Decoding Your $46,000 Car Loan Payment: A Comprehensive Guide to Smart Auto Financing

Decoding Your $46,000 Car Loan Payment: A Comprehensive Guide to Smart Auto Financing Carloan.Guidemechanic.com

The thrill of a new car is undeniable. That sleek design, the new car smell, the promise of adventure – it’s an exciting prospect. But for most of us, that dream ride comes with a significant financial commitment: a car loan. If you’re considering financing a vehicle and anticipate a $46,000 car loan payment, understanding the intricacies of this commitment is paramount.

This isn’t just about a single monthly figure; it’s about a complex interplay of factors that will impact your budget for years to come. Our mission today is to demystify the $46,000 car loan payment, providing you with an in-depth, expert-backed guide to navigate auto financing confidently. By the end of this article, you’ll be equipped with the knowledge to make smart decisions, avoid common pitfalls, and ensure your dream car doesn’t become a financial burden.

Decoding Your $46,000 Car Loan Payment: A Comprehensive Guide to Smart Auto Financing

Understanding the $46,000 Car Loan: More Than Just a Monthly Figure

A $46,000 car loan represents a substantial investment, and approaching it with a clear understanding of all its components is crucial. This isn’t merely the sticker price of a car; it’s the amount you are borrowing after considering your down payment, trade-in value, and any additional fees or taxes that might be rolled into the loan.

Many prospective buyers mistakenly focus solely on the vehicle’s purchase price. However, the true loan amount often differs, and this figure forms the bedrock upon which your entire payment structure is built. It’s the principal amount that your lender expects you to repay, along with the added cost of borrowing.

Your monthly $46,000 car loan payment will be directly influenced by several key variables. These factors work in concert to determine how much you pay each month and, critically, the total amount you will ultimately spend over the life of the loan. Ignoring any of these elements can lead to unwelcome surprises down the road.

The Core Pillars of Your $46,000 Car Loan Payment

To truly grasp your potential $46,000 car loan payment, we must dissect the fundamental components that dictate its size and overall cost. Each of these pillars plays a critical role, and understanding their individual impact is essential for informed decision-making.

A. Loan Amount ($46,000): The Foundation

The $46,000 loan amount is the principal sum you are borrowing from a financial institution. This figure is the starting point for all your calculations and represents the money the lender is extending to you to purchase your vehicle. It’s important to clarify that this isn’t necessarily the vehicle’s purchase price.

Instead, the actual loan amount is derived from the car’s agreed-upon price, minus any down payment you make and the value of any trade-in vehicle. Conversely, it might also include additional costs like sales tax, registration fees, and extended warranties if you choose to roll them into your financing. Based on my experience, many people focus solely on the sticker price and forget to factor in these additional costs, which can significantly inflate the actual loan amount.

A larger initial loan amount, naturally, translates to higher monthly payments and a greater total interest paid over the life of the loan. Therefore, strategically reducing this principal amount from the outset is one of the most effective ways to lower your overall financial burden. Every dollar you don’t have to borrow is a dollar you don’t pay interest on.

B. Interest Rate (APR): The Cost of Borrowing

The interest rate, often expressed as the Annual Percentage Rate (APR), is arguably the most crucial factor determining the true cost of your $46,000 car loan payment. The APR is essentially the price you pay to borrow the money, calculated as a percentage of the principal loan amount. It directly impacts how much extra you’ll pay beyond the initial $46,000.

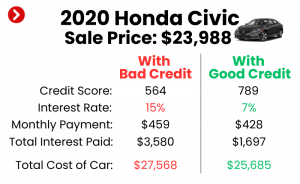

A lower APR means less money spent on interest over the loan term, resulting in lower monthly payments and significant savings overall. Conversely, a higher APR can drastically increase both your monthly payment and the total cost of the vehicle. Your credit score is the primary determinant of the interest rate you qualify for, with excellent credit scores typically securing the most favorable rates. Other factors include current market conditions, the loan term, and the specific lender you choose.

Pro tips from us: Always get pre-approved for a loan before stepping into a dealership. This gives you a benchmark rate and empowers you to negotiate better, as you know what a competitive rate looks like. Don’t be afraid to compare offers from multiple banks, credit unions, and online lenders. For a deeper dive into how APR works and its impact, you can refer to this informative article on Understanding APR by the Consumer Financial Protection Bureau.

C. Loan Term: How Long Will You Pay?

The loan term refers to the duration over which you agree to repay your $46,000 car loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This choice significantly impacts your monthly payment and the total interest you’ll pay. It’s a balancing act between affordability and overall cost.

Shorter loan terms, such as 36 or 48 months, come with higher monthly payments because you’re paying off the $46,000 principal in a shorter timeframe. However, the significant advantage is that you pay substantially less interest over the life of the loan. You also build equity in your vehicle faster and are free from car payments sooner.

Conversely, longer loan terms, like 72 or 84 months, offer lower monthly payments, making the car seem more affordable on a month-to-month basis. The downside is considerable: you’ll pay significantly more in total interest over the extended period. Common mistakes to avoid are automatically opting for the longest term just to achieve the lowest possible monthly payment without considering the increased overall cost and the risk of negative equity (owing more than the car is worth) as the vehicle depreciates.

D. Down Payment: Your Upfront Investment

A down payment is the initial amount of money you pay upfront towards the purchase of your vehicle, directly reducing the amount you need to borrow. For a $46,000 car loan, making a substantial down payment can have a profound positive impact on your financial future. It’s one of the most powerful tools you have to control your loan.

The primary benefit of a larger down payment is a reduced loan principal, which in turn leads to lower monthly payments. Less money borrowed also means less interest accrued over the life of the loan, saving you potentially thousands of dollars. Furthermore, a significant down payment helps mitigate the risk of negative equity, a situation where the car’s value depreciates faster than you pay off the loan.

From a financial planning perspective, a substantial down payment is often your best friend. While there’s no magic number, many financial experts recommend aiming for at least 10-20% of the vehicle’s purchase price, especially for new cars. This upfront investment signals financial stability to lenders and can sometimes even help you secure a slightly better interest rate.

Calculating Your Potential $46,000 Car Loan Payments: Real-World Scenarios

To illustrate how these factors interact, let’s look at a few hypothetical scenarios for a $46,000 car loan. Remember, these are estimates; your actual payment will depend on your specific loan terms and qualifications.

We’ll assume a fixed loan amount of $46,000 for all scenarios.

-

Scenario 1: Good Credit, Average Term

- Interest Rate (APR): 6.0%

- Loan Term: 60 months (5 years)

- Estimated Monthly Payment: Approximately $888

- Total Interest Paid: Approximately $7,280

-

Scenario 2: Excellent Credit, Shorter Term

- Interest Rate (APR): 4.0%

- Loan Term: 48 months (4 years)

- Estimated Monthly Payment: Approximately $1,042

- Total Interest Paid: Approximately $4,016

-

Scenario 3: Fair Credit, Longer Term

- Interest Rate (APR): 9.0%

- Loan Term: 72 months (6 years)

- Estimated Monthly Payment: Approximately $808

- Total Interest Paid: Approximately $12,976

As you can see, even with the same $46,000 car loan amount, your monthly payment and the total interest paid can vary wildly. A lower interest rate and a shorter term, while resulting in a higher monthly payment, save you a significant amount in interest over time. Conversely, a higher interest rate combined with a longer term can make the car considerably more expensive in the long run. We highly encourage using online car loan calculators to get precise estimates based on your specific figures.

Beyond the Monthly Payment: The True Cost of Car Ownership

While your $46,000 car loan payment is a significant part of your automotive budget, it’s far from the only expense. Overlooking these additional costs is a common financial misstep that can quickly turn an affordable monthly payment into an overwhelming financial burden. Understanding the true cost of car ownership is crucial for long-term financial stability.

Based on my experience, many first-time car buyers overlook these critical expenses, leading to budget strain down the line. Here are the other major costs you must factor in:

- A. Car Insurance: This is a non-negotiable expense. The cost of insurance varies widely based on the vehicle type, your driving record, age, location, and the coverage you choose. A more expensive car like one warranting a $46,000 loan will generally have higher insurance premiums.

- B. Maintenance & Repairs: Cars require regular maintenance – oil changes, tire rotations, brake inspections, and occasional repairs. While new cars come with warranties, these don’t cover everything, and unexpected issues can arise. It’s wise to budget a monthly amount for these inevitable costs.

- C. Fuel Costs: Unless you’re going electric, gasoline will be a recurring expense. Your daily commute, weekend trips, and the car’s fuel efficiency will dictate this cost. This can fluctuate with gas prices, making it a variable but essential budget item.

- D. Registration & Taxes: Annual registration fees and various local taxes are mandatory. These vary by state and municipality but are a recurring cost that needs to be accounted for. Don’t forget any initial sales tax that might not be rolled into your loan.

- E. Depreciation: While not an out-of-pocket expense, depreciation is the single largest cost of owning a new car. It’s the loss in value of your vehicle over time. Understanding this invisible cost helps you make smarter decisions about when to sell or trade in your car.

Factoring in all these costs will give you a much more realistic picture of what a $46,000 car loan truly entails for your monthly budget.

Strategies for Securing a Favorable $46,000 Car Loan

Obtaining the best possible terms for your $46,000 car loan requires proactive planning and smart strategies. Don’t just settle for the first offer; empower yourself with these tips to secure favorable financing.

Here’s how you can position yourself for success:

- A. Boost Your Credit Score: Your credit score is the most significant factor influencing your interest rate. Before applying for a loan, check your credit report for errors and work to improve your score. Pay bills on time, reduce existing debt, and avoid opening new lines of credit.

- B. Save for a Larger Down Payment: As discussed, a larger down payment directly reduces the loan amount and the interest you’ll pay. It also makes you a more attractive borrower. Aim for at least 10-20% of the vehicle’s price.

- C. Shop Around for Lenders: Never accept the dealer’s first financing offer without comparing it to others. Get quotes from multiple banks, credit unions, and online lenders. Pro tips from us: Always negotiate the car price and the loan terms separately; don’t let them blend the conversations.

- D. Get Pre-Approved: Getting pre-approved for a loan provides you with a clear budget and an interest rate benchmark before you even step onto a dealership lot. This gives you strong negotiating power and prevents you from falling in love with a car you can’t truly afford.

- E. Consider a Co-signer (if necessary): If your credit score isn’t ideal, a co-signer with excellent credit can help you qualify for a better interest rate. Be aware that the co-signer is equally responsible for the loan.

- F. Negotiate the Car Price: Every dollar you can shave off the vehicle’s purchase price directly reduces the amount you need to borrow. This has a ripple effect, lowering your monthly payments and the total interest paid on your $46,000 car loan.

What If a $46,000 Car Loan Payment Feels Too High?

After crunching the numbers, you might find that a $46,000 car loan payment, combined with other ownership costs, simply doesn’t fit comfortably into your budget. This is a common realization, and it’s a sign to re-evaluate rather than push forward into financial strain. There are several proactive steps you can take.

Firstly, re-evaluate the car itself. Is the vehicle you’re looking at truly within your means, or is there a slightly less expensive model or trim level that would still meet your needs? Sometimes, a minor adjustment in the vehicle choice can lead to significant savings on the loan amount. Secondly, consider certified pre-owned (CPO) vehicles. These often come with manufacturer warranties and have undergone rigorous inspections, offering a "like new" experience at a lower price point.

You could also increase your down payment, even if it means waiting a few more months to save. Every extra dollar you put down reduces the principal, leading to lower monthly payments. Lastly, if the numbers still don’t add up, it might be a sign to wait and save more before making such a significant purchase. For more guidance on budgeting for a car, check out our article on .

Refinancing Your $46,000 Car Loan

Even after you’ve secured your $46,000 car loan, your financial journey isn’t necessarily set in stone. Refinancing your auto loan can be a smart move under certain circumstances, potentially saving you money or adjusting your payment structure. This involves taking out a new loan to pay off your existing car loan, ideally with more favorable terms.

You might consider refinancing if interest rates have dropped since you took out your original loan, or if your credit score has significantly improved. A lower interest rate on the new loan will directly reduce your monthly payments and the total interest you pay over time. Another reason could be to adjust your loan term, either to shorten it for quicker payoff or extend it to lower monthly payments (though the latter increases total interest).

Before refinancing, carefully compare the new loan offer with your current loan, factoring in any fees associated with the new loan. Ensure the benefits outweigh the costs.

Common Mistakes to Avoid When Taking a $46,000 Car Loan

Navigating a substantial financial commitment like a $46,000 car loan can be complex, and it’s easy to fall into common traps. From years of observing consumer behavior, these are the pitfalls we consistently see that lead to financial regret. Avoiding them will put you in a much stronger position.

Here are critical mistakes to steer clear of:

- 1. Focusing Only on the Monthly Payment: This is perhaps the biggest mistake. Dealers often "work the numbers" to get you to a desired monthly payment, often by extending the loan term or increasing the interest rate. Always look at the total cost of the loan, including all interest.

- 2. Not Getting Pre-Approved: Walking into a dealership without a pre-approval from your bank or credit union leaves you vulnerable to potentially less favorable financing options offered by the dealer. You lose your negotiating power.

- 3. Ignoring the True Cost of Ownership: As discussed earlier, forgetting about insurance, maintenance, fuel, and registration costs can severely strain your budget, even if the monthly loan payment seems manageable.

- 4. Extending the Loan Term Too Much: While a longer term lowers monthly payments, it drastically increases the total interest paid and puts you at a higher risk of negative equity. Resist the urge to extend beyond what’s truly necessary.

- 5. Not Reading the Fine Print: Always review the entire loan agreement before signing. Understand all fees, prepayment penalties (if any), and the exact terms and conditions. Don’t rush this crucial step.

- 6. Impulse Buying: Emotional decisions often lead to financial mistakes. Take your time, do your research, and ensure the car and its associated loan truly fit your long-term financial plan.

Conclusion

Navigating a $46,000 car loan payment is a significant financial undertaking, but it doesn’t have to be a daunting one. By thoroughly understanding the core components – the loan amount, interest rate, loan term, and the power of a down payment – you gain control over your auto financing journey. Remember that your monthly payment is just one piece of the puzzle; the true cost of car ownership encompasses far more than just your loan installment.

Empower yourself by boosting your credit score, diligently saving for a down payment, and meticulously shopping around for the best lenders. Avoid common pitfalls like focusing solely on the monthly payment or neglecting the overall cost of ownership. With careful planning and informed decisions, your $46,000 car loan can be a manageable part of your budget, allowing you to enjoy your new vehicle without financial stress. Take charge of your auto financing, and drive away with confidence. To further enhance your financial literacy for car purchases, explore our guide on .