Decoding Navy Federal New Car Loan Interest Rates: Your Ultimate Guide to Smart Auto Financing

Decoding Navy Federal New Car Loan Interest Rates: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new car is an exciting prospect. However, navigating the world of auto loans and interest rates can often feel like a complex maze. For members of the military, veterans, and their families, Navy Federal Credit Union (NFCU) stands out as a beacon of trust and competitive financing options.

This comprehensive guide will meticulously break down everything you need to know about Navy Federal new car loan interest rates. We’ll delve into what influences these rates, how to secure the best possible deal, and provide expert insights to empower you on your path to a new vehicle. Our goal is to equip you with the knowledge to make informed decisions, ensuring you drive away not just with your dream car, but with a financing plan that truly benefits you.

Decoding Navy Federal New Car Loan Interest Rates: Your Ultimate Guide to Smart Auto Financing

Understanding Navy Federal Credit Union and Its Car Loan Benefits

Before we dive deep into interest rates, let’s establish why Navy Federal Credit Union is a preferred choice for many seeking auto loans. NFCU isn’t just another financial institution; it’s a member-owned, not-for-profit cooperative dedicated to serving the financial needs of the armed forces and their families.

Who is Navy Federal and Who Can Join?

Navy Federal Credit Union was founded on the principle of providing financial services to military personnel. Its membership is open to all branches of the armed forces, including active duty, reservists, veterans, Department of Defense civilians, and their immediate family members. This exclusive membership model allows NFCU to tailor its products and services specifically to the unique circumstances of the military community.

Joining NFCU is often the first step towards accessing their highly competitive loan products. Eligibility extends to a wide range of individuals connected to the military, ensuring a broad base can benefit from their offerings. If you have a connection to the armed forces, it’s worth exploring your eligibility.

Why Choose NFCU for a Car Loan? Beyond Just Rates

While competitive interest rates are a significant draw, Navy Federal offers a holistic package that extends beyond just the numbers. Their member-centric approach means you’re more than just a loan application; you’re part of a community. This often translates into exceptional customer service, flexible loan terms, and a genuine understanding of military life’s financial realities.

Based on my experience, NFCU’s commitment to its members shines through in their customer support. They often provide personalized guidance, helping you navigate the complexities of car financing with ease. This level of service can be invaluable, especially when making such a significant financial decision.

Decoding Navy Federal New Car Loan Interest Rates

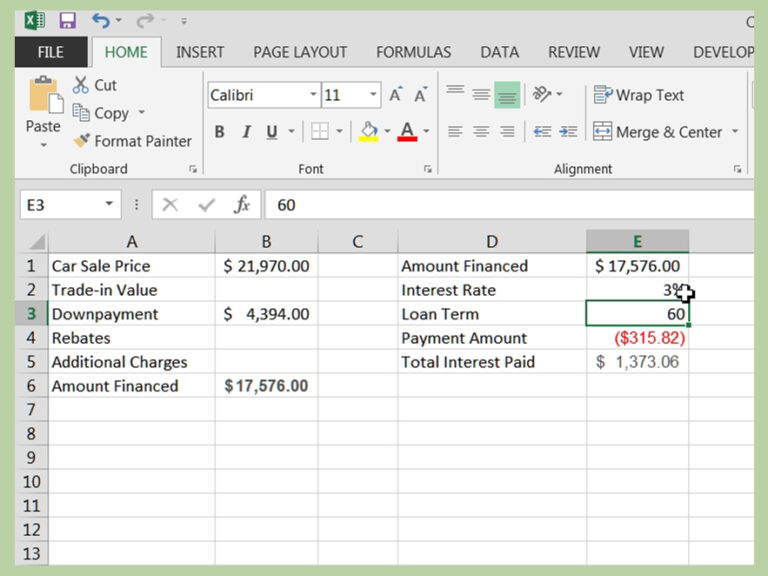

The core of this discussion revolves around understanding the Navy Federal new car loan interest rates. These rates are not static; they fluctuate based on a multitude of factors, both personal to you and related to the broader economic climate. Knowing what influences these rates is your first step towards securing a favorable deal.

What Influences Your Interest Rate?

Several key elements come into play when NFCU determines your specific interest rate for a new car loan. Understanding these can help you strategize before even applying.

- Your Credit Score: This is arguably the most critical factor. A higher credit score signals to lenders that you are a responsible borrower, making you eligible for lower interest rates. NFCU, like most lenders, uses credit scores to assess risk.

- Loan Term: The length of time you take to repay the loan significantly impacts the rate. Shorter loan terms typically come with lower interest rates, though they mean higher monthly payments.

- Down Payment: A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. This can often translate into a better interest rate.

- Vehicle Age and Type: While this article focuses on new car loans, even within new cars, specific models or types might have slightly different rate structures based on their perceived value retention or special promotions.

- Relationship with Navy Federal: Your existing banking relationship with NFCU, including direct deposit or other accounts, can sometimes influence your eligibility for preferred rates or discounts.

- Automatic Payments (Auto Pay): Opting for automatic payments directly from your NFCU account can often qualify you for a slight rate discount, as it reduces the administrative burden and risk of missed payments for the credit union.

Typical Rate Ranges (Acknowledging Variability)

It’s important to understand that providing exact, real-time Navy Federal new car loan interest rates here is impossible due to their dynamic nature. Rates change frequently based on market conditions, Federal Reserve actions, and NFCU’s internal policies. However, NFCU is consistently known for offering highly competitive rates, often lower than traditional banks, especially for members with excellent credit.

Generally, you can expect rates to be in the low single digits for well-qualified borrowers. These rates can climb higher depending on your credit profile and chosen loan terms. The best way to get the most accurate, current rates is always directly from Navy Federal’s official channels.

How to Find Current Navy Federal Auto Loan Rates

To get the most up-to-date and personalized Navy Federal new car loan interest rates, there are a few reliable methods:

- NFCU’s Official Website: Their website typically features a "Rates" section where you can find current auto loan rates. They often provide a range based on credit tiers and loan terms.

- Online Pre-Approval Tool: Utilizing NFCU’s online pre-approval application will give you a personalized rate quote without impacting your credit score significantly (it’s often a "soft" inquiry initially).

- Contact a Loan Officer: Speaking directly with a Navy Federal loan officer, either by phone or in person, allows you to discuss your specific situation and get precise rate information tailored to you.

Pro tips from us: Always check the rates on the day you plan to apply or within a very short window. Rates can shift, and staying current ensures you’re working with the most accurate figures.

Factors That Drive Your Interest Rate (and How to Optimize Them)

Now, let’s break down the major factors influencing your interest rate and explore actionable strategies to optimize each one.

1. Your Credit Score: The Cornerstone of Good Rates

Your credit score is a three-digit number that summarizes your creditworthiness. It’s a key indicator for lenders like NFCU. A higher score signifies a lower risk, translating into more favorable Navy Federal new car loan interest rates.

- Understanding FICO Scores: Most lenders, including Navy Federal, primarily use FICO scores. These scores range from 300 to 850, with higher numbers being better. Scores above 700 are generally considered "good," while those above 760 are "excellent."

- Impact on Rates: The difference between a good and an excellent credit score can mean a full percentage point or more off your interest rate over the life of the loan. This seemingly small difference can save you hundreds, if not thousands, of dollars.

- How to Improve It: Based on my experience, focusing on these areas can significantly boost your score:

- Pay Bills on Time: Payment history is the most important factor in your credit score.

- Reduce Credit Card Balances: Keep your credit utilization (the amount of credit you’re using compared to your total available credit) below 30%, ideally below 10%.

- Avoid New Credit Inquiries: Don’t open multiple new credit accounts just before applying for a car loan.

- Check Your Credit Report for Errors: Regularly review your credit reports from Equifax, Experian, and TransUnion for inaccuracies. You can get free copies annually from AnnualCreditReport.com.

2. Loan Term: The Balancing Act

The loan term is the length of time you have to repay your auto loan. Common terms range from 36 months (3 years) to 72 or even 84 months (7 years).

- Shorter Terms, Lower Rates: Generally, shorter loan terms come with lower interest rates because the lender’s risk is spread over a shorter period. Your total interest paid will be significantly less.

- Longer Terms, Higher Rates (and More Interest): While longer terms offer lower monthly payments, they typically have higher interest rates. This means you’ll pay more in total interest over the life of the loan.

- Finding Your Sweet Spot: The key is to find a term that offers a manageable monthly payment without extending the loan unnecessarily. Pro tips from us: Aim for the shortest term you can comfortably afford, considering your budget and other financial goals.

3. Down Payment: Reducing Risk, Reducing Rates

A down payment is the initial amount of money you pay upfront for the car, reducing the amount you need to borrow.

- Impact on Rates: A larger down payment reduces the loan-to-value (LTV) ratio, which is the amount borrowed relative to the car’s value. A lower LTV means less risk for NFCU, potentially qualifying you for lower Navy Federal new car loan interest rates.

- Benefits Beyond Rates: A substantial down payment also reduces your monthly payments and helps prevent you from being "upside down" on your loan (owing more than the car is worth) early in the ownership period.

- How Much to Put Down? While there’s no magic number, aiming for 10-20% of the vehicle’s purchase price is a good starting point for new cars. If you can do more, it’s often beneficial.

4. Vehicle Age and Type: New vs. Used (and Special Offers)

While this guide focuses on new car loans, it’s worth noting that new cars generally qualify for lower interest rates than used cars. This is because new cars typically retain their value better initially and pose less risk to the lender.

- New Car Advantages: NFCU often has specific, attractive rates for new vehicles, sometimes even partnering with manufacturers for special promotions.

- Leveraging Incentives: Be aware of any manufacturer-backed low-APR (Annual Percentage Rate) offers. Sometimes these are better than what NFCU can offer, but they usually require excellent credit. Always compare the total cost.

5. NFCU Relationship & Auto Pay: Member Benefits

Your existing relationship with Navy Federal can be a valuable asset in securing the best rates.

- Loyalty Benefits: Being a long-standing, responsible member with multiple accounts (checking, savings, credit cards) can sometimes give you an edge. While not always an explicit discount, it builds a history of trust.

- Automatic Payment Discount: As mentioned, opting for automatic payments directly from your NFCU checking account often provides a small interest rate reduction. This is a common and easy way to shave a few basis points off your rate.

- Pro tips from us: If you’re an NFCU member, ensure your accounts are in good standing. Set up direct deposit or maintain a healthy balance to strengthen your relationship before applying for a major loan.

The Application Process: A Step-by-Step Guide

Securing a Navy Federal new car loan involves a straightforward process, but understanding each step can save you time and stress.

- Check Your Credit Score & Report: Before anything else, get a clear picture of your credit health. This helps you anticipate the rates you might qualify for and identify any errors to dispute.

- Determine Your Budget: Figure out how much you can realistically afford for a monthly car payment, including insurance, fuel, and maintenance. Don’t just focus on the loan amount.

- Get Pre-Approved: This is a crucial step. Apply for pre-approval with Navy Federal. This process will give you a firm understanding of the maximum loan amount you qualify for and your actual interest rate. Pre-approval gives you bargaining power at the dealership, as you know your financing is already secured.

- What is Pre-Approval? It’s a conditional offer of credit based on your financial information. It’s not a commitment to buy a specific car, but it shows you’re a serious buyer with financing ready.

- Gather Required Documents: Be prepared with identification (driver’s license), proof of income (pay stubs, W-2s), and possibly proof of residence. If you’re trading in a car, have its title or loan information ready.

- Shop for Your Car: With your pre-approval in hand, you can confidently shop for your new vehicle, knowing your budget and financing terms.

- Finalize the Loan: Once you’ve chosen your car, NFCU will finalize the loan. This often involves submitting the vehicle’s information (VIN, purchase price) and signing the loan documents.

Maximizing Your Chances for the Best Rates (Pro Strategies)

Achieving the lowest possible Navy Federal new car loan interest rates requires a strategic approach. Here are our pro strategies:

- Improve Your Credit Score Before Applying: This cannot be stressed enough. Dedicate a few months to improving your credit if it’s not excellent. Pay down debts, dispute errors, and make all payments on time. Even a 20-point increase can make a difference. For more in-depth advice, check out . (Internal Link Example)

- Save for a Larger Down Payment: The more you put down, the less you borrow, and the lower the risk for NFCU. This often translates directly into better rates. Consider delaying your purchase for a few months to save up more.

- Consider a Shorter Loan Term You Can Comfortably Afford: While longer terms mean lower monthly payments, they come with higher overall costs and interest rates. Crunch the numbers to see if you can manage a 48 or 60-month term instead of 72 or 84.

- Leverage NFCU Membership Benefits: Ensure all your banking activities are in good standing with Navy Federal. Inquire about any specific rate discounts for loyal members or those who use direct deposit.

- Shop Around (Even If You Love NFCU): While NFCU is highly competitive, it’s always wise to compare their offer with at least one or two other lenders (local credit unions, banks, or even manufacturer financing). This ensures you’re getting the absolute best deal available to you. Having multiple offers can also give you leverage.

- Negotiate with the Dealer After Securing Financing: Common mistakes to avoid are discussing your financing with the dealer before you’ve negotiated the car price. Secure your best possible price on the vehicle first, then present your pre-approved NFCU financing. This separates the two transactions, preventing dealers from manipulating numbers.

Common Pitfalls to Avoid When Getting a Car Loan

Even with the best intentions, car buyers can fall into common traps. Being aware of these can save you money and headaches.

- Not Checking Your Credit Report: Blindly applying for a loan without reviewing your credit report is a significant mistake. You might miss errors that are dragging down your score or be surprised by your score itself. Always get your free annual reports from AnnualCreditReport.com. (External Link Example)

- Falling for Dealer Financing Traps: While some dealers offer competitive financing, others may try to steer you towards higher-interest loans, especially if you haven’t secured outside financing. Never let them "run your credit" multiple times without clear consent and understanding.

- Borrowing More Than You Need: It’s easy to get caught up in the excitement of a new car and add on expensive extras or extended warranties to your loan. These additions increase your total loan amount and, consequently, the total interest paid.

- Ignoring the Total Cost of Ownership: Beyond the monthly car payment, remember to factor in insurance, fuel, maintenance, and registration fees. A low monthly payment might seem attractive, but the overall cost of the car could still strain your budget.

- Not Understanding All Loan Terms: Always read the fine print. Understand the APR, any prepayment penalties, late fees, and what happens if you miss a payment. Don’t sign anything you don’t fully comprehend. For more details on loan terms, see . (Internal Link Example)

Comparing Navy Federal to Other Lenders

While this article focuses on Navy Federal, it’s beneficial to understand their position in the broader lending landscape.

- Traditional Banks: Large banks often have broad reach and competitive rates for top-tier credit but may lack the personalized service or specific military benefits of NFCU.

- Other Credit Unions: Like NFCU, other credit unions are member-owned and often provide excellent rates and service. However, they might not have the same military focus or widespread branch network.

- Manufacturer Financing: Car manufacturers sometimes offer very low (even 0%) APR deals. These are usually limited to specific models, require excellent credit, and might mean foregoing other incentives (like cash rebates). Always compare the total savings.

Navy Federal’s competitive edge for its members lies in its combination of excellent rates, flexible terms, and a deep understanding of the military lifestyle. Their pre-approval process is robust, giving members a strong position when negotiating with dealerships. For many, the peace of mind and trusted relationship with NFCU outweigh potential marginal rate differences from other lenders.

Conclusion: Driving Away with Confidence

Securing a new car loan with the best possible interest rate from Navy Federal Credit Union is entirely achievable with the right knowledge and preparation. By understanding the factors that influence your rates – primarily your credit score, loan term, and down payment – you can take proactive steps to optimize your financial profile.

Remember, NFCU offers more than just competitive rates; they provide a valuable partnership for military members and their families. Their commitment to service and member benefits makes them a standout choice for new car financing.

Don’t rush the process. Take the time to improve your credit, save for a down payment, get pre-approved, and compare offers. By following the strategies outlined in this guide, you can confidently navigate the car buying process, secure favorable Navy Federal new car loan interest rates, and drive away knowing you’ve made a smart financial decision. Your dream car awaits, backed by the strength and support of Navy Federal.