g., a mortgage). Set up automatic payments to avoid missing due dates.

- Maintaining Your Vehicle: Follow the manufacturer’s recommended maintenance schedule. Regular oil changes, tire rotations, and inspections prevent major issues down the road, saving you money on costly repairs. Neglecting maintenance can significantly shorten your car’s lifespan and lead to expensive problems. For more tips, check out our guide on Tips for Maintaining Your First Car.

- Building Your Credit History: Continue to manage all your credit accounts responsibly. As your car loan matures with consistent on-time payments, it will serve as an excellent foundation for a robust credit profile.

Common Mistakes First-Time Car Buyers Make (and How to Avoid Them)

From years of experience helping people secure their first vehicle, we’ve identified recurring pitfalls. Being aware of these common mistakes can help you steer clear of them:

- Buying More Car Than You Can Afford: The biggest mistake. Don’t let emotion override your budget. Remember the total cost of ownership, not just the monthly payment.

- Skipping Pre-Approval: Going to a dealership without pre-approval leaves you vulnerable to high-pressure sales tactics and potentially unfavorable financing terms.

- Not Reading the Fine Print: Rushing through the loan and purchase contracts can lead to unexpected fees, unwanted add-ons, or unfavorable clauses. Always read everything carefully.

- Ignoring Total Cost of Ownership: Focusing only on the car’s price or monthly payment and forgetting about insurance, fuel, maintenance, and registration can quickly strain your budget.

- Failing to Get Insurance Quotes Beforehand: This can lead to sticker shock when you realize how much insurance will add to your monthly expenses, potentially making your chosen car unaffordable.

- Trading In a Car Too Early or Without Research: If you have an old car to trade in, research its value independently. Negotiate the new car price first, then discuss the trade-in as a separate transaction.

- Falling for "Payment Shopping": Dealers might ask, "What monthly payment are you looking for?" This can lead them to extend the loan term or add fees to reach that payment, costing you more in the long run. Always negotiate the total price of the car.

Conclusion: Drive Away with Confidence

Securing a car loan for first-time car buyers doesn’t have to be a stressful ordeal. By following the comprehensive steps outlined in this guide, you’ll be well-equipped to make informed decisions, avoid common pitfalls, and confidently navigate the entire process.

Remember, preparation is your most valuable asset. Understand your budget, know your credit score, get pre-approved, and thoroughly research both your car and your loan options. With patience and diligence, you can secure an affordable car loan that fits your financial situation, allowing you to enjoy the freedom and convenience of your very first car without unnecessary financial strain. Happy driving!