Decoding the Common Interest Rate for Car Loans: Your Ultimate Guide to Smart Auto Financing

Decoding the Common Interest Rate for Car Loans: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your first set of wheels or an upgrade. Yet, amidst the thrill of test drives and choosing colors, one critical element often gets overlooked or misunderstood: the car loan interest rate. This seemingly small percentage can have a monumental impact on the total cost of your vehicle and your monthly budget for years to come.

Understanding the common interest rate for car loans isn’t just about knowing an average number; it’s about grasping the intricate factors that determine your specific rate and how to strategically secure the most favorable terms. This comprehensive guide will demystify auto loan interest, empowering you to make informed decisions and drive away with confidence, knowing you’ve secured a deal that truly benefits your financial well-being.

Decoding the Common Interest Rate for Car Loans: Your Ultimate Guide to Smart Auto Financing

What Exactly Are Car Loan Interest Rates? A Fundamental Overview

At its core, a car loan interest rate is the cost of borrowing money from a lender to purchase a vehicle. It’s expressed as a percentage of the principal amount you borrow. Think of it as a rental fee for the money you’re using. The higher the interest rate, the more you pay for the privilege of borrowing.

This rate is typically calculated annually, though your payments are made monthly. Each payment you make goes towards both the principal (the original amount borrowed) and the accrued interest. Over time, as you repay the principal, the amount of interest you pay on the remaining balance gradually decreases.

It’s crucial to distinguish between the simple interest rate and the Annual Percentage Rate (APR). While the interest rate solely reflects the cost of borrowing the principal, the APR provides a more holistic view. The APR includes the interest rate plus any additional fees associated with the loan, such as origination fees or processing charges. When comparing loan offers, always focus on the APR, as it gives you the true total cost of borrowing.

Why Do Car Loan Interest Rates Matter So Much?

The impact of your car loan interest rate extends far beyond just a numerical percentage. It directly influences several key aspects of your financial life. Ignoring its significance can lead to substantial long-term costs and financial strain.

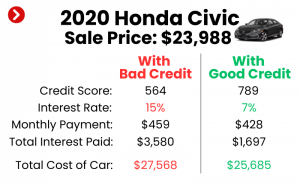

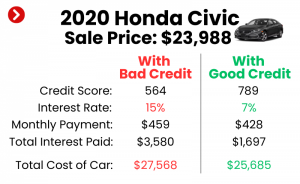

Firstly, your interest rate determines the total amount you will pay for the car. A higher rate means you’ll pay significantly more over the life of the loan, even if the monthly payments seem manageable. For example, a $30,000 loan at 5% interest over five years will cost you thousands less than the same loan at 8% interest. This difference can easily add up to the cost of an extra vacation or a significant contribution to your savings.

Secondly, the interest rate directly shapes your monthly payment. While a lower interest rate naturally reduces your monthly burden, a higher rate pushes it up. For many buyers, the monthly payment is the primary concern, but focusing solely on it without considering the interest rate can be a costly mistake. Lenders might offer longer loan terms to lower monthly payments, but this often comes with a higher overall interest paid.

Finally, your interest rate affects your financial flexibility. A high monthly payment due to a high interest rate can strain your budget, leaving less money for other essential expenses, savings, or investments. Conversely, a favorable interest rate frees up cash flow, providing greater financial breathing room and contributing to your overall financial health. Understanding this impact is the first step toward smart auto financing.

Key Factors Influencing Your Car Loan Interest Rate

The "common interest rate for car loans" isn’t a static figure; it’s a dynamic average influenced by a multitude of personal and economic factors. Lenders assess risk, and your interest rate directly reflects their perception of how likely you are to repay the loan on time. Based on my experience in analyzing countless loan scenarios, here are the most significant elements that dictate the rate you’ll be offered:

1. Your Credit Score: The Undisputed King of Factors

Your credit score is arguably the most impactful determinant of your car loan interest rate. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use this three-digit number to quickly gauge your risk level.

- Excellent Credit (780-850): Borrowers in this tier are considered low-risk. They typically qualify for the lowest available car loan interest rates, often benefiting from promotional rates or manufacturer incentives.

- Good Credit (670-739): This range still secures competitive rates, though they might be slightly higher than those with excellent credit. Most lenders view these borrowers as reliable.

- Fair Credit (580-669): Individuals with fair credit will likely face higher interest rates. Lenders see a moderate risk and compensate with increased charges. Securing approval might be slightly more challenging, and options could be limited.

- Poor Credit (Below 580): Borrowers with poor credit are considered high-risk. They will typically be offered the highest interest rates, sometimes in double digits, to offset the lender’s perceived risk of default. Loan approval may require a larger down payment or a co-signer.

Based on my experience, a difference of even 50 points in your credit score can translate into hundreds, sometimes thousands, of dollars over the life of a loan. Investing time in improving your credit before applying for an auto loan is one of the most financially rewarding actions you can take.

2. The Loan Term (Length of Loan): A Balancing Act

The loan term, or the duration over which you agree to repay the loan, significantly impacts both your monthly payment and the total interest paid. Common terms range from 36 to 84 months, with 60 or 72 months being popular choices.

- Shorter Loan Terms (e.g., 36-48 months): These typically come with lower interest rates. Lenders perceive less risk over a shorter period. While your monthly payments will be higher, you’ll pay substantially less in total interest over the life of the loan. This is often the most cost-effective option if your budget allows.

- Longer Loan Terms (e.g., 72-84 months): These terms offer lower monthly payments, making expensive cars seem more affordable. However, they almost always come with higher interest rates because the lender’s risk exposure is extended. Pro tips from us: While a longer term lowers your monthly payment, it almost always means you’ll pay significantly more in total interest and face a higher likelihood of becoming "upside down" on your loan (owing more than the car is worth).

3. New vs. Used Car: Different Risk Profiles

The age and condition of the vehicle itself play a role in determining your auto loan rates.

- New Car Loan Rates: Generally, new cars qualify for lower interest rates. Lenders view new vehicles as less risky because they are less likely to break down, come with warranties, and their depreciation curve is more predictable initially. Manufacturers also often offer attractive promotional rates on new models to boost sales.

- Used Car Loan Rates: Used car loan rates tend to be higher than those for new cars. This is due to several factors: used cars carry a higher risk of mechanical issues, they depreciate more rapidly, and their value can be harder to ascertain accurately. The older the used car, the higher the perceived risk and, consequently, the higher the potential interest rate.

4. Your Down Payment: Reducing Lender Risk

A significant down payment is one of the most effective ways to secure a lower interest rate. When you put down a substantial amount of your own money, you reduce the principal loan amount, which in turn reduces the lender’s risk.

A larger down payment also signals to the lender that you are financially stable and committed to the purchase. It directly impacts your Loan-to-Value (LTV) ratio, which is the amount financed compared to the car’s value. A lower LTV (meaning a larger down payment) typically results in a more favorable interest rate. Aim for at least 10-20% if possible.

5. Debt-to-Income Ratio (DTI): Your Financial Bandwidth

Your Debt-to-Income (DTI) ratio is a measure of your monthly debt payments compared to your gross monthly income. Lenders use this to assess your ability to take on additional debt. A lower DTI indicates that you have more disposable income available to comfortably make your car payments.

Typically, lenders prefer a DTI below 40%. A high DTI suggests you might be stretched thin financially, increasing the perceived risk for the lender, and potentially leading to a higher interest rate or even loan denial.

6. Current Economic Conditions and Federal Interest Rates

Broader economic forces also influence auto loan rates. The Federal Reserve’s benchmark interest rate, while not directly controlling car loan rates, sets a precedent for borrowing costs across the economy.

When the Federal Reserve raises its rates to combat inflation, for example, it generally leads to higher interest rates for consumers across the board, including car loans. Conversely, during periods of economic stimulus, rates may decrease. From years of analyzing auto financing trends, it’s clear that understanding the current economic climate can give you an edge in predicting rate movements.

7. Lender Type: Shop Around for the Best Fit

Different types of lenders have varying business models and risk appetites, which translates into different interest rate offerings.

- Banks: Offer competitive rates, especially to borrowers with good credit. They have various loan products and may offer rate discounts for existing customers.

- Credit Unions: Often known for offering some of the lowest interest rates, as they are non-profit organizations focused on member benefits. Membership requirements apply, but they are usually easy to meet.

- Dealership Financing: Convenient, as you can arrange financing directly at the dealership. They work with multiple lenders and can sometimes offer promotional rates from manufacturers. However, their primary goal is to sell cars, so always compare their offer with pre-approvals from other lenders.

- Online Lenders: Many online platforms specialize in auto loans, offering quick pre-approvals and competitive rates, often with streamlined application processes.

What is the Common Interest Rate For Car Loan Today? (The "Average")

It’s important to reiterate that there isn’t a single "common" or "average" interest rate that applies to everyone. Your individual circumstances will dictate the rate you receive. However, we can look at typical ranges to give you a general idea. These figures are illustrative and can fluctuate based on market conditions:

- For New Cars (with good to excellent credit): You might see rates ranging from 3.5% to 7.0% APR. Borrowers with impeccable credit scores (780+) might even qualify for rates below 3% during special promotions.

- For Used Cars (with good to excellent credit): Rates typically start a bit higher due to the increased risk associated with older vehicles, often falling between 5.0% to 10.0% APR.

- For Borrowers with Fair Credit (580-669): Expect significantly higher rates, potentially ranging from 10.0% to 18.0% APR or even more, for both new and used cars.

- For Borrowers with Poor Credit (below 580): These rates can be very high, often starting at 18.0% APR and climbing upwards of 25-30% APR. In these cases, it’s critical to weigh the cost carefully.

These ranges underscore why understanding the influencing factors is paramount. Your goal should be to position yourself to qualify for the lowest end of these spectrums.

Strategies to Secure the Best Car Loan Interest Rate

Now that you understand what goes into determining your rate, let’s explore actionable strategies to help you secure the most favorable terms possible. Based on extensive financial planning discussions and real-world outcomes, these steps are proven to make a difference.

1. Improve Your Credit Score Before Applying

This is perhaps the most impactful long-term strategy. Even small improvements can significantly lower your rate.

- Pay Bills on Time: Payment history is the biggest factor in your credit score. Ensure all your credit card, utility, and other loan payments are made punctually.

- Reduce Existing Debt: Lowering your credit card balances, especially, can improve your credit utilization ratio, which positively affects your score.

- Check Your Credit Report: Obtain free copies of your credit report from all three major bureaus (Equifax, Experian, TransUnion) annually. Dispute any errors or inaccuracies, as these can unfairly drag down your score. For more detailed steps on improving your credit, check out our guide on .

2. Shop Around for Lenders (Get Pre-Approved!)

Never take the first loan offer you receive, especially from a dealership. Different lenders will offer different rates based on their specific criteria and risk models.

- Apply for Pre-Approval: Contact multiple banks, credit unions, and online lenders before you even visit the dealership. Pre-approval involves a soft credit inquiry (which doesn’t harm your score) and gives you a concrete offer. This gives you leverage and a clear benchmark.

- Compare APRs, Not Just Interest Rates: Remember, the APR reflects the true cost of the loan. Carefully compare the APRs, loan terms, and any associated fees from various lenders.

- Use Pre-Approval as a Negotiating Tool: Once you have a pre-approval in hand, you can use it to negotiate with the dealership’s financing department. They may be able to beat or match your existing offer to secure your business.

3. Make a Substantial Down Payment

As discussed, a larger down payment reduces the amount you need to borrow and lowers the lender’s risk.

- Aim for 20%: While not always feasible, a 20% down payment is often recommended, especially for new cars, to help avoid being upside down on your loan early on and to secure the best rates.

- Even 10% Helps: If 20% is out of reach, aim for at least 10%. Every dollar you put down reduces the principal and the total interest you’ll pay.

4. Choose a Shorter Loan Term (If Affordable)

While longer terms mean lower monthly payments, they almost always result in higher total interest paid.

- Balance Monthly Payment with Total Cost: If your budget allows, opt for the shortest loan term you can comfortably afford. You’ll pay off the car faster and save significantly on interest.

- Use a Car Loan Calculator: Experiment with different loan terms on an online calculator to see how they impact your monthly payment and total interest.

5. Consider a Co-signer (If Necessary)

If you have a lower credit score or limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate.

- Understand the Risks: Be aware that a co-signer is equally responsible for the loan. If you miss payments, it will negatively affect both your credit scores. This decision should be made with clear communication and trust.

6. Negotiate the Car Price, Not Just the Loan

Remember, a lower purchase price for the car directly translates to a lower loan amount, which means less interest paid over the life of the loan.

- Separate Negotiations: Try to negotiate the car’s purchase price independently from the financing terms. Finalize the car price first, then discuss financing. Dealerships often try to roll these into one discussion, which can obscure the true costs.

Common Mistakes to Avoid When Applying for a Car Loan

Securing a favorable car loan interest rate requires diligence and an informed approach. However, many buyers fall prey to common pitfalls that can cost them dearly. Our expert insights suggest avoiding these mistakes at all costs:

- Not Checking Your Credit Report: One of the biggest oversights is going into the financing process blind. Always review your credit report for errors and understand your score before you apply.

- Only Getting One Loan Offer: Relying solely on the dealership’s financing or accepting the first offer you receive is a surefire way to miss out on better rates. Always shop around and get pre-approved elsewhere.

- Focusing Solely on the Monthly Payment: While important, an attractive monthly payment can hide a very high interest rate or an excessively long loan term, leading to significantly higher total costs. Always look at the total cost of the loan (APR and total interest).

- Extending the Loan Term Too Much: While it lowers monthly payments, an 84-month loan often means paying more interest than the car is worth and being "upside down" for a substantial period.

- Ignoring Additional Fees: Be aware of any origination fees, documentation fees, or other charges that can inflate your APR.

- Getting Emotionally Attached to a Car: Don’t let emotions drive your financial decisions. Secure your financing and understand the full cost before you fall in love with a specific vehicle. This prevents you from accepting unfavorable terms out of desire.

Refinancing Your Car Loan: A Second Chance at a Better Rate

What if you’ve already purchased a car and now realize your interest rate isn’t ideal? All hope is not lost. Refinancing your car loan offers a valuable opportunity to potentially secure a better interest rate and reduce your monthly payments or total interest paid.

When and Why to Consider Refinancing:

- Improved Credit Score: If your credit score has significantly improved since you first took out the loan, you’re likely eligible for a lower rate.

- Market Rates Have Dropped: If overall auto loan rates have decreased since your purchase, you might find a better deal.

- Financial Situation Change: If your income has increased or your debt has decreased, you might qualify for more favorable terms.

- To Reduce Monthly Payments: Refinancing to a lower interest rate or a longer term (if carefully considered) can free up cash flow.

- To Shorten Your Loan Term: If you want to pay off your car faster, you might refinance to a shorter term with potentially lower rates, accepting higher monthly payments but saving on total interest.

Refinancing involves taking out a new loan to pay off your existing car loan. The new loan will ideally have a lower interest rate, saving you money. If you’re considering this option, our article on offers a deeper dive into the process and benefits.

Tools to Help You: Car Loan Calculators

In your journey to understanding and securing the best car loan interest rate, online car loan calculators are indispensable tools. They allow you to plug in different variables – loan amount, interest rate, and loan term – to instantly see how each affects your estimated monthly payment and the total interest you’ll pay.

These calculators can help you:

- Budget Effectively: Determine what monthly payment fits your budget.

- Compare Scenarios: See the impact of different interest rates and loan terms.

- Plan Your Down Payment: Understand how a larger down payment reduces your loan amount and interest.

Utilize these tools from trusted financial sources to run various scenarios before you commit to a loan. A reliable example can be found on sites like Bankrate or NerdWallet, or even directly on major bank websites.

Conclusion: Empowering Your Car Buying Journey

Navigating the world of car loan interest rates can seem daunting, but armed with the right knowledge, it becomes an empowering part of your car buying journey. The "common interest rate for car loans" is a dynamic concept, deeply personal to your financial profile and the economic landscape.

By understanding the critical factors that influence your rate – primarily your credit score, the loan term, and whether you’re buying new or used – you can take proactive steps to position yourself for the most favorable terms. Remember to shop around extensively, make a solid down payment, and avoid common pitfalls like focusing solely on the monthly payment.

Your car loan is likely one of the largest financial commitments you’ll make outside of a mortgage. Approaching it with diligence and an informed perspective will not only save you thousands of dollars over the life of the loan but also contribute significantly to your overall financial well-being. Drive smart, not just hard.