Decoding the Drive: Your Ultimate Guide to Navigating the Consumer Car Loan Landscape

Decoding the Drive: Your Ultimate Guide to Navigating the Consumer Car Loan Landscape Carloan.Guidemechanic.com

Buying a car is more than just a purchase; it’s an investment in freedom, convenience, and often, a significant part of your daily life. For most people, securing a consumer car loan is an essential step in turning that dream into a reality. Yet, the world of car financing can feel like a complex maze, filled with jargon and countless options.

This comprehensive guide is designed to demystify the entire process. We’ll explore everything you need to know about auto loans, from understanding interest rates to mastering the art of pre-approval, ensuring you make informed decisions. Our ultimate goal is to equip you with the knowledge to secure the best possible vehicle financing for your next ride, making your car-buying journey smooth and stress-free. Let’s hit the road to smarter car ownership!

Decoding the Drive: Your Ultimate Guide to Navigating the Consumer Car Loan Landscape

What Exactly is a Consumer Car Loan, and Why Does It Matter?

At its core, a consumer car loan is a sum of money borrowed from a financial institution or lender specifically for the purchase of a vehicle. This loan is then repaid over a set period, typically with interest. It’s the primary way most individuals finance their new car loan or used car loan purchases, bridging the gap between their savings and the car’s total price.

Understanding this fundamental concept is crucial because it sets the stage for every decision you’ll make regarding your car purchase. Without a clear grasp, you might unknowingly agree to terms that are less favorable, impacting your long-term financial health. Think of it as the financial engine that powers your car acquisition.

Most consumer car loans are "secured loans." This means the car itself acts as collateral for the loan. If you fail to make your payments, the lender has the legal right to repossess the vehicle to recover their losses. This structure is what allows lenders to offer more attractive interest rates compared to unsecured loans, as their risk is significantly reduced.

Knowing this distinction helps you appreciate the responsibility that comes with taking on car financing. It’s not just about getting the keys; it’s about fulfilling a commitment to repay, safeguarding your credit, and ultimately, retaining ownership of your vehicle.

The Pillars of Your Auto Loan: Key Factors Lenders Evaluate

When you apply for a consumer car loan, lenders don’t just hand over money; they assess your financial reliability. Several critical factors come into play, each influencing whether your loan application is approved and, more importantly, the terms you receive. Understanding these pillars is your first step towards securing favorable vehicle financing.

Your Credit Score: The Ultimate Financial Report Card

Your credit score is arguably the most significant factor lenders consider. It’s a three-digit number that summarizes your financial history, indicating your likelihood of repaying debt. A higher score signifies a lower risk to lenders, often translating into lower interest rates and better loan terms. Conversely, a low score can lead to higher rates or even a rejected application.

Based on my experience, many first-time car buyers underestimate the power of their credit score. It’s not just a number; it’s your financial reputation speaking volumes before you even say a word. Taking steps to improve your credit before applying can save you thousands over the life of the loan.

Before you even start looking at cars, pull your credit report from one of the major bureaus (Experian, Equifax, TransUnion). Check for any errors and dispute them immediately. A clean, strong credit report is your golden ticket to unlocking the best auto loan offers.

The Down Payment: Your Upfront Investment

A down payment is the initial sum of money you pay towards the purchase of your car, reducing the amount you need to borrow. While not always mandatory, making a substantial down payment offers numerous advantages. It lowers your overall loan amount, which in turn reduces your monthly payments and the total interest you’ll pay over the loan term.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price, especially for a new car loan. For used car loans, a larger down payment can be even more beneficial due to potentially higher interest rates. A larger down payment also builds immediate equity in your vehicle, protecting you from becoming "upside down" on your loan (owing more than the car is worth).

This upfront investment demonstrates your commitment to the purchase and can make you a more attractive borrower to lenders. It signals financial stability and reduces the lender’s risk, potentially leading to better car financing options.

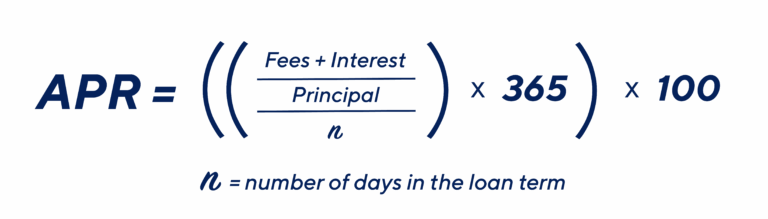

Interest Rates (APR): The Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is essentially the cost you pay to borrow money. It’s calculated as a percentage of the principal loan amount. A lower APR means less money paid back over the life of the loan, making it a critical factor in your overall affordability.

Common mistakes to avoid are focusing solely on the monthly payment without considering the APR. A low monthly payment achieved through an extended loan term can mask a high interest rate, leading to significantly more money paid in total interest. Always compare the APRs across different auto loan offers.

Your credit score, the loan term, the amount of your down payment, and even the current economic climate all play a role in determining the interest rate you’re offered. Shopping around for the best rates from various lenders is a non-negotiable step in smart vehicle financing.

Loan Term: The Repayment Timeline

The loan term refers to the length of time you have to repay the consumer car loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term generally results in lower monthly payments, making the car seem more affordable in the short term. However, this comes at a cost.

Extending the loan term often means paying more interest over the life of the loan, as the interest accrues for a longer period. Moreover, a longer term increases the risk of your car’s value depreciating faster than you pay off the loan, leaving you with negative equity. Our expert advice suggests finding a balance between manageable monthly payments and minimizing the total interest paid.

For most buyers, a loan term between 48 and 60 months offers a good compromise. While longer terms might look appealing initially, they can lead to a more expensive car in the long run. Always calculate the total cost of the loan for different terms before committing.

Debt-to-Income Ratio (DTI): Your Financial Bandwidth

Your debt-to-income ratio (DTI) is a crucial metric lenders use to assess your ability to manage monthly payments. It compares your total monthly debt payments (including the proposed car payment, mortgage/rent, credit cards, student loans, etc.) to your gross monthly income. A lower DTI indicates you have more disposable income available to comfortably cover your new car payment.

Lenders typically prefer a DTI below 36%, though some may go higher depending on other factors like your credit score. A high DTI signals to lenders that you might be overextended financially, increasing their risk. This could lead to a higher interest rate or even a denial of your loan application.

To improve your DTI, consider paying down existing debts or increasing your income before applying for a consumer car loan. Managing your DTI proactively shows financial responsibility and significantly strengthens your position as a borrower.

Where to Find Your Consumer Car Loan: Exploring Lender Options

The landscape of car financing is diverse, offering various avenues to secure your auto loan. Each type of lender has its own advantages and disadvantages, and understanding them will empower you to choose the best fit for your needs. Don’t limit yourself to the first offer you receive; shopping around is key.

Dealership Financing: Convenience at a Cost?

Dealerships often offer their own car financing options, acting as intermediaries between you and various lenders. The convenience of handling the car purchase and financing in one place is undeniable. They can sometimes offer attractive promotional rates, especially on new car loans, to move inventory.

However, based on my experience, dealership financing might not always present you with the absolute best rates available. Their primary goal is to sell cars, and while they can be competitive, they might not shop as extensively on your behalf as you would yourself. It’s always wise to arrive at the dealership with a pre-approved loan in hand, giving you a strong negotiating position.

Banks: The Traditional Route

Major banks are a traditional and reliable source for consumer car loans. They typically offer competitive rates, especially if you have a strong credit history and an existing relationship with them. The application process is generally straightforward, and they provide a sense of security and trust.

When approaching banks, you’ll usually apply directly, and they will assess your creditworthiness. While their rates can be excellent, their approval processes might be more stringent, and they may have less flexibility than some other lenders. It’s a solid choice for those with established credit and a preference for conventional institutions.

Credit Unions: Member Benefits and Lower Rates

Credit unions are non-profit financial cooperatives owned by their members. This structure often translates into lower interest rates on loans and higher returns on savings compared to traditional banks. If you’re eligible to join a credit union (often based on location, employer, or association), they can be an excellent source for vehicle financing.

Pro tips from us: Many credit unions offer highly competitive auto loan rates and may be more flexible with borrowers who have less-than-perfect credit, especially if they are existing members. They focus on member welfare, which can lead to a more personalized and supportive loan experience.

Online Lenders: Speed, Convenience, and Comparison

The rise of online lenders has revolutionized the car financing landscape. These platforms offer a quick, convenient way to apply for a consumer car loan from the comfort of your home. Many online lenders specialize in different credit profiles, from excellent to fair, providing options for a wider range of borrowers.

Their primary advantages include speed of approval, competitive rates due to lower overheads, and the ability to easily compare multiple offers without visiting various physical locations. However, ensure you choose reputable online lenders by checking reviews and their financial credentials. Their digital-first approach makes them a strong contender for efficient loan application processing.

The Consumer Car Loan Application Process: A Step-by-Step Guide

Navigating the consumer car loan application doesn’t have to be daunting. By breaking it down into manageable steps, you can approach the process with confidence and increase your chances of securing the best vehicle financing terms.

Step 1: Determine Your Budget and Affordability

Before you even glance at cars, figure out what you can realistically afford. This isn’t just about the monthly payments; it includes insurance, fuel, maintenance, and potential registration fees. A good rule of thumb is that your total car expenses (loan payment, insurance, fuel) shouldn’t exceed 10-15% of your gross monthly income.

Our expert advice suggests using online calculators to estimate potential monthly payments based on different loan amounts, interest rates, and loan terms. This step is crucial for setting a realistic price range for your car. For a deeper dive into car budgeting, check out our Ultimate Guide to Car Budgeting.

Step 2: Check and Improve Your Credit Score

As discussed, your credit score is paramount. Obtain a free copy of your credit report from AnnualCreditReport.com. Review it for accuracy and dispute any errors. If your score is lower than desired, take steps to improve it, such as paying down existing debts or making all payments on time.

Common mistakes to avoid are applying for a loan without knowing your credit score. Each loan application can result in a "hard inquiry" on your credit report, which can slightly lower your score. It’s better to be informed and prepared. For tips on boosting your score, read our article: How to Boost Your Credit Score Fast.

Step 3: Get Pre-Approved for Your Auto Loan

Getting pre-approval from multiple lenders (banks, credit unions, online lenders) before visiting a dealership is a game-changer. Pre-approval gives you a clear understanding of how much you can borrow, at what interest rate, and for what loan term. It turns you into a cash buyer in the eyes of the dealership.

Based on my experience, arriving at the dealership with a pre-approval letter gives you significant leverage. You’re not relying solely on the dealer’s financing options, which means you can negotiate the car price and then compare the dealer’s financing offer against your pre-approved loan. Choose whichever is better.

Step 4: Gather Necessary Documents

Lenders will require various documents to process your loan application. These typically include:

- Proof of identity (driver’s license, passport)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residence (utility bill, lease agreement)

- Social Security Number

- Information about the vehicle you intend to purchase (if known)

Having these documents ready expedites the process and demonstrates your preparedness. It makes the car financing journey smoother for both you and the lender.

Step 5: Compare Offers and Read the Fine Print

Once you have multiple pre-approval offers, compare them meticulously. Look beyond just the monthly payments. Focus on the APR, total interest paid, any origination fees, and prepayment penalties. Don’t be afraid to ask questions if anything is unclear.

Pro tips from us: Pay close attention to the loan terms and any additional clauses. Understand the difference between fixed and variable interest rates, and ensure there are no hidden fees. A thorough review of the loan agreement before signing is non-negotiable for smart consumer car loan management.

Common Mistakes to Avoid When Taking Out a Car Loan

Even with careful planning, it’s easy to fall into common traps when seeking car financing. Being aware of these pitfalls can save you money, stress, and potential long-term financial headaches.

- Focusing Only on Monthly Payments: This is perhaps the most prevalent mistake. A low monthly payment can be achieved by extending the loan term or accepting a higher interest rate, both of which increase the total cost of the car significantly. Always consider the total amount you’ll pay over the life of the loan.

- Not Getting Pre-Approved: As highlighted earlier, skipping pre-approval leaves you vulnerable to dealership financing that may not be the most competitive. It removes your negotiation leverage and limits your options.

- Extending the Loan Term Too Much: While a longer loan term (e.g., 72 or 84 months) offers lower monthly payments, it almost always means paying substantially more in total interest. It also increases the risk of negative equity, where you owe more than the car is worth, especially for a used car loan.

- Skipping the Down Payment: While zero-down loans exist, they are generally less favorable. A lack of a down payment means borrowing the entire car price, leading to higher monthly payments and more interest. It also means you have no immediate equity in the vehicle.

- Ignoring the Total Cost of Ownership: Beyond the consumer car loan itself, factor in insurance, maintenance, fuel, and registration. A car that seems affordable on paper might be a financial burden once all costs are considered.

- Not Comparing Multiple Offers: Settling for the first auto loan offer you receive is a surefire way to miss out on potentially better rates and terms. Always compare offers from at least 3-4 different lenders.

- Being Dishonest on Your Application: Providing false information on your loan application can lead to severe consequences, including loan denial, legal issues, and damage to your creditworthiness. Always be truthful and transparent.

Pro Tips for Securing the Best Consumer Car Loan

Armed with knowledge of the process and potential pitfalls, here are some expert strategies to ensure you secure the most advantageous consumer car loan terms possible:

- Improve Your Credit Score Proactively: Start months before you plan to buy a car. Pay bills on time, reduce credit card balances, and avoid opening new lines of credit. A higher score is your most powerful tool.

- Save for a Larger Down Payment: The more you put down, the less you borrow, the lower your monthly payments, and the less interest you pay overall. It’s a fundamental principle of smart car financing.

- Negotiate the Car Price Before Discussing Financing: This is crucial. Treat the car purchase and the loan as separate transactions. Agree on the car’s price first, then discuss how you’ll pay for it (cash, your pre-approved loan, or the dealer’s financing if it’s better).

- Consider a Co-Signer if Needed: If you have limited or poor credit, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. Just ensure both parties understand the responsibilities.

- Explore Refinancing Options: If you already have a consumer car loan but your credit score has improved, or interest rates have dropped, consider refinancing. This can lower your interest rate, reduce your monthly payments, or shorten your loan term, saving you money over time.

- Be Patient and Don’t Rush: Car buying can be an emotional decision, but financial decisions require a cool head. Take your time, do your research, and don’t feel pressured into a purchase or a loan that doesn’t feel right.

Beyond the Purchase: Managing Your Car Loan Responsibly

Securing the consumer car loan is just the beginning. Responsible management throughout the loan term is vital for your financial well-being and maintaining good credit.

Making timely monthly payments is paramount. Late payments not only incur fees but also negatively impact your credit score, making future borrowing more expensive. Set up automatic payments to avoid missing due dates. Understand if your loan has any prepayment penalties. While rare for most standard auto loans, some lenders might charge a fee if you pay off your loan early. Knowing this helps you decide if accelerating your payments is truly beneficial.

Finally, keep an eye on market interest rates and your credit health. If rates drop significantly or your credit score improves substantially, revisiting refinancing could be a smart move. It allows you to potentially secure a better deal, reducing your overall cost of vehicle financing.

For more detailed information on consumer financial protection, you can consult trusted external sources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

Drive Smart, Finance Smarter: Your Journey to Confident Car Ownership

Navigating the world of consumer car loans might seem daunting initially, but with the right knowledge and a strategic approach, it becomes a powerful tool for achieving your car ownership dreams. We’ve covered the crucial factors influencing your loan, explored diverse lender options, walked through the application process, and highlighted common pitfalls to avoid.

Remember, the goal isn’t just to get a car, but to get a car on terms that are financially sound and sustainable for you. By understanding your credit score, maximizing your down payment, diligently comparing interest rates and loan terms, and getting pre-approval, you empower yourself to make intelligent car financing decisions.

Your journey to a new vehicle should be exciting, not stressful. By embracing these insights, you’re not just buying a car; you’re investing wisely in your future mobility. Drive smart, finance smarter, and enjoy the open road ahead with confidence!