Decoding "Auto Car Loans Near Me": Your Ultimate Guide to Finding the Best Vehicle Financing

Decoding "Auto Car Loans Near Me": Your Ultimate Guide to Finding the Best Vehicle Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. Whether it’s the thrill of a brand-new car or the practicality of a reliable pre-owned model, one crucial step often stands between you and your dream ride: securing the right auto car loan. The phrase "auto car loans near me" isn’t just a search query; it’s a reflection of your desire for local, convenient, and tailored financing solutions.

This comprehensive guide is designed to be your definitive resource, navigating the complex world of vehicle financing with clarity and expertise. We’ll demystify everything from understanding interest rates to finding local lenders, ensuring you make an informed decision that aligns with your financial goals. Our goal is to empower you with the knowledge needed to confidently secure an excellent auto loan, setting you up for a smooth ownership experience.

Decoding "Auto Car Loans Near Me": Your Ultimate Guide to Finding the Best Vehicle Financing

Understanding the Landscape of Auto Car Loans

Before diving into the "near me" aspect, it’s essential to grasp the fundamentals of auto car loans. Essentially, an auto loan is a secured loan specifically designed to help you finance the purchase of a vehicle. The car itself serves as collateral, meaning the lender can repossess it if you fail to make your payments.

This structure allows lenders to offer more favorable terms compared to unsecured loans, as their risk is reduced. Your ability to secure a good auto loan, with competitive interest rates and manageable terms, largely depends on several key factors, which we will explore in depth. Understanding these basics is the first step towards finding the best "auto car loans near me."

Key Components of an Auto Loan

Every auto loan, regardless of where you get it, consists of several core elements that directly impact your monthly payments and the total cost of the loan. Knowing these components will help you compare offers effectively.

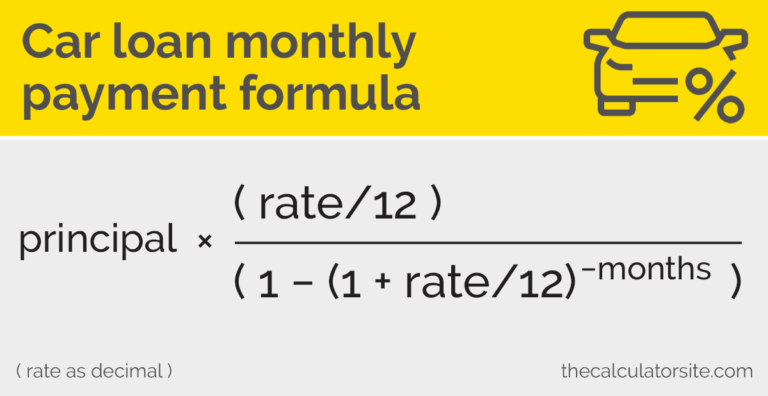

- Principal: This is the actual amount of money you borrow to purchase the car. It’s the sticker price of the vehicle minus any down payment or trade-in value. A lower principal means less interest paid over the life of the loan.

- Interest Rate: This is the cost of borrowing money, expressed as a percentage of the principal. It’s the most significant factor determining how much extra you’ll pay beyond the car’s price. A lower interest rate translates to lower monthly payments and less total interest paid.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term generally means lower monthly payments but results in paying more interest over time. Conversely, a shorter term has higher monthly payments but saves you money on interest.

- Monthly Payment: This is the fixed amount you pay back to the lender each month. It includes a portion of the principal and the interest accrued. Your monthly payment is directly influenced by the principal, interest rate, and loan term.

Based on my experience, many first-time car buyers focus solely on the monthly payment without fully understanding how the interest rate and loan term contribute to the total cost. Always look at the big picture to avoid paying significantly more than necessary.

The Journey to Your Ideal Auto Loan: A Step-by-Step Guide

Finding the perfect auto loan isn’t about stumbling upon a good deal; it’s a strategic process. By following these steps, you’ll be well-equipped to secure the best "auto car loans near me" that fit your financial situation.

Step 1: Assess Your Financial Health – The Foundation

Before you even start looking at cars, you need to understand your own financial standing. This foundational step is critical for determining what you can truly afford and for improving your chances of approval for favorable loan terms.

Your Credit Score: The Ultimate Indicator

Your credit score is arguably the most crucial factor lenders consider. It’s a three-digit number that represents your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score indicates lower risk to lenders, leading to better interest rates and terms.

FICO scores and VantageScores are the two most common types, ranging from 300 to 850. Generally, scores above 700 are considered good, while those above 750 are excellent. Knowing your score allows you to anticipate what kind of rates you might qualify for.

Pro tips from us: Check your credit report from all three major bureaus (Experian, Equifax, TransUnion) at AnnualCreditReport.com at least once a year. This is free and won’t impact your score. Look for any errors that could be dragging your score down and dispute them immediately.

Budgeting for Affordability: Beyond the Monthly Payment

It’s easy to get excited about a car and only think about the monthly payment. However, a smart budget considers the total cost of ownership. This includes not just the loan payment, but also insurance, fuel, maintenance, and potential registration fees.

Your debt-to-income (DTI) ratio is another vital metric. This is the percentage of your gross monthly income that goes towards debt payments. Lenders typically prefer a DTI ratio below 36%, though some auto lenders might accept higher for strong credit profiles. A high DTI can signal to lenders that you might be overextended.

Common mistakes to avoid are: falling in love with a car that’s outside your comfortable budget. Always prioritize affordability over aspiration. A car is a depreciating asset, and financial strain can quickly turn a dream into a nightmare.

The Power of a Down Payment

Making a down payment significantly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. It also shows lenders that you’re committed to the purchase, potentially improving your loan approval odds and securing a better interest rate.

While a 20% down payment is often recommended for new cars to avoid being "upside down" (owing more than the car is worth) early on, even a smaller down payment can make a difference. For used cars, a down payment is equally beneficial.

Step 2: Know Your Car – New vs. Used

The type of car you intend to purchase has a direct impact on the available auto car loans and their terms. Lenders view new and used vehicles differently due to factors like depreciation and reliability.

- New Car Loans: These often come with lower interest rates and longer loan terms, especially from manufacturer-backed financing. However, new cars depreciate rapidly, meaning you could owe more than the car is worth in the first few years.

- Used Car Loans: While typically having slightly higher interest rates than new car loans, used cars are generally more affordable upfront and depreciate slower. The age and mileage of the used car can influence the loan terms, with older models sometimes having shorter maximum loan terms.

Consider your needs, budget, and how long you plan to keep the vehicle. This will guide you towards the most appropriate financing options.

Step 3: Pre-Approval – Your Secret Weapon

One of the most powerful steps you can take is to get pre-approved for an auto loan before you step foot into a dealership. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate, pending a final vehicle selection.

Benefits of Pre-Approval:

- Negotiating Power: You become a cash buyer in the eyes of the dealership, allowing you to focus solely on the car’s price without the pressure of financing.

- Realistic Budget: You know exactly how much you can afford, preventing you from overspending or falling in love with a car outside your price range.

- Peace of Mind: The stress of financing is largely removed, making the car-buying experience much more enjoyable.

- Comparison Tool: You can use your pre-approved offer as a benchmark to compare against any financing offered by the dealership.

Where to Get Pre-Approved:

You can seek pre-approval from various sources, including your current bank, local credit unions, and online lenders. Applying to several lenders within a short window (typically 14-45 days, depending on the credit scoring model) will usually count as a single hard inquiry on your credit report, so don’t be afraid to shop around.

Step 4: Exploring "Auto Car Loans Near Me" – Your Local Options

The "near me" aspect of your search is crucial for finding personalized service and competitive rates. Local lenders often have a better understanding of the community and may offer more flexible options. Let’s explore your primary avenues for auto car loans.

Banks: The Traditional Route

Major banks and local community banks are common sources for auto loans. They typically offer competitive rates for borrowers with good to excellent credit. Their extensive branch networks mean you can often discuss your options in person.

- Pros: Established reputation, wide range of products, convenient branch access.

- Cons: Stricter eligibility requirements, less flexibility for those with lower credit scores.

Credit Unions: Member-Focused Financing

Credit unions are non-profit financial institutions owned by their members. They are renowned for offering some of the most competitive interest rates on auto loans, often beating traditional banks. Their focus on member service means a more personalized approach.

- Pros: Lower interest rates, flexible terms, personalized service, often more forgiving for those with fair credit.

- Cons: Membership requirements (though often easy to meet), fewer branches than large banks.

- For a deeper dive into the advantages of credit unions, you might find our article on "Benefits of Credit Union Car Loans" particularly insightful. (Internal Link 1)

Dealership Financing: Convenience at a Cost?

Dealerships often act as intermediaries, connecting you with a network of lenders. This "one-stop shop" convenience can be appealing, allowing you to complete your purchase and financing in one place. They may also offer special manufacturer incentives or low APR deals.

- Pros: Convenience, potential for special promotions, can often find a lender for various credit profiles.

- Cons: May not always offer the best rates unless you negotiate, potential for hidden fees or pressure to accept less favorable terms.

Common mistake to avoid: accepting the first financing offer from a dealership without comparing it to your pre-approved loan or other independent offers. Always compare the APR, not just the monthly payment.

Online Lenders: Speed and Variety

The digital age has brought a surge of online lenders specializing in auto loans. These platforms offer convenience, quick approvals, and a wide array of options, often allowing you to compare multiple offers from various lenders simultaneously.

- Pros: Fast application process, ability to compare many offers quickly, accessible from anywhere.

- Cons: Less personalized service, may require more self-research to understand terms fully.

Pro Tip: Don’t limit yourself to just one type of lender. Cast a wide net to ensure you find the absolute best "auto car loans near me" or online that fits your specific needs.

Step 5: Comparing Loan Offers – Beyond the Interest Rate

Once you have a few loan offers, it’s time to compare them meticulously. The interest rate is crucial, but it’s not the only factor.

- Annual Percentage Rate (APR) vs. Interest Rate: The interest rate is simply the cost of borrowing. The APR, however, includes the interest rate plus any additional fees associated with the loan (like origination fees). The APR provides a more accurate representation of the true annual cost of your loan. Always compare APRs.

- Loan Term: As discussed, a shorter term means higher monthly payments but less total interest. A longer term means lower monthly payments but more total interest. Choose a term that balances affordability with the total cost.

- Fees and Penalties: Check for any hidden fees, such as application fees, origination fees, or prepayment penalties (though rare with auto loans, always verify). A prepayment penalty means you’ll pay a fee if you pay off your loan early.

- Flexibility and Customer Service: Consider the lender’s reputation for customer service and their flexibility should you encounter financial difficulties. Read reviews and look for transparency.

Step 6: The Application Process & What to Expect

Once you’ve chosen a lender and an offer, the application process is relatively straightforward. You’ll typically need to provide several documents.

- Documents Needed: Proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and potentially proof of insurance.

- Underwriting Process: The lender will verify your information, pull your credit report (a hard inquiry), and assess the vehicle you intend to purchase. This process can take anywhere from a few hours to a few days.

- Closing the Deal: Once approved, you’ll sign the loan agreement, which legally binds you to the terms. Read every single line carefully before signing.

Common mistakes to avoid are: rushing through the paperwork, not asking questions about anything you don’t understand, or feeling pressured to sign without full comprehension.

Special Considerations for Auto Car Loans

Certain situations require a more nuanced approach to auto car loans. Understanding these specific scenarios can save you time and money.

Bad Credit Car Loans Near Me: It’s Possible!

Having a less-than-perfect credit score doesn’t mean you can’t get an auto loan. While you might face higher interest rates, there are still options available, especially from lenders specializing in subprime auto loans.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and secure better terms. They are equally responsible for the loan, so choose someone you trust and who understands the commitment.

- Larger Down Payment: A substantial down payment reduces the lender’s risk, making them more willing to approve your loan despite a lower credit score.

- Subprime Lenders: Some lenders specifically cater to individuals with bad credit. While their rates will be higher, they can provide an opportunity to finance a vehicle and rebuild your credit through consistent, on-time payments.

- Focus on Improvement: In the long term, focus on improving your credit score. Pay all bills on time, reduce existing debt, and keep old credit accounts open.

Pro Tip: Be wary of predatory lenders offering "guaranteed approval" with extremely high interest rates and unfavorable terms. Always compare offers and read reviews.

Refinancing Your Auto Loan: A Smart Move

If your financial situation has improved since you first took out your auto loan – perhaps your credit score has increased, or interest rates have dropped – refinancing could be a smart move. Refinancing involves taking out a new loan to pay off your existing auto loan.

- When to Consider It:

- Your credit score has improved.

- Market interest rates have decreased.

- You want to lower your monthly payments by extending the loan term (though this increases total interest).

- You want to shorten your loan term to save on interest (which will increase monthly payments).

- How It Works: You apply for a new auto loan, much like your original one. If approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new terms.

- For a detailed walkthrough, explore our "Guide to Refinancing Your Car Loan" on our blog. (Internal Link 2)

Understanding Auto Loan Interest Rates

Interest rates are not arbitrary; they are influenced by several factors. Knowing these can help you understand why one person gets a different rate than another.

- Credit Score: The most significant factor. Higher scores mean lower rates.

- Loan Term: Shorter terms generally have lower rates, as the lender’s risk is for a shorter period.

- Economic Conditions: Overall interest rates set by central banks (like the Federal Reserve) influence auto loan rates across the board.

- Vehicle Type: New cars often have slightly lower rates than used cars. The specific make, model, and even the vehicle’s age can also play a role.

- Lender Competition: A competitive market among lenders can drive rates down.

Most auto loans come with fixed interest rates, meaning your rate and monthly payment remain the same throughout the loan term. This provides predictability and stability.

Maximizing Your Chances of Auto Loan Approval

Beyond understanding the mechanics, there are proactive steps you can take to bolster your application and secure the best possible "auto car loans near me."

- Improve Your Credit Score: This cannot be stressed enough. Pay bills on time, keep credit utilization low, and address any errors on your credit report. A higher score unlocks better rates.

- Save for a Larger Down Payment: A significant down payment reduces the loan amount and the lender’s risk, making your application more attractive.

- Reduce Existing Debt: A lower debt-to-income ratio signals to lenders that you have more disposable income to comfortably manage new loan payments.

- Maintain Stable Employment History: Lenders prefer borrowers with a consistent work history, as it demonstrates a reliable source of income.

- Get Pre-Approved: As discussed, pre-approval not only gives you negotiating power but also shows the dealership you are a serious and qualified buyer.

The "Near Me" Advantage: Why Local Matters

In an increasingly digital world, the value of "near me" for auto car loans remains incredibly high. While online lenders offer convenience, local options provide unique benefits.

- Personalized Service: Building a relationship with a local bank or credit union often means you get more personalized advice and attention. They may be more willing to work with you if your financial situation is unique or if you encounter issues during the loan term.

- Community Ties: Local institutions are often more invested in the community’s well-being. They might offer special programs or have a deeper understanding of local economic factors.

- In-Person Consultations: For many, the ability to sit down with a loan officer, ask questions face-to-face, and get immediate answers is invaluable. This can build trust and clarify complex terms more effectively than an online chat.

- Understanding Local Market Conditions: Local lenders are often more attuned to the specific car market in your area, which can sometimes translate into more relevant advice or offers.

Essential Tools and Resources for Your Car Loan Journey

To further empower your search for "auto car loans near me," leverage these valuable tools and resources.

- Car Loan Calculators: These online tools allow you to input various scenarios (loan amount, interest rate, term) to estimate your monthly payments and total interest paid. They are excellent for budgeting and comparing offers.

- Credit Reporting Agencies: Regularly check your credit reports from Experian, Equifax, and TransUnion via AnnualCreditReport.com.

- Consumer Financial Protection Bureau (CFPB): The CFPB offers a wealth of unbiased information on financial products, including auto loans. Their resources can help you understand your rights and avoid common pitfalls. (External Link: https://www.consumerfinance.gov/)

Conclusion: Your Road to a Smart Auto Loan Decision

Navigating the world of auto car loans can seem daunting, but with the right knowledge and a strategic approach, it becomes a manageable and even empowering process. From understanding your credit score to exploring "auto car loans near me" from various lenders, every step contributes to securing the best possible financing for your vehicle.

Remember, the ultimate goal is not just to get a loan, but to get a smart loan – one with competitive rates, manageable terms, and transparent conditions that align with your financial health. By diligently following the steps outlined in this guide, comparing offers thoroughly, and leveraging both local and online resources, you’ll be well on your way to driving off in your new car with confidence and peace of mind. Start your journey today, compare your options, and make an informed decision that benefits your financial future.