Decoding the 18 Percent Car Loan: A Comprehensive Guide to Understanding, Mitigating, and Avoiding High Interest Rates

Decoding the 18 Percent Car Loan: A Comprehensive Guide to Understanding, Mitigating, and Avoiding High Interest Rates Carloan.Guidemechanic.com

Finding yourself staring at an 18 percent interest rate on a car loan can feel like a punch to the gut. It’s a number that immediately raises red flags for most consumers, and for good reason. While the allure of a new (or new-to-you) vehicle can be strong, signing on the dotted line for such a high interest rate can have profound and long-lasting financial consequences.

This isn’t just a number; it’s a significant financial burden that can dramatically inflate the total cost of your vehicle. As an expert blogger and professional SEO content writer, I’ve seen countless individuals struggle with the implications of high-interest loans. My mission with this comprehensive guide is to demystify what an 18 percent interest rate on a car loan truly means, explore why you might be offered such a rate, and, most importantly, provide actionable strategies to mitigate its impact and avoid similar situations in the future.

Decoding the 18 Percent Car Loan: A Comprehensive Guide to Understanding, Mitigating, and Avoiding High Interest Rates

We’ll dive deep into the mechanics of high-interest loans, uncover the underlying causes, and equip you with the knowledge to navigate this challenging financial landscape. Our goal is to empower you with information, ensuring you make informed decisions that protect your financial well-being.

Understanding What 18 Percent Interest Truly Means for Your Car Loan

When you see an 18 percent interest rate, it’s often referring to the Annual Percentage Rate (APR). The APR is a broader measure of the cost of borrowing money, including not just the interest rate but also other charges like origination fees, though these are less common with car loans compared to mortgages or personal loans. For a car loan, it primarily reflects the interest you’ll pay on the principal balance over a year.

An 18% APR means that for every $100 you borrow, you’ll pay $18 in interest annually, assuming a simple interest calculation. However, car loans typically use amortized payments, meaning a portion of each payment goes towards interest and a portion towards the principal. Early in the loan term, a larger share of your payment covers interest, which is why a high rate has such a significant impact.

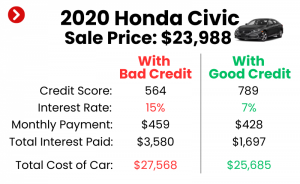

To put this into perspective, let’s consider a $25,000 car loan over 60 months (5 years).

- At a 5% APR, your estimated monthly payment would be around $472, and the total interest paid would be approximately $3,320.

- At an 18% APR, your estimated monthly payment skyrockets to about $634, and the total interest paid would be a staggering $13,040.

This simple comparison highlights a critical point: an 18 percent interest rate doesn’t just mean slightly higher payments; it means paying thousands of dollars more for the exact same vehicle. The car you intended to buy for $25,000 could effectively cost you over $38,000 once all interest is accounted for. This dramatically alters the true value proposition of your purchase.

Why Are You Facing an 18 Percent Interest Rate? Common Causes Explored

An 18 percent interest rate is significantly higher than the average for car loans, which typically hover in the single digits for borrowers with good credit. When a lender offers such a high rate, it’s usually a direct reflection of perceived risk. Understanding these underlying reasons is the first step toward addressing the issue.

Poor Credit Score

This is by far the most common reason. Your credit score, calculated by bureaus like Experian, Equifax, and TransUnion, is a numerical representation of your creditworthiness. Scores typically range from 300 to 850, with anything below 670 generally considered "fair" or "poor." Lenders use this score to assess the likelihood of you repaying your loan. A low score signals a higher risk of default, and lenders compensate for this risk by charging higher interest rates.

Limited Credit History

Even if you’ve never missed a payment in your life, a lack of extensive credit history can also lead to higher rates. If you’re a young borrower, new to the country, or simply haven’t used credit much, lenders have less data to evaluate your repayment behavior. Without a track record, they view you as an unknown quantity, which translates to a higher risk profile and, consequently, a higher interest rate.

High Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer to see a DTI ratio below 36%, including your new car payment. If your existing debt obligations (mortgage, student loans, credit card debt, etc.) consume a large portion of your income, a new car loan could push you into a financially precarious position. A high DTI suggests you might struggle to manage additional payments, prompting lenders to offer less favorable terms.

Loan-to-Value (LTV) Issues

The LTV ratio compares the amount you’re borrowing to the value of the car. If you’re trying to finance a car that’s worth significantly less than the loan amount (e.g., an older model, a vehicle with high mileage, or one with existing negative equity rolled in from a trade-in), lenders perceive this as a higher risk. They might be concerned that if you default, they won’t recover their investment by repossessing and selling the vehicle.

Specific Lender Policies (Subprime Lenders)

Not all lenders operate with the same risk tolerance. Some specialize in "subprime" lending, catering specifically to individuals with lower credit scores or challenging financial histories. While these lenders offer opportunities to those who might otherwise be denied, they typically do so at significantly higher interest rates to offset their increased risk exposure. They are often the ones offering rates like 18 percent.

Market Conditions

While less impactful than personal credit, broader economic conditions can influence interest rates. If the Federal Reserve raises its benchmark interest rates, the cost of borrowing for lenders increases, and they, in turn, pass some of that cost onto consumers. While this usually affects all rates, it can exacerbate the situation for high-risk borrowers.

Lack of Negotiation or Research

Based on my experience in the financial sector, one of the common mistakes consumers make is not shopping around for the best loan rates. Many people focus solely on the car’s price or the monthly payment, neglecting the interest rate itself. Dealers often have relationships with various lenders, but they might present you with the offer that benefits them most, not necessarily the one best for you. Accepting the first offer without comparing can lead you to an unnecessarily high rate.

The Devastating Impact of an 18% Car Loan Interest Rate

An 18 percent interest rate isn’t just an inconvenience; it’s a financial anchor that can drag down your economic stability. Understanding its full implications is crucial for realizing the urgency of addressing it.

Significantly Higher Monthly Payments

As illustrated earlier, a high interest rate directly translates to a much larger chunk of your income going towards your car payment each month. This reduces your disposable income, making it harder to save, invest, or cover unexpected expenses. What might seem like an affordable car could become a significant strain on your budget.

Massive Total Cost of the Vehicle

The most immediate and painful impact is the sheer amount of extra money you’ll pay over the life of the loan. An 18% rate can add thousands, or even tens of thousands, of dollars to the actual price of your car. This means you’re essentially paying for the car and then paying for it again, or at least a very substantial portion of it, in interest alone.

Negative Equity Risk (Upside Down Loan)

With a high interest rate, a larger portion of your early payments goes towards interest rather than reducing the principal. This means the car depreciates faster than you pay off the loan balance, leading to negative equity. You could owe more on the car than it’s worth, making it difficult to sell or trade in without having to pay the difference out of pocket. This can trap you in a cycle of debt.

Limited Financial Flexibility

High car payments can severely limit your financial flexibility. You might find it challenging to qualify for other loans (like a mortgage) because your DTI ratio is too high. It also restricts your ability to save for emergencies, retirement, or other important life goals, potentially delaying your financial progress.

Difficulty with Future Borrowing

While making payments on time can help your credit, the existence of a high-interest loan on your credit report can still signal risk to other lenders. This might make it harder to secure favorable rates on future loans or credit cards, perpetuating a cycle of expensive borrowing.

Stress and Financial Strain

Beyond the numbers, the psychological toll of a high-interest loan can be significant. The constant pressure of large monthly payments and the feeling of being trapped in an expensive agreement can lead to stress, anxiety, and a reduced quality of life. Financial peace of mind is invaluable, and an 18% car loan actively undermines it.

Immediate Strategies to Mitigate the Damage of a High Interest Rate

If you’ve already secured a car loan with an 18 percent interest rate, don’t despair. While reversing the situation completely might take time, there are immediate steps you can take to lessen the financial burden.

Reviewing Your Loan Agreement Thoroughly

The very first thing you should do is meticulously read your loan agreement. Understand every clause, especially regarding early payment penalties, interest calculation methods, and any fees. Some loans have prepayment penalties, which could negate some of the benefits of paying it off early. Knowing these terms will help you plan your strategy effectively.

Paying More Than the Minimum (If Possible)

If your budget allows, paying extra on your principal each month can dramatically reduce the total interest paid and shorten your loan term. Make sure any extra payments are explicitly applied to the principal balance, not just counted as a future payment. Even an extra $25 or $50 a month can make a surprising difference over the life of the loan.

Pro tips from us: Always confirm with your lender that extra payments are allocated to the principal. Some systems automatically apply it to the next month’s payment, which doesn’t accelerate your principal reduction. A quick phone call or a specific instruction on your online payment portal can ensure your extra money works for you.

Considering a Shorter Loan Term (If Affordable)

If you can manage a higher monthly payment, refinancing into a shorter loan term (e.g., from 72 months to 60 or 48 months) will usually result in a lower interest rate, even with the same credit score. Shorter terms mean less time for interest to accrue, significantly reducing the total cost. This is a powerful strategy if your financial situation has improved since you first took out the loan.

Long-Term Solutions: How to Escape or Avoid an 18% Car Loan Rate

While immediate mitigation helps, the real goal is to escape or prevent such high interest rates altogether. These long-term strategies require patience and proactive financial management.

Refinancing Your Car Loan

Refinancing is often the most effective way to escape a high-interest car loan. This involves taking out a new loan, typically with a lower interest rate, to pay off your existing loan.

- When to Consider It: Refinancing is ideal if your credit score has improved since you got the original loan, if interest rates have dropped, or if you can find a lender willing to offer better terms. It’s also a good option if you initially accepted an unfavorable rate due to limited options.

- Steps Involved:

- Check Your Credit Score: Know where you stand. A score improvement is key.

- Shop Around: Don’t just go to your current lender. Get quotes from multiple banks, credit unions, and online lenders. Credit unions often offer very competitive rates.

- Compare Offers: Look beyond just the interest rate. Consider fees, loan terms, and any prepayment penalties.

- Apply: Once you choose a lender, complete the application process. They will pay off your old loan, and you’ll start making payments to the new lender.

To learn more about optimizing this process, check out our comprehensive guide on Refinancing Your Car Loan for Better Rates.

Improving Your Credit Score

This is a foundational step for securing better rates on all future loans, including car loans. It takes time, but the effort pays off significantly.

- Pay Bills On Time, Every Time: Payment history is the most significant factor in your credit score. Set up reminders or automatic payments.

- Reduce Credit Utilization: Keep your credit card balances low, ideally below 30% of your available credit limit. High utilization signals that you might be over-reliant on credit.

- Check Your Credit Reports for Errors: Obtain free copies of your credit reports from AnnualCreditReport.com. Dispute any inaccuracies, as they can negatively impact your score.

- Diversify Credit Mix (Carefully): Having a mix of credit (e.g., credit cards, installment loans) can be beneficial, but only if you manage it responsibly. Don’t open new accounts just for diversity.

- Become an Authorized User: If a trusted family member with excellent credit adds you as an authorized user on one of their credit cards, their positive payment history can sometimes benefit your score.

For a deeper dive into boosting your creditworthiness, explore our article on Understanding and Improving Your Credit Score.

Making a Larger Down Payment (For Future Purchases)

When buying your next car, a substantial down payment reduces the amount you need to borrow, thus lowering your monthly payments and the total interest paid. It also decreases the lender’s risk, potentially qualifying you for a lower interest rate. Aim for at least 20% of the car’s purchase price.

Choosing a Less Expensive Vehicle (For Future Purchases)

Sometimes, the simplest solution is to buy a car that better fits your budget. A more affordable vehicle means a smaller loan amount, which reduces both the monthly payment and the total interest, even with a higher rate. Don’t let emotion override financial sense.

Considering a Co-Signer

If you have poor credit, a co-signer with excellent credit can help you qualify for a much lower interest rate. The co-signer essentially guarantees the loan, taking on equal responsibility for repayment.

- Pros: Can significantly reduce your interest rate and help you build your own credit.

- Cons: The co-signer is fully responsible if you default, which can strain relationships. It’s a serious commitment for both parties.

Exploring Alternatives to Traditional Loans

- Credit Unions: Often offer lower interest rates and more flexible terms than traditional banks, especially for members.

- Personal Loans: In some rare cases, if you have good credit but the car loan terms are unfavorable, a personal loan might offer a better rate. However, personal loans are usually unsecured and can have higher rates than secured car loans. This option requires careful comparison.

Common Mistakes to Avoid When Dealing with High Car Loan Interest

Navigating a high-interest car loan requires careful decision-making. Here are some common pitfalls to steer clear of:

- Ignoring the Problem: Hoping it will go away or simply accepting the high payments without exploring solutions is a recipe for long-term financial pain. Proactive action is essential.

- Not Reading the Fine Print: Skipping over the details of your loan agreement can lead to costly surprises, such as prepayment penalties or hidden fees. Always understand what you’re signing.

- Accepting the First Offer: Whether it’s the initial car loan or a refinancing offer, never settle for the first option presented. Always shop around and compare multiple offers.

- Focusing Only on Monthly Payment: While monthly payments are important for budgeting, fixating solely on them can lead you to accept longer loan terms and significantly higher total interest costs. Always consider the total cost of the loan.

- Missing Payments: Missing payments will severely damage your credit score, making it even harder to refinance or secure better rates in the future. It can also lead to late fees and, eventually, repossession.

- Taking on More Debt: If you’re already struggling with a high car loan, avoid taking on additional debt, especially high-interest credit card debt. This will only exacerbate your financial strain and hurt your DTI ratio.

Proactive Steps for Your Next Car Purchase (Preventing Future High Rates)

The best defense against an 18 percent interest rate is a good offense. Here’s how to ensure your next car purchase comes with a much more favorable loan:

Pre-Approval is Key

Before you even step foot on a dealership lot, get pre-approved for a car loan from your bank, credit union, or an online lender. This gives you a clear understanding of the interest rate you qualify for and the maximum amount you can borrow. It arms you with leverage when negotiating with the dealer.

Know Your Credit Score Before Shopping

Pull your credit reports and scores several months before you plan to buy a car. This gives you time to correct any errors and take steps to improve your score. Knowing your score empowers you to anticipate what rates you should expect.

Budgeting Beyond the Monthly Payment

Consider the total cost of car ownership, including insurance, maintenance, fuel, and registration, in addition to your loan payment. A holistic budget helps you choose a car that’s truly affordable, not just one with a manageable monthly payment.

Negotiating the Total Price, Not Just the Payment

When at the dealership, negotiate the total purchase price of the car first, before discussing financing. Dealers sometimes try to distract from a high interest rate by focusing on a "low" monthly payment that stretches over many years. Separating these negotiations ensures you get the best deal on both the car and the loan.

Researching Interest Rates

Educate yourself on current average car loan interest rates for various credit score ranges. This knowledge helps you identify if an offered rate is fair or excessively high. A great resource for checking current rates and getting financial advice is the Consumer Financial Protection Bureau (CFPB) website, which offers unbiased information on financial products: Consumer Financial Protection Bureau (CFPB) Auto Loans.

Conclusion: Taking Control of Your Car Loan Destiny

An 18 percent interest rate on a car loan is a serious financial challenge, but it is not an insurmountable one. By understanding its implications, identifying the root causes, and implementing the strategies outlined in this guide, you can take significant steps towards mitigating its damage and preventing future occurrences.

Whether you need to refinance, diligently improve your credit score, or simply adopt more proactive habits for your next vehicle purchase, the power to change your financial trajectory lies in your hands. Don’t let a high interest rate define your financial journey. Arm yourself with knowledge, act decisively, and work towards a future where your car loans are a source of convenience, not financial stress. Start by reviewing your current situation, setting clear financial goals, and taking that first crucial step towards a more favorable financial future.