Decoding the Partial Approval Car Loan: Your Ultimate Guide to Driving Away with Confidence

Decoding the Partial Approval Car Loan: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Getting a new car is an exciting milestone, a symbol of freedom and independence for many. However, the path to vehicle ownership often involves navigating the complexities of car loans. For some, the journey hits a speed bump in the form of a "partial approval car loan." This isn’t an outright rejection, but rather an indication that a lender is willing to work with you, albeit with certain conditions.

Understanding a partial approval can feel like deciphering a cryptic message. You know you’re close, but what exactly do you need to do to get the full green light? This comprehensive guide will demystify the partial approval car loan, explaining what it means, why it happens, and most importantly, how you can turn that conditional offer into a successful vehicle purchase. We’ll provide actionable strategies, share expert insights, and help you navigate this common scenario with confidence and clarity.

Decoding the Partial Approval Car Loan: Your Ultimate Guide to Driving Away with Confidence

What Exactly is a Partial Approval Car Loan?

Imagine you’re applying for something important, and instead of a simple "yes" or "no," you receive a "yes, but…" That’s essentially what a partial approval car loan is. It means the lender has reviewed your application and, while they see potential for you to be a borrower, your current financial profile doesn’t quite meet all their standard criteria for an unconditional loan. They’re not saying "no" to lending you money; they’re saying "yes, if you can meet these additional requirements."

This conditional offer serves as a bridge between a full approval and a complete denial. Lenders use it as a risk mitigation strategy. They want to lend money and make a profit, but they also need to protect their investment. By offering a partial approval, they signal their willingness to lend while also setting terms that reduce their perceived risk, based on the information you’ve provided.

For instance, you might have a good income but a limited credit history, or perhaps an excellent credit score but a high debt-to-income ratio. These factors can make a lender hesitant to offer a standard loan without some adjustments. A partial approval then becomes an invitation for further discussion and potential adjustments to the loan terms or your application.

The Underlying Reasons for Partial Approval

Several factors contribute to a lender’s decision to issue a partial approval instead of a full one. Understanding these reasons is the first step toward addressing them and securing your car loan. Based on my experience in the financial sector, these typically revolve around perceived risks associated with the borrower’s ability to repay the loan.

Let’s break down the most common culprits:

Your Credit Score and History

A low or inconsistent credit score is often the primary reason for partial approval. Lenders rely heavily on your credit report to assess your financial responsibility. A score below their preferred threshold, or a history riddled with late payments, defaults, or bankruptcies, signals a higher risk. They might see that you’ve managed credit in the past, but perhaps not perfectly, prompting them to proceed with caution.

Even a "thin" credit file, meaning you haven’t used credit much, can lead to partial approval. Lenders lack sufficient data to predict your repayment behavior, making them hesitant to offer an unconditional loan. They need more assurance than what your current credit history provides.

Debt-to-Income (DTI) Ratio

Your debt-to-income ratio is a crucial indicator of your financial health. This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. If your DTI is too high, it suggests that a significant portion of your income is already allocated to existing debts, leaving less disposable income to comfortably manage another loan payment.

Lenders want to ensure you have enough financial breathing room. A high DTI might not disqualify you entirely, but it will certainly make them nervous, leading to a conditional offer. They want to see that you can handle the new car payment without undue strain on your budget.

Employment History

Stability in employment is another key factor. Lenders prefer to see a consistent work history, ideally with the same employer for a significant period (e.g., two years or more). Frequent job changes, short employment stints, or being newly employed can raise concerns about your income stability. They might worry about your ability to maintain a steady income stream to make timely loan payments.

While being self-employed or working on contract is increasingly common, it can also present challenges. Lenders often require more extensive documentation and a longer history of consistent income for these types of employment, as the income can sometimes be less predictable than a standard salaried position.

Insufficient Down Payment

A down payment demonstrates your commitment to the purchase and reduces the amount you need to borrow. If your proposed down payment is too small, or non-existent, the lender bears more risk. A larger loan amount means higher monthly payments and a greater potential for default.

A substantial down payment, conversely, reduces the loan-to-value (LTV) ratio of the vehicle. This means if you default, the lender is less likely to lose money if they have to repossess and sell the car. A partial approval might indicate that the lender wants you to put more money down to reduce their exposure.

Vehicle Choice

Believe it or not, the car you choose can also influence your loan approval. Lenders consider the vehicle’s age, mileage, make, and model. An older car, one with very high mileage, or a less popular model might be deemed a higher risk. This is because such vehicles can depreciate rapidly or be difficult to sell if the lender needs to repossess it.

Similarly, choosing a car that is significantly more expensive than what your income and credit profile suggest you can comfortably afford can also lead to partial approval. Lenders will often compare the car’s price to your financial capacity to ensure the loan is responsible.

Missing Documentation

Sometimes, partial approval isn’t about your financial standing but simply about incomplete information. Lenders require a host of documents to verify your identity, income, and residency. If you’ve missed providing a pay stub, bank statement, or proof of address, the lender can’t fully assess your application. They’ll issue a conditional approval pending the submission of the missing paperwork.

This is a relatively easy fix, but it’s a common oversight. Always double-check that you’ve submitted all requested documents accurately and promptly.

Decoding the Lender’s Conditions: What Does "Partial" Mean for You?

When a lender offers a partial approval, it always comes with specific conditions. These conditions are not arbitrary; they are designed to mitigate the risks identified in your application. Understanding what these conditions mean for you is crucial for deciding your next steps.

Here are some common conditions you might encounter:

Higher Interest Rate

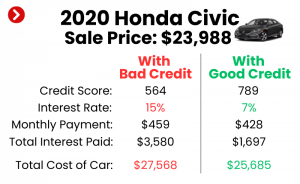

This is perhaps the most frequent condition. If your credit score or financial profile indicates a higher risk, lenders will often compensate by charging a higher Annual Percentage Rate (APR). This means you’ll pay more in interest over the life of the loan. The higher interest rate acts as a premium for the increased risk the lender is taking.

While a higher APR can be disheartening, it’s often the lender’s way of making the loan feasible for them. It’s important to calculate the total cost of the loan with this higher rate to ensure it still fits within your budget.

Larger Down Payment Required

As discussed, a significant down payment reduces the lender’s risk. If your initial down payment was deemed insufficient, the lender might stipulate that you increase it to a certain percentage of the vehicle’s price. This lowers the loan amount, thereby reducing the lender’s exposure and potentially making the monthly payments more manageable for you.

Pro tips from us: Even if not required, offering a larger down payment voluntarily can strengthen your application and potentially lower your interest rate. It shows financial prudence and commitment.

Shorter Loan Term

Lenders might also propose a shorter loan term than you initially requested. While a shorter term means higher monthly payments, it also means you’ll pay off the loan faster and typically incur less interest over time. From the lender’s perspective, a shorter term reduces the period during which you could default, thereby lowering their risk.

This condition might require you to adjust your budget to accommodate the higher monthly payments. It’s a trade-off between affordability per month and the overall cost of the loan.

Co-signer Requirement

If your credit history is limited or your income isn’t quite strong enough on its own, the lender might require a co-signer. A co-signer is someone with good credit and a strong financial standing who agrees to be equally responsible for the loan. If you fail to make payments, the co-signer is legally obligated to do so.

Having a co-signer significantly reduces the lender’s risk, as they now have two parties to pursue for repayment. While a co-signer can be a great help, it’s a serious commitment for the individual, as it impacts their credit and financial obligations.

Different Vehicle Choice

Sometimes, the issue isn’t just your financial profile but the specific vehicle you’ve chosen. If the car is too expensive, too old, or has other attributes that make it a higher risk in the lender’s eyes, they might approve you but with the condition that you select a different vehicle. This could mean choosing a less expensive model, a newer used car, or one with lower mileage.

This condition often reflects the lender’s internal valuation of the collateral. They want to ensure that the car’s value adequately covers the loan amount throughout the term.

Proof of Additional Income or Assets

In some cases, especially for self-employed individuals or those with complex financial situations, a lender might request additional documentation beyond what was initially submitted. This could include more bank statements, tax returns, or proof of other assets that demonstrate your financial stability and capacity to repay the loan. They are looking for a clearer and more robust picture of your overall financial health.

Your Action Plan: Turning Partial Approval into Full Approval

Receiving a partial approval is not the end of your car buying journey; it’s a call to action. With a strategic approach, you can often meet the lender’s conditions and secure the full approval you need.

Here’s your step-by-step action plan:

Step 1: Understand the Specific Conditions

The very first thing you must do is clearly understand why you received a partial approval and what the specific conditions are. Don’t guess. Contact the lender or the dealership’s finance manager immediately and ask for a detailed explanation. Get clarity on every requirement.

Ask questions like: "What specific criteria did my application fall short on?" "What exactly do I need to do to satisfy these conditions?" "Are there any alternative ways to meet these requirements?" The more information you have, the better equipped you’ll be to respond effectively.

Step 2: Improve Your Financial Profile (Short-Term & Long-Term)

This step involves actively working to meet the lender’s demands or strengthen your overall application.

- Increase Your Down Payment: If the lender requires a larger down payment, explore options to gather more funds. Can you tap into savings, sell an unused item, or get a small short-term loan from a trusted family member? Every additional dollar you put down reduces the amount you need to borrow and makes your application stronger.

- Find a Co-signer: If a co-signer is required, approach a trusted family member or friend with a strong credit history. Be transparent about the responsibility involved and ensure they understand the implications for their own credit. A co-signer can be a game-changer for approval.

- Choose a Less Expensive Car: If your current vehicle choice is the issue, consider a more affordable model. Look at cars that are a few years older, have slightly higher mileage, or a less premium trim level. Sometimes, a modest adjustment in vehicle choice can significantly improve your chances of full approval.

- Address Credit Report Errors: Pro tips from us: Before even applying for a loan, always check your credit report. If you find any inaccuracies, dispute them immediately with the credit bureaus. Removing errors can sometimes boost your score enough to meet lender criteria. While this can take time, it’s a crucial long-term strategy for all financial endeavors.

- Reduce Existing Debt (If Possible Quickly): While not always feasible in the short term, if you have a small outstanding debt that you can quickly pay off, doing so can improve your debt-to-income ratio. Even a slight reduction can sometimes make a difference in the lender’s assessment.

- Provide Additional Documentation: If missing paperwork was the issue, gather and submit everything requested promptly. Ensure all documents are clear, current, and accurately reflect your financial situation.

Step 3: Negotiate Wisely

Don’t simply accept the first conditional offer. Once you understand the terms, see if there’s room for negotiation. Can you offer a slightly larger down payment in exchange for a slightly lower interest rate? Can you provide additional proof of income or assets to counter a co-signer requirement?

Be polite but firm in your discussions. Show the lender that you are a responsible borrower willing to work with them. Sometimes, a small adjustment on either side can lead to a mutually agreeable solution.

Step 4: Explore Other Lenders

Common mistakes to avoid are putting all your eggs in one basket. Just because one lender issued a partial approval doesn’t mean all others will. Different lenders have different risk appetites and lending criteria. If you’re unable to meet the conditions of one lender, consider applying to a few others.

However, be mindful of multiple hard inquiries on your credit report, which can temporarily lower your score. It’s generally advised to do all your car loan applications within a short window (e.g., 14-45 days) so they count as a single inquiry for scoring purposes.

The Role of Credit Score in Car Loan Approvals

Your credit score is often the first thing a lender looks at, and for good reason. It’s a numerical representation of your creditworthiness, derived from your credit history. FICO and VantageScore are the most common models, with scores typically ranging from 300 to 850. A higher score indicates lower risk to lenders.

Lenders categorize scores into different tiers:

- Excellent (780-850): Best rates, easiest approval.

- Very Good (740-779): Still excellent rates, strong approval chances.

- Good (670-739): Good rates, standard approval.

- Fair (580-669): Higher rates, more scrutiny, common for partial approvals.

- Poor (300-579): Subprime loans, very high rates, often requires co-signer or significant down payment.

If your score falls into the "Fair" or "Poor" categories, a partial approval is highly likely. Lenders see your history and assess the likelihood of default as higher. They want to protect their investment.

Strategies for improving your credit before applying are invaluable. These include paying all bills on time, keeping credit utilization low, and avoiding opening too many new credit accounts. For a deeper dive into improving your credit score, check out our guide on Mastering Your Credit Score: Your Path to Financial Freedom. (Simulated internal link)

Common Mistakes to Avoid When Facing Partial Approval

Navigating a partial approval requires careful thought and strategic action. Making certain mistakes can hinder your progress or even worsen your financial situation.

Here are common pitfalls to steer clear of:

- Ignoring the Conditions: The worst thing you can do is pretend the conditions don’t exist or hope they’ll magically disappear. The lender has clearly stated what’s needed. Ignoring these requirements will lead to a full rejection. Address them head-on.

- Applying to Too Many Lenders at Once (Indiscriminately): While exploring other options is smart, applying to dozens of lenders within a short period can negatively impact your credit score. Each "hard inquiry" can slightly lower your score. As mentioned, consolidate your applications within a narrow timeframe to minimize the impact.

- Giving Up Too Soon: A partial approval isn’t a "no." It’s an opportunity. Many people get discouraged and walk away, missing out on a perfectly viable path to car ownership. Be persistent, understand the requirements, and actively work to meet them.

- Choosing a Car You Can’t Truly Afford: Even with a partial approval, ensure the car and the associated loan terms (including a potentially higher interest rate) genuinely fit within your budget. Don’t stretch yourself too thin just to get a car. Factor in insurance, maintenance, and fuel costs as well.

- Not Reading the Fine Print: Always, always read the entire loan agreement before signing. Understand the interest rate, loan term, all fees, prepayment penalties (if any), and what happens in case of default. If you have questions, ask. Don’t sign anything you don’t fully comprehend.

Beyond the Loan: What to Consider Before Buying

Securing a car loan, even after a partial approval, is only one part of the car ownership equation. To ensure long-term financial stability and enjoyment of your new vehicle, consider these additional points:

- Budgeting for Ownership Costs: A car loan payment is just the beginning. You’ll need to budget for auto insurance, which can be substantial, especially for newer or more expensive vehicles. Factor in fuel costs, routine maintenance (oil changes, tire rotations), and potential repairs. These ongoing expenses can quickly add up.

- Understanding the Total Cost of the Loan: Don’t just look at the monthly payment. Calculate the total amount you will pay over the life of the loan, including all interest and fees. A lower monthly payment over a very long term might seem attractive, but it often means paying significantly more in total interest.

- The Importance of Financial Literacy: Taking the time to educate yourself about personal finance, credit, and debt management will empower you beyond just this car loan. Understanding how interest works, the impact of your credit score, and responsible budgeting are skills that will serve you throughout your life. For more comprehensive financial planning advice, a great resource is the Consumer Financial Protection Bureau (CFPB) website, which offers unbiased information and tools to help you make informed financial decisions. (https://www.consumerfinance.gov/) (Simulated external link)

Conclusion

Receiving a partial approval car loan can initially feel like a setback, but it’s crucial to view it as an opportunity. It signifies that lenders are willing to work with you, provided you can address specific concerns. By understanding the reasons behind the conditional offer, proactively addressing the lender’s requirements, and making informed decisions, you can successfully navigate this common scenario.

Remember, a partial approval is not a rejection; it’s an invitation to refine your application and demonstrate your commitment. With the right strategy and a clear understanding of your financial situation, you can turn that "yes, but…" into a definitive "yes!" and confidently drive away in your new vehicle. Take control of your car buying journey, empower yourself with knowledge, and make the best choices for your financial future.