Decoding GM Car Loan Interest Rates: Your Ultimate Guide to Smart Financing

Decoding GM Car Loan Interest Rates: Your Ultimate Guide to Smart Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle from General Motors – be it a sleek Chevrolet, a robust GMC, a refined Buick, or a luxurious Cadillac – is an exciting prospect. However, for most buyers, understanding the intricacies of car financing, particularly the ever-important interest rates, can feel like navigating a complex maze. Your car loan interest rate isn’t just a number; it’s a pivotal factor that dictates the total cost of your vehicle over time.

This comprehensive guide is meticulously crafted to demystify GM car loan interest rates. We’ll delve deep into what influences these rates, where to secure the best financing, and crucial strategies to ensure you get the most favorable terms possible. Our ultimate goal is to equip you with the knowledge and confidence to make informed decisions, saving you potentially thousands of dollars and transforming your car buying experience from stressful to seamless.

Decoding GM Car Loan Interest Rates: Your Ultimate Guide to Smart Financing

What Exactly Are GM Car Loan Interest Rates?

When we talk about GM car loan interest rates, we’re referring to the cost of borrowing money to purchase a vehicle from one of General Motors’ esteemed brands. This "cost" is expressed as an Annual Percentage Rate (APR), which encompasses not only the interest charged on the principal loan amount but also any associated fees. It’s the true annual cost of your loan.

Unlike a fixed price tag, there isn’t one universal "GM interest rate." These rates are highly individualized, fluctuating based on a multitude of factors unique to each borrower and economic conditions. Understanding this fundamental variability is the first step toward securing a great deal.

The Powerhouse Behind GM: A Quick Look at Its Brands

General Motors (GM) stands as one of the world’s largest and most respected automotive manufacturers. Its diverse portfolio of brands caters to a wide spectrum of tastes and needs, from daily commuters to luxury enthusiasts. When you’re seeking financing for a GM vehicle, you might be looking at:

- Chevrolet: Known for its wide range of vehicles, from efficient sedans and popular SUVs to powerful trucks and iconic sports cars.

- GMC: Specializes in trucks and SUVs, offering premium features and robust performance for those who demand more from their utility vehicles.

- Buick: Provides refined, near-luxury vehicles with a focus on comfort, quiet rides, and sophisticated design.

- Cadillac: The pinnacle of GM luxury, offering high-performance sedans, SUVs, and future-forward electric vehicles with cutting-edge technology.

Each of these brands falls under the GM umbrella, and while financing options might vary slightly based on specific promotions, the underlying principles of securing a car loan remain consistent across the board.

Key Factors Dramatically Influencing Your GM Car Loan Interest Rate

Securing the best possible interest rate is paramount, as it directly impacts your monthly payments and the total amount you’ll pay over the life of the loan. Based on my experience in the automotive financing sector, several critical elements consistently play a significant role. Let’s explore each one in detail.

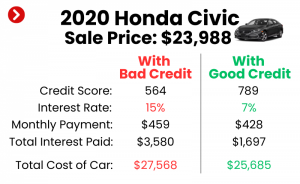

Your Credit Score: The Unquestionable King

Without a doubt, your credit score is the single most influential factor determining the interest rate you’ll be offered. It acts as a report card for your financial responsibility, telling lenders how likely you are to repay your debts.

- Excellent Credit (780+): Borrowers in this tier typically qualify for the lowest available interest rates, often advertised as "special" or "promotional" rates. Lenders view you as a very low-risk borrower.

- Good Credit (670-779): Most consumers fall into this category. You’ll still qualify for competitive rates, though they might be slightly higher than those for excellent credit. You have a solid financial history.

- Fair Credit (580-669): Lenders consider this a moderate risk. You’ll likely be approved for a loan, but with higher interest rates to compensate for the increased risk. Your payment history might show some inconsistencies.

- Poor Credit (Below 580): Securing a loan can be challenging, and if approved, the interest rates will be significantly higher, sometimes even double-digit percentages. Lenders perceive a higher risk of default.

Pro tips from us: Before even stepping foot in a dealership, pull your credit reports from all three major bureaus (Equifax, Experian, TransUnion). Review them for accuracy and dispute any errors immediately. Even a small improvement in your score can translate to substantial savings over the loan term.

Loan Term: The Length of Your Commitment

The loan term, or the duration over which you agree to repay the loan, also profoundly affects your interest rate. Generally, shorter loan terms come with lower interest rates.

- Shorter Terms (e.g., 36 or 48 months): These usually have lower interest rates because the lender’s risk is reduced over a shorter period. Your monthly payments will be higher, but you’ll pay significantly less in total interest.

- Longer Terms (e.g., 60, 72, or even 84 months): While longer terms result in lower monthly payments, making the car seem more affordable upfront, they typically carry higher interest rates. This is because the lender is taking on risk for a longer period, and you’ll end up paying much more in total interest over the life of the loan.

Common mistakes to avoid are extending the loan term purely to reduce the monthly payment without considering the total cost. Always weigh the short-term benefit of lower payments against the long-term cost of increased interest.

Down Payment Amount: Your Initial Investment

A substantial down payment works wonders in securing a lower interest rate. When you put down a significant portion of the car’s price, you immediately reduce the amount you need to borrow.

- Reduced Risk for Lenders: A larger down payment signals to lenders that you are serious about your purchase and have a financial stake in the vehicle. It also reduces their financial exposure.

- Lower Loan-to-Value (LTV) Ratio: Lenders look at the LTV ratio, which compares the loan amount to the car’s value. A lower LTV (meaning you borrowed less relative to the car’s price) is seen as less risky, often leading to better rates.

- Reduced Negative Equity Risk: Cars depreciate rapidly. A good down payment helps prevent you from owing more on the car than it’s worth, especially in the early years of the loan.

Aim for at least 10-20% of the vehicle’s purchase price as a down payment if possible. This can significantly improve your financing terms.

New vs. Used Vehicle: Age Matters

The age and condition of the vehicle you’re financing also play a role in the interest rate. New cars typically qualify for lower interest rates than used cars.

- New Cars: Lenders perceive new cars as lower risk. They have a known value, come with warranties, and are less likely to have immediate mechanical issues. This often translates to lower rates, especially with manufacturer incentives.

- Used Cars: Used cars generally carry higher interest rates. Their value can be more variable, they may have an unknown history, and their depreciation curve is different. Lenders assess a higher risk with used vehicle loans.

However, a well-maintained, certified pre-owned (CPO) GM vehicle might qualify for rates closer to new car financing, as CPO programs often come with extended warranties and rigorous inspections, reducing lender risk.

Debt-to-Income (DTI) Ratio: Your Financial Balance

Your Debt-to-Income (DTI) ratio is another critical metric lenders use to assess your ability to manage additional debt. It compares your total monthly debt payments to your gross monthly income.

- How it’s Calculated: (Total Monthly Debt Payments / Gross Monthly Income) x 100%.

- Lender’s Perspective: A lower DTI ratio (ideally below 36%) indicates that you have plenty of income to cover your existing obligations and a new car payment. A high DTI might suggest you’re overextended, making you a higher risk.

Even with a great credit score, a high DTI could lead to a higher interest rate or even loan denial, as it raises concerns about your capacity to take on more debt.

Current Market Conditions & Promotional Offers

Interest rates are not static; they are influenced by broader economic factors, particularly the federal funds rate set by the Federal Reserve. When the Fed raises rates, borrowing costs generally increase across the board, including for auto loans.

- Federal Reserve Impact: Changes in the federal funds rate trickle down to prime rates, which lenders use as a benchmark.

- Manufacturer Incentives: GM Financial and its brands (Chevrolet, GMC, Buick, Cadillac) frequently offer special promotional rates, such as 0% APR for qualified buyers on specific models. These limited-time offers can be incredibly attractive but usually require excellent credit.

Keep an eye on these promotions, but always read the fine print. They often apply only to new vehicles, specific models, or shorter loan terms.

Where to Secure Your GM Car Loan: Exploring Your Options

When it comes to financing your GM vehicle, you have several avenues to explore. Each has its own advantages and disadvantages.

1. GM Financial (Dealership Financing)

GM Financial is the captive finance arm of General Motors. This means they are directly affiliated with the manufacturer and specialize in financing GM vehicles.

- Pros: Convenience (one-stop shopping at the dealership), often offers special promotional rates (0% APR, low-APR deals) directly from GM, can sometimes be more flexible with credit challenges for specific GM models. They also handle GM leases.

- Cons: Rates might not always be the absolute lowest compared to shopping around, and their focus is primarily on GM vehicles.

Based on my experience, many buyers find the ease of dealership financing appealing, especially when attractive manufacturer incentives are available.

2. Banks

Traditional banks are a popular choice for auto loans. They offer competitive rates and a familiar lending environment.

- Pros: Often have competitive interest rates, especially for existing customers, offer various loan terms, and provide personalized service. You can often get pre-approved before visiting the dealership.

- Cons: Application processes can sometimes be slower than online lenders, and they might have stricter credit requirements for their best rates.

Building a relationship with your bank can sometimes unlock better loan products.

3. Credit Unions

Credit unions are non-profit financial institutions owned by their members. They are renowned for offering some of the most competitive auto loan rates.

- Pros: Typically offer lower interest rates and more flexible terms than traditional banks, often have fewer fees, and provide a more personalized, member-focused service.

- Cons: You usually need to become a member to qualify for a loan, which may involve meeting specific eligibility criteria (e.g., living in a certain area, working for a specific employer).

Pro tips from us: Always check with local credit unions. Their rates can be surprisingly good.

4. Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto loans, offering speed and convenience.

- Pros: Quick application and approval processes, easy rate comparisons from multiple lenders, convenient from home, and often cater to a wider range of credit profiles.

- Cons: Less personalized service, and you might miss out on specific manufacturer incentives.

Online lenders are excellent for getting pre-approved quickly and comparing offers without the pressure of a dealership.

Strategies to Get the Best GM Car Loan Interest Rate

Don’t leave your interest rate to chance. Proactive steps can significantly improve your chances of securing the most favorable terms for your GM vehicle.

1. Check Your Credit Score (and Improve It)

As discussed, your credit score is king. Obtain your free credit report from AnnualCreditReport.com. Review it for accuracy and identify any areas for improvement.

- Pay Bills On Time: Consistency is key. Late payments severely damage your score.

- Reduce Existing Debt: Lowering your credit utilization ratio (how much credit you use vs. how much you have available) can boost your score.

- Avoid Opening New Credit Accounts: Multiple hard inquiries in a short period can temporarily lower your score.

2. Get Pre-Approved Before You Shop

This is perhaps the most powerful tool in your car-buying arsenal. Getting pre-approved means a lender has already evaluated your creditworthiness and offered you a specific loan amount at a certain interest rate.

- Empowered Negotiation: You walk into the dealership knowing exactly what rate you qualify for, giving you a strong negotiating position. You can use this offer to challenge dealership financing.

- Focus on Car Price: With financing secured, you can focus purely on negotiating the best price for the GM vehicle itself, rather than getting distracted by monthly payment discussions.

- for a more in-depth look at this crucial step.

3. Shop Around and Compare Offers

Never take the first offer, whether from the dealership or your primary bank. Apply to several lenders (banks, credit unions, online lenders) within a short window (typically 14-45 days) to minimize the impact on your credit score (multiple inquiries within this period are often treated as a single inquiry for rate shopping).

- Create a Comparison Chart: List out the APR, loan term, monthly payment, and total interest paid for each offer.

- Don’t Just Look at Monthly Payment: Focus on the APR and the total cost of the loan. A lower monthly payment over a longer term can mean paying significantly more overall.

4. Consider a Larger Down Payment

We’ve highlighted the benefits of a down payment. If you can afford it, increasing your down payment can reduce the principal amount borrowed, lowering your monthly payment and potentially securing a better interest rate.

5. Negotiate the Price of the Car First

It’s a common mistake to bundle the car price negotiation with the financing discussion. Dealerships might inflate one to make the other seem better.

- Separate Negotiations: Agree on the final purchase price of the GM vehicle before discussing financing. This ensures you’re getting a fair deal on the car itself.

- Then Present Your Pre-Approval: Once the car price is set, present your pre-approved loan offer. The dealership might try to beat it, or you can simply use your pre-approval.

6. Understand the Full Loan Terms (APR, Not Just Interest Rate)

Always pay attention to the Annual Percentage Rate (APR), not just the stated interest rate. The APR includes the interest rate plus any fees or additional costs wrapped into the loan. This gives you the true cost of borrowing.

- Read the Fine Print: Scrutinize all loan documents before signing. Ensure there are no hidden fees or clauses you don’t understand.

The Application Process: What to Expect

Once you’ve found your ideal GM vehicle and secured a favorable loan offer, the application process is relatively straightforward.

- Documents Needed: Be prepared with identification (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and potentially trade-in details if applicable.

- Credit Check: The lender will perform a hard inquiry on your credit report.

- Approval/Denial: You’ll receive a decision, often quickly, especially with pre-approval or online applications.

Refinancing Your GM Car Loan: A Second Chance at Better Rates

Even if you’ve already financed your GM vehicle, you might be able to secure a better deal through refinancing. This involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms.

- When It Makes Sense:

- Improved Credit Score: If your credit score has significantly improved since you first bought the car.

- Lower Market Rates: If prevailing interest rates have dropped.

- High Original Rate: If you secured a high interest rate initially due to poor credit or lack of research.

- Change Loan Term: To lower monthly payments (by extending the term) or pay off faster (by shortening the term).

Refinancing can save you a substantial amount of money over the remaining life of your loan.

Pro Tips for a Smooth GM Car Financing Journey

Based on my experience helping countless buyers, here are some invaluable tips to make your GM car financing experience as smooth and cost-effective as possible.

- Budget Realistically: Don’t just consider the monthly car payment. Factor in insurance, fuel, maintenance, and potential registration fees. A car payment you can comfortably afford is part of a larger financial picture.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or if the financing terms are unfavorable, be prepared to walk away. There are always other GM vehicles and other lenders.

- Consider Gap Insurance: This insurance covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. It’s often recommended for new cars, especially if you have a small down payment. However, shop around; your auto insurance provider might offer it cheaper than the dealership.

- Read Customer Reviews: Research the dealership and lender online. Positive reviews often indicate transparent practices and good customer service.

Common Mistakes to Avoid When Financing a GM Vehicle

Avoiding these pitfalls can save you significant money and stress.

- Focusing Only on the Monthly Payment: This is the most common mistake. A low monthly payment often comes with a longer loan term and a much higher total interest paid. Always look at the APR and the total cost of the loan.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval is like playing poker without seeing your cards. You lose your negotiation power.

- Ignoring Your Credit Report: Errors on your credit report can needlessly inflate your interest rate. Check it regularly!

- Taking the Longest Loan Term Possible: While it offers the lowest monthly payment, it significantly increases the total interest you pay and prolongs the period you’re making car payments.

- Not Factoring in Trade-In Value Separately: Negotiate your trade-in value and the new car’s price as separate transactions. Don’t let the dealership obscure either figure.

- Buying Unnecessary Add-ons: Be wary of high-pressure sales tactics for extended warranties, paint protection, or other extras that can significantly inflate your loan amount and interest. Only purchase what you truly need and understand.

Conclusion: Drive Smart, Finance Smarter

Navigating the world of GM car loan interest rates doesn’t have to be daunting. By understanding the key factors that influence your rates, exploring all available financing options, and employing smart strategies, you can confidently secure a loan that aligns with your financial goals. Remember, knowledge is power, and taking a proactive, informed approach to financing your Chevrolet, GMC, Buick, or Cadillac will not only save you money but also enhance your overall car ownership experience.

Your dream GM vehicle is within reach. Drive smart, finance smarter, and enjoy the road ahead with the peace of mind that comes from a well-secured loan.