Decoding the 75-Month Car Loan: Your Comprehensive Guide to Extended Auto Financing

Decoding the 75-Month Car Loan: Your Comprehensive Guide to Extended Auto Financing Carloan.Guidemechanic.com

In today’s dynamic automotive market, the dream of owning a new or newer vehicle often comes with a significant price tag. To make monthly payments more manageable, many buyers are turning to longer loan terms, with the 75-month car loan emerging as a popular option. But what exactly does committing to over six years of car payments entail?

This comprehensive guide will demystify the 75-month car loan, exploring its advantages, potential pitfalls, and crucial considerations. Our goal is to equip you with the knowledge needed to make an informed decision, ensuring your journey to vehicle ownership is both affordable and financially sound. Let’s dive deep into the world of extended auto financing.

Decoding the 75-Month Car Loan: Your Comprehensive Guide to Extended Auto Financing

What Exactly is a 75-Month Car Loan?

A 75-month car loan is simply an auto financing agreement structured to be paid back over 75 months, which equates to six years and three months. This extended repayment period stands in contrast to more traditional terms like 36, 48, or 60 months. Its primary appeal lies in making higher-priced vehicles more accessible to a broader range of buyers.

By stretching out the repayment timeline, lenders can offer significantly lower monthly payments compared to shorter loan durations. This reduction in the immediate financial burden can be very attractive, especially for those on a tight budget or looking to purchase a more expensive car. However, this flexibility often comes with trade-offs that are vital to understand before signing on the dotted line.

The Allure of Longer Loan Terms: Why 75 Months?

The growing popularity of the 75-month car loan isn’t accidental. It addresses several common financial pressures faced by today’s car buyers. Understanding these benefits is the first step in deciding if this financing option aligns with your personal circumstances.

Lower Monthly Payments Offer Budget Relief

The most immediate and compelling benefit of a 75-month car loan is the significantly reduced monthly payment. When you extend the repayment period, the total loan amount is spread out over more installments. This directly translates to each individual payment being smaller.

For many individuals and families, this can be a game-changer. It allows them to fit a new car into their budget without feeling overly strained, or it might even make a slightly more expensive or feature-rich vehicle suddenly seem within reach. This perceived affordability is a powerful driver behind the popularity of extended car financing.

Access to More Expensive Vehicles Becomes Possible

Historically, the cost of a desirable new car could be a barrier for many. With a 75-month car loan, that barrier can feel lower. By lowering the monthly financial commitment, these longer terms open the door to purchasing vehicles that might otherwise be out of budget with traditional 3-5 year loans.

This means you could potentially afford a car with better safety features, more advanced technology, or simply a model that better suits your lifestyle and preferences. It’s about enhancing your purchasing power, allowing you to drive the car you truly want without immediate financial discomfort.

Enhanced Financial Flexibility for Other Expenses

Beyond just affording the car itself, lower monthly payments can free up crucial cash flow. This financial flexibility can be invaluable for managing other household expenses, saving for future goals, or simply having a larger emergency fund. In today’s economy, every dollar counts, and reducing a major recurring expense like a car payment can offer significant breathing room.

This extra wiggle room in your budget can prevent financial stress and allow you to allocate funds to other important areas of your life. It’s about balancing your automotive needs with your broader financial responsibilities, providing a sense of control over your money.

The Downsides and Risks: What You MUST Know

While the benefits of a 75-month car loan are clear, it’s crucial to approach this financing option with a full understanding of its potential drawbacks. Based on my experience working with countless car buyers, overlooking these risks can lead to significant financial distress down the road.

Higher Total Interest Paid Over Time

This is arguably the most significant disadvantage of a long-term loan. While your monthly payments are lower, you are paying interest for a much longer period. Even if the interest rate seems similar to a shorter loan, the cumulative effect of those extra months (or years) of interest payments can add up to a substantial amount. You could end up paying thousands more in total interest over the life of a 75-month loan compared to a 60-month or 48-month term, even for the same vehicle. Always calculate the total cost, not just the monthly payment.

A Longer Period of Debt

Committing to a 75-month car loan means you will be in debt for over six years. This extended period of obligation ties up a portion of your income for a considerable length of time. During this period, your financial situation could change dramatically – you might face unexpected expenses, job changes, or new financial goals like buying a home. A long-term car loan can limit your flexibility to take on new debt or save for other aspirations. It’s important to consider your future financial plans before committing to such a long-term obligation.

Increased Risk of Negative Equity (Being Upside Down)

Negative equity, often called being "upside down" on your loan, occurs when you owe more on your car than it’s worth. This is a common and serious risk with 75-month car loans. Vehicles depreciate rapidly, especially in the first few years. With longer loan terms, your loan balance decreases more slowly than the car’s market value, making it very easy to fall into negative equity.

If you need to sell or trade in your car while you’re upside down, you’ll have to pay the difference out of pocket or roll it into your next car loan, which can create a cycle of debt. Pro tips from us: a significant down payment can help mitigate this risk by reducing the initial loan amount and creating immediate equity.

Higher Insurance Costs May Be Required

When you finance a vehicle, lenders typically require comprehensive and collision insurance coverage to protect their investment. While this is standard for any financed car, the risk of negative equity with longer loan terms can sometimes influence insurance considerations. If you’re upside down on your loan, your insurance payout might not cover the full loan balance in the event of a total loss, highlighting the importance of gap insurance.

Out-of-Warranty Repairs Become More Likely

Most new cars come with a manufacturer’s warranty that typically lasts for 3 to 5 years. With a 75-month loan, you’ll likely be making payments for a significant period after your original warranty has expired. This means any repairs, which can be costly, will come directly out of your pocket.

As a seasoned automotive finance expert, I’ve seen firsthand how unexpected repair bills can strain budgets, especially when coupled with ongoing loan payments. It’s crucial to factor in potential maintenance and repair costs when considering a long-term loan for an older vehicle or if you plan to keep a new car for the full loan term.

Is a 75-Month Car Loan Right for YOU? A Decision-Making Framework

Deciding on any major financial commitment requires careful consideration. A 75-month car loan is no exception. To determine if this extended financing option aligns with your needs, ask yourself these critical questions and evaluate your situation thoroughly.

Assess Your Financial Situation Thoroughly

Your personal finances are the bedrock of any loan decision. Before considering a 75-month car loan, take a hard look at your current financial health.

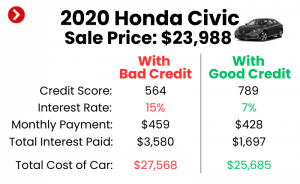

- Credit Score: Your credit score is paramount as it directly impacts the interest rate you’ll be offered. A higher score typically qualifies you for lower rates, which can significantly reduce the total cost of a long-term loan. If your score is low, the interest paid over 75 months could be astronomical. (Internal Link Placeholder: For tips on improving your credit score, read our guide on "How to Boost Your Credit Score for a Car Loan").

- Debt-to-Income Ratio: Lenders assess your debt-to-income (DTI) ratio to understand your ability to manage monthly payments. A high DTI indicates you’re already carrying a lot of debt relative to your income, making additional long-term debt like a 75-month car loan a greater risk for both you and the lender.

- Budget Analysis: Can you truly afford the monthly payments and absorb the higher total interest over the long haul? Create a detailed budget that includes all your income and expenses. Don’t just focus on the monthly payment; consider the entire financial picture, including insurance, fuel, and potential maintenance.

Consider the Vehicle’s Reliability and Depreciation

The car you choose plays a huge role in whether a 75-month loan is a wise choice.

- New vs. Used: New cars generally come with warranties that cover the initial years, but they also depreciate the fastest. Used cars, especially older ones, might have lower initial costs but could incur significant repair expenses once the loan extends beyond their reliable lifespan.

- Depreciation Rate: Some vehicles hold their value better than others. Research the depreciation rate of the specific car you’re interested in. A car that depreciates quickly increases your risk of negative equity, especially with a long loan term. Choosing a model known for its resale value can somewhat mitigate this risk.

Your Long-Term Plans Matter

How long do you typically keep your vehicles? If you’re someone who trades in cars every 3-4 years, a 75-month loan is almost certainly not a good idea due to the high likelihood of negative equity. If you plan to keep the car for a very long time – say, 7-10 years – then you might ride out the negative equity phase and ultimately benefit from the lower monthly payments. Your personal vehicle ownership habits are a key factor.

The Power of a Down Payment & Trade-In

Making a substantial down payment is one of the most effective strategies to mitigate the risks associated with a 75-month car loan. A larger down payment reduces the principal amount you need to finance, thereby lowering both your monthly payments and the total interest paid. Crucially, it also helps establish immediate equity in the vehicle, significantly reducing your chances of going "upside down" on the loan. Similarly, a valuable trade-in can function like a down payment, reducing the financed amount.

Pro Tips for Navigating a 75-Month Car Loan

Based on my experience guiding clients through the complexities of auto financing, here are some invaluable professional tips to help you make the best decisions if you opt for a 75-month car loan.

Shop Around for Lenders Before Visiting the Dealership

Don’t settle for the first loan offer you receive, especially not one from the dealership. Pro tips from us: secure pre-approval from multiple banks, credit unions, and online lenders before you even set foot on a car lot. This allows you to compare interest rates and terms, giving you significant leverage in negotiations. Knowing your financing options upfront empowers you to focus on the car price, rather than being pressured into a less favorable loan.

Negotiate the Price of the Car, Not Just the Payment

A common mistake to avoid is focusing solely on the monthly payment. Dealerships often use long loan terms to make expensive cars seem affordable by quoting low monthly payments, distracting you from the overall cost. Always negotiate the total price of the vehicle first, as if you were paying cash. Once you’ve agreed on a fair price, then discuss the financing terms. This strategy ensures you’re getting a good deal on the car itself, regardless of the loan structure.

Make a Substantial Down Payment to Build Equity

As mentioned earlier, a significant down payment is your best defense against negative equity. Aim for at least 10-20% of the vehicle’s purchase price, if possible. This reduces the amount you need to finance, lowers your monthly payments, and helps you build equity faster than the car depreciates. It’s a proactive step that provides a strong financial buffer throughout your extended loan term.

Seriously Consider Gap Insurance

If you opt for a 75-month car loan, especially with a small down payment, Gap (Guaranteed Asset Protection) insurance is highly recommended. In the event your car is totaled or stolen, your standard auto insurance policy will only pay out the vehicle’s actual cash value at the time of the incident. If you’re upside down on your loan, this payout won’t cover your entire loan balance. Gap insurance covers this difference, protecting you from having to pay for a car you no longer own.

Understand Prepayment Penalties (or Lack Thereof)

Before signing, always check if your loan agreement includes prepayment penalties. Many modern auto loans do not have these, meaning you can pay off your loan early without incurring extra fees. This flexibility is crucial because it allows you to potentially shorten your loan term and save on interest if your financial situation improves. If a loan does have a prepayment penalty, it might be worth looking for another lender.

Budget for Maintenance and Repairs Beyond Warranty

With a 75-month car loan, your vehicle will likely be out of its original manufacturer’s warranty for a substantial portion of the loan term. This means you’ll be responsible for all repair costs. Pro tips from us: Factor in an emergency fund specifically for car maintenance and unexpected repairs. Regular servicing is also vital to keep the car running smoothly and extend its lifespan, ensuring it lasts the full 75 months and beyond.

Explore Refinancing Options if Your Credit Improves

Your financial situation isn’t static. If your credit score improves significantly after you’ve taken out your 75-month car loan, or if interest rates drop, consider refinancing. Refinancing can allow you to secure a lower interest rate, which will reduce your total cost of the loan and potentially even your monthly payments. It’s a smart way to revisit your loan terms and optimize your financial commitment.

Common Mistakes to Avoid When Considering Extended Car Financing

Navigating the world of long-term auto loans can be tricky. As a professional SEO content writer and automotive finance observer, I’ve identified several common pitfalls that borrowers frequently encounter. Avoiding these mistakes can save you a significant amount of money and stress.

Focusing Only on the Monthly Payment

This is perhaps the biggest and most detrimental mistake. While a low monthly payment is appealing, it’s a deceptive metric if not viewed in context. Dealerships often leverage this by extending loan terms to make nearly any car seem affordable. Always ask for the total cost of the loan, including all interest, fees, and the principal. Ignoring the total cost can lead to paying thousands more than necessary over the life of the loan.

Ignoring the Total Cost of the Loan

Following from the point above, many consumers fail to calculate the true cost of their financing. A 75-month car loan, despite its attractive low monthly payments, almost invariably results in a higher total amount paid due to the extended interest accumulation. Always use an online car loan calculator to compare the total interest paid across different loan terms (e.g., 60 months vs. 75 months) for the same vehicle price and interest rate. This clear comparison will highlight the financial impact of a longer term.

Not Understanding Negative Equity (Being Upside Down)

Many borrowers don’t fully grasp the concept or implications of negative equity until it’s too late. With rapid depreciation and slow principal reduction on long loans, you can quickly find yourself owing more than your car is worth. This situation becomes problematic if you need to sell the car, trade it in, or if it’s totaled. Always be aware of your car’s market value versus your outstanding loan balance.

Skipping a Down Payment Entirely

While it’s possible to get a car loan with no down payment, it’s generally a risky move, especially with a 75-month term. No down payment means you start with zero equity, immediately increasing your chances of being upside down on the loan. It also means you’ll be financing the entire purchase price, leading to higher monthly payments and more interest paid over time. A down payment is a critical tool for financial stability in auto financing.

Not Shopping for Competitive Interest Rates

Assuming all lenders offer similar rates is a costly assumption. Interest rates can vary significantly between different banks, credit unions, and even dealership finance departments. Failing to shop around means you could miss out on a lower rate that would save you hundreds, if not thousands, over 75 months. Always compare at least three to five loan offers before making a decision. (External Link: For more information on understanding auto loans, visit the Consumer Financial Protection Bureau’s guide on auto loans at consumerfinance.gov).

Buying More Car Than You Need or Can Afford

The allure of a low monthly payment from a 75-month car loan can tempt buyers into purchasing a more expensive vehicle than they genuinely need or can comfortably afford. This overspending can lead to financial strain, not just from the car payment itself, but from higher insurance costs, increased fuel consumption, and more expensive repairs down the line. Always prioritize your actual needs and budget over aspirational wants when it comes to long-term debt.

Alternatives to a 75-Month Car Loan

If the risks associated with a 75-month car loan seem too daunting, or if you simply want to explore other avenues, there are several viable alternatives that might better suit your financial goals.

- Shorter Loan Terms: If your budget allows, opting for a 36, 48, or 60-month loan will drastically reduce the total interest paid and help you build equity much faster. While monthly payments will be higher, the long-term financial benefits are substantial.

- Buying a Less Expensive Car: Re-evaluating your vehicle needs and choosing a slightly less expensive model can make a shorter loan term (and its associated savings) much more feasible. Sometimes, a slight compromise on features or luxury can lead to significant financial peace of mind.

- Saving Up for a Larger Down Payment: Postponing your car purchase to save up a more substantial down payment can have a profound impact. A larger down payment reduces the amount you need to finance, lowering both your monthly payments and total interest, and significantly mitigating the risk of negative equity.

- Considering Reliable Used Cars: A gently used car, especially one a few years old, has already experienced its steepest depreciation. This means you can often get a reliable vehicle for a much lower price, making shorter loan terms and lower overall costs more attainable. Research models known for their longevity and low cost of ownership.

The Application Process for a 75-Month Car Loan

The process of applying for a 75-month car loan is similar to that of any other auto loan, but understanding the steps can help you navigate it smoothly.

- Gather Your Documents: Lenders will typically require proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and potentially bank statements. Having these ready will expedite the process.

- Check Your Credit Score: Before applying, know your credit score. This will give you an idea of the interest rates you might qualify for and help you identify any errors on your credit report.

- Shop for Lenders & Get Pre-Approved: As emphasized earlier, get pre-approved by several financial institutions. This involves submitting an application with your financial details, allowing lenders to provide you with concrete loan offers.

- Compare Offers: Carefully compare the interest rates, monthly payments, total loan cost, and any fees associated with each pre-approval offer. Don’t just look at the monthly payment.

- Finalize the Purchase: Once you’ve chosen your car and secured the best financing, you’ll sign the loan agreement. Make sure you read every line and understand all terms and conditions before signing.

Conclusion: Is a 75-Month Car Loan the Right Road for You?

The 75-month car loan represents a significant shift in automotive financing, offering a pathway to vehicle ownership that prioritizes lower monthly payments. For many, this extended term provides crucial budget relief and access to vehicles that might otherwise be out of reach. It can offer valuable financial flexibility, freeing up cash flow for other essential expenses or savings goals.

However, as we’ve explored in depth, the allure of reduced immediate payments comes with substantial long-term considerations. The higher total interest paid, the extended period of debt, and the increased risk of negative equity are not to be taken lightly. Common mistakes, such as focusing solely on the monthly payment or neglecting a down payment, can amplify these risks, turning an attractive option into a financial burden.

Ultimately, a 75-month car loan is neither inherently good nor bad. It’s a tool, and like any tool, its effectiveness depends entirely on how it’s used and by whom. It requires a diligent and informed approach. Before committing to a 75-month car loan, thoroughly assess your financial situation, understand the total cost, mitigate risks with a down payment and gap insurance, and explore all alternatives. By doing so, you can ensure your auto financing decision empowers your financial future rather than hindering it. Drive smart, not just with a low monthly payment.