Car Loans For No Credit And Low Income: Your Comprehensive Guide to Getting Approved

Car Loans For No Credit And Low Income: Your Comprehensive Guide to Getting Approved Carloan.Guidemechanic.com

Getting a car is often more than just a convenience; for many, it’s a necessity for work, family, and daily life. Yet, for individuals navigating the challenging landscape of "car loans for no credit and low income," the path to vehicle ownership can feel blocked by insurmountable hurdles. You might be asking yourself: "Is it even possible to get approved?"

Based on my experience working with countless individuals facing similar challenges, the answer is a resounding yes – but it requires a strategic, informed, and persistent approach. This isn’t about finding a magic bullet; it’s about understanding the system, preparing diligently, and knowing exactly where to look. In this super comprehensive guide, we’ll break down every facet of securing a car loan when your credit history is non-existent and your income is modest, providing real value and actionable steps.

Car Loans For No Credit And Low Income: Your Comprehensive Guide to Getting Approved

Navigating the Road: Understanding Car Loans with No Credit and Low Income

Before we dive into solutions, it’s crucial to understand why "no credit" and "low income" pose such significant obstacles in the first place. Lenders assess risk, and these two factors directly impact their perception of your ability to repay a loan.

The Challenge of No Credit History

When you have "no credit," it means you haven’t established a track record of borrowing and repaying money. Lenders have nothing to evaluate. They can’t see if you pay bills on time, manage debt responsibly, or if you’ve defaulted in the past. This lack of data makes you an unknown entity.

For them, lending to someone with no credit is akin to lending money to a stranger without any references. They simply don’t have the information they need to confidently approve a loan, leading to higher interest rates if approved, or outright rejection. Building credit is a slow process, but an essential one for future financial endeavors.

The Hurdle of Low Income

"Low income" presents a different, but equally significant, challenge. Lenders need assurance that you have a stable and sufficient income to cover your monthly loan payments, alongside your existing living expenses. They use a metric called the Debt-to-Income (DTI) ratio.

Your DTI ratio compares your total monthly debt payments to your gross monthly income. If your income is low, even a small car payment can push your DTI ratio into an unacceptable range for many lenders. They want to see that you have enough disposable income to comfortably manage the new debt without struggling.

The Double Whammy: No Credit AND Low Income

When you combine both "no credit and low income," you’re essentially facing a "double whammy." You lack the financial history to prove reliability and the robust income to easily absorb new debt. This scenario demands a multifaceted strategy, focusing on both establishing credibility and demonstrating affordability. It might seem daunting, but it’s far from impossible.

Laying the Foundation: Preparing for a Car Loan When You Have No Credit History

Success in securing "car loans for no credit and low income" begins long before you even step foot into a dealership or submit an application. Preparation is your most powerful tool.

1. Assess Your Financial Situation Realistically

Pro tips from us: The very first step is to create a detailed budget. You need to know exactly how much money comes in each month and precisely where it all goes. Don’t guess; track every expense, from rent and utilities to groceries and entertainment.

Understanding your true financial capacity will help you determine a realistic car payment you can afford without overstretching yourself. This isn’t just about what a lender thinks you can pay; it’s about what you know you can comfortably manage every single month. Being honest with yourself here prevents future financial stress. For a deeper dive into creating a realistic budget, check out our guide to Creating a Realistic Monthly Budget.

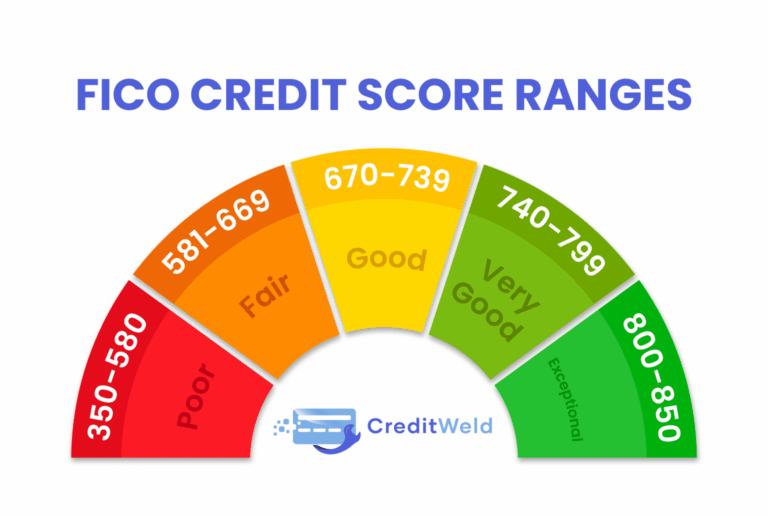

2. Understand Your Credit (Even If It’s Zero)

Even if you have no credit score, it’s wise to understand how credit works. Your credit report contains personal information, accounts you’ve opened, and payment history. With no credit, your report will simply be very thin or non-existent.

You can get a free credit report from AnnualCreditReport.com once a year from each of the three major bureaus (Experian, Equifax, TransUnion). While it might be blank, it confirms your status and ensures no errors exist. This step is about familiarizing yourself with the system that will eventually track your financial progress.

3. Saving for a Down Payment: Your Golden Ticket

One of the most impactful things you can do to improve your chances of getting "car loans for no credit and low income" is to save a substantial down payment. A down payment demonstrates your financial commitment and reduces the amount you need to borrow.

Based on my experience, a significant down payment (10-20% of the car’s value, if possible) directly lowers the lender’s risk. It shows you have some skin in the game, reducing the loan-to-value (LTV) ratio and making the loan more attractive to lenders. Even a few hundred dollars can make a difference.

4. Improving Your Income (Short-Term & Long-Term)

While easier said than done, actively working to increase your income can significantly improve your chances for "low income auto financing."

- Short-term: Consider side hustles like freelance work, gig economy jobs (delivery services, ridesharing), or temporary part-time work. Every extra dollar you can show as income, or save towards a down payment, helps.

- Long-term: Invest in skills development, certifications, or education that could lead to higher-paying opportunities. Even small increases in your regular income can make a substantial difference to your debt-to-income ratio in the eyes of a lender.

Unlocking Opportunities: Strategies for Car Loans with No Credit

When your credit file is empty, you need to explore specific avenues designed for "no credit history car loans."

1. Secured Car Loans

A secured car loan uses the car itself as collateral. If you fail to make payments, the lender can repossess the vehicle. This reduces the risk for the lender, making them more willing to approve loans for individuals with no credit.

While the interest rates might be higher than for those with excellent credit, a secured loan offers a viable pathway to ownership and, crucially, a chance to build your credit history. Making timely payments on a secured loan is an excellent way to start establishing a positive credit profile.

2. First-Time Buyer Programs

Many dealerships and lenders offer special "first-time buyer programs" specifically designed for individuals with limited or no credit history. These programs acknowledge that everyone has to start somewhere.

These programs often have specific eligibility requirements, such as a minimum income, age, or employment history. It’s worth asking dealerships directly about these options. They are tailored to help you get your first auto loan and begin your credit journey.

3. Credit-Builder Loans (as a Precursor)

Sometimes, the best strategy is to build credit before applying for a car loan. A credit-builder loan is a small loan where the funds are held in a locked savings account by the lender. You make payments on the loan, and once it’s fully paid, you receive the money.

This isn’t for buying a car directly, but it’s a powerful tool for establishing a positive payment history. After 6-12 months of making on-time payments, you’ll have a credit score that can significantly improve your chances for "car loans for no credit and low income." For a deeper dive into improving your credit score, read our article on How to Improve Your Credit Score Fast.

4. Dealership Financing (Special Finance Departments)

Many large dealerships have "special finance departments" that specialize in helping customers with challenging credit situations, including "no credit history car loans." They often work with a network of subprime lenders who are more willing to take on higher-risk borrowers.

While these loans typically come with higher interest rates, they can be a gateway to car ownership and credit building. Be prepared for potentially less favorable terms, but use it as an opportunity to prove your reliability. Always read the fine print carefully.

5. Credit Unions

Credit unions are not-for-profit financial institutions known for being more community-focused and often more flexible than traditional banks. They may be more willing to work with members who have "no credit" or "low income" because they prioritize member welfare over shareholder profits.

Becoming a member of a local credit union could open doors to more understanding lending practices and potentially better rates than what you might find at subprime lenders. They often look at your overall financial picture, not just your credit score.

Managing Your Budget: Securing Low Income Auto Financing

Beyond credit, addressing "low income" is paramount. Your income directly impacts the "affordable car payments" you can manage.

1. Realistic Budgeting and Vehicle Choice

With "low income," your car choice becomes critically important. Aim for a reliable, used car that fits squarely within your budget, rather than stretching for a new or expensive model. A more affordable vehicle means a smaller loan amount and, consequently, lower monthly payments.

Focus on total cost of ownership, including insurance, fuel, and maintenance, not just the purchase price. A cheaper car might free up funds for these other essential expenses, making your overall financial burden more manageable.

2. Higher Down Payment: Your Leverage

As mentioned earlier, a higher down payment is even more critical when seeking "low income auto financing." It directly reduces the amount you need to borrow, which in turn lowers your monthly payment.

For example, on a $10,000 car, a $2,000 down payment means you only finance $8,000. This smaller loan amount is less risky for the lender and more affordable for you, easing the strain on your limited income.

3. The Power of a Co-Signer

A co-signer can significantly boost your chances of approval for "car loans for no credit and low income." A co-signer is someone with good credit and a stable income who agrees to be equally responsible for the loan if you default.

Their good credit history and higher income essentially "guarantee" the loan. This reduces the lender’s risk dramatically. However, understand that a co-signer takes on serious responsibility; if you miss payments, their credit will be damaged, and they will be legally obligated to pay. Choose a co-signer wisely and ensure open communication.

4. Comprehensive Proof of Income (Even if Low)

Even with "low income," providing thorough documentation can make a difference. Gather all possible proof of income:

- Recent pay stubs (at least 3-6 months)

- Bank statements showing consistent deposits

- Tax returns (especially if self-employed or have varied income sources)

- Letters from employers verifying employment and salary

- Proof of any additional income sources (side gigs, benefits, alimony)

The more evidence you can provide of consistent income, no matter the amount, the more comfortable a lender will be. They want to see stability and reliability.

5. Improving Your Debt-to-Income Ratio (DTI)

Lenders typically prefer a DTI ratio below 36%, with no more than 28% going towards housing costs. When you have "low income," keeping your existing debt low is crucial.

- Pay down existing debts: Even small personal loans or credit card balances can impact your DTI.

- Avoid new debt: Don’t open new lines of credit or make large purchases on existing credit cards before applying for a car loan.

- Consider a cheaper car: As discussed, a lower car price directly reduces the potential loan payment, thus improving your DTI ratio relative to the car loan.

The Dual Challenge: Car Loans For No Credit And Low Income Simultaneously

When facing both challenges, a combined, strategic approach is essential. This is where patience and persistence become your greatest assets.

1. Prioritize Affordability First

Before even thinking about specific lenders, determine the absolute maximum monthly payment you can realistically afford. This figure should include insurance, fuel, and estimated maintenance. With "no credit and low income," you cannot afford to be car-poor.

Start by looking at reliable, used vehicles in a lower price range. Think about a car that gets you from A to B safely and efficiently, rather than one with all the bells and whistles.

2. Leverage Dealer Relationships

Visit local dealerships that advertise "bad credit car loans" or "special financing." These dealers often have established relationships with subprime lenders who specialize in high-risk loans. Be upfront about your situation ("no credit history car loans" and "low income auto financing").

While you might face higher interest rates, these dealerships are often your best bet for getting an initial approval. Just remember to negotiate and compare offers if possible.

3. Patience and Persistence Are Key

Getting "car loans for no credit and low income" is rarely a quick process. You might face rejections, or receive offers with terms that seem unfavorable. Don’t get discouraged.

It may take time to save a sufficient down payment, or to find the right lender who is willing to work with your specific circumstances. View each attempt as a learning experience, refining your approach based on feedback.

4. Beware of Predatory Lenders

Common mistakes to avoid are falling for "guaranteed car loan approval" promises without scrutiny. While some lenders specialize in high-risk loans, truly "guaranteed" approval often comes with predatory terms: extremely high interest rates (sometimes 25% or more), hidden fees, or unfavorable repayment schedules.

Always read the entire loan agreement before signing. If a deal seems too good to be true, or if you feel pressured, walk away. Your long-term financial health is more important than getting a car immediately.

Navigating the Application: What to Expect When Seeking a Car Loan

Once you’ve done your homework and prepared, it’s time to apply. Knowing what to expect can ease the process.

1. Gather All Necessary Documents

Before you apply, have everything ready. This includes:

- Government-issued ID (driver’s license)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- References (sometimes required for subprime loans)

- Proof of insurance (you’ll need this before driving off the lot)

- Your down payment (check, money order, or cash)

Having these documents organized and readily available will streamline the application process and show the lender you are serious and prepared.

2. Pre-Approval vs. Application

Consider getting "pre-approval car loans" if possible. While challenging with no credit, some credit unions or online lenders might offer it. Pre-approval gives you an idea of how much you can borrow and at what interest rate before you even start shopping for a car.

This empowers you to shop like a cash buyer, focusing on the car rather than the financing. If pre-approval isn’t an option, be prepared to apply directly at the dealership or with a subprime lender.

3. Understanding Loan Terms

When presented with a loan offer, pay close attention to:

- APR (Annual Percentage Rate): This is the total cost of borrowing, including interest and fees, expressed as a yearly percentage. It’s the most important number for comparing loans.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but more interest paid over time.

- Total Cost: Calculate the total amount you will pay over the life of the loan (monthly payment x loan term). You might be surprised how much interest adds up, especially with higher APRs for "no credit history car loans."

4. Negotiating: Don’t Just Accept the First Offer

Even with "no credit and low income," there’s often room for negotiation, especially on the car’s price. If you can lower the purchase price, you reduce the loan amount, which benefits you.

Also, compare offers if you’ve applied to multiple lenders. Even a small difference in APR can save you hundreds of dollars over the life of the loan. Don’t be afraid to walk away if the terms are simply not affordable or fair.

Beyond Approval: Building Credit and Financial Health with Your Car Loan

Congratulations, you’ve secured a "car loan for no credit and low income"! But the journey doesn’t end there. This loan is now your opportunity to build a solid financial foundation.

1. Making Payments On Time: Your Top Priority

This is the single most important step in building a positive credit history. Every single on-time payment you make will be reported to the credit bureaus and will gradually build your credit score.

Set up automatic payments if possible, or mark your calendar with reminders. Missing even one payment can severely damage your newly forming credit profile and trigger late fees. Consistency is key.

2. Understanding Your Credit Report

Regularly monitor your credit report (again, via AnnualCreditReport.com). You’ll start to see your car loan reported, along with your payment history. This allows you to track your progress and ensure there are no errors.

As you make consistent payments, you’ll see your credit score gradually improve. This is a tangible reward for your discipline and a sign of future financial opportunities.

3. Future Financial Goals

This first "bad credit car loan" or "no credit history car loan" is a stepping stone. Once you’ve established a solid payment history for a year or two, you might be able to refinance your car loan at a lower interest rate.

This experience will also open doors to other financial products, like credit cards with better terms, personal loans, or even a mortgage down the line. Use this success as motivation to continue building healthy financial habits.

Conclusion: Your Road to Car Ownership Starts Now

Securing "car loans for no credit and low income" might seem like an uphill battle, but it is absolutely achievable with the right strategy and mindset. By understanding the challenges, preparing meticulously, exploring all available avenues, and committing to responsible repayment, you can turn a seemingly impossible situation into a significant financial victory.

Remember, patience, persistence, and proactive planning are your most valuable allies. Start by assessing your finances, saving that down payment, and diligently seeking out lenders who are willing to work with your unique situation. Your journey to car ownership and building a stronger financial future starts today. Don’t let your past or current circumstances define your potential. Take these steps, and drive towards a brighter tomorrow.