Car Loans for Recent College Graduates: Your Ultimate Guide to Driving Off with Confidence

Car Loans for Recent College Graduates: Your Ultimate Guide to Driving Off with Confidence Carloan.Guidemechanic.com

Graduating from college is a monumental achievement, opening doors to new career paths, independence, and exciting opportunities. One of the first major steps many recent graduates consider is buying a car. Reliable transportation is often essential for commuting to a new job, running errands, and embracing the freedom of adulthood. However, securing a car loan for recent college graduates can often feel like navigating a complex maze, especially when faced with limited credit history or existing student loan debt.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to successfully obtain an auto loan for new grads. We’ll delve deep into the challenges you might face, equip you with smart financial practices, and walk you through the entire process, ensuring you drive off the lot with confidence and a manageable financial plan.

Car Loans for Recent College Graduates: Your Ultimate Guide to Driving Off with Confidence

The Unique Hurdles for Recent Grads in the Auto Loan Market

While the excitement of a new car is undeniable, recent college graduates often encounter specific obstacles when applying for an auto loan. Understanding these challenges is the first step toward overcoming them.

The "Thin File" Problem: Lack of Established Credit History

One of the primary hurdles for many new graduates is having a "thin credit file." This means you haven’t had enough time or opportunities to build a substantial credit history. Lenders rely heavily on credit scores and reports to assess risk. A thin file makes it difficult for them to gauge your repayment reliability, often leading to higher interest rates or even outright denial.

Without a robust history of managing credit responsibly, such as credit cards, personal loans, or mortgages, lenders see you as an unknown quantity. They prefer to lend to individuals with a proven track record of timely payments and sensible debt management.

Student Loan Debt: The Debt-to-Income Ratio Challenge

It’s no secret that many college graduates carry a significant burden of student loan debt. While student loans are generally considered "good debt" for educational investment, they directly impact your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. Lenders use DTI to determine if you can comfortably afford additional debt, like a car payment.

A high DTI ratio signals to lenders that a large portion of your income is already committed to existing debts. This can make them hesitant to approve another loan, especially if your entry-level salary isn’t high enough to offset your student loan obligations.

Entry-Level Income: Proving Repayment Ability

Many recent graduates start their careers in entry-level positions, which often come with more modest salaries. While you might be earning a steady income, it might not be substantial enough in the eyes of a lender to comfortably cover a car payment, insurance, and other living expenses, especially when coupled with student loan payments.

Lenders need assurance that you have a stable job and sufficient disposable income to make your car loan payments consistently. A steady employment history, even if short, and a clear understanding of your budget are crucial.

Laying Your Financial Foundation: Building Credit Wisely

Before you even think about stepping into a dealership, building a solid credit foundation is paramount. This will significantly improve your chances of approval and help you secure a better interest rate.

The Power of a Secured Credit Card

A secured credit card is an excellent tool for recent graduates to start building credit. You deposit a sum of money with the issuer, which typically becomes your credit limit. This deposit acts as collateral, reducing the risk for the lender.

By using the card responsibly – making small purchases and paying off the full balance on time every month – you demonstrate positive credit behavior. This activity is reported to the major credit bureaus, gradually building your credit history and improving your score.

Authorized User Status: A Shortcut with Caveats

Becoming an authorized user on a parent’s or trusted family member’s credit card can be a quick way to benefit from their established credit history. Their positive payment history will appear on your credit report, giving your score a boost.

However, it’s crucial that the primary cardholder maintains excellent credit. If they miss payments, it could negatively impact your credit score as well. Always have a clear understanding and agreement with the primary cardholder.

Rent and Utility Reporting: Leveraging Existing Payments

Traditionally, rent and utility payments haven’t been reported to credit bureaus unless they go unpaid and are sent to collections. However, some newer services and rent payment platforms now offer to report your on-time rent and utility payments to credit bureaus.

This can be a valuable way to leverage payments you’re already making to build a positive credit history. Check with your landlord or utility providers to see if they participate in such programs, or explore third-party services that offer this reporting.

Pro Tips from Us: Start building your credit as soon as possible. Even a few months of responsible credit use can make a difference. The longer your positive credit history, the better.

Decoding Car Loan Essentials: What Every Grad Needs to Know

Understanding the terminology and key components of a car loan will empower you to make informed decisions and avoid common pitfalls.

APR vs. Interest Rate: Understanding the True Cost

The interest rate is the percentage charged by the lender for borrowing money. However, the Annual Percentage Rate (APR) provides a more comprehensive picture of the total cost of borrowing. It includes the interest rate plus any additional fees, such as origination fees or administrative charges, expressed as an annual percentage.

Always compare APRs when shopping for loans, as it reflects the actual yearly cost of your loan. A lower APR means less money paid over the life of the loan.

Loan Term: The Shorter, The Better (Usually)

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term means lower monthly payments, which can seem appealing.

However, a longer term also means you’ll pay more in total interest over the life of the loan. Based on my experience, it’s often wiser to opt for the shortest loan term you can comfortably afford, even if it means a slightly higher monthly payment. This saves you significant money in the long run.

Down Payment: Your Best Friend

A down payment is the initial amount of money you pay upfront for the car. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay.

For recent graduates, a substantial down payment is even more critical. It demonstrates financial responsibility to lenders and significantly reduces their risk, making them more likely to approve your loan and offer a favorable interest rate. Aim for at least 10-20% of the car’s purchase price if possible.

Understanding Your Credit Score: FICO and VantageScore

Your credit score is a three-digit number that summarizes your creditworthiness. The most widely used models are FICO and VantageScore. These scores range from 300 to 850, with higher scores indicating lower risk to lenders.

Lenders use your credit score as a primary factor in determining your eligibility and interest rate. Knowing your score before you apply allows you to anticipate what kind of rates you might qualify for and gives you time to address any inaccuracies on your credit report.

Strategic Moves: How Recent Grads Can Boost Approval Chances

Even with a thin credit file or student loan debt, there are powerful strategies you can employ to increase your chances of securing a favorable car loan for recent college graduates.

The Impact of a Significant Down Payment

We touched on this earlier, but it’s worth reiterating and expanding. A substantial down payment doesn’t just reduce your loan amount; it changes the entire dynamic of the loan. It tells the lender you have skin in the game, reducing their perceived risk.

Pro tips from us: Saving up for a larger down payment (e.g., 15-20% or more) can be the single most effective way to secure better terms, especially if your credit history is limited. It can also help you avoid being "upside down" on your loan, where you owe more than the car is worth.

The Co-signer Advantage: A Double-Edged Sword

If your credit history is insufficient, having a co-signer with excellent credit can significantly boost your approval chances. A co-signer legally agrees to be responsible for the loan if you fail to make payments.

While this can be a lifesaver for new grads, it’s a serious commitment for both parties. The co-signer’s credit will be affected if you miss payments, and it ties up their credit line. Only consider this option with someone you trust implicitly and who understands the full implications.

Leveraging College Graduate Programs

Many major auto manufacturers and some financial institutions offer special college graduate car programs. These programs are specifically designed to help recent graduates (typically within two years of graduation) secure auto loans, often with relaxed credit requirements and sometimes even special discounts or rebates.

Based on my experience, these programs are an excellent, often overlooked, resource. Always ask about them at dealerships or when speaking with lenders. You’ll usually need to provide proof of graduation, employment, and a minimum income.

Exploring Lender Options: Where to Look

Don’t just walk into the first dealership you see. Shopping around for your loan is crucial.

- Banks: Traditional banks often have competitive rates, but their credit requirements can be stricter. If you already bank with them, they might offer a slight advantage.

- Credit Unions: These member-owned financial institutions often have more flexible lending criteria and can offer lower interest rates, especially for those with less-than-perfect credit. They are known for their community-focused approach.

- Dealership Financing: Dealerships offer convenience, as you can arrange financing directly with them. They work with multiple lenders, but their rates might not always be the best. It’s wise to have a pre-approval from an external lender before discussing dealership financing.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, or Carvana Financing offer quick pre-approvals and competitive rates, often making the process very streamlined.

Pro Tip: Get pre-approved by at least 2-3 different lenders before you even start serious car shopping. This gives you a benchmark and strengthens your negotiating position at the dealership.

Choosing the Right Vehicle: Practicality Over Flash

As a recent graduate, making a sensible choice about your first car is crucial. While a brand-new luxury vehicle might be tempting, it’s often financially imprudent.

- New vs. Used: A reliable used car that’s a few years old can be a much smarter investment. It depreciates slower than a new car, and its purchase price will be significantly lower, leading to a smaller loan amount.

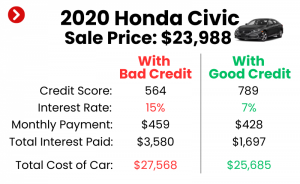

- Affordable Models: Research vehicles known for their reliability, fuel efficiency, and lower insurance costs. Toyota Corollas, Honda Civics, and Mazda3s are often excellent choices for first-time buyers.

- Consider Insurance Costs: Get insurance quotes for different models before you commit. Insurance can be a significant monthly expense, especially for younger drivers.

Optimizing Your Debt-to-Income Ratio

While you can’t magically erase student loan debt overnight, you can strategically improve your DTI ratio before applying for a car loan.

- Pay Down Small Debts: If you have any small credit card balances or other minor debts, focus on paying them off entirely. This frees up monthly cash flow and improves your DTI.

- Increase Income: If possible, look for opportunities to increase your income, even temporarily. A higher income immediately lowers your DTI.

- Delay Other Large Purchases: Avoid taking on any new debt (like furniture loans or additional credit cards) in the months leading up to your car loan application.

Navigating the Application Process: Your Step-by-Step Guide

Once you’ve done your homework, built some credit, and explored your options, it’s time to apply for the loan.

Gathering Your Documents

Be prepared. Lenders will require several documents to verify your identity, income, and employment. Have these ready to streamline the process:

- Government-issued ID (Driver’s License)

- Proof of income (Recent pay stubs, offer letter, bank statements)

- Proof of employment (Employer contact information, recent W-2s)

- Proof of residence (Utility bill, lease agreement)

- Proof of graduation (Diploma or transcript for college grad programs)

- Bank account information

Getting Pre-Approved

This is perhaps the most important step in the application process. Getting pre-approved means a lender has reviewed your financial information and agreed to lend you a certain amount at a specific interest rate, before you’ve even chosen a car.

Why it’s crucial: A pre-approval gives you immense power at the dealership. You know your budget, your interest rate, and you’re negotiating as a cash buyer. This separates the car price negotiation from the financing negotiation, which often leads to a better overall deal. Be aware that pre-approvals usually involve a "soft credit pull" initially, which doesn’t affect your score, followed by a "hard credit pull" when you finalize the loan.

The Dealership Experience

Armed with your pre-approval, you can confidently shop for your car.

- Focus on the Car Price: Negotiate the car’s purchase price first, separate from financing. Let the dealership know you have outside financing secured.

- Compare Financing: Once you’ve agreed on a car price, then you can see if the dealership can beat your pre-approved rate. They might offer incentives or lower rates to close the sale.

- Read Everything Carefully: Before signing anything, thoroughly read all documents. Understand every line item, fee, and condition. Don’t be rushed.

For more tips on negotiating car prices, check out our article on How to Negotiate Car Prices Like a Pro.

Common Pitfalls to Avoid for New Grads

As an Expert Blogger and Professional SEO Content Writer, I’ve seen countless individuals make avoidable mistakes. For recent graduates, these pitfalls can be particularly damaging.

Overextending Your Budget

The biggest mistake is buying more car than you can truly afford. Don’t just look at the monthly payment. Consider the total cost of ownership, including insurance, fuel, maintenance, and potential repairs.

Common mistakes we see are new grads getting approved for a loan amount that feels exciting, but whose monthly payments, combined with other living expenses and student loans, quickly become a burden. Stick to a budget that leaves room for emergencies and savings.

Skipping the Pre-approval Step

As mentioned, skipping pre-approval puts you at a significant disadvantage. You lose negotiating power and might end up accepting a higher interest rate from the dealership simply because it’s convenient.

Not Shopping Around for Rates

Assuming the first offer you get is the best is a costly error. Different lenders have different criteria and offer varying rates. Taking the time to get multiple quotes can save you thousands of dollars over the life of the loan.

Falling for Unnecessary Add-ons

Dealerships often push add-ons like extended warranties, rustproofing, paint protection, or VIN etching. While some might offer legitimate value for certain situations, many are overpriced and unnecessary. Carefully evaluate each add-on and don’t hesitate to decline them.

Ignoring Insurance Costs

A brand-new car or a high-performance vehicle will almost certainly come with higher insurance premiums. Get insurance quotes for your desired vehicles before you commit to a purchase. Factor this into your monthly budget.

Beyond the Loan: Smart Car Ownership for Grads

Securing the car loan is just the beginning. Responsible car ownership involves ongoing financial discipline.

Budgeting for Maintenance and Fuel

Cars require regular maintenance – oil changes, tire rotations, brake checks, etc. – and fuel costs add up. Create a dedicated budget for these ongoing expenses to avoid being caught off guard. Neglecting maintenance can lead to more expensive repairs down the line.

Making Payments On Time: Building Future Credit

Every on-time car loan payment is an opportunity to strengthen your credit history. This positive behavior will be reported to credit bureaus, paving the way for better rates on future loans, mortgages, and credit cards. Conversely, missing payments will severely damage your credit.

Refinancing Opportunities

If you secure a car loan for recent college graduates with a higher interest rate due to your limited credit history, don’t despair. After 12-18 months of consistent, on-time payments, your credit score will likely have improved significantly.

At that point, you might be eligible to refinance your car loan at a lower interest rate, which can save you a substantial amount of money over the remaining loan term. It’s always worth exploring this option once your financial situation stabilizes and your credit score improves.

For detailed information on budgeting and managing your finances effectively, the Consumer Financial Protection Bureau offers excellent resources and guides. You can find valuable tools and advice on their website: https://www.consumerfinance.gov/

Conclusion: Drive Off with Confidence and a Smart Financial Plan

Securing a car loan for recent college graduates is a significant financial milestone that requires careful planning, research, and responsible decision-making. While the journey might seem daunting at first, by understanding the unique challenges, strategically building your credit, and making informed choices, you can navigate the process successfully.

Remember to prioritize practicality, shop around for the best loan terms, and always read the fine print. Your first car loan is not just about getting a vehicle; it’s about establishing a strong financial foundation that will benefit you for years to come. Drive wisely, manage your finances diligently, and enjoy the freedom and independence your new wheels bring!