Decoding the Deal: Your Comprehensive Guide to Used Car Loan Mileage Limits

Decoding the Deal: Your Comprehensive Guide to Used Car Loan Mileage Limits Carloan.Guidemechanic.com

Dreaming of hitting the open road in a reliable pre-owned vehicle? For many, a used car offers the perfect blend of affordability and practicality. However, the path to financing that dream car isn’t always a smooth one, especially when you encounter the often-misunderstood hurdle of used car loan mileage limits.

This isn’t just a random number lenders pull out of a hat; it’s a critical factor that significantly impacts your loan approval, interest rate, and overall financing options. As expert bloggers and professional SEO content writers, we’ve delved deep into the automotive financing world to bring you this super comprehensive guide. Our goal is to demystify these limits, empower you with knowledge, and help you secure the best possible loan for your next used car.

Decoding the Deal: Your Comprehensive Guide to Used Car Loan Mileage Limits

Understanding the "Why": Why Lenders Care So Much About Mileage

Before we dive into the specifics of mileage limits, it’s crucial to understand the underlying reasons lenders impose them. From their perspective, every loan carries a degree of risk, and the mileage on a used car is a direct indicator of that risk.

The Depreciation Factor

A car’s value begins to depreciate the moment it leaves the dealership lot. Mileage is one of the most significant accelerators of this depreciation. The more miles a car has accumulated, the faster its market value typically declines.

Lenders need to ensure that the car, which serves as collateral for your loan, retains sufficient value throughout the loan term. If the car’s value plummets rapidly due to high mileage, the lender faces a greater loss if you default on the loan and they have to repossess and sell the vehicle. It’s a fundamental aspect of their risk assessment.

Mechanical Reliability and Future Expenses

High mileage often correlates with increased wear and tear on a vehicle’s components. Engines, transmissions, brakes, suspension systems – all have finite lifespans that are directly impacted by the miles they’ve traveled. A car with significantly higher mileage is generally perceived as having a greater likelihood of requiring expensive repairs in the near future.

This isn’t just a concern for you as the owner; it’s a concern for the lender. If you’re constantly facing large repair bills, your ability to make timely loan payments could be compromised. Lenders prefer to finance vehicles that are less likely to become financial burdens for their owners, thereby reducing the chance of default.

The Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio is a key metric for lenders. It compares the amount you want to borrow against the car’s appraised market value. For example, if a car is valued at $10,000 and you borrow $8,000, your LTV is 80%.

High mileage directly impacts a car’s market value, driving it down. This can push the LTV ratio higher, making the loan riskier for the lender. A higher LTV means the lender has less equity in the vehicle, increasing their exposure if the car needs to be repossessed. They want to ensure they aren’t lending more than the car is actually worth, especially considering future depreciation.

What Are Typical Used Car Loan Mileage Limits?

There isn’t a universal "magic number" for used car loan mileage limits. These limits can vary significantly based on several factors, including the lender, the specific vehicle, your creditworthiness, and even current market conditions. However, we can identify common ranges and influential factors.

General Mileage Thresholds

Based on my experience working with countless car buyers, most conventional lenders, such as major banks and credit unions, typically prefer vehicles with mileage under certain thresholds. A common sweet spot for the easiest financing is often under 75,000 to 80,000 miles. Some might extend this to 100,000 miles for newer models or specific brands known for their reliability.

Beyond 100,000 miles, financing options tend to narrow, and interest rates may increase to compensate for the perceived higher risk. While it’s certainly possible to finance cars with 120,000 or even 150,000 miles, it usually requires a stronger applicant profile or specialized lenders.

Lender Type Matters

The type of lender you approach will significantly influence the mileage limits they impose.

- Traditional Banks and Credit Unions: These institutions generally have stricter guidelines, often preferring vehicles under 100,000 miles, and sometimes even lower for older models. They typically offer the most competitive interest rates to qualified borrowers.

- Captive Finance Companies: These are financing arms of car manufacturers (e.g., Toyota Financial Services, Ford Credit). They often have slightly more flexible limits for their own brands, especially for Certified Pre-Owned (CPO) vehicles, but still prefer lower mileage.

- Subprime Lenders and "Buy Here, Pay Here" Dealerships: These lenders cater to individuals with lower credit scores or those who have been turned down by traditional lenders. They tend to have much higher, or sometimes no explicit, mileage limits. However, this flexibility comes at a significant cost, often in the form of much higher interest rates and less favorable loan terms.

The Role of Vehicle Age

Mileage isn’t the only factor; a car’s age plays an equally vital role. A 5-year-old car with 70,000 miles is often viewed differently than a 10-year-old car with 70,000 miles, even though the mileage is the same. Older vehicles, regardless of mileage, inherently carry a higher risk of age-related component failures.

Most lenders will have a maximum age limit for used cars they’re willing to finance, often around 8 to 10 years old, regardless of mileage. Some might stretch to 12-15 years for specific models, but this becomes increasingly rare. The combination of high mileage and high age creates a significantly higher risk profile for lenders.

The Interplay of Mileage, Age, and Vehicle Condition

It’s a common misconception that mileage is the only thing that matters. In reality, lenders assess a holistic picture, where mileage, age, and the vehicle’s overall condition are all intertwined. A car with slightly higher mileage but impeccable maintenance records and pristine condition might be more attractive than a lower-mileage car that has been neglected.

Maintenance History: Your Golden Ticket

A comprehensive and well-documented maintenance history can be a game-changer when financing a higher-mileage vehicle. Service records demonstrate that the car has been properly cared for, mitigating some of the perceived risks associated with its mileage.

Lenders and buyers alike feel more confident knowing that oil changes, tire rotations, and major services have been performed according to the manufacturer’s recommendations. This history suggests the car is more likely to be reliable and less prone to unexpected breakdowns, directly influencing its perceived value and financeability.

The Non-Negotiable Pre-Purchase Inspection (PPI)

When considering a used car, especially one approaching or exceeding typical mileage limits, a pre-purchase inspection (PPI) by an independent, certified mechanic is absolutely non-negotiable. This isn’t just for your peace of mind; it provides tangible proof of the vehicle’s current mechanical condition.

A positive PPI report can serve as a powerful tool in your loan application, showing the lender that the car, despite its mileage, is currently in good working order. It addresses many of their concerns about immediate mechanical failures and helps justify the loan amount. We highly recommend you read our detailed guide on to ensure you cover all bases.

Impact of Make and Model

Certain car brands are renowned for their longevity and reliability, even at higher mileages. For instance, some Toyota or Honda models with 120,000 miles might be more readily financed than a European luxury car with the same mileage, simply due to their reputation for robust engineering and lower long-term ownership costs.

Lenders are aware of these industry reputations and often adjust their risk assessment accordingly. A car known for enduring high mileage without major issues presents a lower risk, potentially allowing for more flexible financing terms.

Strategies for Financing High-Mileage Used Cars

So, what if your dream car has more miles than typical lenders prefer? Don’t despair! While it might require a bit more effort and strategic planning, financing a high-mileage used car is absolutely possible.

Boost Your Credit Score

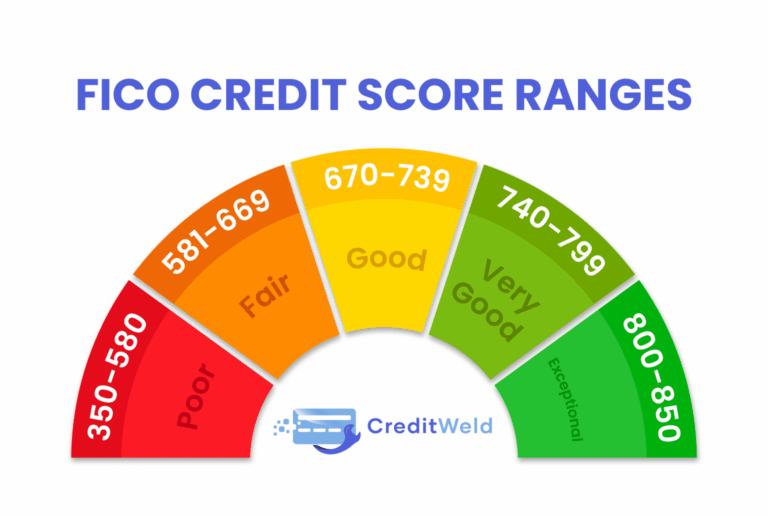

Your credit score is arguably the most influential factor in any loan application. A strong credit profile (generally FICO scores above 670) can offset some of the risk associated with a higher-mileage vehicle. Lenders are more willing to take a chance on a vehicle if they are confident in your ability to repay the loan based on your financial history.

Before applying, take steps to improve your credit: pay down existing debts, dispute any errors on your credit report, and ensure you make all payments on time. Even a small improvement can make a difference in your interest rate and approval chances.

Offer a Larger Down Payment

A larger down payment directly reduces the amount you need to borrow and, consequently, the lender’s risk. By putting more money down upfront, you increase your equity in the vehicle from day one, which lowers the Loan-to-Value (LTV) ratio.

This makes the loan more attractive to lenders, as their potential loss in case of default is significantly reduced. Pro tips from us: Aim for at least 20% down, especially for higher-mileage vehicles, to show serious commitment and improve your chances.

Opt for a Shorter Loan Term

While a longer loan term means lower monthly payments, it also means you’ll be paying interest for a longer period, and the car will depreciate further over that time. For high-mileage cars, a shorter loan term (e.g., 36 or 48 months instead of 60 or 72) can be beneficial.

A shorter term reduces the overall risk for the lender, as the car will have less time to accumulate more miles and depreciate substantially before the loan is paid off. You’ll pay off the loan faster, often at a lower total interest cost, and mitigate the depreciation risk for the lender.

Secure a Co-Signer

If your credit isn’t stellar or the car’s mileage is pushing limits, bringing in a co-signer with excellent credit can significantly improve your chances of approval and secure a better interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

This additional layer of security drastically reduces the lender’s risk. Just be sure both you and your co-signer understand the full implications and responsibilities involved.

Shop Around for Lenders

A common mistake many buyers make is only applying with one or two lenders. Different lenders have different risk appetites, lending criteria, and preferred mileage limits. What one bank rejects, another credit union might approve.

Take the time to compare offers from various sources: traditional banks, credit unions, online lenders, and even the dealership’s finance department. Getting pre-approved from multiple lenders allows you to compare terms and choose the best fit for your specific situation and the car you’re eyeing.

Demonstrate Vehicle Reliability with Extended Warranties

If you’re buying a high-mileage car, consider purchasing an extended warranty or vehicle service contract. While an additional cost, it can provide a strong selling point to lenders. It shows that potential future repair costs are covered, reducing the likelihood that these expenses will prevent you from making your loan payments.

This demonstrates foresight and financial prudence on your part, reassuring the lender about the vehicle’s long-term viability and your ability to manage potential repair costs.

Beyond the Loan: What High Mileage Means for You

Securing the loan is just one part of the equation. Owning a high-mileage car comes with its own set of considerations that you, as the buyer, need to be fully prepared for.

Increased Maintenance and Repair Costs

As discussed, high-mileage cars are inherently more prone to needing repairs. While a PPI and maintenance history help, anticipate that you will likely spend more on maintenance and potential repairs over your ownership period compared to a lower-mileage vehicle.

Budgeting for these costs is crucial. An emergency fund specifically for car repairs can prevent financial stress and ensure you can keep your vehicle running reliably.

Potential for Lower Fuel Efficiency

Older, higher-mileage engines may not be as fuel-efficient as their newer, lower-mileage counterparts. Components can wear, sensors might degrade, and overall engine performance can decrease, leading to slightly higher fuel consumption.

Factor this into your overall budget. Even a small difference in MPG can add up significantly over months and years of ownership.

Insurance Considerations

While not always a direct correlation, some insurance companies might view older, higher-mileage vehicles as having a higher risk of breakdown or being involved in accidents due to potential mechanical issues. This could subtly influence your insurance premiums, though other factors like your driving record and location usually have a larger impact.

It’s always wise to get insurance quotes for any specific vehicle you’re considering before finalizing your purchase to avoid surprises.

Future Resale Value

Just as high mileage impacts the car’s value now, it will continue to do so when you eventually decide to sell or trade it in. Be realistic about the future resale value. A car with 150,000 miles now will have 200,000+ miles by the time you’re ready to part with it, making it even harder to sell and significantly reducing its market worth.

Consider your long-term plans. If you plan to keep the car until it gives out, this might not be a major concern. But if you foresee trading it in within a few years, factor in accelerated depreciation.

The Application Process: What Lenders Really Look For

When you apply for a used car loan, especially for a higher-mileage vehicle, lenders meticulously evaluate several aspects of your financial health and the vehicle’s details.

Your Credit History and Score

This is the bedrock of your application. Lenders will pull your credit report to assess your payment history, outstanding debts, and overall creditworthiness. A higher score signifies a lower risk.

Debt-to-Income (DTI) Ratio

Lenders want to see that you have enough disposable income to comfortably afford your car payments in addition to your other monthly financial obligations. Your DTI ratio, which compares your total monthly debt payments to your gross monthly income, is a key indicator of your ability to repay.

Employment Stability

Consistent employment demonstrates a reliable income stream. Lenders prefer applicants who have been steadily employed for at least a year or two, as it indicates financial stability and a reduced risk of sudden income loss.

Vehicle Specifics

The lender will require detailed information about the car: make, model, year, VIN (Vehicle Identification Number), and, of course, the exact mileage. They will use this information to assess its market value and determine its eligibility for financing.

Your Down Payment

The size of your down payment directly impacts the loan amount and the lender’s risk. A substantial down payment shows commitment and reduces the LTV, making your application more attractive.

For additional resources on managing your personal finances and understanding credit, we recommend visiting the Consumer Financial Protection Bureau website, a trusted external source for unbiased financial guidance.

Pro Tips and Final Considerations

Navigating the world of used car loans and mileage limits can feel complex, but with the right approach, you can find the perfect vehicle and financing solution.

Get Pre-Approved Before You Shop

This is perhaps the most crucial tip. Getting pre-approved for a loan before you even step foot on a dealership lot empowers you. You’ll know exactly how much you can borrow, at what interest rate, and what mileage limits your lender is comfortable with. This knowledge gives you strong negotiating power and prevents you from falling in love with a car you can’t finance.

Be Realistic About Your Options

While it’s good to be optimistic, it’s also important to be realistic. If your budget only allows for cars with very high mileage, understand that your financing options might be limited to subprime lenders with higher interest rates. Adjust your expectations accordingly or consider saving up for a larger down payment.

Explore Certified Pre-Owned (CPO) Vehicles

If you’re looking for a balance between affordability and reliability, Certified Pre-Owned (CPO) programs are an excellent option. CPO vehicles typically undergo rigorous inspections, come with extended warranties, and often have lower mileage limits set by the manufacturer. While they might be slightly more expensive than non-CPO used cars, the added peace of mind and easier financing can be well worth it.

Avoid Predatory Loans

If you find yourself repeatedly rejected by traditional lenders, beware of "guaranteed approval" offers with extremely high interest rates and unfavorable terms. These predatory loans can trap you in a cycle of debt. It’s often better to wait, improve your credit, or save more money than to take on a loan that puts you in a worse financial position.

Read the Fine Print

Before signing any loan agreement, meticulously read every single detail. Understand the interest rate, APR, loan term, all fees, and any prepayment penalties. Don’t hesitate to ask questions until you fully comprehend every aspect of the loan. For a deeper dive into how interest rates work, explore our guide on .

Conclusion: Driving Forward with Confidence

The concept of a used car loan mileage limit is a fundamental aspect of auto financing, rooted in a lender’s need to manage risk. By understanding why these limits exist, what typical thresholds are, and how your credit and the car’s condition play a role, you can approach the used car market with confidence.

Armed with knowledge and the right strategies – from improving your credit to securing a pre-approval – you can navigate these limits effectively. Remember, finding the right car is just the first step; securing the right financing ensures your journey is smooth and worry-free. Happy car hunting!