Decoding the Numbers: Your Ultimate Guide to the Average APR for Used Car Loans

Decoding the Numbers: Your Ultimate Guide to the Average APR for Used Car Loans Carloan.Guidemechanic.com

Navigating the world of used car financing can feel like deciphering a complex code. One of the most critical pieces of this puzzle is the Annual Percentage Rate, or APR. Understanding the average APR for a used car loan isn’t just about knowing a number; it’s about empowering yourself to make smart financial decisions, save money, and drive away with confidence.

As an expert blogger and professional SEO content writer who has extensively researched and written about automotive finance for years, I understand the nuances that can make or break your deal. This comprehensive guide will peel back the layers, revealing everything you need to know about used car loan APRs, how they’re determined, and crucially, how you can secure the best rate possible. Our ultimate goal is to arm you with the knowledge to navigate the market like a pro.

Decoding the Numbers: Your Ultimate Guide to the Average APR for Used Car Loans

What Exactly is APR and Why Does It Matter for Your Used Car Loan?

Before we dive into averages, let’s clarify what APR truly represents. Many people mistakenly believe the interest rate is the only cost associated with borrowing money. While the interest rate is a significant component, the Annual Percentage Rate (APR) provides a more holistic view of your loan’s actual cost.

APR encompasses not only the stated interest rate but also any additional fees charged by the lender, such as origination fees, processing fees, or discount points. These fees are rolled into the overall cost, expressed as a yearly percentage. This means the APR gives you a clearer, more accurate picture of what you’ll pay over the life of the loan. It’s the single best metric for comparing different loan offers side-by-side.

For example, a loan with a lower interest rate but higher fees might actually have a higher APR than a loan with a slightly higher interest rate but no fees. Always compare APRs, not just interest rates, to ensure you’re getting the best deal. This is a fundamental principle in personal finance that many overlook when they’re excited about a new vehicle.

The Current Landscape: What is the Average APR for Used Car Loans Today?

Determining a single, definitive "average APR for a used car loan" is challenging because rates are constantly in flux. They are influenced by a myriad of factors, from broader economic conditions to your personal financial profile. However, based on current market trends and data from reputable financial institutions, we can identify general ranges.

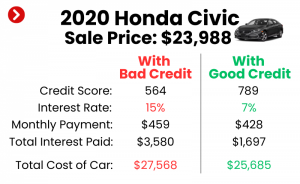

Generally, for borrowers with excellent credit (typically FICO scores 720+), you might see used car loan APRs ranging from 5% to 9%. For those with good credit (660-719), rates often fall between 9% and 13%. If your credit score is fair or needs improvement (below 660), rates can escalate significantly, potentially reaching 15% or even higher, sometimes into the 20s.

These figures are averages and can fluctuate based on the specific lender, the vehicle’s age, and the loan term. Economic indicators like the Federal Reserve’s benchmark interest rates play a significant role. When the Fed raises rates, borrowing costs for consumers typically increase across the board, including for used car loans. Conversely, lower Fed rates can lead to more attractive loan offers. Always check current market conditions when you’re ready to apply.

Key Factors That Significantly Influence Your Used Car Loan APR

Your APR isn’t arbitrary; it’s a carefully calculated reflection of the risk you present to a lender. Several critical factors come into play, each weighing heavily on the final rate you’re offered. Understanding these elements is your first step toward securing a more favorable loan.

1. Your Credit Score: The Undisputed King of Factors

Without a doubt, your credit score is the single most influential factor determining your used car loan APR. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your loan on time. A higher credit score signals a lower risk, translating into lower interest rates and a more attractive APR.

- Excellent Credit (720-850 FICO): Borrowers in this tier typically qualify for the lowest available rates. Lenders view them as highly reliable.

- Good Credit (660-719 FICO): You’ll still get competitive rates, but they might be a percentage point or two higher than those with excellent credit.

- Fair Credit (600-659 FICO): Rates begin to climb noticeably. Lenders perceive a moderate risk here, so they charge more to offset it.

- Poor Credit (Below 600 FICO): Expect significantly higher APRs. Lenders see a substantial risk, and the rates reflect that. In some cases, securing a loan might be challenging without a co-signer or a larger down payment.

Based on my experience, consistently paying bills on time, keeping credit utilization low, and avoiding new credit inquiries right before applying for a loan are paramount to maintaining a strong credit profile. Check your credit report regularly for errors; it can save you hundreds, if not thousands, of dollars over the life of a loan.

2. Loan Term (Length of the Loan): Balancing Monthly Payments and Total Cost

The length of your loan, or its term, directly impacts your APR and the total amount of interest you’ll pay. Common terms for used car loans range from 36 months (3 years) to 72 months (6 years), and sometimes even longer.

- Shorter Loan Terms (e.g., 36 or 48 months): Generally come with lower APRs. Lenders face less risk over a shorter period, and you’ll pay less interest overall. However, your monthly payments will be higher.

- Longer Loan Terms (e.g., 60 or 72 months): Often have higher APRs. The extended repayment period increases the lender’s risk, so they charge more. While monthly payments are lower and seem more affordable, you’ll pay significantly more in total interest over the life of the loan. This can also lead to negative equity (being "upside down" on your loan) for a longer period, especially with used cars that depreciate quickly.

Pro tips from us: While lower monthly payments can be tempting, carefully consider the total cost of the loan. A 72-month term might seem attractive now, but paying extra interest for years on a depreciating asset is a common mistake to avoid.

3. Down Payment: Reducing Risk and Your Loan Amount

The amount of money you put down upfront on a used car can significantly influence your APR. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk.

- Benefits of a Substantial Down Payment:

- Lower APR: Lenders see less risk and are more likely to offer a better rate.

- Reduced Loan Amount: You borrow less, meaning less interest paid overall.

- Lower Monthly Payments: A smaller principal balance results in more manageable monthly installments.

- Less Chance of Negative Equity: You’re less likely to owe more than the car is worth, especially important for used vehicles.

Common mistakes to avoid are neglecting a down payment entirely or making a very small one. While 0% down loans exist, they almost always come with higher APRs and place you at greater financial risk. Aim for at least 10-20% of the car’s purchase price if possible.

4. Vehicle Age and Mileage: Collateral Value and Risk

The characteristics of the used car itself play a role in its financing. Lenders consider the vehicle as collateral for the loan.

- Older or High-Mileage Vehicles: These cars typically depreciate faster and are perceived as higher risk by lenders. They may break down more often, making it harder for the borrower to repay the loan while also covering repair costs. As a result, lenders might offer higher APRs or require a larger down payment for such vehicles.

- Newer Used Cars (e.g., 1-3 years old): These usually hold their value better and are seen as less risky. This can lead to more favorable APRs compared to significantly older models.

From years of observing the market, lenders are often more comfortable financing vehicles that have a strong resale value, as it protects their investment if you default.

5. Lender Type: Banks, Credit Unions, Online Lenders, and Dealerships

Where you get your loan can have a noticeable impact on your APR. Different types of lenders have varying business models and risk tolerances.

- Banks: Offer competitive rates, especially for borrowers with good credit. They have established processes but can sometimes be slower.

- Credit Unions: Often known for offering some of the lowest APRs, as they are non-profit organizations focused on member benefits. They are an excellent option if you qualify for membership.

- Online Lenders: Provide convenience and quick approvals, with a wide range of rates depending on your credit profile. They can be very competitive.

- Dealership Financing: While convenient, dealerships act as intermediaries and may mark up the interest rate they receive from their lending partners to make a profit. It’s essential to compare their offer with pre-approvals from other sources.

Pro tips from us: Always get pre-approved from at least two or three independent lenders (banks, credit unions, online) before stepping into a dealership. This gives you leverage and a benchmark to compare against the dealer’s offer.

6. Debt-to-Income Ratio (DTI): Your Financial Capacity

Your debt-to-income (DTI) ratio is another crucial metric lenders use to assess your ability to take on new debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income.

- Lower DTI: A lower DTI indicates that you have plenty of income to cover your existing debts and the new car payment, making you a less risky borrower. This can lead to a better APR.

- Higher DTI: A high DTI suggests you might be overextended financially. Lenders may offer a higher APR to compensate for the increased risk, or even deny the loan. Most lenders prefer a DTI below 43%, but lower is always better.

Ensure you have a clear picture of your income and existing debt obligations before applying for a loan. This can also help you determine an affordable monthly payment.

7. Market Conditions and Federal Reserve Rates: The Economic Undercurrent

Beyond your personal financial situation, broader economic forces influence the average APR for used car loans.

- Federal Reserve Interest Rates: The Fed’s decisions on benchmark interest rates ripple throughout the economy. When the Fed raises rates to combat inflation, borrowing costs for consumers, including car loans, generally increase.

- Economic Outlook: During periods of economic uncertainty, lenders may become more cautious, leading to stricter lending criteria and potentially higher APRs. Conversely, in a robust economy, competition among lenders can drive rates down.

While you can’t control these macro factors, being aware of them helps you understand why rates might be higher or lower than expected.

How to Secure a Lower Used Car Loan APR: Actionable Strategies

Now that you understand what influences your APR, let’s turn our attention to actionable strategies you can employ to secure the most favorable rate possible. Every percentage point you save translates into real money over the life of your loan.

1. Boost Your Credit Score Before You Apply

This is arguably the most impactful step you can take. A higher credit score directly correlates with a lower APR.

- Review Your Credit Report: Obtain your free credit reports from AnnualCreditReport.com and meticulously check for any errors. Dispute inaccuracies immediately, as they can drag down your score.

- Pay Bills On Time, Every Time: Payment history is the biggest factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Your Debt: Lowering your credit card balances reduces your credit utilization ratio (the amount of credit you’re using compared to your total available credit), which positively impacts your score.

- Avoid New Credit Inquiries: Try not to open new credit accounts in the months leading up to your car loan application, as this can temporarily ding your score.

Based on my experience, even a 20-point jump in your FICO score can move you into a better credit tier, unlocking significantly lower APRs.

2. Shop Around for Lenders – Get Pre-Approved!

This cannot be stressed enough: do not rely solely on dealership financing. Getting pre-approved by multiple lenders is one of the most powerful tools you have.

- Contact Various Institutions: Reach out to your bank, local credit unions, and reputable online lenders. Apply for pre-approval with each.

- Understand Pre-Approval: Pre-approval gives you a conditional loan offer, including an estimated APR, based on a soft credit inquiry (which doesn’t harm your score). This allows you to compare offers without commitment.

- Use the "Shopping Window": Multiple hard credit inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, minimizing the impact on your credit score. This gives you time to shop rates.

Pro tips from us: Walking into a dealership with a pre-approval in hand transforms you from a vulnerable buyer into a powerful, informed negotiator. It forces the dealer to either match or beat your external offer.

3. Make a Larger Down Payment

As discussed, a substantial down payment reduces the loan amount and the lender’s risk, often resulting in a lower APR.

- Save Up: Prioritize saving for a down payment before you even start car shopping.

- Consider Selling Your Current Car: If you have a vehicle to trade in, treat its value as a down payment. Ensure you understand its true market value before negotiations.

One common mistake I’ve seen is buyers underestimating the power of a down payment. Even an extra few hundred or thousand dollars can make a difference in your APR and overall cost.

4. Choose a Shorter Loan Term (If Affordable)

While longer terms offer lower monthly payments, they almost always come with higher APRs and significantly more interest paid over time.

- Assess Your Budget: Determine the maximum monthly payment you can comfortably afford.

- Balance Cost and Affordability: Opt for the shortest loan term that fits your budget. For instance, if you can afford a 48-month term, choose that over a 60-month term, even if the monthly payment is slightly higher. The long-term savings on interest will be substantial.

This strategy is key to minimizing your total cost of ownership for a used car.

5. Consider a Co-signer (If Necessary)

If your credit score is fair or poor, or you have limited credit history, a co-signer with excellent credit can help you secure a better APR.

- Benefits: The co-signer’s strong credit profile reduces the lender’s risk, potentially leading to a lower APR and higher chance of approval.

- Risks: Both you and the co-signer are equally responsible for the loan. If you miss payments, it negatively impacts both credit scores, and the co-signer is legally obligated to make the payments. Only consider this option with someone you trust implicitly and who understands the full implications.

This can be a valuable tool for first-time buyers or those rebuilding credit, but it requires careful consideration.

6. Negotiate the Car Price

Remember that the loan is for the price of the car. A lower purchase price means you’re borrowing less, which directly reduces your total interest paid, even if the APR remains the same.

- Research Market Value: Use resources like Kelley Blue Book (KBB.com) or Edmunds to understand the fair market value of the used car you’re interested in.

- Separate Negotiations: Try to negotiate the car’s price independently of the financing. This prevents the dealer from shifting costs between the two.

A good deal on the car itself is the first step toward a good deal on the financing.

Common Mistakes to Avoid When Financing a Used Car

Even savvy buyers can fall into traps when financing a used car. Being aware of these common pitfalls can save you time, money, and headaches.

- Focusing Only on Monthly Payments: This is perhaps the biggest mistake. Dealers often try to "sell" you on a monthly payment, extending the loan term to make it seem affordable. Always ask for the total cost of the loan and the APR. A low monthly payment over 72 or 84 months can mean paying thousands more in interest.

- Not Getting Pre-Approved: As mentioned, skipping pre-approval means you go into negotiations blind, without a benchmark to compare the dealer’s offer against. This puts you at a significant disadvantage.

- Ignoring the Total Cost of the Loan: Add up the principal amount borrowed plus all the interest you’ll pay over the loan term. This figure reveals the true cost of your financing.

- Extending Loan Terms Too Long: While tempting for lower monthly payments, excessively long terms (e.g., 72 or 84 months for a used car) increase your total interest, put you at higher risk of negative equity, and mean you’re making payments long after the car has significantly depreciated.

- Not Reading the Fine Print: Always thoroughly review all loan documents before signing. Look for hidden fees, prepayment penalties, and ensure the APR matches what was discussed. If something seems unclear, ask for clarification.

Pro tips from us: Don’t let the excitement of a new car rush you. Take your time, do your due diligence, and be prepared to walk away if the deal isn’t right.

When Refinancing Your Used Car Loan Makes Sense

Sometimes, you might find yourself with a less-than-ideal used car loan APR, perhaps because your credit wasn’t great when you first bought the car, or interest rates have dropped since. Refinancing can be a smart move in certain situations.

- Lower Your APR: If your credit score has improved significantly since you took out the original loan, or if current market interest rates are lower, you might qualify for a lower APR through refinancing.

- Reduce Monthly Payments: A lower APR or a longer (but still reasonable) loan term through refinancing can decrease your monthly payments, freeing up cash flow.

- Change Loan Terms: You might want to switch from a variable-rate loan to a fixed-rate loan, or adjust the length of your repayment period.

The process for refinancing is similar to applying for an initial loan. You’ll shop around with different lenders, get pre-approved, and compare offers. Be sure to calculate how much you’ll save over the remaining term of your loan to ensure refinancing is truly beneficial after any potential fees. For more insights into managing your car payments, you might find our article on (placeholder for internal link) helpful.

Pro Tips from an Expert Blogger: Your Financial Advantage

Having guided countless readers through the intricacies of auto financing, I’ve distilled some key insights that truly set informed buyers apart. These aren’t just tips; they’re foundational principles for financial success when buying a used car.

- Knowledge is Power: The more you understand about APR, credit scores, and lending practices, the better equipped you are to negotiate and secure a favorable deal. Don’t assume the dealer or lender will always have your best interest at heart; empower yourself with information.

- Patience Pays Off: Rushing into a purchase, especially under pressure, often leads to costly mistakes. Take your time to research, compare, and deliberate. A few extra days of preparation can save you thousands.

- Separate the Deals: Always negotiate the price of the car first, then discuss financing. When these are bundled, it’s easier for dealerships to manipulate figures to their advantage.

- Read Everything Carefully: This might sound obvious, but it’s astonishing how many people sign contracts without fully understanding them. Ask questions until you’re completely clear on all terms and conditions.

Remember, your goal isn’t just to get approved for a loan; it’s to get approved for the best possible loan that aligns with your financial goals. By applying these strategies, you’re not just buying a car; you’re making a sound financial investment. You can also explore resources like the Consumer Financial Protection Bureau’s auto loan guide for more government-backed advice on auto financing.

Conclusion: Driving Forward with Confidence

Understanding the average APR for a used car loan is more than just knowing a benchmark; it’s about recognizing the levers you can pull to influence your own financial outcome. From meticulously building your credit score to diligently shopping around for lenders, every step you take to prepare can translate into significant savings over the life of your loan.

Don’t let the complexity of financing deter you. Arm yourself with knowledge, ask the right questions, and approach the car-buying process with a strategic mindset. By doing so, you’ll not only secure a more favorable APR but also ensure your used car purchase is a smart, financially sound decision. Drive forward with confidence, knowing you’ve done your homework and secured the best possible deal. For further reading on managing your finances, check out our insights on (placeholder for internal link).