Deal or No Deal: Mastering Car Loans – Unveiling Lesson 3 Answers for Smart Auto Financing

Deal or No Deal: Mastering Car Loans – Unveiling Lesson 3 Answers for Smart Auto Financing Carloan.Guidemechanic.com

Navigating the world of car loans can often feel like a high-stakes game of "Deal or No Deal." Every decision, from the interest rate to the loan term, carries significant financial implications. If you’ve been grappling with the complexities of auto financing, especially after tackling introductory lessons, you’re likely ready for a deeper dive. This comprehensive guide serves as your ultimate resource for Deal Or No Deal Understanding Car Loans Lesson 3 Answers, providing an in-depth exploration of the critical concepts you need to master to secure the best possible auto loan.

Based on my experience as an expert blogger and SEO content writer, the key to successful car financing isn’t just finding a car you love; it’s understanding the intricate mechanics of the loan itself. This article will transform you from a passive borrower into an empowered negotiator, equipped with the knowledge to identify a great deal and confidently walk away from a bad one. We’ll break down complex financial jargon into easy-to-understand explanations, ensuring you gain real value that translates into tangible savings.

Deal or No Deal: Mastering Car Loans – Unveiling Lesson 3 Answers for Smart Auto Financing

The Core Components of Your Car Loan: Unpacking the Deal

Before you even step foot into a dealership, understanding the fundamental elements of a car loan is paramount. These aren’t just numbers on a page; they are the bedrock of your financial commitment. Mastering these concepts is the first step in truly understanding car loans, much like acing the foundational questions in Deal Or No Deal Understanding Car Loans Lesson 3 Answers.

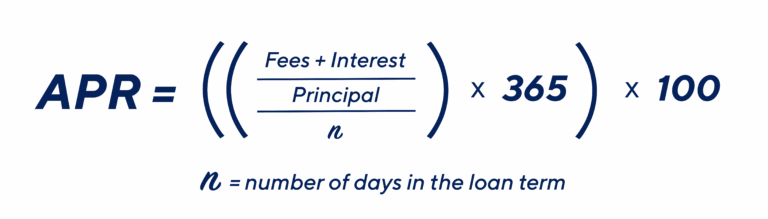

What is APR (Annual Percentage Rate) and Why Does It Matter So Much?

Many people mistakenly believe the interest rate is the only factor determining the cost of borrowing money. While crucial, the Annual Percentage Rate (APR) offers a more complete picture. APR is the true annual cost of your loan, expressed as a percentage, encompassing not just the interest rate but also certain fees charged by the lender. It represents the total cost of credit over the life of the loan.

A lower APR directly translates to less money you’ll pay in interest over the loan term. This is why comparing APRs from different lenders is one of the most critical steps in securing a car loan. Even a seemingly small difference in APR can save you hundreds, or even thousands, of dollars over several years. Don’t just look at the monthly payment; always scrutinize the APR.

Common mistakes to avoid are focusing solely on the quoted "interest rate" without confirming it’s the full APR. Lenders might sometimes highlight a lower interest rate while burying fees that push the true cost higher. Always ask for the APR to make an apples-to-apples comparison between loan offers.

Understanding Loan Term Length: Short vs. Long-Term Implications

The loan term, or the duration over which you agree to repay the loan, is another pivotal factor in your car financing journey. Car loan terms can range from 24 months to 84 months, or even longer. Your choice here significantly impacts both your monthly payment and the total amount of interest you’ll pay.

A shorter loan term, such as 36 or 48 months, typically comes with higher monthly payments. However, the trade-off is substantial: you’ll pay significantly less in total interest over the life of the loan. This is because the principal amount is paid off faster, reducing the time interest has to accrue. It’s often the financially savvy choice if your budget can accommodate the higher payments.

Conversely, a longer loan term, like 60 or 72 months, results in lower monthly payments, making the car seem more affordable upfront. The downside, however, is that you’ll end up paying much more in total interest over the extended period. You also risk owing more on the car than it’s worth (being "upside down" or "underwater") as it depreciates faster than you pay off the loan. Pro tips from us: always weigh the immediate affordability against the long-term cost.

Principal vs. Interest: The Real Cost Breakdown of Your Payments

Every car loan payment you make consists of two primary components: the principal and the interest. The principal is the actual amount of money you borrowed to purchase the car. The interest is the cost of borrowing that money, charged by the lender. Understanding how these two components are balanced within your payments is crucial.

During the initial months and even years of your car loan, a larger portion of your monthly payment goes towards paying off the interest. This is a common practice known as amortization. As the loan progresses, and the principal balance decreases, a progressively larger portion of your payment then goes towards reducing the principal. This structure means that early extra payments can have a disproportionately large impact on reducing your total interest paid.

Based on my experience, many borrowers are surprised to learn how much of their early payments are purely interest. This realization often prompts them to consider strategies like making larger down payments or even making extra payments when possible to accelerate their principal reduction. This knowledge is a key "answer" to truly understanding your car loan.

Decoding Your Monthly Payment and Total Cost: The Ultimate Negotiation

Beyond the fundamental components, understanding how your monthly payment is calculated and, more importantly, how to determine the true total cost of your loan, is where the "Deal or No Deal" decision truly crystallizes. This section provides the insights needed to confidently evaluate any loan offer.

Factors Influencing Your Monthly Payment: A Detailed Look

Your monthly car loan payment isn’t pulled out of thin air; it’s a direct result of several interconnected factors. Mastering these factors allows you to manipulate them in your favor during negotiations. The primary determinants include:

- Loan Amount (Principal): This is the actual price of the car minus any down payment or trade-in value. A higher loan amount naturally leads to a higher monthly payment.

- APR (Annual Percentage Rate): As discussed, a higher APR means more interest accrues, directly increasing your monthly payment.

- Loan Term: A shorter term means fewer payments to spread the principal and interest over, resulting in higher individual monthly payments. Conversely, a longer term lowers monthly payments but increases total interest.

- Down Payment: The amount of cash you pay upfront reduces the principal you need to borrow. A larger down payment immediately lowers your monthly payments and reduces the total interest paid over the life of the loan.

- Trade-in Value: If you trade in your old car, its value acts like a down payment, reducing the amount you need to finance.

Imagine you’re buying a car for $30,000. If you put $5,000 down, you’re financing $25,000. At a 5% APR over 60 months, your payment will be different than if you put $2,000 down and financed $28,000 at 6% over 72 months. Each variable has a ripple effect.

Beyond the Monthly Payment: Calculating the True Total Cost

This is perhaps the most critical "answer" in Deal Or No Deal Understanding Car Loans Lesson 3 Answers. Many buyers fall into the trap of only focusing on the monthly payment, often stretching the loan term to achieve a seemingly affordable number. However, this often hides the real financial burden: the total cost of the loan.

To truly understand the "deal," you must calculate the total amount you will pay for the car, including all interest and fees. The simple formula is:

Total Loan Cost = (Monthly Payment x Loan Term in Months) + Down Payment + Any Upfront Fees (e.g., documentation fees, taxes not financed)

Let’s illustrate. A $25,000 loan at 5% APR:

- 60-month term: Monthly payment ~ $471.79. Total paid = $471.79 x 60 = $28,307.40. Interest paid = $3,307.40.

- 72-month term: Monthly payment ~ $402.77. Total paid = $402.77 x 72 = $29,000.14. Interest paid = $4,000.14.

As you can see, extending the loan by 12 months adds nearly $700 in interest. This is your "Deal or No Deal" moment: are you willing to pay more for the convenience of lower monthly payments? Always perform this calculation before signing anything.

The Power of a Down Payment and Trade-in: Cutting Your Costs

A substantial down payment is one of the most effective tools you have to reduce the overall cost of your car loan. When you put more cash down upfront, you reduce the principal amount you need to borrow. This, in turn, decreases both your monthly payments and the total amount of interest you’ll pay over the loan term.

For example, on a $30,000 car, putting down $5,000 instead of $2,000 means you’re financing $25,000 instead of $28,000. This smaller loan amount immediately translates to lower interest accrual. Based on my experience, a down payment of at least 10-20% of the car’s purchase price is ideal. It helps you build equity faster and reduces your risk of being underwater on the loan.

Similarly, a trade-in works like a down payment. The value of your old car is deducted from the purchase price of the new car, reducing the amount you need to finance. Pro tips from us: always research your car’s trade-in value before heading to the dealership. Websites like Kelley Blue Book or Edmunds can give you a good estimate, empowering you to negotiate effectively.

Navigating the Car Loan Landscape: Making the Right Choice

The path to a great car loan isn’t always straightforward. There are multiple avenues to explore, each with its own advantages and pitfalls. Understanding these options and being aware of potential traps is vital for anyone seeking the answers to Deal Or No Deal Understanding Car Loans Lesson 3 Answers.

Pre-Approval vs. Dealership Financing: Your Strategic Advantage

One of the most powerful strategies in car buying is getting pre-approved for a loan before you even set foot in a dealership. This means applying for a loan with a bank, credit union, or online lender and getting an offer for a specific loan amount at a particular APR, subject to the final vehicle purchase.

- Benefits of Pre-Approval:

- Shopping Power: You know exactly how much you can afford, empowering you to negotiate on the car’s price, not the monthly payment.

- Comparison Tool: You have a benchmark loan offer to compare against any financing options the dealership presents. If the dealership can beat your pre-approved rate, great! If not, you have a solid "deal" to fall back on.

- Focus on Price: With financing secured, you can focus solely on negotiating the car’s purchase price.

Dealership financing, on the other hand, involves applying for a loan directly through the dealership. They act as an intermediary, working with various banks and financial institutions to find you a loan. While convenient, it can sometimes be less transparent. Dealerships might mark up the interest rate they receive from their lenders, keeping the difference as profit.

Common mistakes to avoid are letting the dealership control the financing conversation entirely. Always come prepared with your own pre-approval. This puts you in the driver’s seat and ensures you’re getting a competitive rate.

Beware of Hidden Fees and Add-ons: Scrutinizing the Fine Print

When you’re ready to sign the paperwork, it’s crucial to be vigilant about potential hidden fees and add-ons. Dealerships often present these at the end of the buying process, when you’re excited and eager to finalize the deal. These can significantly inflate the total cost of your car.

- Documentation Fees (Doc Fees): These are administrative fees charged by the dealership for preparing the paperwork. While legitimate to an extent, they can vary widely and are often negotiable.

- Extended Warranties/Service Contracts: These offer coverage beyond the manufacturer’s warranty. While some can provide peace of mind, they are often expensive and may duplicate existing coverage. Research their value carefully.

- GAP Insurance (Guaranteed Asset Protection): This covers the "gap" between what you owe on your loan and what your insurance company will pay if your car is totaled or stolen. It can be valuable, especially if you have a small down payment or a long loan term. However, you can often get it cheaper from your own insurance provider or a third-party.

- Undercoating, Paint Protection, VIN Etching: These are often high-profit, low-value add-ons. Most modern cars already have excellent rust protection and durable paint finishes.

Pro tips from us: Always review the final purchase agreement line by line. Question every charge you don’t understand or didn’t explicitly agree to. Don’t be pressured into accepting add-ons you don’t need or want. Remember, you have the right to decline them.

When to Consider Refinancing Your Car Loan: A Second Chance at a Better Deal

Even after you’ve secured a car loan, your financial journey isn’t necessarily set in stone. Refinancing your car loan involves taking out a new loan to pay off your existing one, typically with more favorable terms. This can be a smart move in several situations:

- Lower Interest Rates: If market interest rates have dropped since you took out your original loan, you might qualify for a significantly lower APR, saving you money on interest.

- Improved Credit Score: If your credit score has improved considerably since your initial purchase, you’re likely eligible for better rates now.

- Change in Financial Situation: If you need to lower your monthly payments (e.g., due to a job change), refinancing to a longer term could help, though it will increase total interest. Conversely, if you have extra cash, refinancing to a shorter term can save you substantial interest.

- Removing a Co-signer: If your credit has improved, you might be able to refinance and remove a co-signer from the loan.

Refinancing can be an excellent way to reduce your financial burden or adjust your loan to better fit your current circumstances. It’s an important "answer" to consider even after the initial deal is done. offers more insights into how interest rates fluctuate and how they impact refinancing opportunities.

Your "Deal or No Deal" Car Loan Strategy: Applying the Answers

Armed with the comprehensive knowledge from this deep dive into Deal Or No Deal Understanding Car Loans Lesson 3 Answers, you are now ready to formulate your winning strategy. This final section consolidates the advice into actionable steps and highlights common pitfalls to avoid, ensuring you make an informed decision every time.

Building Your Car Loan Checklist: Your Roadmap to Success

Approaching car financing with a structured plan is your best defense against high costs and unwanted surprises. Use this checklist to guide your journey:

- Check Your Credit Score: Know where you stand. A higher score typically means a lower APR. Get a free report from AnnualCreditReport.com. provides excellent resources on credit and car buying.

- Set a Realistic Budget: Determine how much you can comfortably afford for a monthly payment and the total cost. Don’t forget insurance, maintenance, and fuel costs.

- Get Pre-Approved: Apply to several banks, credit unions, and online lenders to compare APRs and get a solid offer before visiting dealerships.

- Research Car Values: Understand the market value of the car you want to buy and your trade-in (if applicable).

- Negotiate the Car Price First: Agree on the vehicle’s price before discussing financing. This prevents "payment packing."

- Scrutinize the Loan Offer: Compare the dealership’s financing offer against your pre-approval. Pay close attention to the APR, loan term, and total cost.

- Read All Documents Carefully: Before signing, ensure every detail, especially any fees or add-ons, is understood and agreed upon.

This checklist is your game plan, ensuring you cover all bases and make a well-informed decision. provides a detailed breakdown of how your credit score impacts your loan eligibility and rates.

Common Mistakes to Avoid When Securing a Car Loan

Even experienced buyers can fall prey to common missteps. Being aware of these will help you avoid costly errors:

- Focusing Only on Monthly Payments: This is the biggest trap. A low monthly payment often comes with a much longer term and significantly higher total interest. Always ask for the total cost.

- Not Shopping Around for Loans: Accepting the first loan offer, especially from a dealership, can mean missing out on better rates from other lenders. Comparison shopping is vital.

- Ignoring the Total Cost of the Loan: As discussed, the true measure of a deal is the total amount you’ll pay over the loan’s life, not just the monthly installment.

- Impulse Buying: Rushing into a purchase without proper research and financial preparation often leads to buyer’s remorse and a bad loan deal.

- Not Reading the Fine Print: Every document you sign has legal implications. Take your time, understand everything, and ask questions. Don’t be rushed.

- Disclosing Your Ideal Monthly Payment Too Early: Dealers often use this information to structure a deal that hits your target payment but might inflate the total cost with a longer term or higher price. Keep your financing discussions separate from the car price.

Pro Tips for a Successful Car Loan Journey

To truly win the "Deal or No Deal" game of car financing, integrate these expert tips into your strategy:

- Do Your Homework: The more informed you are about car values, loan terms, and interest rates, the stronger your negotiating position.

- Be Prepared to Walk Away: This is your ultimate power. If a deal doesn’t feel right, or if the numbers don’t add up, don’t be afraid to leave. There will always be another car and another loan.

- Don’t Be Afraid to Ask Questions: If anything is unclear, demand clarification. A reputable lender or dealer will be transparent.

- Seek Clarity on Every Line Item: Before signing, ensure every fee, charge, and term is explained to your satisfaction.

- Consider a Short Test Drive: While not directly loan-related, ensuring the car is truly what you want helps prevent regret and potential early trade-ins, which can complicate loan situations.

Conclusion: Empowering Your Car Loan Decisions with Lesson 3 Answers

The journey to understanding car loans, much like mastering Deal Or No Deal Understanding Car Loans Lesson 3 Answers, is about empowering yourself with knowledge. By thoroughly grasping concepts like APR, loan terms, principal vs. interest, and the true total cost of a loan, you transform from a vulnerable consumer into a savvy negotiator. You learn to dissect offers, identify hidden costs, and confidently make financial decisions that benefit your wallet.

Remember, every car loan decision is a unique "Deal or No Deal" scenario. With the insights and strategies provided in this comprehensive guide, you are now equipped to open the right briefcases, avoid the pitfalls, and ultimately secure an auto financing deal that brings you satisfaction and financial peace of mind. Drive away confident, knowing you’ve made the smartest possible choice for your next vehicle.