Car Loans Near Me For Bad Credit: Your Ultimate Guide to Getting Approved

Car Loans Near Me For Bad Credit: Your Ultimate Guide to Getting Approved Carloan.Guidemechanic.com

Needing a reliable vehicle is more than just a convenience; for many, it’s an absolute necessity for work, family, and daily life. But what happens when you’re facing a less-than-perfect credit score and the thought of securing a car loan feels like an uphill battle? The good news is, getting car loans near me for bad credit is not only possible, but it’s a journey many people successfully navigate every day.

This comprehensive guide is designed to empower you with the knowledge, strategies, and confidence needed to secure the financing you require, even when your credit history has a few bumps. We’ll dive deep into understanding your credit, finding the right lenders, and making smart choices that pave the way for a brighter financial future. Let’s shift gears and get you on the road to approval!

Car Loans Near Me For Bad Credit: Your Ultimate Guide to Getting Approved

Understanding the Landscape: Bad Credit and Car Loans

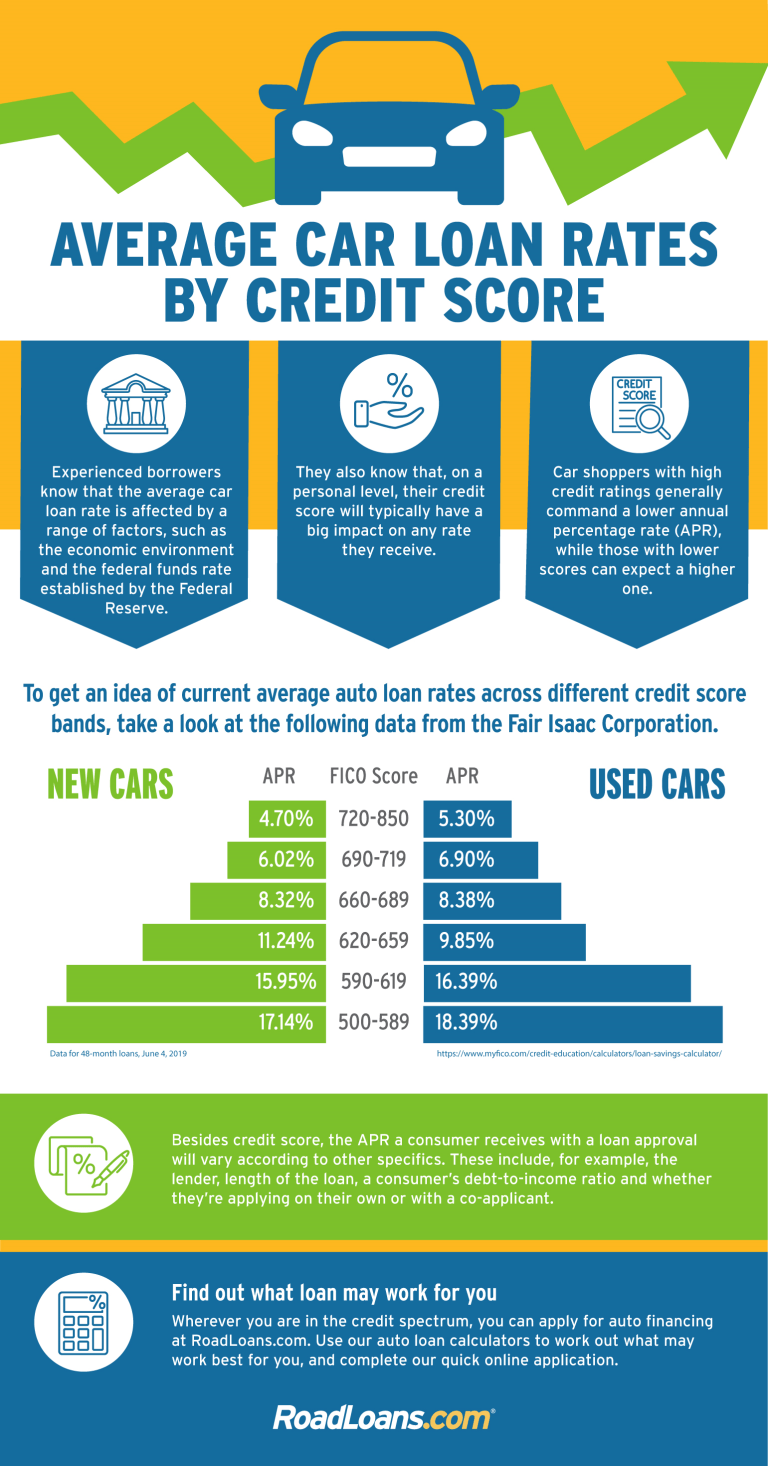

Before we explore solutions, it’s crucial to understand what "bad credit" typically means in the eyes of a lender. Your credit score is a numerical representation of your creditworthiness, with FICO scores generally ranging from 300 to 850. A score below 620 often falls into the "subprime" or "bad credit" category.

Lenders use this score, alongside your credit report, to assess the risk associated with lending you money. A lower score suggests a higher risk of default, making traditional lenders more hesitant. However, this doesn’t mean all doors are closed. It simply means you’ll need to approach the process strategically and with the right information.

Based on my experience, many individuals mistakenly believe their credit history automatically disqualifies them from car ownership. This simply isn’t true. While it might influence the terms of your loan, such as interest rates, there are numerous lenders specifically designed to work with borrowers in your situation.

Dispelling Common Myths About Bad Credit Auto Loans

The world of bad credit car loans is often shrouded in misconceptions that can deter even the most determined buyer. Let’s bust some of these myths right now:

- Myth 1: It’s Impossible to Get a Car Loan with Bad Credit.

- Reality: This is perhaps the biggest misconception. While traditional lenders might be more restrictive, a significant market exists for subprime auto loans. Many dealerships and specialized lenders focus specifically on helping people with challenging credit histories.

- Myth 2: All Bad Credit Loans Are Predatory or Scams.

- Reality: While caution is always advised, and some lenders do offer less favorable terms, many reputable financial institutions provide legitimate and fair bad credit car loans. The key is knowing how to identify them and understanding the terms before you sign.

- Myth 3: You’ll Always Pay Exorbitant Interest Rates.

- Reality: Yes, bad credit generally means higher interest rates due to increased risk. However, there are strategies to mitigate this, such as making a larger down payment or having a co-signer. Furthermore, making on-time payments on a subprime loan can actually improve your credit over time, allowing you to refinance at a better rate later.

Essential Strategies for Securing a Car Loan with Bad Credit

Navigating the path to securing auto loans bad credit requires preparation and a proactive approach. Here are the core strategies you need to employ:

1. Know Your Credit Score and Report Inside Out

Before you even think about stepping onto a car lot or applying for a loan, you absolutely must understand your current credit standing. This means pulling your credit report from all three major bureaus (Experian, Equifax, TransUnion) and reviewing your credit score.

You are entitled to a free credit report from each bureau once every 12 months via AnnualCreditReport.com. Scrutinize these reports for any inaccuracies or errors. Pro tip from us: Even a small mistake on your report could negatively impact your score. Dispute any discrepancies immediately, as correcting them could give your score a vital boost.

2. Save for a Significant Down Payment

One of the most impactful things you can do to improve your chances of approval for a car loan with poor credit is to make a substantial down payment. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk.

When a lender sees you’re investing your own money upfront, it signals commitment and can make them more comfortable extending credit. Aim for at least 10-20% of the car’s purchase price, if possible. Even a smaller down payment is better than none.

3. Explore Different Lender Types

Not all lenders are created equal, especially when it comes to financing a car with bad credit. Broaden your search beyond traditional banks. Here are some avenues to explore:

- Subprime Lenders: These financial institutions specialize in lending to individuals with lower credit scores. They understand the challenges and structure loans accordingly.

- Dealership Financing: Many dealerships have relationships with multiple lenders, including those who cater to subprime borrowers. They can often streamline the application process. Be cautious with "buy-here-pay-here" lots, as they often have very high interest rates and less consumer protection, though they can be a last resort.

- Credit Unions: Often more community-focused than large banks, credit unions may be more willing to work with members who have bad credit. Their interest rates can also be more competitive.

- Online Lenders: A growing number of online platforms specialize in bad credit auto loans. These can be convenient and allow you to compare offers from multiple lenders quickly, often providing pre-approval options.

When searching for "car loans near me for bad credit," start by looking for local credit unions and dealerships that advertise special financing programs. This local approach can sometimes yield more personalized service and better understanding of your specific situation.

4. Consider a Co-Signer

If you have a trusted family member or friend with good credit who is willing to co-sign your loan, this can significantly improve your approval odds and potentially secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

Common mistakes to avoid are asking someone who isn’t fully aware of the responsibility or who has their own shaky financial standing. A co-signer’s credit will be affected if you miss payments, so this decision should be made with extreme care and mutual understanding.

5. Choose the Right Vehicle for Your Budget

When your credit isn’t perfect, it’s crucial to prioritize affordability over luxury. Opt for a reliable used car that meets your essential needs rather than an expensive new model. A lower purchase price means a smaller loan amount, which translates to lower monthly payments and less risk for the lender.

Pro tips from us: Focus on cars that are known for their longevity and lower maintenance costs. A car that costs less to buy and own will make it easier to consistently make your payments, which is vital for rebuilding your credit.

6. Get Pre-Approved Before You Shop

One of the most powerful tools in your arsenal is pre-approval. This process involves a lender evaluating your financial situation and provisionally agreeing to lend you a certain amount, usually at a specific interest rate, before you’ve even chosen a car.

Based on my experience, walking into a dealership with a pre-approval letter in hand transforms you from a hopeful buyer into a confident negotiator. It gives you a clear budget, tells the dealership you’re serious, and allows you to focus on the car’s price rather than getting caught up in financing details at the sales desk. This is especially useful when seeking car loans near me for bad credit, as it puts you in control.

The Application Process: What to Expect

Once you’ve done your homework and chosen a potential lender, the application process for getting a car loan with poor credit will typically involve providing several key documents:

- Proof of Income: Pay stubs, tax returns, or bank statements. Lenders want to see stable, sufficient income to cover your loan payments.

- Proof of Residency: Utility bills or lease agreements. This verifies your address.

- Proof of Identity: Driver’s license or state ID.

- Credit Report: The lender will pull this, but having reviewed yours beforehand means no surprises.

- Down Payment: Be ready to provide this at the time of purchase.

Lenders specializing in subprime auto loans are primarily looking for stability and your ability to repay. They understand past credit issues, but they want to see that your current situation is stable enough to handle a new financial commitment.

Common mistakes to avoid are applying for multiple loans simultaneously without checking if they are "soft" or "hard" inquiries, as too many hard inquiries can further ding your score. Also, never misrepresent your income or financial situation; honesty is always the best policy.

Improving Your Chances & Future Credit

Securing a bad credit car loan isn’t just about getting a vehicle; it’s also a golden opportunity to rebuild your credit history. Here’s how:

- Make Every Payment On Time: This is paramount. Consistent, on-time payments are the single most effective way to improve your credit score. Lenders report your payment history to credit bureaus, directly impacting your score.

- Avoid New Credit: While paying off your car loan, try to avoid taking on new debts. This shows financial discipline and focuses your resources on your current obligations.

- Monitor Your Credit Regularly: Keep an eye on your credit report to ensure payments are being reported correctly and to catch any new errors.

A successfully managed auto loan can significantly boost your credit score over time, opening doors to better financial products and lower interest rates in the future.

"Car Loans Near Me For Bad Credit": Navigating Local Options

When you search for "car loans near me for bad credit," you’re looking for local solutions that can offer convenience and sometimes, more personalized service. Here’s how to maximize your local search:

- Local Dealerships: Many dealerships have "special finance" departments. They often work with a network of subprime lenders and can help match you with a suitable loan. Visit a few different dealerships to compare offers.

- Community Banks & Credit Unions: As mentioned, these institutions often have a more flexible approach to lending, especially if you have an existing relationship with them. They might be more willing to look beyond just your credit score and consider your overall financial picture.

- Online Search Filters: Use filters on search engines and financial aggregators to specifically target lenders in your geographic area that cater to bad credit borrowers.

While "buy-here-pay-here" dealerships are local and cater to bad credit, exercise extreme caution. Their interest rates are often very high, and terms can be less favorable. If considering one, read every line of the contract, understand all fees, and ensure they report payments to credit bureaus so you can build credit.

For more details on improving your credit score, check out our guide on .

Pro Tips from an Expert: Your Ultimate Checklist

Based on my experience working with countless individuals navigating the challenges of bad credit, here are some final, invaluable pro tips:

- Read the Fine Print: Never sign anything until you’ve thoroughly read and understood every single clause in the loan agreement. Pay close attention to the interest rate (APR), loan term, total cost of the loan, and any prepayment penalties. If you’re unsure about the difference between APR and interest rate, our article can help clarify.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or if the terms seem too restrictive or expensive, be prepared to walk away. There are always other options and other lenders.

- Negotiate Beyond the Monthly Payment: Salespeople often focus on the monthly payment to make a car seem affordable. Always negotiate the total price of the car first, then discuss financing. Understand the total cost of the loan over its entire term, not just what you’ll pay each month.

- Understand Add-ons: Be wary of high-pressure sales tactics for add-ons like extended warranties, GAP insurance, or etching. While some can be beneficial, ensure they are genuinely needed and not just inflating your loan amount.

- Check for Hidden Fees: Ask for a full breakdown of all fees associated with the loan and the purchase. This includes documentation fees, processing fees, and title and registration costs.

For additional unbiased financial advice on car loans, you can always consult trusted external sources like the Consumer Financial Protection Bureau (CFPB) at . They offer excellent resources to help you make informed decisions.

Your Road to Approval Starts Here

Securing car loans near me for bad credit is a goal that is absolutely within your reach. It requires diligence, research, and a strategic approach, but it is entirely achievable. By understanding your credit, exploring all your lending options, preparing a down payment, and making smart choices about your vehicle, you can overcome past financial hurdles.

Remember, this isn’t just about getting a car; it’s about taking a crucial step towards rebuilding your financial health. With every on-time payment, you’re improving your credit score and opening doors to a more secure financial future. So, take a deep breath, equip yourself with the knowledge from this guide, and confidently embark on your journey to finding the perfect car and the right loan. Your path to a reliable ride, and better credit, begins now!