Cracking the Car Loan Numbers Crossword: Your Ultimate Guide to Decoding Auto Financing

Cracking the Car Loan Numbers Crossword: Your Ultimate Guide to Decoding Auto Financing Carloan.Guidemechanic.com

The thrill of a new car — the scent of fresh upholstery, the gleam of polished paint, the promise of open roads. It’s an exciting prospect, but for many, the joy quickly turns to apprehension when the conversation shifts to financing. Suddenly, you’re faced with a barrage of terms, percentages, and figures that can feel as intricate and baffling as a complex crossword puzzle.

This is where the "Car Loan Numbers Crossword" metaphor truly comes to life. Each number, from the APR to the loan term, represents a crucial clue. Misunderstand even one, and you might find yourself stuck, unable to complete the picture of affordable car ownership. But what if you had an expert guide to help you decipher every clue and solve the puzzle with confidence?

Cracking the Car Loan Numbers Crossword: Your Ultimate Guide to Decoding Auto Financing

Based on my extensive experience in automotive finance and consumer education, I understand the challenges borrowers face. This comprehensive guide is designed to empower you. We’ll break down every element of a car loan, transforming those intimidating "car loan numbers" into clear, actionable insights. By the end, you’ll not only solve your current car loan crossword but also gain the skills to tackle any future auto financing challenge.

The Essential Puzzle Pieces: Key Car Loan Terminology & Numbers

Before you can solve any puzzle, you need to understand its fundamental components. Car loans are no different. They come with a specific vocabulary and a set of numerical elements that directly impact your financial well-being. Grasping these basics is your first step towards mastering the car loan numbers crossword.

The All-Important APR (Annual Percentage Rate)

Many people confuse the interest rate with the Annual Percentage Rate (APR), but understanding the distinction is crucial. The interest rate is simply the cost of borrowing the principal loan amount. The APR, however, gives you a more comprehensive picture of the total cost of your loan over a year.

It includes not only the interest rate but also any additional fees or charges associated with the loan, such as origination fees or processing fees. Therefore, when comparing loan offers, always look at the APR, as it provides the true annual cost of borrowing. A lower APR directly translates to less money paid over the life of the loan.

Understanding Loan Term: Your Time Commitment

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This number significantly influences both your monthly payment and the total amount of interest you’ll pay. A longer loan term means lower monthly payments, which might seem appealing at first glance.

However, a longer term also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term will result in higher monthly payments but a significantly lower total interest paid. It’s a delicate balance between affordability and long-term cost, a key "car loan number" to consider carefully.

Principal, Interest, and the Total Cost of the Loan

The principal amount is the initial sum of money you borrow to purchase the car. Interest is the cost you pay for borrowing that principal, calculated as a percentage of the outstanding balance. Every monthly payment you make is split between reducing the principal and covering the accrued interest.

Pro tips from us: Always focus on the "total cost of the loan," not just the monthly payment. This total cost includes the principal borrowed plus all the interest you will pay over the full loan term. Dealers often highlight low monthly payments without emphasizing the extended term and higher overall cost.

The Power of a Down Payment

A down payment is the initial sum of money you pay upfront for the car, reducing the amount you need to borrow. This is one of the most powerful "car loan numbers" you can control. A larger down payment immediately lowers your principal loan amount.

This, in turn, reduces the total interest you’ll pay over the loan’s life and often results in a lower monthly payment. Furthermore, a substantial down payment can make you a less risky borrower in the eyes of lenders, potentially qualifying you for better interest rates. It’s a clear win-win strategy for smart financing.

Deciphering Your Monthly Payment

Your monthly payment is the fixed amount you’ll send to your lender each month until the loan is fully repaid. This number is a direct result of your principal loan amount, interest rate (or APR), and loan term. While it’s the most visible "car loan number," it can also be the most misleading if you focus on it exclusively.

Dealers are skilled at adjusting loan terms to achieve a desired monthly payment, often stretching the loan out for an extended period. Always remember that a lower monthly payment doesn’t always mean a better deal overall. It’s crucial to understand the total cost implication behind that seemingly attractive monthly figure.

Solving Clue #1: How Your Credit Score Dictates Your Loan Numbers

If car loan numbers are a crossword puzzle, your credit score is the first and most critical clue. It’s the primary factor lenders use to assess your creditworthiness and, consequently, determine the interest rate you’ll be offered. Understanding and managing this number is paramount to securing favorable auto loan financing.

Your Credit Score: The Master Key

Your credit score, typically a FICO Score or VantageScore, is a three-digit number that summarizes your credit risk. It’s generated from the information in your credit reports, reflecting your payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders rely on this score to predict how likely you are to repay your debts.

Scores generally range from 300 to 850, with higher scores indicating lower risk. An excellent score (780-850) signals a highly responsible borrower, while a poor score (300-579) suggests a higher risk of default. This single number profoundly impacts every other car loan number you’ll encounter.

The Direct Impact on Interest Rates

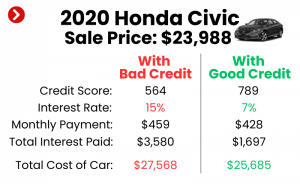

The correlation between your credit score and the interest rate you receive on a car loan is direct and significant. Borrowers with excellent credit scores typically qualify for the lowest available interest rates, sometimes even 0% APR promotions. This means they pay substantially less in interest over the life of the loan.

Conversely, individuals with lower credit scores are considered higher risk, leading to much higher interest rates. For instance, a borrower with a 750 score might get a 3% APR, while someone with a 600 score might face a 10% or even 15% APR on the same car and loan amount. Over five or six years, this difference can amount to thousands of dollars in extra payments, dramatically increasing the total cost of car ownership.

Strategies to Boost Your Credit Score Before Applying

Improving your credit score before applying for a car loan is one of the smartest moves you can make. Start by checking your credit reports from all three major bureaus (Equifax, Experian, TransUnion) for inaccuracies. Dispute any errors immediately, as they can unfairly lower your score.

Focus on paying all your bills on time, as payment history is the most impactful factor. Reduce your outstanding debt, especially on credit cards, to lower your credit utilization ratio. Avoid opening new credit accounts right before applying for an auto loan, as this can temporarily ding your score. Even a modest improvement in your credit score can unlock significantly better auto loan interest rates, making your car loan numbers far more manageable.

Navigating the Labyrinth of Lenders: Where to Find the Best Numbers

Just as a crossword puzzle can have multiple paths to a solution, there are several avenues for securing car loan financing. Each type of lender offers different advantages and disadvantages, and knowing where to look for the best "car loan numbers" is a crucial part of your strategy. Don’t limit your search; exploring all options can lead to significant savings.

Dealership Financing: Convenience vs. Cost

Dealership financing is often the most convenient option, allowing you to handle the car purchase and loan application all in one place. Salespeople can quickly submit your application to multiple lenders, sometimes even offering special manufacturer incentives or promotional rates. This convenience, however, often comes at a cost.

Based on my experience, dealerships frequently mark up the interest rates they receive from lenders, adding profit for themselves. While they might seem to offer competitive rates, it’s always wise to compare their offer with those from other sources. Always remember that the dealer’s primary goal is to sell you a car, not necessarily to get you the absolute lowest interest rate.

Banks and Credit Unions: Your Traditional Allies

Traditional banks and local credit unions are often excellent sources for competitive auto loan financing. Credit unions, in particular, are known for offering some of the lowest interest rates because they are not-for-profit organizations focused on their members’ financial well-being. Building a relationship with your bank or credit union can also provide leverage for better deals.

A significant advantage of these institutions is the ability to get pre-approved for a loan before you even step foot in a dealership. This pre-approval gives you a clear budget and an interest rate, essentially turning you into a cash buyer at the dealership. This power gives you immense negotiation leverage, as the dealer knows you already have financing secured.

Online Lenders: The Digital Advantage

In the digital age, online lenders have emerged as powerful contenders in the auto loan market. Companies like Capital One Auto Finance, LightStream, and others offer streamlined application processes, often with quick approval times. They typically have lower overhead costs, which can translate into very competitive interest rates for qualified borrowers.

Online platforms also make it incredibly easy to compare offers from multiple lenders side-by-side. You can input your information once and receive several personalized quotes without impacting your credit score with multiple hard inquiries. This efficiency and transparency make online lenders a fantastic resource for finding the best car loan deals and understanding the current market rates.

Unlocking the Best Solution: Pro Strategies for Favorable Loan Terms

Solving the "Car Loan Numbers Crossword" isn’t just about understanding the clues; it’s about employing smart strategies to get the best possible outcome. With the right approach, you can significantly reduce your total cost and secure auto loan financing that truly benefits you. These pro tips are drawn from years of observing successful car buyers.

The Art of Pre-Approval: Your Negotiation Superpower

Getting pre-approved for an auto loan from an external lender (bank, credit union, or online lender) before you visit a dealership is arguably the most powerful strategy you can employ. This step separates the car buying process into two distinct negotiations: the price of the car and the terms of the loan. When you walk into a dealership with a pre-approval in hand, you effectively become a cash buyer.

You know your maximum loan amount and your interest rate, giving you a firm baseline for comparison. This prevents the dealer from manipulating loan terms to obscure the true price of the car or inflate their profit margin on the financing. It empowers you to focus solely on negotiating the best vehicle price.

Comparing Offers: Don’t Settle for the First Quote

Never accept the first loan offer you receive, whether it’s from a dealership or your initial bank inquiry. Professional SEO content writer tip: Always shop around! Gather at least three to five loan offers from different types of lenders (banks, credit unions, online lenders, and even the dealership’s best offer). Compare the APR, loan term, and total cost of each offer.

This comparison allows you to identify the most competitive rates and use better offers as leverage in negotiations. Sometimes, a dealership might match or even beat an outside offer to secure your business. Remember, every percentage point reduction in your APR can save you hundreds, if not thousands, of dollars over the loan’s lifetime.

The Smart Approach to Down Payments and Loan Terms

As we discussed, a larger down payment reduces the principal and the total interest paid. Aim for at least a 20% down payment on a new car, if possible, and 10% on a used car. This helps avoid being "upside down" on your loan, meaning you owe more than the car is worth, a common mistake to avoid.

Regarding loan terms, while longer terms offer lower monthly payments, they significantly increase the total interest paid. Based on my experience, generally, a 60-month (5-year) loan is a good balance for new cars, and 36-48 months for used cars. Only consider longer terms (e.g., 72 or 84 months) if absolutely necessary for budget, and ensure the interest rate remains low. For more on this, check out our article:

Beware of Add-ons: Decoding the Extra Numbers

When finalizing your purchase, dealerships often present a menu of "add-ons" like extended warranties, GAP insurance, paint protection, or service contracts. While some of these might offer value, many are highly profitable for the dealer and can unnecessarily inflate your loan amount. Don’t let these additional "car loan numbers" muddy your clear financial picture.

Carefully evaluate each add-on. For instance, GAP insurance can be wise if you make a small down payment, but you might find it cheaper from your auto insurer. Extended warranties can be useful, but research third-party options and negotiate the price. Always ask for the price of add-ons separately and consider if you truly need them before rolling them into your financing.

Common "Crossword" Traps: Mistakes to Avoid in Car Financing

Even with all the right clues, it’s easy to fall into common traps when solving the car loan numbers crossword. Many buyers make predictable errors that cost them significant money and stress. Learning from these common mistakes is just as important as understanding the correct strategies.

The Monthly Payment Myopia

One of the most pervasive and costly mistakes buyers make is focusing solely on the monthly payment. Dealerships are masters at leveraging this. They can easily adjust the loan term to hit your desired monthly payment, often stretching it to 72 or even 84 months. While your monthly outlay might seem manageable, the total interest paid skyrockets.

Common mistakes to avoid are signing up for a loan that makes the car seem affordable month-to-month but ultimately costs you thousands more than necessary. Always ask for the total cost of the loan over its entire term, including all principal and interest. This holistic view reveals the true financial burden.

Skipping the Pre-Approval Step

As highlighted earlier, neglecting to get pre-approved for a loan before visiting a dealership is a significant misstep. Without a pre-approval, you lose a crucial piece of your negotiation power. You enter the dealership without knowing what interest rate you truly qualify for, making you susceptible to less favorable financing offers.

You also lose the ability to easily separate the car price negotiation from the financing negotiation. The dealer can then manipulate both aspects simultaneously, potentially giving you a seemingly good deal on one while making up the difference on the other. This makes comparing apples to apples virtually impossible.

Not Understanding the Total Cost of Ownership

While not strictly part of the loan itself, failing to consider the total cost of car ownership beyond the monthly payment is a common pitfall. Many buyers focus exclusively on the "car loan numbers" and forget about other essential expenses. These include insurance premiums, fuel costs, routine maintenance, unexpected repairs, and registration fees.

Pro tips from us: Always create a comprehensive budget that includes all these recurring costs before committing to a car loan. A car that seems affordable based on its monthly payment might quickly become a financial burden when you factor in all other associated expenses.

The "Pro Solver’s" Toolkit: Advanced Tips for Mastering Your Car Loan

Once you’ve secured your car loan, the puzzle isn’t entirely finished. There are advanced strategies and tools that a "pro solver" uses to optimize their financing, potentially saving even more money and gaining greater financial flexibility. These steps go beyond the initial application process.

Refinancing: A Second Chance at Better Numbers

If your credit score has improved since you first took out your car loan, or if interest rates have dropped significantly, refinancing could be a smart move. Refinancing means taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can significantly reduce your monthly payments or the total interest paid over the life of the loan.

Based on my experience, many people overlook this option, but it can be a powerful tool for financial optimization. Always research current rates and compare them to your existing loan. To learn more about when refinancing is right for you, read our detailed guide:

Making Extra Payments: Accelerating Your Payoff

Even small additional payments can make a huge difference in the total interest you pay and how quickly you pay off your loan. Since interest is calculated on the remaining principal balance, any extra money you apply directly to the principal reduces that base amount, saving you future interest. Consider making bi-weekly payments, which essentially means you make one extra monthly payment per year.

For example, if your payment is $400, paying $200 every two weeks results in 26 half-payments, totaling 13 full payments annually instead of 12. This simple strategy can shave months off your loan term and save you hundreds of dollars in interest.

Understanding Early Payoff Penalties

While rare in standard auto loans, it’s crucial to check your loan agreement for any early payoff penalties. Some loans, particularly older ones or those from less conventional lenders, might include clauses that charge a fee if you pay off your loan before the scheduled term. This is to compensate the lender for the interest they would have earned.

Always review your loan documents carefully before signing. Understanding these "car loan numbers" and clauses ensures you won’t be surprised if you decide to pay off your loan ahead of schedule. For a deeper dive into understanding your loan agreement, refer to our article:

Budgeting Beyond the Loan Payment

A truly savvy car owner budgets for more than just the monthly loan payment. As a professional SEO content writer and finance expert, I always advise clients to consider the full spectrum of costs associated with car ownership. This includes fuel, insurance, maintenance, tires, and potential repair costs.

The Consumer Financial Protection Bureau offers excellent resources for understanding the overall costs of owning a vehicle, helping you make informed decisions beyond the initial purchase price. This holistic view ensures that your car remains an asset, not a financial burden, throughout its lifetime. For valuable tools and information, visit the Consumer Financial Protection Bureau’s Auto Loans section.

Conclusion: Drive Away Confidently

The "Car Loan Numbers Crossword" doesn’t have to be a source of frustration or confusion. With the right knowledge, strategic approach, and a keen eye for detail, you can confidently decipher every clue and solve the puzzle to your advantage. Understanding APR, loan terms, credit scores, and the various lending options empowers you to make informed decisions that save you money in the long run.

By avoiding common pitfalls and utilizing advanced strategies like pre-approval and refinancing, you transform from a puzzled consumer into a savvy auto financing expert. Remember, knowledge is your most powerful tool in the car buying process. Drive away not just with a new car, but with the peace of mind that comes from mastering your auto loan financing.