Cracking the Code: Your Ultimate Guide to Credit for Car Loans and Driving Away Approved

Cracking the Code: Your Ultimate Guide to Credit for Car Loans and Driving Away Approved Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering freedom, convenience, and independence. However, the path to owning your dream vehicle often hinges on one crucial factor: your credit. Understanding "credit for car loan" isn’t just about getting approved; it’s about securing the best possible terms, saving thousands over the life of the loan, and making a financially sound decision.

As an expert in personal finance and auto lending, I’ve seen firsthand how a little knowledge about credit can dramatically change a buyer’s experience. This comprehensive guide will demystify the entire process, providing you with an in-depth understanding of how your credit impacts your car loan, what lenders look for, and actionable strategies to improve your chances of approval with favorable rates. Let’s get you in the driver’s seat, both literally and financially.

Cracking the Code: Your Ultimate Guide to Credit for Car Loans and Driving Away Approved

Understanding the Foundation: What is Credit for a Car Loan?

When we talk about "credit for a car loan," we’re essentially referring to your financial trustworthiness in the eyes of a lender. It’s their way of assessing the risk involved in lending you money to purchase a vehicle. Lenders want to be confident that you will repay the loan as agreed, on time and in full.

This assessment is primarily based on your credit history and credit score. Your credit history chronicles your past borrowing and repayment behaviors, while your credit score distills this information into a three-digit number. This number acts as a quick snapshot of your financial responsibility, influencing everything from your interest rate to the loan term.

How Lenders Assess Your Creditworthiness

Lenders don’t just glance at your credit score and make a snap decision. They delve into various aspects of your financial profile to build a complete picture. This comprehensive evaluation helps them determine not only if you qualify for a car loan but also the specific terms they are willing to offer you. It’s a careful balance of risk versus reward from their perspective.

They look at consistency in payments, your overall debt burden, and how long you’ve managed credit accounts. Their goal is to predict your future payment behavior based on your past actions. A strong credit profile indicates a lower risk, often translating to better loan offers.

The Credit Score Spectrum: How Yours Impacts Your Car Loan

Your credit score is arguably the most influential number when applying for an auto loan. It signals to lenders how likely you are to repay your debts. Understanding where your score falls on the spectrum can help you anticipate the kind of car loan offers you might receive.

Excellent Credit (780+)

If your credit score is 780 or higher, you are in an enviable position. Lenders view you as an extremely low-risk borrower, making you highly attractive. This translates directly into the most favorable loan terms available on the market.

Based on my experience, individuals with excellent credit typically qualify for the lowest interest rates, often advertised as "promo rates" by manufacturers. They also have access to longer loan terms if desired, and enjoy significant flexibility in negotiations. Your application process will likely be smooth and straightforward, with quick approvals.

Good Credit (670-779)

A good credit score indicates a solid financial standing and a history of responsible borrowing. While you might not qualify for the absolute lowest promotional rates, you will still receive very competitive offers. Lenders generally consider you a reliable borrower.

With good credit, you’ll find a wide range of lenders willing to work with you, including major banks, credit unions, and online lenders. You’ll still have strong negotiating power for interest rates and loan terms. It’s always a good idea to shop around for the best deal, even with a good score.

Fair/Average Credit (580-669)

Having a fair or average credit score means you might face slightly higher interest rates compared to those with good or excellent credit. Lenders perceive a bit more risk, so they compensate with a higher Annual Percentage Rate (APR). Approval is certainly possible, but the terms might be less flexible.

For those with fair credit, focusing on a larger down payment can be a game-changer. A substantial down payment reduces the amount you need to borrow, thereby lowering the lender’s risk and potentially qualifying you for a better rate. It demonstrates your commitment and ability to save.

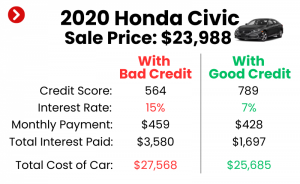

Poor/Bad Credit (Below 580)

Securing a car loan with a poor or bad credit score can be challenging, but it’s not impossible. Lenders consider you a high-risk borrower due to past financial difficulties or a limited credit history. This usually results in significantly higher interest rates and potentially stricter loan conditions.

A common mistake with bad credit is not exploring all your options beyond the first offer. You might need to look at subprime lenders, who specialize in higher-risk loans. Be prepared for higher interest rates, shorter loan terms, or even a requirement for a co-signer. Patience and thorough research are key in this situation.

Key Factors Lenders Consider Beyond Just Your Score

While your credit score is a major component, it’s not the only piece of the puzzle. Lenders delve into several other aspects of your financial life to gauge your overall creditworthiness. These factors collectively paint a more detailed picture of your financial habits and stability.

Understanding these elements can help you prepare for your car loan application and even strengthen your profile. Addressing weaknesses in these areas can significantly improve your chances of approval and secure better terms.

Payment History

This is perhaps the most critical component of your credit report. Lenders scrutinize your record of paying bills on time, especially for other loans and credit cards. A consistent history of timely payments signals reliability and responsibility.

Conversely, late payments, defaults, or bankruptcies will negatively impact your application. They suggest a higher risk of future missed payments. Demonstrating a recent history of on-time payments, even after past issues, can help rebuild trust.

Credit Utilization

Your credit utilization ratio is the amount of revolving credit you’re currently using compared to your total available credit. For example, if you have a credit card with a $10,000 limit and a $3,000 balance, your utilization is 30%. Lenders prefer to see this ratio below 30%, as higher utilization can indicate financial strain.

A low utilization ratio shows that you can manage your credit responsibly without relying too heavily on borrowed funds. It suggests you have a healthy financial buffer and aren’t stretched thin.

Credit Mix

Lenders appreciate seeing a diverse portfolio of credit accounts, such as a mix of revolving credit (credit cards) and installment loans (mortgages, student loans, previous car loans). This demonstrates your ability to manage different types of debt responsibly.

Having only one type of credit, or very few accounts, might not give lenders enough information to assess your risk comprehensively. A well-rounded credit mix often contributes positively to your credit score.

Length of Credit History

The longer your credit accounts have been open and actively managed, the better. A lengthy credit history provides lenders with a substantial record of your borrowing behavior, making it easier for them to assess your risk. It shows consistency over time.

Newer credit profiles, especially for young borrowers, might have thinner files, making it harder for lenders to make a confident decision. Building a long history of responsible credit use is a marathon, not a sprint.

New Credit

Be cautious about opening several new credit accounts or applying for multiple loans in a short period before applying for a car loan. Each application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Too many inquiries can make lenders wary.

It might suggest you are desperate for credit or taking on too much debt. It’s best to space out credit applications and only apply for credit when genuinely needed, especially in the months leading up to a major loan application like a car loan.

Debt-to-Income Ratio (DTI)

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to determine if you can comfortably afford an additional car loan payment. A lower DTI ratio indicates that you have more disposable income to cover your new car payment.

Typically, lenders prefer a DTI ratio below 43%, though this can vary. A high DTI suggests that a significant portion of your income is already allocated to existing debts, raising concerns about your ability to manage a new car loan.

Employment History

Lenders look for stability in your employment. A consistent work history, ideally with the same employer for several years, assures them of a steady income stream. This stability directly impacts your ability to make regular loan payments.

Frequent job changes or periods of unemployment can be red flags, indicating potential income instability. Be prepared to provide proof of income, such as pay stubs or tax returns, to verify your employment and earnings.

Down Payment

While not strictly a credit factor, a substantial down payment significantly impacts your loan approval and terms. It reduces the amount you need to borrow, thereby lowering the lender’s risk. A larger down payment also shows your commitment and financial preparedness.

Pro tips from us: Even with excellent credit, a down payment can secure an even better rate. With less-than-perfect credit, it can be the difference between approval and denial, or between a high and a more manageable interest rate.

Strategies to Improve Your Credit for a Car Loan

Improving your credit takes time and consistent effort, but the benefits, especially when it comes to securing a car loan, are well worth it. By strategically addressing weaknesses in your credit profile, you can significantly enhance your chances of approval and secure more favorable terms.

These steps are foundational for anyone looking to optimize their financial standing before a major purchase. Start early, be diligent, and watch your credit health improve.

Review Your Credit Report

Your first step should always be to obtain and meticulously review your credit reports from all three major bureaus: Experian, Equifax, and TransUnion. Look for any inaccuracies, such as incorrect personal information, accounts that aren’t yours, or outdated negative entries. Errors are surprisingly common and can unfairly lower your score.

For more detailed steps on fixing credit report errors, check out our guide on How to Dispute Credit Report Errors. Correcting these can provide an immediate boost to your score. To get your free annual credit report from a trusted source, visit AnnualCreditReport.com.

Pay Bills On Time

This is the most impactful action you can take to improve your credit. Payment history accounts for a significant portion of your credit score. Make sure all your credit card bills, utility payments, and existing loan installments are paid by their due dates, every single month.

Setting up automatic payments or reminders can help ensure you never miss a deadline. Consistency is key here; a long string of on-time payments will gradually and steadily build your credit.

Reduce Existing Debt

Focus on paying down high-interest revolving debt, such as credit card balances. Lowering your credit utilization ratio (the amount of credit you use versus your total available credit) can quickly improve your score. Aim to keep your utilization below 30% on all cards.

Reducing your overall debt also improves your debt-to-income ratio, making you a more attractive borrower. Prioritize paying off smaller balances first for a psychological win, or target the highest interest debts to save money.

Avoid New Credit Applications

In the months leading up to your car loan application, refrain from opening new credit cards or taking out other loans. Each new application results in a hard inquiry on your credit report, which can temporarily lower your score. It can also make you appear desperate for credit.

Allow your credit profile to stabilize and mature before adding a significant new obligation like a car loan. Focus on managing your existing accounts responsibly.

Become an Authorized User

If you have a trusted family member with excellent credit, they might consider adding you as an authorized user on one of their credit card accounts. This can allow you to benefit from their positive payment history, as long as they continue to manage the account responsibly.

Be aware that their activity will appear on your report, so choose wisely. This strategy is most effective for those with limited credit history.

Secured Credit Cards/Credit Builder Loans

For individuals with very limited or poor credit, secured credit cards or credit builder loans can be excellent tools. A secured credit card requires a cash deposit, which typically becomes your credit limit. This helps you build credit by demonstrating responsible use of a credit card.

Credit builder loans are small loans held in a savings account until you’ve made all payments, then released to you. Both options report your payment activity to credit bureaus, helping you establish or rebuild a positive credit history.

Navigating Car Loans with Less-Than-Perfect Credit

Having less-than-perfect credit doesn’t mean you can’t get a car loan. It simply means you’ll need to be more strategic and perhaps more patient. There are specific avenues and considerations for borrowers with lower credit scores.

The key is to understand your options, manage expectations, and take steps to mitigate the risks for lenders. This approach can help you secure approval and eventually improve your credit for future financial endeavors.

Secured Car Loans

Most car loans are "secured" loans, meaning the vehicle itself acts as collateral. If you fail to make payments, the lender can repossess the car to recover their losses. This inherent security makes lenders more willing to approve loans for those with lower credit scores, as their risk is somewhat reduced.

Understanding this dynamic can help you appreciate why these loans are often more accessible than unsecured personal loans. However, it also underscores the importance of making your payments on time.

Co-Signers

If your credit score is particularly low, a co-signer with good credit can significantly improve your chances of approval. A co-signer legally agrees to be responsible for the loan if you default. Their good credit history essentially offsets your weaker one.

However, understand the implications: the loan appears on their credit report too, and any missed payments by you will negatively impact their score. Only consider this option with someone you trust implicitly and who understands the full responsibility.

Larger Down Payment

As mentioned earlier, a larger down payment is incredibly beneficial for those with fair or poor credit. It reduces the loan amount, thereby decreasing the lender’s exposure to risk. This can often lead to approval when it might otherwise be denied.

It can also help you qualify for a slightly lower interest rate, as the loan-to-value (LTV) ratio becomes more favorable. The more you put down, the less risky you appear.

Buy Here, Pay Here Dealerships

"Buy here, pay here" (BHPH) dealerships offer in-house financing, often catering specifically to individuals with bad or no credit. While they can provide a path to car ownership, be aware of the trade-offs. Interest rates at BHPH dealerships are typically much higher than traditional lenders.

Common mistakes to avoid are not fully understanding the total cost of the loan and only focusing on the monthly payment. Scrutinize the contract carefully and be prepared for higher overall costs.

Pre-Approval

Regardless of your credit score, seeking pre-approval from multiple lenders (banks, credit unions, online lenders) before visiting a dealership is a crucial step. Pre-approval gives you a clear idea of the loan amount and interest rate you qualify for. It empowers you with leverage.

With a pre-approval in hand, you can negotiate with the dealership on the car price, not the financing. This prevents them from manipulating the numbers to their advantage.

Consider a Used Car

For those with challenging credit, opting for a used car can be a more realistic and financially sound choice. Used cars are generally less expensive, which means you’ll need to borrow less money. A smaller loan amount is often easier to get approved for, especially with a lower credit score.

This approach can help you establish a positive payment history on a car loan, which will in turn improve your credit for future, perhaps more expensive, purchases.

The Car Loan Application Process: What to Expect

Navigating the car loan application process can feel daunting, but being prepared makes a world of difference. Understanding each step, from gathering documents to negotiating terms, empowers you to make informed decisions and secure the best possible outcome for your "credit for car loan" journey.

This systematic approach minimizes stress and maximizes your chances of a successful application. Don’t rush; take your time to ensure everything is in order.

Gather Documents

Before you even start shopping for a car or a loan, collect all necessary documentation. This typically includes government-issued identification (driver’s license), proof of residence (utility bill), proof of income (pay stubs, tax returns), and bank statements. Having these ready will streamline the application process.

Some lenders might also ask for proof of insurance or references. Being organized shows preparedness and responsibility.

Shop Around for Lenders

Do not settle for the first loan offer you receive, especially if it’s from the dealership. Explore various lending options:

- Banks: Offer competitive rates, especially if you have an existing relationship.

- Credit Unions: Often have some of the best rates and more flexible terms, particularly for members.

- Online Lenders: Provide quick approvals and competitive rates, often specializing in different credit tiers.

- Dealership Financing: Convenient, but usually mark up interest rates for profit. Use their offer as a point of negotiation against your pre-approved rates.

Pro tips from us: Apply for pre-approval with several lenders within a 14-day window. Multiple inquiries within this period typically count as a single hard inquiry for credit scoring models, minimizing impact.

Pre-Approval vs. Application

Understand the difference between pre-qualification, pre-approval, and a full application.

- Pre-qualification: A soft credit pull (no impact on score) gives you an estimate of what you might qualify for.

- Pre-approval: Involves a hard credit inquiry, giving you a firm offer of a loan amount, interest rate, and terms, valid for a certain period. This is what you want before hitting the dealership.

- Full Application: This is when you formally apply for the loan with a specific vehicle in mind, often through the dealership or directly with your chosen lender.

Always aim for pre-approval to have leverage.

Understanding the Loan Offer

Once you receive loan offers, don’t just look at the monthly payment. Scrutinize the following:

- APR (Annual Percentage Rate): This is the true cost of borrowing, including interest and fees. Compare APRs, not just interest rates.

- Loan Term: How long you have to repay the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid overall.

- Total Cost of the Loan: Multiply your monthly payment by the number of months in the term, then add your down payment. This gives you the actual total expense.

- Fees: Look for origination fees, application fees, or prepayment penalties.

Negotiating

Remember, everything is negotiable. This includes not just the price of the car, but also the terms of the loan. If you have a pre-approval from an external lender, use it to challenge the dealership’s financing offer. They might match or even beat it to keep your business.

Negotiate the purchase price of the car first, then discuss financing. Don’t let them combine the two, as it can confuse the real numbers.

Pro Tips for Securing the Best Car Loan

Securing the best car loan goes beyond just having good credit; it involves strategic planning and savvy negotiation. As an expert, I’ve compiled these "pro tips" to give you an edge in the car buying process.

These insights are drawn from years of observing successful borrowers and helping clients avoid common pitfalls. Implement these, and you’ll be well on your way to a smart car loan.

Know Your Budget

Before you even start looking at cars, determine your absolute maximum budget. This includes not just the car price and loan payment, but also insurance, registration, fuel, and estimated maintenance costs. A common mistake is focusing only on the car’s price.

Based on my experience, many buyers overlook the ongoing costs of car ownership, leading to financial strain later. A good rule of thumb is that your total monthly car expenses shouldn’t exceed 10-15% of your net monthly income.

Get Your Credit Report and Score

Always, always know your credit standing before you step foot in a dealership or apply for a loan. Obtain your credit report and score weeks or even months in advance. This allows you time to correct any errors and understand where you stand.

Knowing your score empowers you to anticipate offers and confidently challenge any unfavorable terms. It’s your financial report card.

Don’t Settle for the First Offer

This cannot be stressed enough. Lenders and dealerships operate on margins, and their first offer is rarely their best. Comparison shop aggressively for loan rates. Get multiple pre-approvals from different types of lenders.

Use these offers as leverage against each other. For example, if your credit union offers 4.5%, tell the bank, and see if they can beat it. This competitive dynamic works in your favor.

Beware of Add-ons

Dealerships often try to upsell you on various add-ons like extended warranties, paint protection, undercoating, or GAP insurance. While some, like GAP insurance, might be worthwhile depending on your situation, many are overpriced and unnecessary.

Pro tips from us: Always scrutinize these additions. Negotiate their prices separately or decline them if they don’t offer real value. Don’t let them roll these high-profit items into your loan without careful consideration.

Read the Fine Print

Before signing any loan agreement, meticulously read every single clause. Understand the APR, the total loan amount, any penalties for late payments, and prepayment clauses. Don’t let anyone rush you.

If you have questions, ask them and demand clear answers. A common mistake is signing without fully comprehending the commitment, leading to costly surprises down the road.

Common Mistakes to Avoid

Even with the best intentions, car buyers often fall into common traps that can negatively impact their finances. Being aware of these pitfalls is just as important as knowing the right steps to take.

By proactively avoiding these mistakes, you can ensure a smoother, more financially sound car-buying experience. Learn from the experiences of others to protect your own interests.

- Not Checking Your Credit First: As discussed, this is a fundamental error. Going into the process blind leaves you vulnerable to unfavorable terms.

- Applying for Too Many Loans at Once: While shopping for rates is good, applying to dozens of lenders indiscriminately can trigger numerous hard inquiries, temporarily hurting your score. Stick to a focused window for rate shopping.

- Focusing Only on the Monthly Payment: This is a classic dealer tactic. A low monthly payment might seem attractive, but it could be due to an excessively long loan term or a hidden balloon payment, meaning you pay significantly more in interest over time.

- Ignoring the Total Cost of the Loan: Always calculate the total amount you will pay over the life of the loan (down payment + (monthly payment x loan term)). This reveals the true financial commitment.

- Impulse Buying: Rushing into a purchase without proper research, budget planning, or credit preparation often leads to buyer’s remorse and a less-than-ideal loan. Take your time, do your homework, and make a reasoned decision.

- Lying on Your Application: Never provide false information. This can lead to loan denial, legal repercussions, and severely damage your credit standing.

Conclusion

Navigating the world of "credit for car loan" can seem complex, but with the right knowledge and strategic approach, it becomes an empowering journey. Your credit score is more than just a number; it’s a reflection of your financial responsibility and a powerful tool that dictates the cost and accessibility of your auto financing. By understanding how lenders assess your credit, taking proactive steps to improve your financial standing, and employing smart shopping tactics, you can drive away with confidence, knowing you’ve secured the best possible deal.

Remember, preparation is your greatest asset. Know your credit, set your budget, shop around for lenders, and meticulously review every detail of your loan agreement. Armed with this comprehensive guide, you are now equipped to make informed decisions, avoid common pitfalls, and achieve your goal of car ownership on favorable terms. Happy driving!