Decoding Car Loan Rates in Cincinnati: Your Ultimate Guide to Driving a Great Deal

Decoding Car Loan Rates in Cincinnati: Your Ultimate Guide to Driving a Great Deal Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether you’re cruising through the vibrant streets of Over-the-Rhine or commuting across the scenic bridges of the Ohio River. For most Cincinnati residents, this journey involves securing a car loan. But navigating the world of auto financing, especially understanding Car Loan Rates Cincinnati, can feel like a complex puzzle.

This comprehensive guide is designed to demystify car loan rates, empowering you with the knowledge and strategies to secure the best possible deal. We’ll delve deep into every aspect, from what influences your rate to where to find the most competitive offers, ensuring you drive away with confidence, not just a new set of wheels. Our ultimate goal is to transform you into an informed consumer, ready to tackle the Cincinnati auto market like a pro.

Decoding Car Loan Rates in Cincinnati: Your Ultimate Guide to Driving a Great Deal

Understanding the Core: What Exactly Are Car Loan Rates?

Before we dive into the specifics of Car Loan Rates Cincinnati, it’s crucial to grasp what a car loan rate actually represents. Simply put, it’s the cost of borrowing money from a lender to purchase a vehicle. This rate is usually expressed as an Annual Percentage Rate (APR).

The APR isn’t just the interest rate; it also incorporates certain fees associated with the loan, giving you a more complete picture of the total cost. A lower APR means you’ll pay less over the life of the loan, saving you potentially thousands of dollars. Therefore, understanding and optimizing your APR is paramount.

There are two primary types of interest rates you’ll encounter: fixed and variable. A fixed-rate loan means your interest rate, and consequently your monthly payment, will remain constant throughout the entire loan term. This provides predictability and makes budgeting much easier, as you know exactly what to expect each month.

On the other hand, a variable-rate loan means your interest rate can change over time, typically in response to a benchmark interest rate like the prime rate. While variable rates might start lower, they introduce an element of risk, as your payments could increase if market rates rise. For car loans, fixed rates are overwhelmingly more common and generally recommended for stability.

The Big Influencers: What Shapes Your Car Loan Rate in Cincinnati?

Several critical factors come into play when lenders determine your Car Loan Rates Cincinnati. Understanding these elements is your first step toward influencing a favorable outcome. Each factor tells a story about your financial health and the perceived risk you present to a lender.

Your Credit Score: The Ultimate Determinant

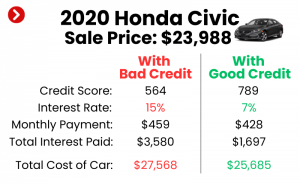

Without a doubt, your credit score is the single most significant factor influencing the car loan rate you’ll be offered. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your loan on time. A higher credit score signals a lower risk, leading to more attractive interest rates.

FICO scores, which range from 300 to 850, are the most widely used credit scoring model. Generally, a score above 700 is considered good, while scores above 750 often qualify for the very best rates. Scores below 600, however, can make it challenging to secure a loan at a reasonable rate, sometimes leading to significantly higher APRs.

Pro tips from us: Before even thinking about applying for a car loan, pull your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) and check your scores. You can do this annually for free at AnnualCreditReport.com. Review them carefully for any errors that could be dragging your score down. Disputing inaccuracies can quickly improve your score.

If your score isn’t where you want it to be, focus on paying bills on time, reducing outstanding debt, and avoiding new credit applications for a few months. Even a modest improvement can have a noticeable impact on your potential Car Loan Rates Cincinnati. For more in-depth strategies, you might find our article "Understanding Your Credit Score: A Comprehensive Guide" helpful in preparing for your car loan journey.

Loan Term: The Length of Your Commitment

The loan term, or the repayment period, also plays a crucial role in determining your interest rate. Shorter loan terms, such as 36 or 48 months, typically come with lower interest rates. This is because the lender is exposed to risk for a shorter period. While your monthly payments will be higher with a shorter term, you’ll pay less interest overall.

Conversely, longer loan terms (e.g., 60, 72, or even 84 months) often have higher interest rates. Lenders perceive a greater risk over an extended period. Although longer terms result in lower monthly payments, they significantly increase the total amount of interest you’ll pay over the life of the loan. It’s a trade-off between monthly affordability and total cost.

Your Down Payment: Showing Your Commitment

Making a substantial down payment is one of the most effective ways to reduce your Car Loan Rates Cincinnati. When you put down a significant portion of the car’s purchase price, you reduce the amount you need to borrow. This lowers the lender’s risk, as they have less money invested in the vehicle, and it shows your commitment to the purchase.

A larger down payment also helps to offset depreciation, preventing you from being "upside down" on your loan (owing more than the car is worth) early in the ownership period. Aiming for at least 10-20% of the car’s value as a down payment is a strong strategy. It not only reduces your loan amount but can also open doors to better rates.

Debt-to-Income Ratio: Your Financial Health Snapshot

Lenders will also look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments (including the potential new car payment) to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to comfortably manage your loan payments, making you a less risky borrower.

Typically, lenders prefer a DTI ratio of 36% or lower, though some might go up to 43% depending on other factors. A high DTI can signal that you’re already stretched thin financially, which could lead to a higher interest rate or even loan denial. Reducing other debts before applying for a car loan can positively impact this ratio.

Vehicle Type and Age: Risk Assessment for the Asset

The type and age of the vehicle you intend to purchase also influence the loan rate. New cars generally command slightly lower interest rates than used cars. This is because new cars hold their value better initially, and their maintenance history is known, presenting less risk to the lender.

Used cars, especially older models, might come with higher interest rates. Lenders perceive a greater risk with used vehicles due to potential mechanical issues and faster depreciation. However, a certified pre-owned (CPO) vehicle, which undergoes rigorous inspections and often comes with an extended warranty, might qualify for rates closer to those of new cars.

Navigating the Cincinnati Car Loan Landscape: Where to Look

When you’re ready to secure your auto loan, knowing where to shop for the best Car Loan Rates Cincinnati is crucial. The options are diverse, each with its own set of advantages and considerations. Exploring multiple avenues is key to finding the most competitive offer.

Banks & Credit Unions: Local vs. National Powerhouses

Your first stop should often be traditional financial institutions. Both large national banks and local Cincinnati banks offer car loans. National banks like Chase, PNC, or Fifth Third Bank often have competitive rates and convenient online application processes. They are typically well-equipped to handle a high volume of loan applications.

However, don’t overlook local Cincinnati banks and especially credit unions. Credit unions, being non-profit organizations owned by their members, often provide some of the most competitive Car Loan Rates Cincinnati. They are known for their personalized service and might be more flexible, especially if you have an existing relationship with them or if your credit score is borderline. Cincinnati has several excellent credit unions, such as General Electric Credit Union or Kemba Credit Union, which are worth investigating.

Based on my experience: Many consumers find that credit unions offer rates that are consistently a quarter to a half-point lower than traditional banks. This seemingly small difference can add up significantly over a 5-year loan term. Always check with at least one local credit union, even if you’re not currently a member, as joining is often straightforward.

Dealership Financing: Convenience at a Potential Cost

Dealerships offer financing as a one-stop shop convenience. You can select your car, negotiate the price, and secure a loan all in the same location. They often work with a network of lenders, sometimes even their own captive finance companies (e.g., Ford Credit, Honda Financial Services).

While convenient, dealership financing isn’t always the cheapest option. They might mark up the interest rate they receive from a lender to generate additional profit. However, dealerships also frequently offer special low-APR promotions, especially on new vehicles, to move inventory. These "subvented rates" can be incredibly attractive, sometimes even 0% APR for well-qualified buyers.

Common mistakes to avoid are: falling for the convenience trap without comparing outside offers. Always arrive at the dealership with a pre-approval in hand. This gives you leverage and ensures you have a benchmark to compare against any offers the dealer presents. If the dealership can beat your pre-approved rate, fantastic! If not, you already have a solid financing option.

Online Lenders: Speed and Comparison Tools

The digital age has brought a surge of online lenders specializing in auto loans. Companies like Capital One Auto Finance, LightStream, or PenFed Credit Union (which also operates like a credit union but has broad eligibility) offer quick online applications and pre-approvals. Many online platforms also allow you to compare multiple loan offers simultaneously, simplifying the shopping process.

Online lenders are known for their speed and efficiency. You can often get a decision within minutes, and funds can be disbursed quickly. They can be particularly useful for comparing rates without the pressure of a salesperson. However, always ensure you’re dealing with reputable lenders by checking reviews and their Better Business Bureau ratings.

The Application Process: Steps to Success

Once you’ve done your research and identified potential lenders, the application process itself requires careful attention to detail. A strategic approach can significantly improve your chances of securing the best Car Loan Rates Cincinnati.

The Power of Pre-Approval

We cannot stress this enough: get pre-approved before you step foot on a dealership lot. Pre-approval means a lender has reviewed your credit, income, and other financial details and provisionally agreed to lend you a certain amount at a specific interest rate. This is not a final loan offer, but it’s very close.

Having a pre-approval serves two critical purposes. First, it clarifies your budget, so you know exactly how much car you can afford without overextending yourself. Second, and perhaps more importantly, it gives you immense negotiating power at the dealership. You’re no longer just a buyer; you’re a buyer with your own financing, which puts you in a much stronger position to negotiate the car’s price rather than just the loan terms.

Gathering Your Documents: Be Prepared

Lenders will require various documents to verify your identity, income, and residency. Being prepared with these documents can expedite the application process. Expect to provide:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residency: Utility bill or lease agreement with your Cincinnati address.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a specific car (VIN, make, model, mileage).

Having these ready to go will make the process smoother and faster, reducing any potential delays in securing your Car Loan Rates Cincinnati.

Reading the Fine Print: Understanding Terms and Conditions

Once you receive a loan offer, resist the urge to sign immediately. Carefully read all the terms and conditions. Pay close attention to:

- The APR: Is it fixed or variable? What is the exact percentage?

- Loan Term: How many months is the loan for?

- Total Loan Amount: Does this match what you need?

- Monthly Payment: Can you comfortably afford this?

- Any Fees: Are there origination fees, documentation fees, or prepayment penalties?

- Insurance Requirements: Lenders typically require full coverage insurance on financed vehicles.

Based on my experience: Many consumers overlook prepayment penalties. While less common with auto loans than mortgages, it’s still worth checking. A prepayment penalty means you’ll be charged a fee if you pay off your loan early. This can hinder your ability to refinance or pay down debt faster.

Special Situations & Advanced Strategies in Cincinnati

Life isn’t always a straight road, and neither is auto financing. Sometimes, you need specific strategies to navigate unique circumstances or optimize an existing loan.

Bad Credit Car Loans Cincinnati: Options and Realities

Having a less-than-perfect credit score doesn’t mean you can’t get a car loan in Cincinnati, but it does mean you’ll likely face higher Car Loan Rates Cincinnati. Lenders view bad credit as a higher risk, and they compensate for that risk with increased interest. However, options are available.

- Specialized Lenders: Some lenders specialize in "subprime" loans for individuals with poor credit. These are often accessible through dealerships.

- Cosigner: A cosigner with good credit can significantly improve your chances of approval and help you secure a lower rate. Their creditworthiness effectively backs your loan.

- Larger Down Payment: As discussed, a larger down payment reduces the loan amount and the lender’s risk, making you a more attractive borrower.

- Secured Loan: Some lenders might offer a secured loan where the car itself serves as collateral, potentially offering better rates than unsecured options for those with poor credit.

While the rates will be higher, successfully managing a bad credit car loan can be an excellent way to rebuild your credit score. Consistent, on-time payments will gradually improve your credit profile, opening doors to better financing in the future.

Refinancing Your Car Loan in Cincinnati: When It Makes Sense

If you’ve already secured a car loan but your financial situation has improved, or market rates have dropped, refinancing could be a smart move. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with better terms.

When does it make sense to refinance?

- Improved Credit Score: If your credit score has significantly increased since you took out the original loan, you might qualify for a much lower rate.

- Lower Market Rates: If prevailing auto loan rates have fallen, you could secure a better deal.

- High Original Rate: Perhaps you had bad credit initially and received a very high rate; now that your credit is better, you can improve it.

- Change in Loan Term: You might want to shorten your term to pay off the loan faster or extend it to lower monthly payments (though this means more interest overall).

Pro tips from us: Check with multiple lenders, including the one that holds your current loan, to compare refinancing offers. Be mindful of any fees associated with the new loan that could negate the savings from a lower interest rate. Our article, "Refinancing Your Auto Loan: Is It Right For You?" offers a deeper dive into this valuable strategy.

Beyond the Rate: Hidden Costs and Long-Term Considerations

While securing the best Car Loan Rates Cincinnati is paramount, it’s just one piece of the puzzle. A truly informed car buyer considers the full financial picture, including costs beyond the monthly payment.

Fees and Charges: The Small Print Surprises

Beyond the interest rate, be aware of various fees that can add to the total cost of your car loan. These can include:

- Origination Fees: A fee charged by the lender for processing your loan.

- Documentation Fees (Doc Fees): Charged by dealerships for preparing paperwork. In Ohio, these are capped or regulated, but always ask for an itemized list.

- Prepayment Penalties: (As discussed) A fee for paying off your loan early.

- Late Payment Fees: Penalties for missing a payment due date.

Always request a detailed breakdown of all fees before signing any loan agreement. Question anything you don’t understand or that seems excessive.

Insurance Requirements: Ohio’s Mandates

Lenders typically require you to carry full coverage auto insurance (collision and comprehensive) on a financed vehicle for the entire loan term. This protects their investment in case of an accident, theft, or natural disaster. The cost of this insurance must be factored into your overall budget.

In Ohio, minimum liability insurance is legally required, but full coverage is usually much more expensive. Get insurance quotes before finalizing your car purchase to avoid any sticker shock. Many insurance providers offer discounts for bundling policies or for safe driving.

Maintenance Costs: The Ongoing Expense

A car loan payment is only one part of owning a vehicle. Don’t forget to budget for ongoing maintenance and repairs. Newer cars come with warranties, but routine maintenance (oil changes, tire rotations, brake service) is always necessary. Used cars, especially older ones, might require more frequent and costly repairs.

Research the typical maintenance costs for the specific make and model you’re considering. Websites like Edmunds or Kelley Blue Book often provide estimates. Overlooking these costs can quickly strain your budget, even if you secured a fantastic Car Loan Rates Cincinnati.

Depreciation: The Silent Cost

Every car begins to lose value the moment it’s driven off the lot. This is called depreciation. While not a direct loan cost, it’s a significant financial reality of car ownership. Understanding depreciation helps you make smarter decisions about your purchase and future trade-in value.

Some vehicles hold their value better than others. Researching resale values can provide insight into which models depreciate more slowly. A car that holds its value well can lead to a better trade-in or sale price down the line, effectively reducing your overall cost of ownership.

For more information on consumer protection in auto financing, you can always refer to trusted external sources like the Federal Trade Commission (FTC) at ftc.gov/autos. They provide valuable insights into your rights as a consumer and common pitfalls to avoid.

Conclusion: Drive Away with Confidence in Cincinnati

Navigating the world of Car Loan Rates Cincinnati doesn’t have to be daunting. By understanding the factors that influence your rate, knowing where to shop, preparing thoroughly, and reading the fine print, you can empower yourself to make informed decisions. Remember, securing the best possible car loan rate is about more than just a low monthly payment; it’s about minimizing your total cost of ownership and ensuring financial peace of mind.

Take the time to improve your credit, gather your documents, and compare offers from multiple lenders. Don’t settle for the first rate you’re offered. With a strategic approach, you’ll not only find a vehicle that fits your needs and lifestyle but also secure a financing deal that keeps your budget on track as you enjoy the open roads of Cincinnati and beyond. Happy driving!