Decoding Car Loans: Your Ultimate Guide to Navigating Auto Financing with Confidence

Decoding Car Loans: Your Ultimate Guide to Navigating Auto Financing with Confidence Carloan.Guidemechanic.com

The dream of a new car, or even a reliable used one, often comes with a significant financial decision: how to pay for it. For the vast majority of people, this means exploring the world of car loans. But how do car loans work, exactly? It can seem like a complex maze of terms, rates, and agreements.

As an expert in personal finance and auto purchasing, I’ve guided countless individuals through this process. My mission with this comprehensive guide is to demystify car financing, breaking down every aspect from understanding your credit to signing on the dotted line and beyond. We’ll explore the mechanics of an auto loan, share insider tips, and highlight common pitfalls to help you make the smartest choices. This isn’t just about getting a loan; it’s about securing a loan that genuinely works for you, ensuring financial peace of mind throughout your car ownership journey.

Decoding Car Loans: Your Ultimate Guide to Navigating Auto Financing with Confidence

The Fundamentals of a Car Loan: What You Absolutely Need to Know

At its core, a car loan is a simple concept: you borrow money from a lender to purchase a vehicle, and you agree to pay that money back over a set period, plus interest. However, understanding the nuances of how do car loans work can save you thousands of dollars and a lot of stress.

What Exactly is a Car Loan?

A car loan is typically a secured loan. This means the vehicle you’re purchasing serves as collateral for the loan. If you fail to make your payments as agreed, the lender has the legal right to repossess the car to recover their losses. This collateral aspect makes car loans generally less risky for lenders compared to unsecured loans, often resulting in lower interest rates than, say, a personal loan.

Based on my experience, recognizing that your car is collateral is crucial. It underscores the importance of consistent, on-time payments to protect your asset and your credit history.

The Key Components of Every Car Loan

To truly grasp how auto loans function, you need to understand the individual elements that make up your loan agreement. Each component plays a vital role in determining your monthly payment and the total cost of the loan.

-

The Principal Amount: This is the actual amount of money you borrow to purchase the car. It’s the sticker price of the vehicle, minus any down payment, trade-in value, or rebates. The higher the principal, generally the higher your monthly payments and overall interest paid, assuming other factors remain constant.

-

The Interest Rate (and APR): The interest rate is the percentage charged by the lender for the use of their money. It’s the cost of borrowing. A lower interest rate means less money you’ll pay back over the life of the loan.

- Pro Tip: Always focus on the Annual Percentage Rate (APR). The APR is a more comprehensive measure of the cost of borrowing because it includes not only the interest rate but also other fees associated with the loan, expressed as a single annual percentage. This makes it easier to compare different loan offers accurately.

-

The Loan Term (Duration): This refers to the length of time you have to repay the car loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term generally results in lower monthly payments, which can be appealing for budgeting.

- Common Mistake: Opting for the longest loan term solely to achieve the lowest monthly payment. While it reduces your immediate burden, it significantly increases the total interest you’ll pay over the life of the loan and extends the period you’re "upside down" (owing more than the car is worth) due to depreciation.

-

The Monthly Payment: This is the fixed amount you agree to pay back to the lender each month. It’s calculated based on the principal amount, interest rate, and loan term. This payment covers a portion of the principal and the accrued interest for that month.

Understanding these foundational elements is your first step toward becoming a savvy car loan borrower. They are interconnected, and a change in one will inevitably affect the others.

The Pre-Loan Preparation Phase: Setting Yourself Up for Success

Before you even step foot into a dealership or apply for a car loan, a significant amount of preparation can dramatically improve your chances of securing favorable terms. This phase is about understanding your financial standing and what you can realistically afford.

Understanding Your Credit Score: Your Financial Report Card

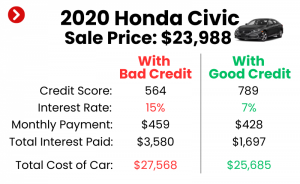

Your credit score is arguably the most influential factor in determining your car loan approval and the interest rate you’ll be offered. Lenders use it to assess your creditworthiness – essentially, how likely you are to repay your debt.

- Why it Matters: A higher credit score (typically 700+) signals to lenders that you are a low-risk borrower, making them more willing to offer you lower interest rates. Conversely, a lower score indicates higher risk, leading to higher interest rates or even loan denial.

- How to Check and Improve It: You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, TransUnion) annually via AnnualCreditReport.com. Review it for errors and address any discrepancies. To improve your score, focus on paying bills on time, reducing existing debt, and avoiding opening too many new credit accounts at once.

Pro Tip from us: Get your credit report and score at least a few months before you plan to buy a car. This gives you time to correct any errors and potentially boost your score, which could save you thousands in interest.

Budgeting for Your Car Loan: Beyond the Monthly Payment

Many prospective car buyers focus solely on the monthly payment, but this is a narrow view. A truly comprehensive budget considers the total cost of ownership.

- Total Cost vs. Monthly Payment: While a low monthly payment might seem attractive, it could be tied to a very long loan term or a high interest rate, significantly increasing the overall amount you pay for the car. Always calculate the total amount you’ll pay back over the loan term, including all interest.

- The Importance of a Down Payment: A substantial down payment reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest paid. It also helps you avoid being "upside down" on your loan (owing more than the car is worth) as quickly, given depreciation. Aim for at least 10-20% if possible.

- Affordability: Your Debt-to-Income Ratio (DTI): Lenders also look at your DTI, which compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 36-40%) indicates you have enough disposable income to comfortably manage new debt, increasing your chances of approval and better rates.

Researching Car Prices and Values: Knowing What You’re Buying

Knowledge is power, especially when it comes to car prices. Don’t go into negotiations blind.

- New vs. Used Cars: Decide whether a new or used vehicle best fits your needs and budget. New cars depreciate rapidly in the first few years, while used cars offer better value for money.

- Understanding Trade-in Value: If you have an existing car, research its potential trade-in value using resources like Kelley Blue Book (KBB.com) or Edmunds. This value can act as a down payment on your new vehicle.

- Depreciation: Be aware that cars lose value over time. Understanding depreciation helps you make realistic financial decisions and avoids negative equity situations down the road.

The Car Loan Application Process: From Pre-Approval to Offer

Once you’ve done your homework, the next step is actively seeking out a car loan. This process involves getting pre-approved, submitting a formal application, and carefully evaluating loan offers.

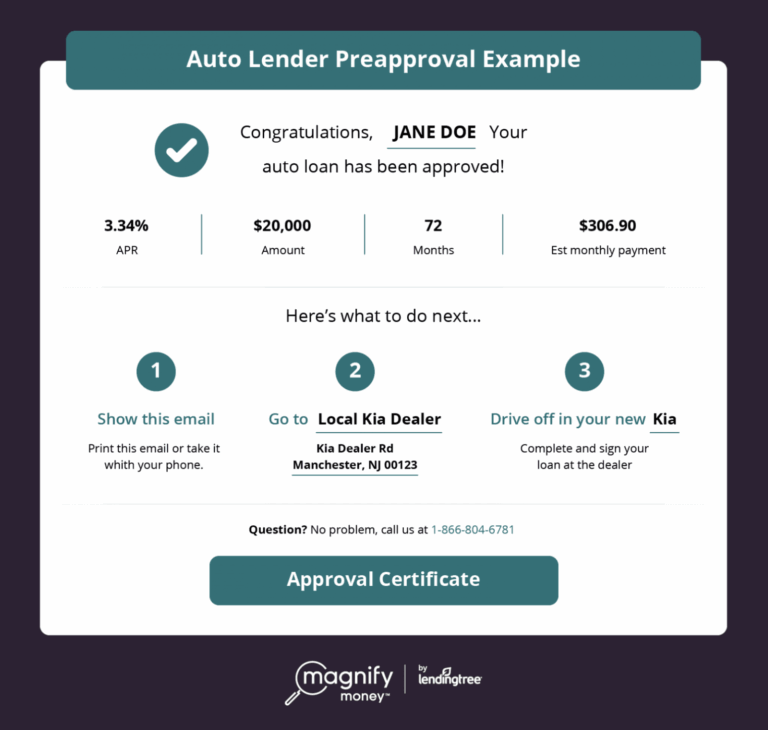

Getting Pre-Approved: Your Secret Weapon

Pre-approval is a conditional commitment from a lender to provide you with a car loan up to a certain amount, at a specific interest rate, before you even choose a car. It’s a game-changer in the car buying process.

- What is Pre-Approval? Lenders will review your credit score, income, and debt to determine how much they are willing to lend you and at what interest rate. This often involves a "soft" credit inquiry, which doesn’t harm your score, though a full application usually involves a "hard" inquiry.

- Benefits of Pre-Approval:

- Negotiating Power: You walk into the dealership knowing exactly how much you can spend and what your interest rate will be. This allows you to negotiate the car price as if you were a cash buyer, rather than focusing on monthly payments that a salesperson might manipulate.

- Knowing Your Budget: It sets clear boundaries for your car search, preventing you from falling in love with a vehicle you can’t truly afford.

- Streamlined Process: It speeds up the buying process at the dealership.

- Where to Get Pre-Approved: Don’t limit yourself to the dealership’s financing. Explore options from banks, credit unions, and reputable online lenders. Credit unions, in particular, often offer very competitive rates.

Based on my experience, getting pre-approved by at least one external lender (like your bank or credit union) before visiting a dealership is non-negotiable. It gives you a benchmark and ensures you get the best possible financing terms.

The Loan Application: What to Expect

Once you’ve found a car and are ready to finalize financing, you’ll submit a formal car loan application.

- Required Documents: Be prepared to provide identification (driver’s license), proof of income (pay stubs, tax returns), proof of residency (utility bill), and potentially information about your existing debts and assets.

- Information Requested: The application will ask for personal details, employment history, financial information, and the specifics of the vehicle you intend to purchase.

- Common Mistakes to Avoid:

- Applying to Too Many Places at Once: While rate shopping is good, submitting multiple loan applications within a very short period (typically 14-45 days) will usually be grouped as a single inquiry by credit bureaus, minimizing impact. However, spreading out applications too much can lower your score. Focus on a few strong contenders.

- Not Being Honest: Always provide accurate information. Misrepresenting your financial situation can lead to loan denial or even legal issues.

Understanding the Loan Offer: Read the Fine Print

Once your application is approved, you’ll receive a loan offer (or multiple offers if you’ve applied to several lenders). This is where critical evaluation comes in.

- Comparing Multiple Offers: Don’t just pick the first offer. Compare the APR, loan term, and total cost of the loan from all your pre-approvals and any offers from the dealership.

- Focus on APR, Not Just Monthly Payment: As discussed, APR gives you the true cost of borrowing. A lower monthly payment might mask a higher overall cost due to a longer term or hidden fees.

- Reading the Fine Print: Scrutinize the entire loan agreement. Look for any origination fees, prepayment penalties (though rare for car loans), late payment fees, and specific clauses regarding repossession. Ask questions about anything you don’t understand.

Navigating the Loan Agreement and Purchase: Sealing the Deal

With your loan offer in hand, you’re ready to complete the purchase. This stage involves understanding the legal agreement and finalizing the transaction.

The Loan Agreement: Your Legal Contract

The car loan agreement is a legally binding contract between you and the lender. It outlines the terms and conditions of your loan.

- What to Look For: Ensure all the details match what you discussed and agreed upon: the principal amount, the exact APR, the loan term, the monthly payment, and the total amount repayable. Check for any added services or warranties that might have been tacked on without your explicit consent.

- The Role of a Guarantor/Co-signer: If your credit score is insufficient, a lender might require a co-signer. This person legally agrees to be responsible for the loan if you fail to make payments. This significantly increases your approval chances but places a substantial financial burden on the co-signer if you default.

Making the Purchase: Finalizing the Deal

Whether you’re buying from a dealership or a private seller, the final steps require attention to detail.

- Finalizing the Deal at the Dealership: If you’re using dealership financing, they will present their offer. Compare it to your pre-approvals. If their offer is better, great! If not, stick with your pre-approved loan. Be wary of last-minute changes or pressure tactics.

- Avoiding Common Dealership Financing Traps: Watch out for "four-square" worksheets that juggle trade-in value, purchase price, down payment, and monthly payments to confuse you. Negotiate each aspect separately. Also, be careful about extended warranties or add-ons that significantly increase your loan amount if you don’t truly need them.

- Pro Tip: Don’t rush the process. Take your time to review all documents before signing. You have the right to understand everything you’re agreeing to.

Title and Registration: How the Lender Holds Your Car

Once the loan is finalized, the car is yours, but the lender maintains an interest in it.

- Lienholder: The lender will be listed as a "lienholder" on the car’s title. This means they legally own a portion of the vehicle until the loan is fully paid off.

- Registration: The car will be registered in your name, but the title will be held by the lender or an electronic record will show their lien. You’ll receive the physical title only after the loan is satisfied.

Managing Your Car Loan & Beyond: Life After Purchase

Getting the car is just the beginning. Responsible loan management is key to a positive financial outcome and protects your credit score.

Making Payments: Consistency is Key

- On-Time Payments Are Crucial: Missing or making late payments will incur late fees and negatively impact your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

- Understanding Amortization: In the early stages of your loan, a larger portion of your monthly payment goes towards interest. As the loan matures, more of your payment goes towards reducing the principal. This is called amortization.

Early Payoff Strategies: Saving on Interest

If your financial situation improves, paying off your car loan early can save you a significant amount in interest.

- Pros and Cons: The primary benefit is reducing the total interest paid and becoming debt-free sooner. The main con is that this money could potentially be invested elsewhere for a higher return, or used to pay off higher-interest debt (like credit cards).

- Bi-Weekly Payments: Instead of one monthly payment, you make a payment every two weeks. Since there are 26 bi-weekly periods in a year, this results in 13 full monthly payments annually, effectively shaving time and interest off your loan.

Refinancing Your Car Loan: When and Why to Consider It

Refinancing means taking out a new loan to pay off your existing car loan, often with a different lender or different terms.

- When to Consider It:

- If interest rates have dropped since you took out your original loan.

- If your credit score has significantly improved.

- If you need to lower your monthly payments (though this often means extending the loan term).

- If you want to shorten your loan term to pay less interest overall.

- How it Works: You apply for a new loan. If approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new terms.

When Your Loan is Paid Off: The Final Steps

Congratulations! Once you’ve made your final payment, there are a few important steps to complete.

- Getting the The lender will remove their lien and send you the clear title to your vehicle. Keep this document in a safe place.

- Updating Insurance: While not always necessary, you might choose to adjust your comprehensive or collision coverage now that the lender no longer has a financial stake in your car.

Common Car Loan Myths Debunked

There are many misconceptions about car loans that can lead borrowers astray. Let’s set the record straight.

- Myth 1: "Longer terms always mean lower overall cost."

- Reality: While longer terms lead to lower monthly payments, they almost always result in a significantly higher total cost due to more interest accruing over a longer period. Always compare the total repayment amount.

- Myth 2: "Dealership financing is always the best option."

- Reality: Dealerships are businesses, and while they can sometimes offer competitive rates (especially through manufacturer incentives), they often mark up interest rates to increase their profit. Always shop around with banks and credit unions before visiting the dealership.

- Myth 3: "My credit score doesn’t matter much for a car loan."

- Reality: Your credit score is paramount. It’s the primary factor lenders use to determine your risk and, consequently, the interest rate you’ll receive. A poor score can mean paying thousands more over the life of the loan.

Conclusion: Driving Away with Confidence

Navigating the world of car loans doesn’t have to be daunting. By understanding how do car loans work, from the initial research to the final payment, you empower yourself to make informed decisions that benefit your financial health. Remember to prioritize preparation, shop around for the best rates, read every document carefully, and manage your loan responsibly.

Your journey to car ownership should be exciting, not stressful. With the comprehensive knowledge gained from this guide, you’re well-equipped to secure a car loan that fits your budget and helps you drive away with confidence, knowing you’ve made a smart financial choice.