Car Loans Salt Lake City: Your Ultimate Guide to Financing Your Ride in SLC

Car Loans Salt Lake City: Your Ultimate Guide to Financing Your Ride in SLC Carloan.Guidemechanic.com

Navigating the world of car loans can feel like a winding mountain road, especially when you’re looking for the best options right here in Salt Lake City. Whether you’re a first-time buyer, looking to upgrade, or simply need to understand your financing options, securing the right car loan is crucial. It’s not just about getting a vehicle; it’s about smart financial planning that fits your lifestyle in the heart of Utah.

This comprehensive guide is designed to be your trusted resource for everything related to car loans Salt Lake City. We’ll delve deep into the process, reveal expert tips, and help you confidently drive away with a deal that makes sense for you. From understanding interest rates to navigating bad credit situations, we’ve got you covered.

Car Loans Salt Lake City: Your Ultimate Guide to Financing Your Ride in SLC

Why Salt Lake City Car Loans Matter for Local Drivers

Salt Lake City offers a unique blend of urban living and easy access to stunning natural landscapes. From daily commutes downtown to weekend adventures in the Wasatch Front, a reliable vehicle is often essential for residents. This makes auto financing in SLC a critical component of life for many.

The local market dynamics, including specific lenders and economic factors, can influence the types of car loans Salt Lake City residents can access. Understanding these nuances is key to finding the most favorable terms for your vehicle purchase. Our goal is to empower you with local insights and universal financial wisdom.

Understanding the Fundamentals of Car Loans

Before diving into the specifics of car loans Salt Lake City, it’s essential to grasp the basic terminology. A car loan is essentially a sum of money borrowed from a lender to purchase a vehicle, which you then repay over a set period, usually with interest.

Knowing these key terms will help you speak confidently with lenders and understand your loan agreement. It demystifies the process, putting you in a stronger negotiating position.

Key Terms You Need to Know:

- Principal: This is the initial amount of money you borrow to buy the car. It’s the purchase price minus any down payment or trade-in value.

- Interest Rate: Expressed as a percentage, this is the cost of borrowing money. A lower interest rate means you pay less over the life of the loan.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer term usually means lower monthly payments but more interest paid overall.

- Annual Percentage Rate (APR): The APR represents the total annual cost of your loan, including the interest rate and any additional fees. It’s a more accurate measure of the loan’s true cost than the interest rate alone.

- Down Payment: This is the initial amount of cash you pay upfront for the vehicle. A larger down payment can reduce the principal, lower your monthly payments, and potentially secure a better interest rate.

Based on my experience, many buyers focus solely on the monthly payment. While important, understanding the APR and total cost of the loan is far more critical for your long-term financial health.

Exploring the Types of Car Loans Available in Salt Lake City

The landscape of car financing Utah is diverse, offering various loan types to suit different needs and financial situations. Knowing which type of loan aligns with your purchase can significantly impact your overall experience and costs.

Whether you’re eyeing a brand-new model or a reliable pre-owned vehicle, there’s a specific loan product designed for you. Let’s explore the common options for auto loans SLC residents can consider.

New Car Loans

These loans are specifically for brand-new vehicles straight from the dealership. They often come with competitive interest rates due to the lower risk associated with financing a new asset. Lenders typically view new cars as having a predictable value depreciation schedule.

Many dealerships in Salt Lake City offer attractive promotional rates on new car loans, sometimes even 0% APR for qualified buyers. However, these often require excellent credit.

Used Car Loans

If you’re looking for a pre-owned vehicle, a used car loan is your go-to option. These loans are structured similarly to new car loans but may have slightly higher interest rates due to the vehicle’s age and mileage. The risk for the lender is generally higher with a used car.

When considering a used car loan in Salt Lake City, be sure the vehicle’s age and mileage don’t exceed the lender’s limits, as some institutions have restrictions on financing older models.

Refinance Car Loans Salt Lake City

Already have a car loan but think you could get a better deal? A refinance car loan allows you to replace your existing auto loan with a new one, often with a lower interest rate or different terms. This can save you a substantial amount of money over the life of the loan.

Pro tip from us: If your credit score has improved since you first financed your car, or if interest rates have dropped, refinancing your car loan in Salt Lake City could be a very smart financial move.

Bad Credit Car Loans SLC

Don’t let a less-than-perfect credit score deter you from finding reliable transportation. Many lenders in Salt Lake City specialize in bad credit car loans SLC, understanding that financial hiccups happen. While the terms might be less favorable initially, these loans provide an opportunity to rebuild your credit.

We’ll dive deeper into navigating bad credit options later, but know that approval is often possible with the right approach and realistic expectations.

Private Party Car Loans

If you’re planning to buy a car from an individual seller rather than a dealership, you’ll need a private party car loan. Not all lenders offer these, as they involve a different set of risks and paperwork compared to dealership financing.

When pursuing a private party loan, the lender will likely require an appraisal of the vehicle to ensure its value aligns with the loan amount. This protects both you and the lender.

The Car Loan Application Process in SLC: Step-by-Step

Securing a car loan in Salt Lake City involves several key steps, from preparing your finances to signing the final papers. Understanding this process can significantly streamline your experience and help you avoid common pitfalls.

As a seasoned professional in auto financing, I’ve seen countless applications. Preparation is the single biggest factor in a smooth approval process.

1. Check Your Credit Score and Report

Your credit score is the most significant factor lenders consider when evaluating your loan application. It directly influences the interest rate you’ll be offered. Before you even start car shopping, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) and check your score.

Reviewing your report allows you to identify and dispute any inaccuracies that could negatively impact your score. A higher score typically translates to better loan terms for car loans Salt Lake City.

2. Determine Your Budget

Before falling in love with a specific car, establish a realistic budget. Consider not just the monthly loan payment, but also insurance, fuel, maintenance, and registration costs specific to Utah. A common mistake is overlooking these additional expenses.

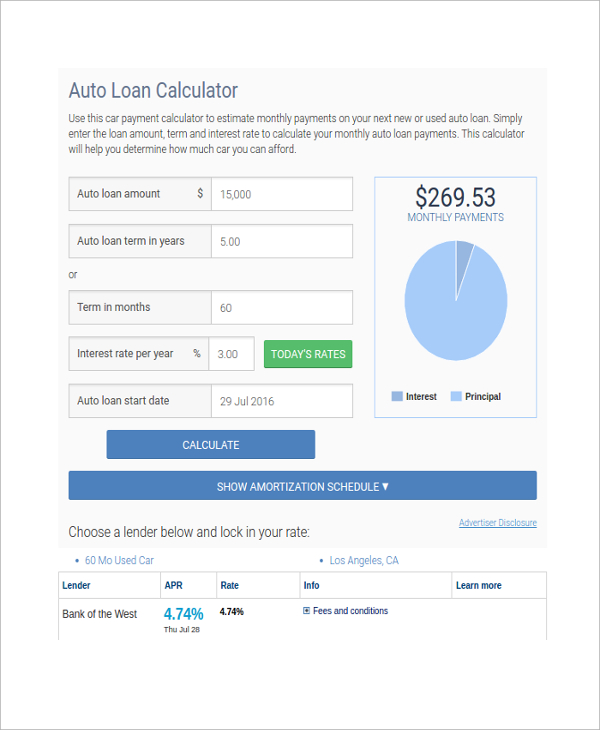

Use online calculators to estimate potential monthly payments based on different loan amounts and interest rates. This foresight will prevent financial strain down the road.

3. Get Pre-Approved for a Loan

Pre-approval is a game-changer. It means a lender has reviewed your financial information and provisionally agreed to lend you a specific amount at a certain interest rate. This gives you concrete buying power before you even step onto a dealership lot.

Having a pre-approval from a bank or credit union in Salt Lake City turns you into a cash buyer at the dealership, giving you a strong negotiating position. It shifts the focus from "Can I get approved?" to "Which car do I want?"

4. Gather Required Documents

Lenders will need specific documents to finalize your loan. Having these ready in advance can speed up the approval process.

Common documents include:

- Proof of identity (driver’s license)

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bill)

- Social Security number

- Vehicle information (for private party loans or refinancing)

5. Shop for Your Car

With pre-approval in hand, you can confidently shop for your desired vehicle. You know exactly how much you can spend, which narrows down your options and prevents you from overextending your budget.

Remember to test drive multiple vehicles and research their reliability and resale value, especially for used car loans Salt Lake City.

6. Finalize Your Loan

Once you’ve chosen your car, you’ll work with the lender to finalize the loan terms. This is where you review the contract carefully, ensuring all agreed-upon terms, interest rates, and fees are accurately reflected.

Don’t hesitate to ask questions if anything is unclear. This is a legally binding agreement, so complete understanding is crucial.

Finding the Best Car Loan Rates in Salt Lake City

Securing the lowest possible interest rate on your car loan Salt Lake City can save you thousands of dollars over the loan term. It requires a bit of effort, but the financial rewards are significant.

The difference between a good rate and an average rate can be substantial, so shopping around is not just recommended, it’s essential.

Shop Around: Banks, Credit Unions, and Online Lenders

Don’t settle for the first offer you receive. Different lenders have varying criteria and rates.

- Local Banks: Large banks in Salt Lake City like Zions Bank or Wells Fargo offer competitive rates, especially for customers with strong credit.

- Credit Unions: Credit unions such as Mountain America Credit Union or Goldenwest Credit Union are often known for offering lower interest rates and more flexible terms to their members. They are member-owned, which often translates to better deals.

- Online Lenders: Companies like LightStream or Capital One Auto Finance provide convenient online applications and often pre-approval options. They can be a great option for comparing rates quickly.

Pro tip from an expert: Apply to 3-5 different lenders within a short timeframe (usually 14-30 days) to minimize the impact on your credit score. Multiple inquiries within this window are typically treated as a single inquiry for rate shopping.

Negotiate Your Rate

Even after receiving an offer, there might be room for negotiation, especially if you have multiple offers. Use competing offers as leverage to push for a lower rate from your preferred lender.

Dealerships also want your business, so present your pre-approval letter and see if they can beat it. Sometimes they have special financing programs directly from the manufacturer.

Improve Your Credit Score

As mentioned, your credit score is paramount. If you have time before needing a car loan, focus on improving your score. This involves paying bills on time, reducing existing debt, and avoiding new credit applications.

For more detailed insights into managing your credit, check out our guide on . (Simulated internal link)

Credit Scores and Your Car Loan: What You Need to Know

Your credit score acts as your financial report card, signaling to lenders how risky you are as a borrower. A strong score can unlock the best car loan rates Salt Lake City, while a lower score might mean higher interest or more limited options.

Understanding how your score impacts your loan is crucial for setting realistic expectations and strategizing your approach.

How Credit Scores Are Calculated (Briefly)

Your FICO score, the most commonly used, considers several factors:

- Payment History (35%): Timely payments are key.

- Amounts Owed (30%): How much debt you carry relative to your credit limits.

- Length of Credit History (15%): Older accounts are generally better.

- New Credit (10%): Avoid opening too many new accounts at once.

- Credit Mix (10%): Having a variety of credit types (e.g., credit cards, mortgage, auto loan) can be beneficial.

Good vs. Fair vs. Bad Credit Implications

- Excellent (780-850): Expect the very best rates and terms.

- Good (670-779): Still eligible for competitive rates, though not always the absolute lowest.

- Fair (580-669): You’ll likely pay higher interest rates, but approval is still common.

- Poor (300-579): This is where bad credit car loans SLC come into play. Expect significantly higher rates and possibly a requirement for a larger down payment or a co-signer.

Strategies to Improve Credit Before Applying

If your score isn’t where you want it, consider these steps:

- Pay bills on time, every time. This is the most impactful factor.

- Reduce credit card balances. Aim for utilization below 30%.

- Avoid closing old accounts. This shortens your credit history.

- Check for and dispute errors on your credit report.

Navigating Bad Credit Car Loans in Salt Lake City

Having a low credit score doesn’t mean you can’t get a car loan. It simply means you’ll need to approach the process strategically. Many lenders in Salt Lake City are equipped to offer bad credit car loans SLC, providing essential transportation for those rebuilding their financial standing.

It’s a pathway to not only getting a car but also potentially improving your credit score with responsible repayment.

Yes, It’s Possible to Get a Car Loan with Bad Credit!

The key is to understand that lenders specializing in bad credit loans take on more risk. As a result, they mitigate this risk with higher interest rates, shorter loan terms, or requirements for larger down payments. Don’t be discouraged; focus on finding the best terms available for your situation.

Specialized Lenders and Dealerships

Look for dealerships advertising "bad credit financing" or "second-chance auto loans." Many have relationships with subprime lenders who specialize in working with borrowers with lower credit scores. Credit unions might also offer more flexible terms than traditional banks.

Tips for Securing Approval with Bad Credit:

- Larger Down Payment: A substantial down payment reduces the amount you need to borrow, making you less risky to lenders.

- Co-signer: If you have a trusted friend or family member with good credit willing to co-sign, it can significantly improve your chances of approval and secure a better rate.

- Realistic Vehicle Choice: Opt for an affordable, reliable used car rather than an expensive new one. This lowers the loan amount and reduces the overall risk.

- Proof of Stable Income: Lenders want to see that you can consistently make payments. Provide clear documentation of stable employment and income.

Common Mistakes to Avoid When Seeking Bad Credit Loans:

- Falling for "Guaranteed Approval" Scams: No reputable lender can guarantee approval without reviewing your financial information. Be wary of such promises.

- Ignoring the APR: Because rates will be higher, it’s even more critical to understand the full APR, not just the monthly payment. For clarity, our article on can help. (Simulated internal link)

- Not Checking Your Credit Report First: You need to know exactly what lenders will see. Correcting errors can make a big difference.

The Role of Down Payments and Trade-Ins

Your down payment and any vehicle trade-in are powerful tools in reducing the total cost of your car loan Salt Lake City. These directly reduce the principal amount you need to finance.

Understanding how to leverage these can save you money and improve your loan terms.

Benefits of a Larger Down Payment

- Lower Monthly Payments: Less money borrowed means smaller installments.

- Reduced Total Interest Paid: You’re financing less, so you accrue less interest over time.

- Better Interest Rates: Lenders see a larger down payment as a sign of financial commitment, making you a less risky borrower.

- Avoid Being Upside Down: A larger down payment helps prevent you from owing more on the car than it’s worth, especially as depreciation sets in.

Based on my experience, aiming for at least 10-20% down on a new car and 5-10% on a used car is a solid strategy.

How Trade-Ins Work

If you have an existing vehicle, trading it in at a dealership can serve as a down payment. The dealership will assess its value and apply that amount directly to your new purchase.

Always research your car’s trade-in value beforehand using resources like Kelley Blue Book or Edmunds. This ensures you get a fair offer. You can also consider selling your car privately to potentially get more money, though this requires more effort.

Understanding Loan Terms and Monthly Payments

The length of your car loan (the term) significantly impacts both your monthly payment and the total amount of interest you’ll pay. It’s a balancing act between affordability and overall cost.

This is a critical decision point for anyone pursuing auto loans SLC.

Short vs. Long Terms

- Shorter Terms (e.g., 36 or 48 months):

- Pros: Pay less interest overall, pay off the loan faster, build equity quicker.

- Cons: Higher monthly payments.

- Longer Terms (e.g., 60 or 72 months, sometimes 84 months):

- Pros: Lower monthly payments, making the car more affordable in the short term.

- Cons: Pay significantly more interest over the life of the loan, take longer to build equity, higher risk of being "upside down" on the loan.

Common pitfalls we’ve observed: Many buyers extend their loan term to lower the monthly payment without realizing the substantial increase in total interest paid. Always ask for the total cost of the loan for different terms.

Common Mistakes to Avoid When Getting a Car Loan in Salt Lake City

Even experienced buyers can make missteps during the car loan process. Being aware of these common errors can save you time, money, and stress when seeking car loans Salt Lake City.

Arming yourself with knowledge is your best defense against less-than-ideal outcomes.

- Not Getting Pre-Approved: As discussed, pre-approval is your power move. Without it, you’re negotiating blindly at the dealership.

- Focusing Only on Monthly Payments: This is a classic trap. A low monthly payment can hide a very long loan term or a high interest rate, leading to significantly more money paid over time.

- Ignoring the APR: The interest rate alone doesn’t tell the whole story. The APR includes all fees and is the true measure of your loan’s cost. Always compare APRs.

- Not Checking Your Credit Report: Errors on your report could be costing you a better rate. Always review it before applying.

- Rushing the Decision: Car buying and financing should not be rushed. Take your time to research, compare offers, and understand all the terms.

- Accepting Dealership Financing Without Comparing: While convenient, dealership financing isn’t always the best deal. Compare it with offers from banks and credit unions.

- Not Reading the Fine Print: Every line of your loan agreement matters. Understand all clauses, including prepayment penalties (rare for auto loans but possible), late fees, and default terms.

Pro Tips for a Smooth Car Loan Experience in SLC

As a seasoned professional in auto financing, I’ve seen firsthand what leads to a successful and stress-free car buying journey. These pro tips are designed to give you an edge in the Salt Lake City market.

Be Prepared and Organized

Have all your financial documents, credit report, and pre-approval letters organized and ready. This professionalism signals to lenders and dealerships that you’re a serious and responsible buyer.

Don’t Be Afraid to Negotiate

Everything is negotiable – the car price, the trade-in value, and even the interest rate. Use your pre-approval to negotiate the car’s price first, separate from financing. Then, discuss financing options.

Consider a Shorter Loan Term If Possible

While a longer term means lower monthly payments, a shorter term saves you a lot in interest. If your budget allows, opt for the shortest term you can comfortably afford.

Automate Your Payments

Set up automatic payments from your bank account. This ensures you never miss a payment, which is crucial for maintaining a good credit score and avoiding late fees.

Know Your Vehicle’s Value

Whether buying or trading in, understanding the market value of the vehicle you’re interested in is paramount. Resources like Kelley Blue Book, Edmunds, and NADAguides provide excellent valuation tools. This knowledge helps you determine a fair purchase price and a fair trade-in value.

Local Considerations for Salt Lake City Drivers

Salt Lake City’s unique environment adds a few specific considerations when choosing a vehicle and securing its financing. These local factors can influence your choice of car and, consequently, your loan needs.

- Weather and Terrain: SLC experiences all four seasons, including significant snowfall in winter. Many residents opt for all-wheel-drive (AWD) or four-wheel-drive (4WD) vehicles for better traction. Financing a slightly more expensive AWD vehicle might be a priority for safety and utility.

- Commute Patterns: While downtown is walkable, many residents commute across the valley or into surrounding areas. Fuel efficiency and comfort for longer drives are often important.

- Outdoor Lifestyle: With mountains and national parks nearby, vehicles suitable for outdoor recreation (SUVs, trucks) are popular. These might command higher prices and thus larger loan amounts.

Factor these elements into your decision-making process for car loans Salt Lake City to ensure your vehicle truly meets your lifestyle needs.

Your Road to a Great Car Loan in Salt Lake City Starts Here

Securing a car loan in Salt Lake City doesn’t have to be a daunting task. By understanding the fundamentals, preparing thoroughly, and knowing how to navigate the lending landscape, you can confidently find a financing solution that perfectly fits your budget and lifestyle. Remember, knowledge is power when it comes to financial decisions.

We hope this comprehensive guide has provided you with the insights and tools necessary to make informed choices for your next vehicle purchase. Drive safely and smartly!