Decent Credit Score For Car Loan: Your Ultimate Guide to Driving Away with the Best Deal

Decent Credit Score For Car Loan: Your Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

The thrill of a new car is undeniable. Imagining yourself behind the wheel, cruising down the open road, can be incredibly exciting. However, before you even step onto a dealership lot, there’s a crucial financial factor that dictates whether that dream becomes a reality, and at what cost: your credit score.

Navigating the world of car loans can feel overwhelming, especially when terms like "APRs," "credit tiers," and "debt-to-income ratios" start flying around. Many prospective buyers wonder, "What exactly is a decent credit score for a car loan?" This isn’t just a simple number; it’s a gateway to better interest rates, more favorable terms, and ultimately, significant savings over the life of your vehicle.

Decent Credit Score For Car Loan: Your Ultimate Guide to Driving Away with the Best Deal

This comprehensive guide is designed to demystify the credit score requirements for auto financing. We’ll dive deep into what lenders consider "decent," explore how your score impacts your loan, and provide actionable strategies to improve your financial standing. Our goal is to empower you with the knowledge needed to secure the best possible car loan, ensuring you drive away happy and financially smart.

What is a Credit Score and Why Does it Matter for Car Loans?

Before we define what makes a credit score "decent," let’s understand its fundamental role. A credit score is a three-digit number, typically ranging from 300 to 850, that represents your creditworthiness. It’s a snapshot of your financial history, indicating how reliably you manage debt. Lenders use this score to assess the risk of lending money to you.

For car loans specifically, your credit score is arguably the most significant factor in a lender’s decision-making process. It tells them how likely you are to repay the loan on time and in full. A higher score signals lower risk, making you a more attractive borrower. Conversely, a lower score suggests a higher risk of default, which can lead to higher interest rates or even loan denial.

Based on my experience in the financial industry, understanding this basic principle is step one. Many people underestimate how profoundly this single number affects their monthly car payments and the total cost of their vehicle. It’s not just about approval; it’s about getting the best approval.

Defining "Decent": What’s a Good Credit Score for a Car Loan?

The term "decent" is subjective, but in the realm of auto financing, we can define it by what lenders typically consider favorable. While there isn’t one universal cutoff, credit scores are generally categorized into tiers that dictate the types of loan offers you’ll receive. These tiers are largely consistent across different lenders and credit bureaus.

Let’s break down the common credit score ranges and what they mean for your car loan prospects:

-

Exceptional/Excellent Credit (780-850):

- This is the top tier, representing borrowers with an impeccable financial history. If your score falls into this range, you are considered a low-risk borrower. Lenders will compete for your business, offering the absolute best interest rates available, often significantly below the national average.

- You’ll likely qualify for the most flexible terms, potentially requiring lower down payments or having longer repayment periods at attractive rates. Securing pre-approval is often straightforward, giving you strong negotiating power at the dealership.

- Pro tips from us: With excellent credit, always shop around for the best rates from multiple lenders, including banks, credit unions, and online lenders. Don’t settle for the first offer.

-

Very Good Credit (740-779):

- Borrowers in this range also enjoy highly favorable terms. You are still seen as a very reliable borrower, though perhaps not with the absolute perfect credit history of the "Exceptional" tier. Interest rates will be very competitive, often just a hair above the absolute lowest rates.

- Approval for a car loan will be virtually guaranteed, and you’ll have access to a wide range of financing options. You might still qualify for manufacturer special financing offers, which often require top-tier credit.

- A score in this range is definitely considered a decent credit score for car loan approval and excellent terms.

-

Good Credit (670-739):

- This is where the majority of consumers fall, and it’s a solid range for securing a car loan. With a "Good" credit score, you are still considered a responsible borrower. You can expect to be approved for a car loan with reasonable interest rates, though they might be slightly higher than those offered to borrowers in the "Very Good" or "Excellent" tiers.

- Lenders will still be willing to work with you, and you’ll have decent options for loan terms. While you might not get the absolute lowest rates, you’ll avoid the high-interest rates associated with lower scores. This is often the minimum many lenders consider "decent."

- Common mistakes to avoid are: Not comparing offers, assuming you’ll get the absolute best rate. Always get multiple quotes even with good credit.

-

Fair Credit (580-669):

- Borrowers in the "Fair" range will find it more challenging to secure highly favorable terms. Lenders perceive a moderate risk, which translates to higher interest rates. While approval is still possible, your monthly payments will be significantly higher than someone with good or excellent credit.

- You might also be required to make a larger down payment or accept shorter loan terms to mitigate the lender’s risk. Special financing offers are generally out of reach. This range borders on what some might consider "not quite decent," but loans are still accessible.

- For those with fair credit, securing a loan from a credit union might offer slightly better rates than traditional banks, as credit unions are often more community-focused.

-

Poor Credit (300-579):

- If your credit score falls into this category, securing a traditional car loan will be difficult and expensive. Lenders view you as a high-risk borrower. Interest rates will be very high, often in the double digits, leading to significantly inflated overall costs for the vehicle.

- You may face challenges getting approved at all, or might be limited to subprime lenders who specialize in high-risk loans. A substantial down payment will almost certainly be required.

- While technically possible to get a loan, it’s crucial to weigh the long-term financial implications. Sometimes, improving your credit first or saving for a larger down payment is a wiser strategy.

The Impact of Your Credit Score on Loan Terms

Your credit score doesn’t just determine if you get approved; it directly influences every aspect of your car loan. Understanding these impacts can motivate you to improve your score.

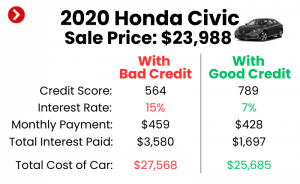

- Interest Rates: This is the most significant factor. A higher credit score translates to a lower interest rate. Even a difference of a few percentage points can save you thousands of dollars over the life of a loan. For instance, on a $30,000 loan over five years, a 3% interest rate compared to a 7% interest rate could mean saving over $4,000 in total interest paid.

- Monthly Payments: Lower interest rates naturally lead to lower monthly payments. This improves your cash flow and makes the car more affordable within your budget. It also reduces the stress of making large payments each month.

- Loan Amount and Term Flexibility: Lenders are more willing to lend larger sums and offer longer repayment terms (e.g., 72 or 84 months) to borrowers with excellent credit. This flexibility allows you to choose a payment plan that truly fits your financial situation without incurring exorbitant interest.

- Down Payment Requirements: While a down payment is always a good idea, borrowers with high credit scores might be able to get approved with a smaller or even no down payment. Those with lower scores, however, will almost certainly be required to put down a significant amount to reduce the lender’s risk.

- Approval Chances: This is straightforward: a decent credit score significantly increases your likelihood of loan approval. With a strong score, you can walk into a dealership or apply online with confidence, knowing that financing is within reach.

Beyond the Score: Other Factors Lenders Consider

While your credit score is paramount, it’s not the only piece of the puzzle. Lenders conduct a holistic review of your financial situation. Ignoring these other factors can derail even a borrower with a good credit score.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. A low DTI indicates you have enough income to comfortably manage additional debt. Lenders prefer a DTI below 40%, with under 30% being ideal.

- Income Stability and Employment History: Lenders want to see a steady source of income. A long, consistent employment history with the same employer or within the same industry signals reliability. Recent job changes or gaps in employment might raise red flags.

- Down Payment Amount: A larger down payment reduces the loan amount, thereby lowering the lender’s risk. It also demonstrates your financial commitment and ability to save. Putting down 20% or more is often recommended to avoid being "upside down" on your loan.

- Loan-to-Value (LTV) Ratio: This compares the loan amount to the car’s actual market value. If you’re borrowing more than the car is worth (e.g., rolling negative equity from a trade-in), it increases the LTV and makes the loan riskier for the lender. A lower LTV is always preferable.

- Payment History: Even if your credit score is decent, a recent history of missed payments on other loans or credit cards will be scrutinized. Lenders look at current financial behavior as a strong indicator of future behavior.

How to Find Out Your Credit Score (and Report)

You can’t improve what you don’t know. The first step towards securing a great car loan is understanding your current credit standing. You have the right to access your credit information.

- AnnualCreditReport.com: This is the only federally authorized website for consumers to obtain a free copy of their credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. While it doesn’t directly provide your score, it offers the detailed information lenders use to calculate it. Reviewing these reports for errors is critical.

- Credit Card Issuers & Banks: Many credit card companies and banks now offer free credit scores (often FICO Score or VantageScore) as a perk to their customers. Check your online banking portal or monthly statements.

- Free Credit Score Services: Websites like Credit Karma (VantageScore), Experian, or myFICO provide free access to your credit score and sometimes elements of your credit report. These can be valuable tools for monitoring your progress.

- Auto Lenders: When you apply for pre-approval, the lender will pull your credit report and score. This is a "hard inquiry" which can temporarily ding your score, but multiple inquiries within a short period (typically 14-45 days, depending on the scoring model) for the same type of loan are usually treated as a single inquiry.

Based on my experience, regularly checking your credit report for inaccuracies is crucial. One error could unfairly lower your score and cost you money on a car loan. If you find errors, dispute them immediately with the credit bureau.

Strategies to Improve Your Credit Score Before Applying

If your credit score isn’t quite where you want it to be for a "decent credit score for car loan" approval, don’t despair. There are actionable steps you can take to boost it.

-

Pay Your Bills On Time, Every Time:

- Payment history is the single most important factor in your credit score, accounting for about 35% of your FICO score. Late payments can severely damage your credit. Set up automatic payments or calendar reminders for all your debts, including credit cards, utilities, and existing loan payments.

- Consistency is key here. A long history of on-time payments demonstrates reliability to lenders and gradually builds your score.

-

Reduce Your Credit Utilization Ratio:

- This ratio measures how much of your available credit you are using. For example, if you have a credit card with a $10,000 limit and a $3,000 balance, your utilization is 30%. Lenders prefer to see this ratio below 30%, with lower being better. High utilization suggests you might be over-reliant on credit.

- Focus on paying down credit card balances. If you can, pay them off in full each month. Even paying down a significant portion can make a noticeable difference in your score.

-

Address Derogatory Marks:

- Collections, charge-offs, bankruptcies, or foreclosures significantly hurt your score. While these take time to fall off your report (usually 7-10 years), you can mitigate their impact. If there are outstanding collections, consider negotiating a "pay for delete" agreement with the collection agency, though this is not guaranteed.

- Ensure any negative marks on your report are accurate. If not, dispute them with the credit bureaus.

-

Avoid Opening New Credit Accounts (Unless Necessary):

- Each new credit application results in a "hard inquiry" on your credit report, which can temporarily lower your score by a few points. While applying for a car loan is necessary, avoid opening new credit cards or other loans in the months leading up to your car purchase.

- A longer average age of accounts generally looks better to lenders, so resist the urge to close old, unused accounts, especially if they have a long positive history.

-

Build a Diverse Credit Mix:

- Having a mix of credit types (e.g., credit cards, installment loans like student loans or mortgages) can positively impact your score. It shows you can manage different kinds of debt responsibly. However, only take on new debt if you genuinely need it and can afford it.

- For those with very limited credit history, a secured credit card or a small credit-builder loan can be a good starting point.

These strategies require patience, but the financial benefits of a better credit score for your car loan are well worth the effort. For more in-depth advice on improving your credit, you might find our article on invaluable. (Internal Link 1: Placeholder for an article about credit building).

What If Your Credit Isn’t "Decent"? Navigating Car Loans with Less-Than-Perfect Credit

Even if your credit score falls into the "Fair" or "Poor" categories, getting a car loan isn’t impossible. It just requires a different strategy and realistic expectations.

- Consider a Larger Down Payment: This is often the most effective way to offset a low credit score. A substantial down payment reduces the loan amount and signals to lenders that you have skin in the game, making them more willing to take a chance on you.

- Find a Co-Signer: A co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. The co-signer essentially guarantees the loan, taking on equal responsibility for repayment. Choose a co-signer carefully, as their credit will be affected if you miss payments.

- Explore Dealership Financing (Carefully): Some dealerships have relationships with subprime lenders who specialize in loans for borrowers with lower credit scores. While this can provide an avenue for approval, these loans often come with very high interest rates. Read all terms and conditions meticulously.

- Credit Unions: As mentioned earlier, credit unions are non-profit organizations that often have more flexible lending criteria and potentially better rates for members, even those with less-than-perfect credit. It’s always worth checking with local credit unions.

- Buy Here, Pay Here Dealerships: These dealerships offer in-house financing, often without a traditional credit check. However, they typically charge extremely high interest rates and may have unfavorable terms. This should generally be a last resort.

- Wait and Improve Your Credit: Sometimes, the best option is to delay your car purchase. Use the time to implement the credit-building strategies discussed above. Even a few months of diligent effort can significantly boost your score and save you thousands in interest.

Pre-Approval: Your Secret Weapon

One of the smartest moves you can make before shopping for a car is to get pre-approved for a loan. This simple step can dramatically change your car-buying experience.

- Know Your Budget: Pre-approval tells you exactly how much you can afford to borrow, setting a clear budget before you fall in love with a car outside your price range.

- Shop as a Cash Buyer: With a pre-approval in hand, you walk into the dealership with your financing already secured. This puts you in a position of power, allowing you to focus on negotiating the car’s price rather than worrying about loan terms.

- Compare Offers: Getting pre-approved from your bank or credit union gives you a benchmark. You can then compare the dealer’s financing offers against your pre-approval, ensuring you get the best possible rate. If the dealer can beat your pre-approval, great! If not, you have a solid offer to fall back on.

- Streamlined Process: Pre-approval often speeds up the purchasing process at the dealership, as much of the paperwork for financing is already handled.

Based on my experience, many buyers skip this step and end up paying more. Don’t make that mistake! A pre-approval is a free, no-obligation way to empower yourself. For more insights on pre-approval, see this resource from the Consumer Financial Protection Bureau: Understanding Car Loan Pre-Approval. (External Link)

Common Mistakes to Avoid When Applying for a Car Loan

Even with a decent credit score, certain missteps can hinder your chances of securing the best deal.

- Not Checking Your Credit Report Beforehand: As discussed, errors can cost you. Always review your report for accuracy and dispute any discrepancies.

- Applying to Too Many Lenders at Once (Indiscriminately): While rate shopping is good, applying to dozens of lenders over a long period can result in multiple hard inquiries that negatively impact your score. Focus your applications within a concentrated period (e.g., 14-45 days) to minimize impact.

- Focusing Only on the Monthly Payment: Dealers often try to "sell the payment." While important, a low monthly payment achieved by extending the loan term excessively can mean paying much more in interest over time. Always consider the total cost of the loan.

- Rolling Negative Equity into a New Loan: If you owe more on your trade-in than it’s worth, don’t just roll that negative equity into your new car loan. This increases your new loan amount, raises your monthly payments, and puts you "underwater" on your new vehicle from day one. Try to pay off negative equity separately.

- Skipping the Down Payment: Even with great credit, a down payment is beneficial. It reduces your loan amount, lowers monthly payments, and reduces the risk of being upside down on the loan.

- Not Understanding All the Loan Terms: Read the fine print! Understand the interest rate, APR, loan term, any prepayment penalties, and late fees. Don’t be afraid to ask questions until everything is clear.

Pro Tips for Securing the Best Car Loan

As an expert in this field, I’ve seen countless car loan scenarios. Here are some pro tips to help you maximize your chances of getting an excellent deal:

- Shop for the Loan First, Not Just the Car: This cannot be stressed enough. Get pre-approved from several lenders (banks, credit unions, online lenders) before you start test-driving cars. This empowers you with leverage.

- Negotiate the Car Price Separately from Financing: Always agree on the vehicle’s purchase price first. Once that’s settled, then discuss financing options. Mixing the two gives the dealer more room to manipulate figures.

- Consider a Shorter Loan Term if Affordable: While longer terms mean lower monthly payments, they also mean more interest paid. If your budget allows, opt for a 36 or 48-month loan instead of 60 or 72 months to save significant money.

- Know Your Trade-In Value: Use online resources like Kelley Blue Book or Edmunds to get an accurate estimate of your current car’s trade-in value. This prevents you from being lowballed at the dealership.

- Don’t Be Afraid to Walk Away: If the numbers don’t feel right, or if the dealer is pressuring you, be prepared to leave. There are always other cars and other dealerships. Patience is a virtue in car buying.

- Understand Dealer Add-Ons: Be wary of extra fees and add-ons like extended warranties, paint protection, or VIN etching that are often pushed at the financing stage. While some might be useful, many are overpriced and negotiable. Only pay for what you truly need.

- Explore Refinancing Options: If you get a loan with a higher interest rate due to less-than-ideal credit, you can always work on improving your credit score and then refinance your car loan later. This could save you a lot of money down the road. You can learn more about this in our article: . (Internal Link 2: Placeholder for an article about auto loan refinancing).

Conclusion: Drive Away Confident

Securing a car loan is a significant financial decision, and your credit score plays a pivotal role in the entire process. A "decent credit score for car loan" approval isn’t just about getting the keys; it’s about unlocking the most favorable terms, saving money on interest, and ensuring your car purchase is a financially sound one.

By understanding what lenders look for, actively working to improve your credit, and adopting smart car-buying strategies, you empower yourself. Remember to check your credit reports, get pre-approved, compare offers, and never settle for a deal that doesn’t feel right. With this knowledge, you’re well-equipped to navigate the auto loan landscape and drive away with the best possible deal for your dream ride. Happy driving!