Decoding the Drive: Your Ultimate Guide to Car Loan Underwriting and Approval

Decoding the Drive: Your Ultimate Guide to Car Loan Underwriting and Approval Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your first set of wheels or an upgrade. However, the path to driving off the lot isn’t always a straight line. Before you get the keys, there’s a crucial, often mysterious, process that happens behind the scenes: car loan underwriting. This isn’t just a formality; it’s the bedrock upon which your entire car financing experience is built.

Understanding car loan underwriting is like having a roadmap for your financial journey. It demystifies why lenders approve some applications and decline others, and, most importantly, it empowers you to approach the car buying process with confidence and a clear strategy. As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate this process, and my mission today is to pull back the curtain, providing you with an in-depth, actionable guide that will significantly improve your chances of securing favorable auto loan terms.

Decoding the Drive: Your Ultimate Guide to Car Loan Underwriting and Approval

Let’s dive deep into the world of car loan underwriting, transforming it from a complex financial hurdle into a transparent, manageable step towards your dream car.

What is Car Loan Underwriting? The Foundation of Your Auto Financing

At its core, car loan underwriting is the process by which a lender evaluates your financial risk to determine if they should approve your auto loan application. Think of it as a comprehensive assessment of your creditworthiness and your ability to repay the loan. Lenders aren’t just looking at a single number; they’re piecing together a complete financial picture to assess the likelihood of default.

This process is absolutely crucial for lenders. It protects their investments and helps them manage their overall risk portfolio. Without robust underwriting, lenders would face significantly higher losses, which would ultimately drive up interest rates for everyone. It’s a system designed to create a balanced ecosystem between borrowers and financial institutions.

Based on my experience, many people view underwriting as a black box. However, understanding the criteria involved can transform your approach to car financing. It’s about more than just filling out a form; it’s about presenting yourself as a reliable borrower.

The Pillars of Underwriting: Key Factors Lenders Evaluate

When you apply for a car loan, underwriters meticulously examine several critical factors. These aren’t just checkboxes; they are the fundamental pillars upon which your loan approval and terms are decided. Let’s break down each one in detail.

1. Credit Score and History: The Borrower’s Financial Fingerprint

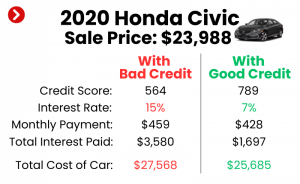

Your credit score, typically a FICO or VantageScore, is often the first thing a lender looks at. It’s a three-digit number that summarizes your credit risk based on your past borrowing behavior. A higher score generally indicates lower risk and can unlock better interest rates and more favorable terms.

Underwriters delve much deeper than just the score itself. They examine your full credit report, which details your payment history, the types of credit accounts you have, the length of your credit history, your credit utilization (how much credit you’re using versus how much you have available), and any recent credit inquiries. A history of on-time payments is gold, while late payments, collections, or bankruptcies can significantly raise red flags.

Pro tips from us: Regularly check your credit report from all three major bureaus (Experian, Equifax, TransUnion) for accuracy. Dispute any errors immediately. Building a strong credit history takes time and consistent responsible behavior, so start early!

2. Debt-to-Income (DTI) Ratio: Balancing Your Financial Books

Your Debt-to-Income (DTI) ratio is a crucial indicator of your ability to manage additional debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your monthly debt payments (including rent/mortgage, credit card minimums, student loans, etc.) are $1,500 and your gross monthly income is $4,000, your DTI would be 37.5% ($1,500 / $4,000 = 0.375).

Lenders use DTI to ensure you have enough disposable income to comfortably make your car loan payments without becoming overextended. A low DTI ratio signals to lenders that you have a healthy financial buffer. Most lenders prefer a DTI ratio below 40%, and often ideally below 36%, including the proposed new car payment.

Common mistakes to avoid are taking on significant new debt, such as opening new credit cards or taking out personal loans, right before applying for a car loan. This can inflate your DTI and make you appear riskier.

3. Loan-to-Value (LTV) Ratio and the Vehicle Itself: The Car’s Role in the Equation

The Loan-to-Value (LTV) ratio compares the amount you want to borrow to the market value of the car you intend to purchase. It’s calculated by dividing the loan amount by the vehicle’s appraised value. For instance, if a car is valued at $25,000 and you’re borrowing $22,000, your LTV is 88% ($22,000 / $25,000).

A lower LTV ratio, ideally below 100%, is highly desirable for lenders because it means there’s less risk of them losing money if you default and they have to repossess and sell the vehicle. A higher LTV, especially above 100% (often seen when rolling negative equity from a trade-in into a new loan), increases the lender’s exposure.

Based on my experience, the vehicle itself plays a significant role. Underwriters assess the car’s age, mileage, condition, make, and model. New cars generally hold their value better initially, while older, high-mileage vehicles depreciate faster and carry higher risk. Lenders also consider the vehicle’s marketability; some cars are simply easier to resell than others.

4. Down Payment: Your Commitment to the Loan

The down payment is the initial amount of money you pay upfront for the car, reducing the amount you need to borrow. This is a powerful factor in underwriting for several reasons. For the borrower, a larger down payment means lower monthly payments, less interest paid over the life of the loan, and a better LTV ratio.

For the lender, a substantial down payment significantly reduces their risk. It shows your financial commitment to the purchase and means they have less money "on the line." If you put down 20% or more, you immediately create equity in the vehicle, which is a strong signal of reliability.

Pro tips from us: Aim for at least a 10-20% down payment if possible. Even a smaller down payment can make a noticeable difference in your LTV and interest rate. It also provides a buffer against immediate depreciation.

5. Employment Stability and Income Verification: Proving Your Repayment Capacity

Lenders need assurance that you have a stable and reliable source of income to make your monthly payments. Underwriters will scrutinize your employment history, looking for consistency and longevity in your job. Frequent job changes or gaps in employment can be a red flag, indicating potential income instability.

You’ll be asked to provide proof of income, which typically includes recent pay stubs (usually 2-3 months’ worth), W-2 forms, and sometimes even tax returns, especially if you’re self-employed. For self-employed individuals, proving stable income can be more challenging, often requiring two years of tax returns to demonstrate consistent earnings.

Common mistakes to avoid include misrepresenting your income or employment status. Lenders verify this information rigorously, and any discrepancies can lead to immediate denial.

6. Other Factors: Beyond the Core

While the five factors above are paramount, underwriters may also consider other elements:

- Residency Stability: A long-term, stable address can indicate reliability.

- Existing Relationship with the Lender: If you have other accounts in good standing with the same bank or credit union, they might be more inclined to approve your loan.

- Co-signer: If your own credit profile isn’t strong enough, a co-signer with excellent credit can significantly boost your application. However, remember that the co-signer is equally responsible for the debt.

The Underwriting Process: Step-by-Step

Understanding the individual factors is one thing; seeing how they fit into the overall process is another. Here’s a typical step-by-step breakdown of how car loan underwriting unfolds:

- Application Submission: You complete a loan application, either online, at a dealership, or directly with a bank or credit union. This form collects your personal, financial, and employment information.

- Data Gathering: The lender initiates a "hard inquiry" on your credit report. They also begin verifying your income, employment, and residency using the documents you provide. This is where the underwriter starts compiling your financial profile.

- Risk Assessment: An underwriter, often with the aid of automated systems, reviews all the collected data. They compare your financial profile against the lender’s specific lending criteria and risk tolerance. This is where your credit score, DTI, LTV, income stability, and other factors are weighed against each other.

- Decision Making: Based on the risk assessment, the underwriter makes a decision. This could be:

- Approved: Your loan is approved with the proposed terms.

- Conditionally Approved: Your loan is approved, but with specific conditions (e.g., provide additional documentation, a larger down payment, or a co-signer).

- Denied: Your application does not meet the lender’s criteria.

- Communication of Terms: If approved, you receive the loan offer detailing the interest rate, loan term, monthly payment, and any other conditions. If denied, the lender is legally required to provide a reason for the denial.

This process can take anywhere from a few minutes (with automated systems for well-qualified applicants) to a few business days for more complex cases.

Common Reasons for Car Loan Denial and How to Avoid Them

Even with a good understanding of the process, denials can happen. Knowing the most common reasons can help you proactively address potential issues.

- Poor Credit Score or Limited Credit History: This is a primary culprit. A low score signals high risk, while a very short credit history makes it difficult for lenders to assess your reliability.

- High Debt-to-Income (DTI) Ratio: If your existing debt obligations consume too much of your income, lenders will question your ability to take on another monthly payment.

- Insufficient or Unstable Income: Lenders need to be confident you have the consistent income to cover payments. Unemployment, short job tenure, or highly variable income (without strong supporting documentation) can lead to denial.

- High Loan-to-Value (LTV) Ratio: If you’re trying to borrow significantly more than the car is worth, or if you have no down payment, the lender’s risk exposure increases dramatically.

- Incomplete or Inaccurate Application Information: Any missing details or discrepancies between your application and verified information can halt the process or lead to denial. Lenders value transparency and accuracy.

- Vehicle-Related Issues: Sometimes the car itself is the problem. An older vehicle, one with very high mileage, or a make/model with a poor resale value might be deemed too risky for the loan amount requested.

Pro tips from us: Before applying, perform a "self-underwriting" check. Review your credit, calculate your DTI, and gather all necessary income documentation. Addressing these points before you apply can save you time and frustration.

Improving Your Chances: Strategies for a Smoother Approval

Don’t despair if your financial profile isn’t perfect. There are many proactive steps you can take to strengthen your application and increase your likelihood of approval.

- Boost Your Credit Score: Pay all your bills on time, reduce your credit card balances to lower your credit utilization, and avoid opening new credit accounts right before applying. These actions can incrementally improve your score over time.

- Reduce Existing Debt: Pay down credit card balances or personal loans. This will lower your DTI ratio, making you a more attractive borrower. Even small reductions can make a difference.

- Save for a Larger Down Payment: As discussed, a larger down payment reduces LTV and signals commitment. Aim for at least 10%, or even 20% if possible, especially on used cars.

- Choose an Affordable Vehicle: Be realistic about what you can afford. A lower-priced car means a smaller loan amount, which translates to a lower monthly payment and often a better LTV.

- Get Pre-Approved: Obtaining pre-approval from banks or credit unions before visiting the dealership gives you a solid understanding of your approved loan amount and terms. This transforms you into a cash buyer at the dealership, giving you more negotiation power.

- Consider a Co-signer: If your credit is challenged, a co-signer with excellent credit and a stable financial history can significantly improve your chances and potentially secure a better interest rate. Ensure both parties understand the full responsibility involved.

- Shop Around for Lenders: Don’t just rely on the dealership’s financing. Explore options from multiple banks, credit unions, and online lenders. Different lenders have different underwriting criteria and risk appetites. You can compare offers without impacting your credit score too much, as multiple hard inquiries for the same type of loan within a short period (typically 14-45 days) are often counted as a single inquiry.

Based on my experience, preparation is key. The more you understand about your own financial standing and the underwriting process, the better equipped you will be to present a strong application.

Navigating Different Lender Types: Banks, Credit Unions, and Dealerships

The source of your car loan can also influence the underwriting experience. Each type of lender has its own approach and potential advantages.

- Banks: Traditional banks often have stringent underwriting criteria, especially for those with less-than-perfect credit. However, if you have an existing relationship and good credit, they can offer competitive rates.

- Credit Unions: Known for their member-focused approach, credit unions often have more flexible underwriting standards and can be more willing to work with borrowers who have unique financial situations. They frequently offer excellent rates. For a deeper dive into choosing the right lender, check out our guide on Choosing the Right Car Loan Lender: A Comprehensive Guide. (Internal Link Placeholder)

- Dealerships: While convenient, dealership financing often acts as an intermediary, submitting your application to multiple lenders. They can sometimes secure approvals for those with lower credit scores, but it’s always wise to compare their offers with your pre-approvals.

The Future of Car Loan Underwriting: Technology and Trends

The landscape of car loan underwriting is constantly evolving. We’re seeing an increasing reliance on technology, with artificial intelligence (AI) and machine learning algorithms playing a larger role in assessing risk. These advanced systems can analyze vast amounts of data more quickly and efficiently than human underwriters alone.

Furthermore, lenders are beginning to explore alternative data points beyond traditional credit scores, such as utility payment history or banking transaction data, to get a more holistic view of a borrower’s financial behavior, particularly for those with thin credit files. This could potentially open up opportunities for more people to secure auto financing in the future. For more insights into emerging trends in auto finance, you might find this industry report from J.D. Power insightful: J.D. Power Auto Finance Study. (External Link Placeholder)

Your Drive Starts Here: Empowering Your Car Loan Journey

Car loan underwriting, while intricate, doesn’t have to be intimidating. By understanding the core factors lenders consider—your credit score, DTI, LTV, down payment, and income stability—you gain a significant advantage. This knowledge empowers you to proactively address potential weaknesses in your application and present yourself as a reliable and responsible borrower.

Remember, securing a car loan isn’t just about getting approved; it’s about securing the best possible terms for your financial situation. With this comprehensive guide, you are now equipped to navigate the auto loan process with confidence, making informed decisions that lead to a smoother, more affordable path to your next vehicle. Your journey to car ownership starts with a solid understanding of the financial road ahead.