Decoding Bank of America Car Loan APR Rates: Your Ultimate Guide to Smarter Auto Financing

Decoding Bank of America Car Loan APR Rates: Your Ultimate Guide to Smarter Auto Financing Carloan.Guidemechanic.com

Securing a new or used vehicle often involves navigating the complex world of auto loans. For many, Bank of America stands out as a prominent lender, offering a wide range of financing options. But what exactly are their car loan APR rates, and more importantly, how can you ensure you get the best possible deal?

This comprehensive guide is designed to demystify Bank of America car loan APR rates, providing you with an in-depth understanding of how they work, what influences them, and expert strategies to optimize your financing. As an expert blogger and SEO content writer, my goal is to equip you with the knowledge to make informed decisions, transforming what can be a daunting process into a confident financial move.

Decoding Bank of America Car Loan APR Rates: Your Ultimate Guide to Smarter Auto Financing

Understanding the Basics: What is APR and Why Does It Matter?

Before diving into specifics about Bank of America, it’s crucial to grasp the fundamental concept of APR. APR stands for Annual Percentage Rate, and it represents the true annual cost of borrowing money. This isn’t just the interest rate; it also includes certain fees and charges associated with the loan, spread out over the loan term.

While the interest rate is the primary component of your borrowing cost, the APR provides a more holistic picture. It’s the standardized way lenders present the total cost, making it easier for you to compare offers across different institutions. A lower APR directly translates to less money paid over the life of your car loan.

Based on my experience in consumer finance, many people mistakenly focus solely on the monthly payment. While crucial for budgeting, overlooking the APR can lead to significantly higher overall costs. Always prioritize understanding the APR when comparing loan offers.

Bank of America’s Position in the Auto Loan Market

Bank of America is one of the largest financial institutions in the United States, offering a broad spectrum of banking products, including robust auto loan programs. They cater to a diverse clientele, from first-time car buyers to those looking to refinance an existing auto loan. Their extensive reach and established reputation make them a go-to option for many.

They provide financing for both new and used vehicles, as well as lease buyouts. Their online platform allows for convenient application and management of loans, appealing to the modern borrower. Understanding their general offerings sets the stage for a deeper dive into their specific rates.

The Core Influencers: Factors Affecting Your Bank of America Car Loan APR

The APR you receive on a Bank of America car loan isn’t a one-size-fits-all figure. It’s a highly personalized rate, meticulously calculated based on several key factors. Understanding these elements is your first step towards securing a favorable rate.

From an expert perspective, these factors are interconnected, and improving one often positively impacts others. Let’s break down the most significant contributors to your potential APR.

1. Your Credit Score: The Unquestionable King

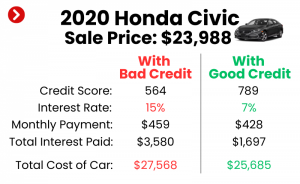

Without a doubt, your credit score is the single most influential factor determining your Bank of America car loan APR. Lenders use your credit score to assess your creditworthiness – essentially, how likely you are to repay the loan on time. A higher credit score signals lower risk to the lender, resulting in a more attractive APR.

Typically, credit scores range from 300 to 850. Scores in the "excellent" (780-850) and "very good" (740-779) ranges will unlock the lowest available rates. "Good" scores (670-739) can still get competitive rates, while "fair" (580-669) and "poor" (below 580) scores will likely face significantly higher APRs, if approved at all.

Pro tips from us: Before even thinking about applying, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, and TransUnion). Dispute any inaccuracies and focus on paying down high-interest debt to boost your score. A small improvement in your credit score can translate into thousands of dollars saved over the life of your loan.

2. Loan Term: Shorter Usually Means Cheaper

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). While longer terms offer lower monthly payments, they almost always come with a higher APR. This is because a longer repayment period increases the lender’s risk exposure and the time value of money.

Consider a 72-month loan versus a 48-month loan. The 72-month loan will have a lower monthly payment, making it seem more affordable. However, the total interest paid will be substantially higher due to the increased APR and the extended period over which interest accrues.

Common mistakes to avoid are extending the loan term purely to reduce the monthly payment without considering the total cost. If you can comfortably afford a shorter term, you’ll save a significant amount of money in the long run.

3. Loan Amount: How Much You Borrow

The total amount you wish to borrow also plays a role, albeit a less direct one than credit score or term. Generally, very small loan amounts might sometimes have slightly higher administrative costs reflected in the APR. Conversely, extremely large loans might also be subject to different risk assessments.

However, the main impact of the loan amount is how it interacts with the loan term and your creditworthiness. A larger loan amount, combined with a longer term or a lower credit score, amplifies the risk for the lender, potentially pushing the APR upwards.

4. Down Payment: Your Upfront Investment

A substantial down payment significantly reduces the amount you need to borrow, thereby lowering the lender’s risk. When you put more money down upfront, Bank of America views you as a more committed and less risky borrower. This often translates directly into a lower APR.

Based on my experience, aiming for a down payment of at least 10-20% of the vehicle’s purchase price is ideal. Not only does it help secure a better APR, but it also reduces your monthly payments and helps you build equity in the car faster. It’s a win-win strategy.

5. Debt-to-Income (DTI) Ratio: Your Financial Balance

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to gauge your ability to handle additional debt. A high DTI ratio indicates that a significant portion of your income is already committed to other obligations, making you a riskier borrower.

Bank of America, like other lenders, prefers borrowers with a low DTI ratio. A DTI below 36% is generally considered excellent, while anything above 43% might make securing a favorable APR more challenging. Managing your existing debts and increasing your income can positively impact this ratio.

6. Vehicle Type and Age: New vs. Used

The type of vehicle you’re financing also influences the APR. New cars typically qualify for lower interest rates than used cars. This is because new cars hold their value better initially, are less prone to immediate mechanical issues, and present less risk to the lender if repossession becomes necessary.

Used cars, especially older models, carry higher risk due to potential depreciation and maintenance costs. Consequently, Bank of America’s APR rates for used car loans are often slightly higher than those for new vehicles. This is a standard practice across most lenders.

7. Market Conditions: The Federal Reserve’s Influence

Broader economic conditions and the prevailing interest rate environment, largely influenced by the Federal Reserve, impact all lending rates, including auto loans. When the Federal Reserve raises its benchmark interest rate, lenders typically follow suit, leading to higher APRs across the board. Conversely, during periods of lower rates, you might find more attractive offers.

While you can’t control market conditions, being aware of them helps you understand why rates might fluctuate. Checking the news for updates on the Fed’s monetary policy can provide context for current Bank of America car loan APR rates.

8. Relationship with Bank of America: Preferred Rewards

If you are an existing Bank of America customer, especially one enrolled in their Preferred Rewards program, you might be eligible for special APR discounts. This program offers tiered benefits based on your combined balances across eligible Bank of America and Merrill accounts.

Preferred Rewards members can receive interest rate reductions on new auto loans, making an already competitive rate even better. This is a significant perk and a strong incentive to consolidate your banking relationship.

How to Find Bank of America’s Current APR Rates

Bank of America makes it relatively straightforward to get an idea of the rates you might qualify for. They typically don’t publish a universal APR table because, as discussed, rates are highly personalized.

- Online Pre-qualification: The most common and convenient method is to use their online pre-qualification tool. This allows you to input basic financial information and get an estimate of your potential APR without impacting your credit score (it uses a soft credit inquiry).

- Official Website: Visit the auto loan section of the Bank of America website. They often display "as low as" rates, which represent the best possible rates for highly qualified borrowers. Remember, these are not guaranteed for everyone.

- Visit a Branch: For a more personalized discussion, you can visit a Bank of America financial center. A loan officer can walk you through the process and provide estimated rates based on your profile.

- Speak with a Loan Officer: You can also call their customer service or auto loan department to inquire about current rates and the application process.

Pro tips from us: Always get a pre-qualification first. This gives you a strong negotiating tool when you visit a dealership, as you’ll know the financing rate you’re approved for directly from Bank of America.

The Application Process for a Bank of America Car Loan

Applying for a Bank of America car loan is a streamlined process, whether you do it online, by phone, or in person. Understanding the steps can help you prepare and expedite approval.

- Gather Your Information: You’ll need personal details (SSN, address, contact info), employment information (employer name, income, job title), and financial details (assets, existing debts).

- Pre-qualification (Optional but Recommended): As mentioned, this step gives you an estimated rate and loan amount without a hard credit pull.

- Formal Application: Once you’re ready, you’ll complete a full application. This involves a hard credit inquiry, which will temporarily affect your credit score.

- Review Offer: Bank of America will present you with a loan offer detailing the APR, loan term, monthly payment, and total cost.

- Funding: If approved and you accept the terms, the funds will be disbursed. Often, this involves sending the funds directly to the dealership.

Based on my experience, having all your documents and information readily available before you start the application saves a lot of time and reduces stress. Be prepared to provide proof of income, such as pay stubs or tax returns.

Pro Tips for Securing the Best Bank of America Car Loan APR

Achieving the lowest possible Bank of America car loan APR requires strategic planning and proactive steps. Here are some expert recommendations:

- Boost Your Credit Score: This is paramount. Pay bills on time, reduce credit card balances, and avoid new credit applications in the months leading up to your car loan application. A higher score directly translates to a lower APR.

- Save for a Larger Down Payment: Aim for at least 10-20% of the vehicle’s price. The less you borrow, the less risk for the lender, and the better your potential APR.

- Shop Around (Even If BofA is Your Primary Choice): Get quotes from multiple lenders, including credit unions and other banks. This gives you leverage and ensures you’re getting a competitive rate. Bank of America often matches or beats competitor offers.

- Keep the Loan Term as Short as Possible: While longer terms mean lower monthly payments, they result in higher overall interest. Choose the shortest term you can comfortably afford.

- Leverage Your Bank of America Relationship: If you’re a Preferred Rewards member, ensure you highlight this during your application to receive applicable discounts. Even without Preferred Rewards, a long-standing, positive banking relationship can sometimes be a minor factor.

- Don’t Overlook Refinancing: If you already have a car loan with a higher APR, consider refinancing with Bank of America, especially if your credit score has improved or market rates have dropped.

Common Mistakes to Avoid When Applying for a Car Loan

Even experienced borrowers can make missteps. Avoiding these common errors can save you money and headaches.

- Not Checking Your Credit Score: Applying without knowing your credit standing is like driving blind. You won’t know what rates you truly qualify for, putting you at a disadvantage.

- Only Applying to One Lender: Limiting yourself to a single lender, even if it’s Bank of America, means you miss out on potentially better offers elsewhere. Always compare.

- Focusing Solely on Monthly Payment: While important for budgeting, fixating only on the monthly payment can lead you to accept longer terms with higher APRs, costing you more in the long run. Always consider the total cost of the loan.

- Ignoring the Total Cost of the Loan: Factor in all aspects: the principal, interest, and any fees. A lower monthly payment isn’t always the cheapest option overall.

- Not Reading the Fine Print: Before signing, thoroughly review your loan agreement. Understand the APR, repayment schedule, prepayment penalties (if any), and late payment fees.

Refinancing Your Bank of America Car Loan: A Second Chance at Better Rates

Perhaps you secured your initial car loan when your credit wasn’t stellar, or interest rates were higher. Refinancing your car loan with Bank of America could be a smart financial move. It essentially means taking out a new loan to pay off your existing one, ideally at a lower APR or with more favorable terms.

When does refinancing make sense?

- Improved Credit Score: If your credit score has significantly improved since you first financed your car.

- Lower Market Rates: If prevailing interest rates have dropped since you took out your original loan.

- High Original APR: If your initial loan came with a very high interest rate.

- Need for Lower Payments: If you need to reduce your monthly payments, though be cautious not to extend the term excessively.

Bank of America offers competitive refinancing options. You can often apply online and receive a decision quickly. Refinancing can lead to substantial savings over the life of your loan, freeing up cash flow or helping you pay off your car faster.

Bank of America Preferred Rewards and Auto Loan Benefits

For loyal Bank of America customers, the Preferred Rewards program offers tangible benefits that can directly impact your auto loan APR. This program rewards clients based on their combined balances across eligible Bank of America deposit accounts and Merrill investment accounts.

There are three tiers: Gold, Platinum, and Platinum Honors, each offering increasing benefits. These benefits include interest rate discounts on new Bank of America auto loans. For example, a Platinum Honors member might receive a 0.50% reduction on their APR. This can translate into hundreds or even thousands of dollars saved, making a compelling case for consolidating your financial relationship with Bank of America. It’s a prime example of how loyalty can pay off in real financial terms.

Understanding Your Loan Agreement: Key Terms to Scrutinize

Once you’re approved and ready to sign, the loan agreement is the most critical document. Don’t rush through it. Here are the key terms you must understand:

- Annual Percentage Rate (APR): Confirm it matches what you were quoted.

- Principal Amount: The original amount you borrowed.

- Total Interest Paid: The total amount of interest you will pay over the loan term.

- Total Cost of the Loan: The sum of the principal and total interest.

- Monthly Payment: The exact amount due each month.

- Payment Due Date: Mark this on your calendar.

- Late Payment Penalties: Understand the charges for missed or late payments.

- Prepayment Penalties: While less common on auto loans, check if there are any fees for paying off your loan early. Bank of America typically does not have these.

- Collateral: The car itself serves as collateral. Understand what happens if you default.

From an expert perspective, taking the time to read and understand every clause prevents future surprises. Don’t hesitate to ask your Bank of America loan officer for clarification on anything you don’t understand. Knowledge is power, especially in financial agreements.

Conclusion: Driving Towards Smarter Bank of America Auto Financing

Navigating Bank of America car loan APR rates doesn’t have to be a mystery. By understanding the core factors that influence your rate, proactively improving your financial profile, and applying strategic tips, you can significantly enhance your chances of securing the best possible auto loan.

Remember, your credit score, down payment, and chosen loan term are paramount. Leverage your existing relationship with Bank of America, especially if you’re a Preferred Rewards member. Most importantly, always compare offers, read the fine print, and focus on the total cost of the loan, not just the monthly payment.

With the insights provided in this guide, you are now well-equipped to approach Bank of America for your next auto loan with confidence and clarity. Drive away knowing you’ve made an informed financial decision. For more details on current rates and to begin your pre-qualification, visit the official Bank of America auto loan page: https://www.bankofamerica.com/auto-loans/