Decoding Your Car Loan: A Comprehensive Guide to Initials, Terms, and Crossword Clues

Decoding Your Car Loan: A Comprehensive Guide to Initials, Terms, and Crossword Clues Carloan.Guidemechanic.com

Have you ever found yourself staring at a crossword puzzle, a single clue holding you captive: "Car loan initials, perhaps?" Or maybe you’re simply preparing to finance a new vehicle and feel overwhelmed by the jargon. Whatever brings you here, you’ve landed in the right place. Understanding the various car loan initials crossword clues and the financial terms they represent is not just a brain exercise; it’s a crucial step towards making smart, informed decisions about one of life’s biggest purchases.

This isn’t just about solving a puzzle; it’s about empowering you. We’re going to dive deep into the world of car loan terminology, explaining the key acronyms and concepts that frequently appear in financing discussions – and yes, sometimes even in your favorite daily crossword. By the end of this article, you’ll not only be better equipped to fill in those tricky boxes but also to navigate the car buying process with confidence and clarity.

Decoding Your Car Loan: A Comprehensive Guide to Initials, Terms, and Crossword Clues

The Foundation: Why Car Loan Initials Matter Beyond the Crossword

Before we break down specific terms, let’s understand why these initials are so important. When you apply for an auto loan, you’re entering into a legally binding agreement. This agreement is filled with terms and conditions that directly impact how much you pay, for how long, and what happens if circumstances change. Ignoring these details can lead to unexpected costs, longer repayment periods, or even financial strain.

Based on my experience working with countless individuals navigating car financing, a lack of understanding is the biggest hurdle. Many people sign documents without fully grasping the implications of terms like APR or LTV. This article aims to demystify these concepts, turning what might seem like confusing financial shorthand into clear, actionable knowledge.

Pro tip from us: Always approach a car loan application with the mindset of a detective. Ask questions, understand every initial, and never sign anything you don’t fully comprehend. Your future financial well-being depends on it.

The Top Car Loan Initials That Every Borrower (and Crossword Enthusiast) Should Know

Let’s get into the nitty-gritty. These are the initials and acronyms you’ll encounter most frequently when dealing with car loans, and the ones most likely to appear as car loan initials crossword clues. We’ll explore each one in detail, explaining its significance and offering practical advice.

1. APR: Annual Percentage Rate

This is arguably the most critical initial you’ll encounter. APR stands for Annual Percentage Rate, and it represents the true cost of borrowing money over a year, expressed as a percentage. It includes not just the interest rate but also certain fees associated with the loan, giving you a more complete picture of what you’ll pay.

Understanding APR is vital because it allows you to compare different loan offers accurately. A lower interest rate might look appealing, but if another loan has a slightly higher interest rate but significantly lower fees, its overall APR might actually be better. Always focus on the APR when comparing loan options from different lenders. It’s the standard metric for comparison.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan, which is heavily influenced by the APR. A low monthly payment achieved by stretching out the loan term (e.g., 72 or 84 months) can result in paying significantly more in interest over the life of the loan, even with a seemingly good APR. This is a classic "car loan initials crossword" answer that signifies the cost of borrowing.

2. LTV: Loan-to-Value

LTV, or Loan-to-Value, is a ratio that lenders use to assess the risk of a loan. It compares the amount of money you want to borrow against the actual value of the car you intend to purchase. For instance, if a car is valued at $20,000 and you’re asking to borrow $18,000, your LTV would be 90% ($18,000 / $20,000).

Lenders typically prefer a lower LTV because it means you have more equity (or are putting more money down) in the vehicle from the start. A high LTV, especially over 100%, can occur if you roll negative equity from a trade-in into your new loan, or if you finance additional costs like extended warranties. A high LTV signals higher risk to the lender, which can result in a higher interest rate or even denial of the loan.

Based on my observations, many buyers overlook LTV, especially when trading in a car that’s worth less than what they owe on it. This "negative equity" can dramatically increase your LTV on the new vehicle, making it harder to get favorable terms. Aim for an LTV of 80% or less if possible, by making a substantial down payment.

3. DTI: Debt-to-Income Ratio

DTI, or Debt-to-Income ratio, is another critical metric lenders use to evaluate your ability to repay a loan. It’s calculated by dividing your total monthly debt payments (including the new car loan payment) by your gross monthly income. For example, if your total monthly debt payments (mortgage/rent, credit card minimums, student loans, and the proposed car payment) are $1,500 and your gross monthly income is $4,000, your DTI would be 37.5% ($1,500 / $4,000).

Lenders use DTI to determine if you have enough disposable income to comfortably make your car payments without overextending yourself. While specific thresholds vary, a DTI below 36% is generally considered good, indicating a healthy financial situation. A higher DTI might signal to lenders that you’re already stretched thin, potentially leading to a higher interest rate or a loan denial.

Pro tips from us: Before applying for a car loan, calculate your DTI. If it’s on the higher side, consider paying down other debts or increasing your income to improve your ratio. This shows lenders you’re a responsible borrower. This initial often comes up in crosswords as a "financial health metric."

4. MSRP: Manufacturer’s Suggested Retail Price

MSRP stands for Manufacturer’s Suggested Retail Price. This is the price the vehicle manufacturer recommends that dealerships sell the car for. It’s often referred to as the "sticker price" or "list price." While it’s a starting point, it’s important to remember that the MSRP is just a suggestion.

You should rarely pay the MSRP, especially for popular models where competition among dealerships is high. The actual transaction price can be lower, particularly if you’re a skilled negotiator or if the dealership is eager to move inventory. MSRP also typically doesn’t include destination charges, taxes, registration fees, or additional dealer add-ons, which can significantly inflate the final price.

Common mistakes to avoid are thinking the MSRP is non-negotiable. Always research the invoice price (what the dealer paid for the car) and average transaction prices in your area before stepping onto the lot. This knowledge gives you leverage during negotiations.

5. VIN: Vehicle Identification Number

While not directly related to the terms of your loan, the VIN, or Vehicle Identification Number, is absolutely crucial for any car purchase or loan. This unique 17-character alphanumeric code identifies a specific vehicle, much like a social security number identifies a person. You’ll find it on the dashboard (visible through the windshield) and on the driver’s side door jamb.

The VIN provides a wealth of information about the car, including its manufacturer, model, year, engine size, and where it was built. It’s essential for conducting vehicle history reports (like Carfax or AutoCheck), which can reveal accidents, flood damage, recall information, and previous ownership. For lenders, the VIN confirms the exact vehicle being financed.

Based on my experience, checking the VIN and running a history report is a non-negotiable step before buying any used car. It can save you from purchasing a vehicle with hidden problems that could lead to significant repair costs down the road. Always ensure the VIN on the car matches the VIN on all paperwork, including the loan agreement.

Expanding Your Financial Vocabulary: Other Key Car Loan Concepts

Beyond the core initials, several other terms and concepts are vital to understanding car loans. While they might not always appear as direct initials in a crossword, the initials of these concepts (e.g., DP for Down Payment) could certainly be a clue.

Down Payment (DP)

A down payment is the initial amount of money you pay upfront when purchasing a car, reducing the amount you need to borrow. This is a critical factor in your loan. A larger down payment directly translates to a lower loan amount, which means less interest paid over the life of the loan and lower monthly payments.

From a lender’s perspective, a substantial down payment reduces their risk. It shows you’re committed to the purchase and have a financial stake in the vehicle. This often results in more favorable loan terms, including a lower APR. Based on my observations, many financial experts recommend a down payment of at least 10-20% for new cars and 20% or more for used cars.

Common mistakes to avoid include stretching your budget too thin to afford a minimal down payment, or worse, skipping it altogether. While zero-down loans exist, they typically come with higher interest rates and put you in an "upside down" position (owing more than the car is worth) much faster.

Loan Term

The loan term refers to the length of time you have to repay the car loan, typically expressed in months (e.g., 36, 48, 60, 72, or 84 months). This choice significantly impacts your monthly payment and the total interest you’ll pay. A shorter loan term means higher monthly payments but less interest paid overall. Conversely, a longer loan term offers lower monthly payments but results in more interest paid over time.

While lower monthly payments from longer terms can be tempting, remember the trade-off. Over an 84-month loan, you’ll likely pay thousands more in interest compared to a 60-month loan for the same amount, even with a similar APR. You also risk the car depreciating faster than you pay off the loan, leaving you with negative equity.

Pro tips from us: Aim for the shortest loan term you can comfortably afford. This minimizes your interest costs and helps you build equity in the vehicle more quickly. Consider whether you plan to keep the car for the entire loan term, as longer terms increase the likelihood of unexpected repairs while still paying off the loan.

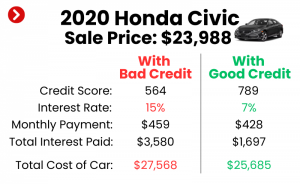

Credit Score (CS)

While "CS" isn’t an initial within the loan itself, your credit score is the single most influential factor in determining the car loan terms you’ll be offered. Lenders use your credit score to assess your creditworthiness and the likelihood that you’ll repay the loan. A higher credit score (typically 700+) indicates a lower risk borrower and qualifies you for the best interest rates.

A lower credit score, on the other hand, signals higher risk, leading to higher interest rates and potentially less favorable loan terms. Your credit score is a numerical representation derived from your credit history, including payment history, amounts owed, length of credit history, new credit, and credit mix.

Common mistakes to avoid are applying for a car loan without checking your credit score first. Knowing your score allows you to anticipate the rates you might qualify for and gives you time to address any errors on your credit report. for more detailed information on how to improve and maintain a healthy credit score.

Empowering Yourself: Why This Knowledge is Your Best Tool

Understanding these car loan initials crossword terms and concepts isn’t just an academic exercise; it’s your armor in the car buying battlefield. Dealerships and lenders often use these terms, assuming you understand them. When you do, you level the playing field.

Based on my experience, informed buyers tend to:

- Negotiate better prices: They know what they’re paying for and can challenge inflated figures.

- Secure better loan terms: They understand APR, LTV, and DTI, allowing them to compare offers effectively.

- Avoid common pitfalls: They recognize when a deal is too good to be true or when they’re being pushed into an unfavorable long-term loan.

- Reduce stress: Confidence in your understanding translates to a less stressful and more enjoyable car buying process.

This knowledge directly contributes to your financial health. By minimizing interest paid, securing favorable terms, and avoiding negative equity, you keep more money in your pocket and protect your assets.

Tackling the Crossword and Beyond: A Strategic Approach

So, how does all this help with your crossword puzzle? When you see a clue like "Car loan rate initials (3 letters)," your mind should immediately jump to APR. If it asks for "Vehicle ID letters," VIN should come to mind. By internalizing these key terms, you not only solve the puzzle but also reinforce valuable financial literacy.

For a deeper dive into general financial literacy and how it applies to major purchases, consider exploring resources from reputable organizations like the Consumer Financial Protection Bureau (CFPB). Their website offers invaluable guides on various financial topics, including auto loans: .

Remember, the goal is not just to get a car, but to get a smart car loan. This involves diligent research, understanding your personal financial situation, and knowing the language of financing. Don’t be afraid to ask questions, read every line of your contract, and walk away if a deal doesn’t feel right.

Conclusion: Drive Away with Confidence

From solving that tricky car loan initials crossword clue to signing on the dotted line for your new vehicle, understanding the language of auto financing is an indispensable skill. We’ve journeyed through the crucial acronyms like APR, LTV, DTI, MSRP, and VIN, along with other vital concepts such as down payments and loan terms. Each of these elements plays a significant role in the overall cost and manageability of your car loan.

By equipping yourself with this comprehensive knowledge, you transform from a passive borrower into an active, empowered consumer. You’re not just buying a car; you’re making a significant financial investment, and knowing the intricacies of your loan ensures that investment works for you, not against you. So, go forth, conquer those crosswords, and more importantly, secure the best possible car loan for your financial future. Drive safely, and drive smartly!