Decoding Schwab Car Loan Rates: Your Ultimate Guide to Smart Car Financing

Decoding Schwab Car Loan Rates: Your Ultimate Guide to Smart Car Financing Carloan.Guidemechanic.com

The dream of a new car often comes with the practical reality of financing. Many aspiring car owners, seeking the best rates and trusted financial partners, naturally wonder about "Schwab Car Loan Rates." Charles Schwab is a household name in financial services, synonymous with investing, wealth management, and brokerage accounts. But when it comes to direct auto loans, the picture isn’t quite what many expect.

This comprehensive guide will demystify the relationship between Schwab and car financing. We’ll explore why Schwab isn’t a traditional car loan provider, yet how their extensive financial ecosystem can be an incredibly powerful ally in securing your dream car – and doing so on your own terms. Prepare to dive deep into strategies for smart car buying, leveraging financial planning, and understanding the true path to optimal auto loan rates.

Decoding Schwab Car Loan Rates: Your Ultimate Guide to Smart Car Financing

The Truth About Schwab and Direct Car Loans

Let’s address the elephant in the room right away: Charles Schwab primarily operates as a brokerage and wealth management firm. They are renowned for their investment platforms, retirement planning services, and financial advisory expertise. Their core business revolves around helping individuals and institutions grow and manage their wealth through various investment vehicles.

Based on my experience, many people mistakenly assume that a large, reputable financial institution like Schwab would offer every conceivable banking product, including direct auto loans. However, unlike traditional banks or credit unions, Schwab’s business model is not centered on consumer lending for specific assets like cars or homes in the conventional sense. This means you won’t find a dedicated "Schwab Car Loan" application form on their website or specific advertised rates for auto financing directly from them.

Their focus is on empowering clients through investment and financial planning, which, as we’ll soon discover, can indirectly lead to a much stronger position when seeking car financing elsewhere. Understanding this distinction is the first crucial step in leveraging Schwab’s strengths for your car buying journey.

How Schwab Can Still Empower Your Car Purchase

While Schwab doesn’t offer direct car loans, their services provide a robust foundation for strategic car financing. By utilizing their investment platforms and financial planning tools, you can put yourself in an advantageous position to secure better rates from other lenders or even finance your vehicle in alternative, often more flexible, ways.

Strategic Savings and Investment for a Down Payment

One of the most impactful ways to lower your car loan rate and overall cost is to make a substantial down payment. A larger down payment reduces the amount you need to borrow, thereby decreasing the lender’s risk and often translating into more favorable interest rates. This is where Schwab’s investment accounts shine.

You can leverage various Schwab accounts to accumulate funds for your down payment. A Schwab brokerage account, for instance, offers a wide range of investment options, from low-risk money market funds for short-term savings to diversified portfolios for longer-term growth. Even their Schwab Bank Investor Checking Account or High-Yield Investor Savings account can be excellent places to park funds earmarked for a car.

Pro tips from us: For a down payment needed within the next 1-2 years, consider lower-volatility investments like short-term bond funds or high-yield savings accounts within your Schwab ecosystem. If your car purchase is further out (3-5+ years), you might explore a more balanced portfolio with a mix of equities and fixed income to potentially grow your capital more aggressively. Disciplined saving and smart investment within Schwab’s platform can significantly reduce your borrowing needs.

Leveraging Existing Assets: Pledged Asset Lines or Portfolio Loans

For established Schwab clients with substantial investment portfolios, a Pledged Asset Line (PAL) or portfolio loan can be an intriguing alternative to a traditional car loan. This allows you to borrow money using your non-retirement investment portfolio as collateral, without having to sell your holdings. It’s essentially a flexible line of credit against your investments.

The benefits can be significant. Often, the interest rates on PALs can be lower than those of conventional unsecured personal loans or even some auto loans, especially for well-qualified borrowers. You maintain ownership of your investments, which can continue to grow, and the application process can be much quicker and simpler than a traditional loan. Plus, there are typically no fixed repayment schedules, offering greater flexibility.

However, common mistakes to avoid are overleveraging and not understanding the risks. If the market experiences a significant downturn, the value of your collateral could drop, leading to a margin call where you’d need to deposit more funds or sell off assets. Based on my experience, it’s crucial to use PALs cautiously and ensure you have a clear repayment strategy to avoid potential financial strain. Always consult with a Schwab financial advisor to understand if this option aligns with your overall financial goals and risk tolerance.

Financial Planning and Advisory Services

Schwab’s strength lies in holistic financial planning. Their financial advisors can help you integrate a car purchase into your broader financial picture, rather than viewing it as an isolated transaction. This includes evaluating how a car loan fits into your budget, assessing its impact on your savings goals, and exploring strategies to pay it off efficiently.

An advisor can help you analyze the total cost of ownership for different vehicles, factoring in not just the loan payments but also insurance, maintenance, and depreciation. They can guide you on setting realistic down payment goals, optimizing your investment strategy to reach those goals, and even helping you understand the long-term implications of various financing options. This expert guidance can be invaluable in making a financially sound decision.

Understanding Traditional Car Loan Avenues (When Schwab Isn’t Direct)

Since Schwab doesn’t offer direct car loans, you’ll likely turn to traditional lenders. Knowing your options and how to navigate them is key to securing the best rates.

Banks and Credit Unions

Traditional banks and credit unions are primary sources for auto loans. Credit unions, in particular, often offer competitive rates because they are member-owned non-profit organizations. It’s always a good idea to check with your existing bank or credit union first, as they might offer preferred rates to loyal customers.

When comparing offers, look beyond just the interest rate. Consider the loan term, any origination fees, prepayment penalties, and the overall customer service. A slightly higher rate with excellent service and no hidden fees might be preferable to a rock-bottom rate with rigid terms.

Dealership Financing

Dealerships often offer financing options directly or through partnerships with various lenders. This can be convenient, allowing you to complete the car purchase and financing in one place. Dealerships might also offer special promotions, such as 0% APR deals, though these are typically reserved for buyers with excellent credit on specific new models.

However, based on my experience, dealership financing isn’t always the most cost-effective. While convenient, the rates might be higher than what you could secure independently. It’s always best to arrive at the dealership with a pre-approved loan offer from another lender. This gives you a strong negotiating position and ensures you have a benchmark against which to compare their offer.

Online Lenders

The digital age has brought a surge of online lenders specializing in auto loans. Companies like Capital One Auto Finance, LightStream, or Carvana Financing often provide quick approval processes and competitive rates, as they have lower overhead costs than traditional brick-and-mortar institutions.

The primary benefit of online lenders is the speed and ease of application. You can often get pre-approved within minutes, comparing multiple offers from the comfort of your home. However, it’s crucial to thoroughly vet any online lender, checking their reputation, reviews, and ensuring they are legitimate. Always read the fine print before committing to any loan offer.

Key Factors Influencing Car Loan Rates (Regardless of Lender)

Regardless of where you seek your car loan, several critical factors will determine the interest rate you’re offered. Understanding these elements empowers you to take steps to secure the most favorable terms.

Credit Score

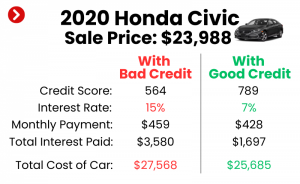

Your credit score is arguably the most significant factor influencing your car loan rate. Lenders use your credit score as a primary indicator of your creditworthiness and your likelihood of repaying the loan. A higher credit score (generally 700 and above) signals lower risk to lenders, which typically translates into lower interest rates.

Conversely, a lower credit score will result in higher interest rates, as lenders perceive a greater risk of default. It’s wise to check your credit score and report well before applying for a car loan. If your score isn’t ideal, dedicate time to improving it by paying bills on time, reducing existing debt, and correcting any errors on your credit report.

Loan Term and Amount

The length of your loan (the term) and the amount you borrow also play a crucial role. Longer loan terms (e.g., 72 or 84 months) typically result in lower monthly payments, but you’ll pay significantly more in total interest over the life of the loan. Shorter terms (e.g., 36 or 48 months) mean higher monthly payments but substantially less interest paid overall.

The loan amount directly impacts your monthly payment and total interest. The less you need to borrow, the lower your payments and the less interest you’ll accrue. This reinforces the importance of a strong down payment, as it directly reduces the principal loan amount.

Down Payment

We’ve touched on this, but it bears repeating: a substantial down payment is a powerful tool. Lenders view a larger down payment as a sign of your commitment and reduces their risk. It also means you’re financing a smaller portion of the car’s value, which can lead to better rates.

Common mistakes to avoid are stretching your budget too thin for a minimal down payment. Aim for at least 10-20% of the car’s purchase price, if possible. For used cars, a larger down payment is even more critical as they depreciate faster.

Interest Rate Type (Fixed vs. Variable)

Most car loans come with a fixed interest rate, meaning your interest rate and monthly payment remain the same for the entire loan term. This provides stability and predictability, making budgeting easier.

Variable interest rates, while less common for traditional auto loans, can fluctuate based on a benchmark interest rate. While they might start lower, they carry the risk of increasing, leading to higher monthly payments. For the vast majority of car buyers, a fixed-rate loan is the safer and more advisable choice.

Strategies for Securing the Best Car Loan Rates

Armed with knowledge about Schwab’s role and the factors influencing rates, here are actionable strategies to ensure you get the best possible deal on your car loan.

Get Pre-Approved

This is a golden rule for car buying. Getting pre-approved for a loan before you step onto the dealership lot gives you immense power. It means you know exactly how much you can borrow, at what interest rate, and what your monthly payments will be.

With a pre-approval in hand, you become a cash buyer in the eyes of the dealership, shifting the focus to negotiating the car’s price, not the financing. If the dealership can beat your pre-approved rate, fantastic! If not, you already have a great offer ready to go.

Improve Your Financial Health

Beyond your credit score, a lender will look at your overall financial health. This includes your debt-to-income ratio, employment history, and stability. Before applying for a loan, try to pay down other high-interest debts, especially credit card balances.

Ensure your income is stable and verifiable. The stronger your financial profile, the more attractive you appear to lenders, and the better the rates you’ll be offered. A robust financial foundation, often built with Schwab’s investment and planning tools, is your best asset.

Research and Comparison

Never settle for the first loan offer you receive. Based on my experience, diligence in researching and comparing multiple lenders can save you thousands of dollars over the life of the loan. Get quotes from several banks, credit unions, and online lenders.

Pro tip from us: Use online comparison tools that allow you to input your details and receive multiple offers without impacting your credit score significantly (if done within a short shopping window). This makes the comparison process efficient and effective.

Negotiation Skills

When it comes to the dealership, separate the car price negotiation from the financing negotiation. First, agree on the vehicle’s price. Only then should you discuss financing options. This prevents the dealership from "packing" the loan or shifting numbers around to make it seem like you’re getting a good deal on both when you might not be.

Be firm, informed, and ready to walk away if the offer isn’t right. Remember, you have your pre-approved loan as leverage.

The Schwab Advantage: A Holistic Approach to Car Ownership

While Schwab might not be your direct lender for a car loan, their true advantage lies in fostering a holistic approach to your financial well-being. By utilizing Schwab’s investment platforms, financial planning resources, and advisory services, you are building a stronger financial foundation that benefits every major purchase, including a car.

This means strategically saving for a down payment, potentially leveraging existing assets responsibly, and ensuring your car purchase aligns with your broader financial goals like retirement, homeownership, or education. Schwab empowers you to become a more financially savvy consumer, capable of securing the best possible terms from any lender, because you’ve prepared for it. It’s about long-term wealth building and intelligent money management, which inherently leads to better outcomes for short-term needs like car financing.

Conclusion

When considering "Schwab Car Loan Rates," it’s essential to understand that Charles Schwab’s role in your car buying journey is more strategic than direct. While they don’t offer traditional auto loans, their robust suite of investment and financial planning services provides an unparalleled advantage. By leveraging Schwab for strategic savings, potentially utilizing pledged asset lines, and benefiting from expert financial advice, you can position yourself to secure the most competitive car loan rates from other lenders.

Remember, the path to a great car loan rate begins long before you step into a dealership. It starts with a strong credit score, a healthy down payment, and a well-thought-out financial plan – all areas where Schwab excels. So, while you won’t find a direct "Schwab Car Loan," you’ll discover that Schwab can be your most powerful partner in making your car ownership dreams a financially sound reality. Start planning today, invest wisely, and drive away with confidence.

Further Reading:

- How to Build an Emergency Fund with Schwab (Internal Link Placeholder)

- Understanding Investment Risk: A Beginner’s Guide (Internal Link Placeholder)

- Understanding Your Credit Score – Consumer Financial Protection Bureau (External Link)