Decoding SBI Car Loan Interest Rates: Your Ultimate Guide to Driving Home Your Dream Car

Decoding SBI Car Loan Interest Rates: Your Ultimate Guide to Driving Home Your Dream Car Carloan.Guidemechanic.com

The dream of owning a car is a common aspiration for many, offering unparalleled freedom and convenience. However, turning that dream into a reality often involves navigating the world of car loans. Among the myriad of financial institutions, the State Bank of India (SBI) stands out as a reliable and popular choice, trusted by millions across the nation. Understanding the intricacies of SBI Car Loan Interest Rates is paramount to making an informed financial decision.

This comprehensive guide is designed to be your one-stop resource, delving deep into every facet of SBI car loans, with a particular focus on their interest rates. We’ll explore not just the numbers, but also the factors influencing them, the types of loans available, the application process, and crucial tips to secure the best deal. Our goal is to equip you with the knowledge needed to confidently apply for an SBI car loan, ensuring a smooth journey to your new vehicle.

Decoding SBI Car Loan Interest Rates: Your Ultimate Guide to Driving Home Your Dream Car

Understanding SBI Car Loans: More Than Just Interest Rates

SBI, India’s largest public sector bank, offers a diverse range of car loan products tailored to meet various customer needs. Their offerings go beyond simply financing a vehicle; they aim to provide a holistic solution that considers different budgets, vehicle types, and financial profiles. This extensive reach and customer-centric approach have made SBI a preferred financier for many car buyers.

While the interest rate is undeniably a significant factor, it’s essential to view the entire loan package. This includes processing fees, repayment tenure options, eligibility criteria, and the overall transparency of the process. A seemingly low interest rate might come with hidden charges or rigid terms, which is why a thorough understanding of all components is crucial.

Decoding SBI Car Loan Interest Rates: What You Need to Know

The interest rate is the cost you pay for borrowing money, expressed as a percentage of the principal amount. For an SBI car loan, this rate directly impacts your Equated Monthly Installment (EMI) and the total cost of your loan over its tenure. A lower interest rate translates to lower EMIs and less money paid back to the bank in the long run.

However, the "SBI Car Loan Interest Rate" isn’t a single, static figure. It’s a dynamic variable influenced by several internal and external factors. Understanding these elements will empower you to potentially secure a more favorable rate and plan your finances effectively.

Factors Influencing SBI Car Loan Interest Rates

Several key elements come into play when SBI determines the interest rate for your car loan. Being aware of these can help you optimize your application.

Credit Score (CIBIL)

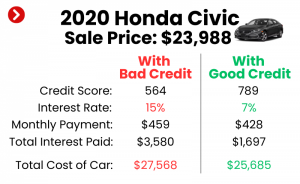

Your credit score, particularly your CIBIL score in India, is perhaps the most critical factor. It’s a three-digit number that reflects your creditworthiness based on your past repayment behavior. A higher CIBIL score (generally above 750) signals to the bank that you are a responsible borrower.

Based on my experience, banks, including SBI, view applicants with excellent credit scores as lower risk. This often translates into more attractive interest rates and better loan terms. Conversely, a low credit score might lead to a higher interest rate or even loan rejection, as the bank perceives a greater risk of default.

Loan Amount and Tenure

The amount you wish to borrow and the chosen repayment period also influence the interest rate. While it might seem counterintuitive, sometimes opting for a slightly shorter tenure, if financially feasible, can lead to better rates. Banks often prefer loans that are repaid within a reasonable timeframe.

However, a longer tenure reduces your monthly EMI, making the loan more affordable on a day-to-day basis. It’s a delicate balance between managing monthly outflows and minimizing the total interest paid. Pro tip from us: Use an EMI calculator to compare different loan amounts and tenures to find your sweet spot.

Vehicle Type (New vs. Used, Electric vs. Petrol/Diesel)

The type of vehicle you intend to purchase significantly impacts the interest rate. New car loans typically attract lower interest rates compared to used car loans. This is because new cars have a higher resale value and are considered less risky collateral by the bank.

Furthermore, SBI has been proactive in promoting green mobility. Their "SBI Green Car Loan" for electric vehicles (EVs) often comes with preferential interest rates, making them an attractive option for environmentally conscious buyers. This initiative not only supports sustainable living but also provides a financial incentive.

Applicant’s Relationship with SBI

If you are an existing customer with SBI, maintaining a good relationship can work in your favor. This might include having a salary account, a long-standing savings account, or other loan products with the bank. Banks often offer special concessions or slightly lower interest rates to their loyal customers.

This relationship provides the bank with a clear track record of your financial dealings, building trust and potentially leading to better terms. It’s always a good idea to inquire about any loyalty benefits if you’re an existing SBI account holder.

Market Conditions / Repo Rate

External economic factors, particularly the Reserve Bank of India’s (RBI) Repo Rate, play a crucial role. The Repo Rate is the rate at which commercial banks borrow money from the RBI. Changes in this rate directly influence the lending rates of banks across the country.

When the Repo Rate decreases, banks may pass on the benefit to customers by lowering their interest rates, and vice versa. Therefore, the prevailing economic climate and RBI’s monetary policies can indirectly affect the SBI Car Loan Interest Rate you receive.

Special Schemes/Promotions

From time to time, SBI introduces special schemes, promotional offers, or festival discounts on car loans. These offers might include reduced interest rates, waived processing fees, or extended repayment periods. Such promotions are often seasonal or tied to specific events.

Keeping an eye on SBI’s official announcements and visiting their website or a local branch can help you capitalize on these limited-time opportunities. These schemes can provide significant savings on the overall cost of your car loan.

Types of SBI Car Loans and Their Interest Rate Implications

SBI offers a variety of car loan products, each designed for a specific segment of borrowers and vehicle types. Understanding these different options is crucial as their interest rates can vary.

SBI New Car Loan (e.g., SBI Car Loan Scheme)

This is the most common type, designed for purchasing brand-new passenger cars, multi-utility vehicles (MUVs), and SUVs. These loans generally offer the most competitive interest rates due to the lower depreciation risk associated with new vehicles. The repayment tenure can be quite flexible, often extending up to 7 years.

SBI Used Car Loan (e.g., SBI Loyalty Car Loan)

For those looking to buy a pre-owned vehicle, SBI offers specific used car loan products. The interest rates for used car loans are typically slightly higher than those for new cars. This is primarily because used cars have already undergone some depreciation, and their future resale value is harder to ascertain. The maximum age of the used car at the time of loan sanction and the maximum repayment tenure might also be restricted.

SBI Green Car Loan

As mentioned earlier, the SBI Green Car Loan is a special initiative for financing electric vehicles. This loan category often features preferential interest rates, making EVs more affordable and encouraging their adoption. This is a fantastic option if you’re considering an eco-friendly mode of transport, as it comes with both environmental and financial benefits.

Car Loan for Government/Defense Personnel

SBI frequently offers special schemes and slightly lower interest rates for government employees, including those in central, state, and public sector undertakings, as well as defense personnel. These schemes recognize the stable employment and financial discipline typically associated with these professions. If you fall into this category, it’s definitely worth inquiring about specific benefits.

Current SBI Car Loan Interest Rates: A Snapshot (Illustrative)

It’s crucial to understand that SBI Car Loan Interest Rates are dynamic and subject to change based on market conditions and internal bank policies. While we provide an illustrative overview here, always refer to the official SBI website or visit your nearest branch for the most current and accurate rates.

Generally, SBI Car Loan Interest Rates for new cars might start from around 8.70% per annum and go upwards, depending on the applicant’s profile and loan specifics. For SBI Green Car Loans, you might find rates that are slightly lower, perhaps starting from 8.60% per annum, reflecting the bank’s push for sustainable transport. Used car loans typically have rates that are 0.5% to 1% higher than new car loans, starting from around 9.20% per annum.

These figures are indicative and designed to give you a general idea. The final rate offered to you will depend on a thorough assessment of your eligibility, credit score, and the specific loan product you choose. Pro tip: Always check the official SBI website for the latest interest rates and any ongoing promotional offers before applying.

Eligibility Criteria for SBI Car Loan: Are You Ready?

Before you even consider the interest rates, it’s vital to ensure you meet SBI’s eligibility criteria. These requirements are in place to ensure that borrowers have the financial capacity to repay the loan.

Age

Applicants typically need to be between 21 and 67 years of age. The maximum age ensures that the loan can be repaid comfortably within the individual’s active earning years.

Income (Salaried, Self-Employed, Professionals, Agriculturists)

SBI caters to a wide range of income groups.

- Salaried Individuals: You generally need a minimum net annual income of ₹3 lakh. This includes salary, allowances, and any other regular income. You’ll need to provide salary slips and bank statements as proof.

- Self-Employed Individuals/Professionals: Minimum net profit of ₹3 lakh per annum (as per IT Returns) is usually required. Income tax returns for the past two years are essential documentation.

- Agriculturists: A minimum net annual income of ₹4 lakh (including income of co-applicant) is typically needed. Proof of land holding and agricultural income records will be required.

Common mistake to avoid: Many applicants underestimate the importance of consistent and verifiable income proof. Ensure all your financial records are up-to-date and easily accessible.

Credit Score

As discussed, a good credit score is crucial. SBI will assess your credit history to determine your repayment capability and reliability. A score above 750 is generally considered excellent and can open doors to better rates.

Residency Status

Applicants must be Indian residents. Non-Resident Indians (NRIs) might have specific schemes available, but the primary offerings are for resident Indians.

Essential Documents for Your SBI Car Loan Application

Gathering all necessary documents beforehand can significantly streamline your application process. Missing papers are a common cause of delays.

- Identity Proof: Passport, PAN Card, Voter ID, Driving License.

- Address Proof: Passport, Voter ID, Driving License, Utility Bills (electricity, telephone), Ration Card.

- Income Proof:

- Salaried: Latest 3 months’ salary slips, Form 16, latest 2 years’ Income Tax Returns (ITR).

- Self-Employed/Professionals: Latest 2 years’ IT Returns, Audited Balance Sheet, Profit & Loss statements.

- Agriculturists: Land holding statement, income proof from agricultural activities.

- Bank Statements: Last 6 months’ bank statements for all active accounts.

- Vehicle Quotation: Proforma invoice or quotation from the car dealer for the vehicle you intend to purchase.

- Photograph: Recent passport-sized photographs.

Pro tip: Organize all your documents in a file, making sure they are clear and valid. This simple step can save you a lot of hassle and speed up the approval process.

The SBI Car Loan Application Process: A Step-by-Step Guide

Applying for an SBI car loan is a straightforward process, whether you prefer digital or traditional methods.

- Enquiry and Research: Start by visiting the SBI official website or a branch to understand the latest interest rates and schemes. Use their online EMI calculator to estimate your monthly payments.

- Eligibility Check: Self-assess your eligibility based on the criteria mentioned above. This helps you understand your chances of approval.

- Application Submission:

- Online: You can apply online through the SBI website or YONO app. This is convenient and allows you to upload documents digitally.

- Branch Visit: Alternatively, visit your nearest SBI branch, fill out the application form, and submit your documents in person.

- Document Verification: SBI will review all submitted documents. They might contact you for further clarification or additional papers if required.

- Credit Appraisal: The bank will assess your creditworthiness, including your credit score and financial history.

- Loan Sanction: If all criteria are met and your application is approved, SBI will issue a sanction letter detailing the loan amount, interest rate, tenure, and terms and conditions.

- Disbursement: Once you accept the terms and complete any final formalities (like hypothecation of the vehicle), the loan amount will be disbursed directly to the car dealer.

Based on my experience, having all your documents ready and accurate significantly speeds up the verification and approval stages. Pre-approvals, if offered by SBI based on your existing relationship, can also expedite the process.

Beyond Interest Rates: Other Costs to Consider

While the SBI Car Loan Interest Rate is crucial, it’s not the only financial aspect to consider. Several other costs contribute to the overall expense of your loan. Overlooking these can lead to unexpected financial burdens.

Processing Fees

SBI, like other lenders, charges a processing fee for evaluating your loan application. This is a one-time fee and can vary based on the loan amount or specific promotions. Always inquire about the exact processing fee upfront.

Pre-payment/Foreclosure Charges

If you decide to repay your loan earlier than the agreed tenure, some banks levy pre-payment or foreclosure charges. These charges are a percentage of the outstanding loan amount. Common mistake to avoid: Many borrowers don’t consider these charges when planning to clear their loan early, leading to unexpected costs. Always check SBI’s policy on pre-payment before signing the loan agreement.

Late Payment Penalties

Missing an EMI payment or delaying it beyond the due date will attract late payment penalties. These charges can be substantial and can also negatively impact your credit score. It’s always best to set up auto-debit for your EMIs to avoid such penalties.

Stamp Duty/Other Statutory Charges

Depending on your state, there might be stamp duty or other statutory charges applicable to your loan agreement. These are government-mandmandated fees and are typically a small percentage of the loan amount.

Insurance Costs (Mandatory)

While not directly part of the loan interest, comprehensive motor insurance is mandatory for any new vehicle and must be renewed annually. This is an ongoing cost associated with car ownership that borrowers must factor into their budget. While SBI might offer insurance products, you are generally free to choose your preferred insurer.

Strategies to Secure the Best SBI Car Loan Interest Rate

Getting a car loan is a significant financial commitment. Employing smart strategies can help you secure the most favorable SBI Car Loan Interest Rate possible.

- Maintain a High CIBIL Score: This is your strongest asset. Regularly check your credit report for errors and ensure timely repayment of all existing debts.

- Choose a Shorter Tenure (If Affordable): While a longer tenure reduces EMIs, a shorter one often results in lower total interest paid and can sometimes lead to slightly better interest rates from the bank’s perspective of reduced risk.

- Opt for a Higher Down Payment: Putting down a larger sum upfront reduces the loan amount, which in turn reduces the bank’s risk. This can sometimes lead to a more attractive interest rate.

- Consider the SBI Green Car Loan: If you’re open to an electric vehicle, leverage the lower interest rates and other benefits associated with SBI’s green initiatives.

- Negotiate (Especially for Existing Customers): If you have a strong banking relationship with SBI, don’t hesitate to inquire if there’s any flexibility on the offered interest rate.

- Compare Offers: While this article focuses on SBI, it’s always wise to compare SBI’s rates with those of other banks and NBFCs to ensure you’re getting a competitive deal.

Pro tip: Don’t just look at the EMI; consider the total cost of the loan over its entire tenure, including all fees and charges. A slightly higher EMI with a lower interest rate and fewer fees might be cheaper in the long run.

SBI Car Loan EMI Calculator: Your Financial Planning Tool

The SBI Car Loan EMI Calculator is an invaluable tool for any prospective borrower. It helps you understand your monthly financial commitment before you even apply for the loan.

This online tool requires you to input three key variables:

- Principal Loan Amount: The total amount you wish to borrow.

- Interest Rate: The estimated SBI Car Loan Interest Rate.

- Loan Tenure: The number of months or years over which you plan to repay the loan.

By adjusting these variables, you can instantly see how your EMI changes. This allows you to plan your budget effectively and choose a loan amount and tenure that aligns with your financial capabilities. For a deeper dive into managing your monthly finances, check out our guide on .

Why Choose SBI for Your Car Loan? Unpacking the Benefits

Beyond competitive interest rates, SBI offers several compelling reasons to consider them for your car loan needs.

- Trusted Brand: As a public sector behemoth, SBI carries immense trust and reliability, offering peace of mind to borrowers.

- Competitive Interest Rates: SBI consistently offers competitive SBI Car Loan Interest Rates, often among the best in the market, especially for well-qualified applicants.

- Flexible Repayment Options: With varying tenures and customization options, SBI aims to provide flexible repayment solutions.

- Wide Branch Network: With an extensive network of branches across India, physical assistance and support are always within reach.

- Transparent Process: SBI is known for its transparent loan application and disbursement process, with clear terms and conditions.

- Dedicated Customer Service: The bank provides robust customer service to address queries and provide assistance throughout the loan lifecycle.

Considering other options? Our article on might offer valuable insights into making the best choice for your specific situation.

Common Mistakes to Avoid When Applying for an SBI Car Loan

Even with all the information, it’s easy to make common mistakes that can impact your loan experience.

- Not Checking Your Credit Score: A low score can lead to higher rates or rejection. Always review it before applying.

- Ignoring Hidden Charges: Focus solely on the interest rate and forget processing fees, pre-payment penalties, and other charges.

- Applying for Too Much Loan: Borrowing more than you can comfortably repay can lead to financial strain and potential defaults.

- Not Reading the Fine Print: Always read the loan agreement thoroughly, understanding all terms and conditions, especially those related to interest rate changes and foreclosure.

- Overlooking Eligibility Criteria: Applying without meeting the basic eligibility requirements wastes time and can negatively impact your credit inquiry history.

Based on my experience, many applicants get caught out by pre-payment clauses or fail to understand how interest is calculated on a reducing balance basis. Always ask questions if anything is unclear.

Frequently Asked Questions (FAQs) about SBI Car Loans

To further clarify common concerns, here are answers to some frequently asked questions regarding SBI car loans:

Q1: Can I get an SBI car loan for a used car?

A1: Yes, SBI offers specific schemes for used cars. The eligibility criteria and interest rates might differ slightly from new car loans.

Q2: What is the maximum tenure for an SBI car loan?

A2: For new car loans, the maximum repayment tenure is typically up to 7 years (84 months). For used cars, it might be slightly shorter.

Q3: Can I pre-pay my SBI car loan?

A3: Yes, SBI generally allows pre-payment of car loans. However, it’s crucial to check if any pre-payment or foreclosure charges apply as per your loan agreement.

Q4: How long does it take for SBI car loan approval?

A4: The approval time can vary. If all documents are in order and your profile is strong, approval can sometimes be as quick as a few days. However, it can take up to a week or more in some cases, especially if additional verification is required.

Q5: Is a guarantor required for an SBI car loan?

A5: Generally, a guarantor is not mandatory for an SBI car loan, especially for salaried individuals with a good credit score and stable income. However, in certain cases, based on the applicant’s profile or loan amount, SBI might request one.

Conclusion

Navigating the landscape of car loans can seem daunting, but with a clear understanding of SBI Car Loan Interest Rates and the associated terms, you can make a financially sound decision. SBI offers a robust and customer-friendly car loan portfolio, making it an excellent choice for many aspiring car owners. By being aware of the factors influencing interest rates, meticulously preparing your documents, and understanding all associated costs, you are well-positioned to secure a favorable loan.

Remember, the key to a successful car loan journey lies in informed decision-making. Don’t hesitate to visit the official SBI website or consult with their loan officers for the most up-to-date information and personalized guidance. Your dream car is within reach, and with SBI, you can drive towards it with confidence.