Decoding Your Car Loan Cost Per Month: A Comprehensive Guide to Smart Auto Financing

Decoding Your Car Loan Cost Per Month: A Comprehensive Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your very first vehicle or an upgrade to better suit your lifestyle. For most people, financing that purchase through a car loan is a necessity. However, understanding the car loan cost per month goes far beyond just knowing the number your lender quotes you. It’s about dissecting the various components that contribute to that figure, ensuring you make an informed decision that aligns with your financial well-being.

This comprehensive guide will demystify auto financing, helping you understand precisely what drives your monthly car payment. We’ll delve into the critical factors, explore hidden costs, and equip you with strategies to secure the best possible deal. Our ultimate goal is to empower you to navigate the world of car loans with confidence and clarity.

Decoding Your Car Loan Cost Per Month: A Comprehensive Guide to Smart Auto Financing

Understanding the Basics: What Drives Your Monthly Car Payment?

Your monthly car loan payment isn’t a random figure. It’s the result of a precise calculation involving several key variables. Grasping these fundamentals is the first step towards controlling your auto financing experience. Let’s break down the core components.

The Principal Amount: The Foundation of Your Loan

The principal amount is simply the total sum of money you borrow to purchase the car. This isn’t necessarily the sticker price of the vehicle. Instead, it’s the agreed-upon purchase price minus any down payment you make and any trade-in value from your old car. A lower principal means you’re borrowing less, which directly translates to lower monthly payments and less interest paid over the life of the loan.

Interest Rate: The Cost of Borrowing

The interest rate is arguably the most significant factor influencing your car loan cost per month. It represents the cost of borrowing money from a lender, expressed as a percentage of the principal. A higher interest rate means you’ll pay more for the privilege of borrowing, significantly increasing both your monthly payments and the total cost of the loan over time. Even a small difference in interest rates can save you hundreds, if not thousands, of dollars.

Loan Term: How Long You’ll Be Paying

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term will generally result in lower monthly payments because the principal is spread out over more installments. However, this convenience comes at a cost, as you’ll pay more in total interest over the extended period. Conversely, a shorter term means higher monthly payments but less total interest paid.

Down Payment: Your Upfront Investment

A down payment is the initial amount of cash you pay towards the purchase of the car, reducing the amount you need to borrow. This upfront investment plays a crucial role in lowering your monthly car payment. By reducing the principal, a substantial down payment can also help you secure a better interest rate, as lenders perceive less risk when you have more equity in the vehicle from the start.

Key Factors That Influence Your Interest Rate

While the principal, term, and down payment are crucial, the interest rate you qualify for has a monumental impact on your overall car loan cost per month. Several factors are at play here, and understanding them can help you optimize your borrowing power.

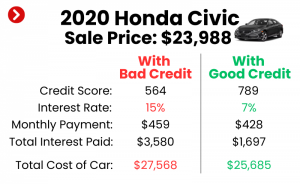

Your Credit Score: The Biggest Determinant

Your credit score is a numerical representation of your creditworthiness. Lenders use it to assess the risk of lending you money. A high credit score (generally 700+) indicates a responsible borrower and typically qualifies you for the lowest available interest rates. Conversely, a low credit score signals higher risk, leading to significantly higher interest rates.

Based on my experience, many first-time buyers underestimate the power of a good credit score. Taking steps to improve your credit before applying for a car loan can save you a fortune.

Loan Term: Shorter vs. Longer Terms

Believe it or not, the length of your loan can also influence the interest rate. Lenders often offer slightly lower interest rates for shorter loan terms. This is because there’s less risk of economic changes or your financial situation deteriorating over a shorter period. Longer terms, while offering lower monthly payments, may come with a slightly higher interest rate.

Vehicle Age and Type: New vs. Used

The type of car you’re financing can affect the interest rate. New cars often qualify for lower interest rates, sometimes even promotional rates from manufacturers. Used cars, particularly older models, generally carry higher interest rates due to their higher depreciation rate and perceived higher risk of mechanical issues. Luxury vehicles or those with high depreciation might also see slightly different rates.

Current Market Rates: Economic Factors

The broader economic environment also plays a role. When the Federal Reserve raises or lowers interest rates, it impacts the cost of borrowing across the board, including auto loans. These market fluctuations are beyond your control but are important to be aware of when you’re in the market for a car. Timing your purchase can sometimes yield better rates.

Lender Type: Banks, Credit Unions, Dealerships

Where you get your loan can make a difference. Traditional banks, credit unions, and online lenders all offer auto loans. Credit unions are often known for competitive rates, while dealerships might offer special manufacturer-backed financing. Shopping around among different lender types is crucial to finding the best deal.

The Role of Your Down Payment: More Than Just an Initial Outlay

While we touched on the down payment, its importance warrants a deeper dive. It’s not just a lump sum you hand over; it’s a strategic financial move that profoundly impacts your car loan cost per month and overall financial health.

Reducing the Principal

The most direct impact of a down payment is reducing the total amount of money you need to borrow. If a car costs $30,000 and you put down $5,000, you only need to finance $25,000. This smaller principal immediately translates into lower monthly payments.

Lowering Monthly Payments

With a reduced principal, each monthly installment will be smaller, making the car more affordable on a day-to-day basis. This can free up cash flow for other expenses or savings. For instance, a $25,000 loan over 60 months will have a significantly lower payment than a $30,000 loan over the same term.

Reducing Total Interest Paid

This is where a down payment truly shines. By borrowing less, you accrue less interest over the life of the loan. Even if the interest rate remains the same, a smaller principal means the interest is calculated on a lower base, leading to substantial savings. A substantial down payment is often your best friend in minimizing the total cost of your auto financing.

Building Equity Faster

A larger down payment means you start with more equity in your vehicle from day one. This is especially beneficial if the car depreciates quickly. It helps prevent you from being "upside down" on your loan, which means owing more than the car is worth. This equity also provides a buffer if you need to sell the car before the loan is paid off.

Choosing the Right Loan Term: Balancing Monthly Payments and Total Cost

The loan term is a critical decision point that requires careful consideration. It’s a balancing act between making your car loan cost per month affordable now and minimizing the total amount you pay in the long run.

Shorter Terms (e.g., 36-48 months): Higher Monthly, Less Total Interest

Opting for a shorter loan term means you’ll have higher monthly payments. However, the significant advantage is paying much less in total interest over the life of the loan. You’ll also own your car outright sooner, freeing up that monthly payment for other financial goals. This option is ideal if your budget can comfortably accommodate the higher installments.

Longer Terms (e.g., 60-84 months): Lower Monthly, More Total Interest

Longer loan terms spread the cost over more months, resulting in lower and seemingly more manageable monthly payments. This can make more expensive cars appear affordable. However, the downside is paying significantly more in total interest because the lender earns interest for a longer period.

A common mistake to avoid is solely focusing on the lowest monthly payment without considering the total cost. While a lower payment might seem appealing, it could mean you’re paying thousands more over the life of the loan. Always calculate the total cost for different terms.

Beyond the Sticker Price: Hidden Costs to Consider

Your car loan cost per month is just one piece of the financial puzzle when buying a car. There are several other "hidden" or often overlooked expenses that contribute to the true cost of vehicle ownership. Ignoring these can quickly derail your budget.

Sales Tax: A State-Specific Cost

Almost every state charges sales tax on vehicle purchases. This can be a substantial amount, often calculated on the purchase price of the car before your down payment. Some states even tax the full value before any trade-in. Always factor this into your initial budget.

Registration and Licensing Fees: Annual Necessities

These are the fees you pay to your state’s Department of Motor Vehicles (DMV) to legally operate your vehicle. They cover license plates, title registration, and sometimes annual renewal fees. These are ongoing costs that you’ll incur every year.

Dealer Fees: The Fine Print

Dealerships often include various fees, such as documentation fees, preparation fees, or advertising fees. While some are legitimate, others can be negotiable or even questionable. Always ask for a detailed breakdown of all fees and question anything that seems unclear or excessive. Pro tips from us: Many of these are negotiable, so don’t be afraid to push back.

Insurance Costs: A Major Variable

Car insurance is a non-negotiable expense. Your premium will vary significantly based on the car’s make and model, your driving record, age, location, and the type of coverage you choose. Before finalizing a car purchase, get insurance quotes for specific vehicles to avoid a shocking monthly bill. This can sometimes make a seemingly affordable car prohibitively expensive to insure.

Maintenance & Repairs: Especially for Used Cars

Every car requires regular maintenance, from oil changes to tire rotations. For used cars, the potential for unexpected repairs increases. Factor in a budget for these expenses. A thorough pre-purchase inspection can help mitigate some risks with used vehicles, but an emergency fund for repairs is always a wise idea.

Gap Insurance: When It’s Necessary

Gap insurance covers the "gap" between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. Cars depreciate quickly, and it’s common to owe more than the car is worth, especially in the early years of a loan. If you make a small down payment or have a long loan term, gap insurance can protect you from a significant financial loss.

Calculating Your Car Loan Cost Per Month: Tools and Techniques

Estimating your car loan cost per month is a crucial step in budgeting and decision-making. Fortunately, you don’t need to be a math wizard to get an accurate figure.

Online Loan Calculators: Your Best Friend

The easiest and most common way to calculate your monthly payment is using an online car loan calculator. These tools are widely available on bank websites, financial aggregators, and even dealership sites. You simply input the principal amount, interest rate, and loan term, and the calculator instantly provides your estimated monthly payment.

From my perspective as someone who’s guided countless individuals through this process, these calculators are invaluable. They allow you to quickly compare different scenarios – what if you put down more, or choose a shorter term, or get a lower interest rate? Experiment with various inputs to see how each factor impacts your monthly payment.

Manual Calculation (Amortization): Understanding the Process

While online calculators do the heavy lifting, understanding the basic concept of amortization can be empowering. Car loans are typically "simple interest" loans, meaning interest is calculated on the remaining principal balance. Each monthly payment consists of both principal and interest. In the early stages of the loan, a larger portion of your payment goes towards interest. As the principal decreases, more of your payment goes towards reducing the principal. This systematic repayment schedule is called amortization.

Strategies to Lower Your Monthly Car Payment

If your initial estimated car loan cost per month is higher than your budget allows, don’t despair. There are several effective strategies you can employ to bring that figure down.

Increase Your Down Payment

As discussed, a larger down payment directly reduces the principal amount you borrow. This is one of the most effective ways to lower your monthly payments and save on total interest. Even an extra few hundred dollars upfront can make a noticeable difference.

Improve Your Credit Score

A higher credit score unlocks lower interest rates. Before applying for a loan, take steps to improve your credit: pay bills on time, reduce existing debt, and check for errors on your credit report. This preparation can lead to significant long-term savings.

Shop Around for the Best Interest Rate

Don’t settle for the first offer you receive. Get pre-approved by several lenders – banks, credit unions, and online lenders. Compare their interest rates and terms. This competition can often lead to a better deal than simply taking the dealer’s financing.

Negotiate the Car Price

The lower the purchase price of the car, the less you need to finance. Be prepared to negotiate with the dealership on the vehicle’s price. This can directly reduce your principal and, consequently, your monthly payment. Pro tips from us: Negotiation is key, so research market values beforehand.

Choose a More Affordable Vehicle

It sounds obvious, but sometimes the best strategy is to simply choose a car that costs less. Re-evaluate your needs versus wants. A slightly less expensive model or trim level can significantly reduce your monthly commitment.

Consider Refinancing (Later in the Loan)

If interest rates drop, your credit score improves, or your financial situation changes after you’ve already secured a loan, refinancing might be an option. Refinancing allows you to replace your existing loan with a new one, potentially with a lower interest rate or a different term, thereby reducing your monthly payment.

The Pre-Approval Advantage: Why It Matters

Getting pre-approved for a car loan is one of the most powerful steps you can take before stepping foot in a dealership. It’s not just a formality; it’s a strategic move that puts you in control.

Knowing Your Budget Upfront

Pre-approval tells you exactly how much you can borrow and at what interest rate. This clarity allows you to shop for cars with a firm budget in mind, preventing you from falling in love with a vehicle you can’t truly afford. It helps you understand your potential car loan cost per month before any commitment.

Empowering Negotiation

Walking into a dealership with a pre-approval letter is like having a secret weapon. It shows the dealer you’re a serious buyer with financing already secured. This takes the focus off the monthly payment and allows you to negotiate more effectively on the actual price of the car. You’re no longer just a "payment buyer."

Comparing Offers Effectively

With a pre-approved offer in hand, you have a benchmark. You can then ask the dealership if they can beat or match your pre-approved rate. This fosters competition and often results in a better deal, either through a lower interest rate or a more favorable overall package. Based on my experience, getting pre-approved is one of the most powerful steps to ensuring you don’t overpay for your auto financing.

Common Mistakes to Avoid When Financing a Car

Even with all the information, it’s easy to fall into common traps when financing a vehicle. Being aware of these pitfalls can save you from costly errors.

Not Checking Your Credit Score

Many people go into car shopping without knowing their credit score. This leaves them vulnerable to whatever rate the dealer offers. Always check your credit score and report beforehand to understand your standing.

Focusing Only on Monthly Payment

As discussed, fixating solely on the lowest car loan cost per month can lead to longer loan terms and significantly higher total interest paid. Always consider the total cost of the loan, not just the monthly installment.

Skipping the Down Payment

While a zero-down loan might seem attractive, it means you’re financing the entire cost of the car, leading to higher monthly payments and more interest. It also puts you at risk of being upside down on your loan immediately.

Ignoring Total Cost of Ownership

Beyond the loan, remember all those hidden costs like insurance, maintenance, and registration. Failing to factor these into your overall budget can lead to financial strain.

Not Shopping Around for Loans

Accepting the first loan offer, especially from the dealership, can be a costly mistake. Always compare offers from multiple lenders to ensure you’re getting the most competitive interest rate and terms. For more details on avoiding these pitfalls, check out our guide on .

Impulse Buying

Rushing into a purchase without proper research, budgeting, and pre-approval often leads to buyer’s remorse and a less-than-ideal loan situation. Take your time, do your homework, and make an informed decision.

Refinancing Your Car Loan: When and Why?

Even after you’ve secured a loan, your financial journey with your car doesn’t necessarily end. Refinancing your car loan can be a smart move in certain situations, potentially lowering your car loan cost per month or changing your loan terms.

Getting a Lower Interest Rate

If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a lower interest rate. Refinancing at a lower rate can reduce your monthly payment and the total interest you pay over the life of the loan.

Changing Loan Terms

Perhaps you initially opted for a long loan term to keep payments low, but now your financial situation has improved, and you want to pay off the car faster. Refinancing to a shorter term can achieve this, reducing total interest. Conversely, if you’re facing financial hardship, refinancing to a longer term might lower your monthly payment, providing some breathing room (though you’ll pay more in total interest).

Improving Your Financial Situation

Life happens, and sometimes your credit score improves dramatically after you’ve financed a car. This improved creditworthiness can open doors to better loan terms that weren’t available to you initially. Refinancing can allow you to take advantage of your stronger financial standing.

Before you refinance, make sure to calculate the total savings and consider any fees associated with the new loan. It’s important to ensure the benefits outweigh the costs. For a deeper dive into whether refinancing is right for you, consider resources like Investopedia’s guide on auto loan refinancing.

Conclusion: Mastering Your Car Loan Cost Per Month

Understanding your car loan cost per month is about more than just looking at a number. It’s about understanding the intricate dance between the principal, interest rate, loan term, and down payment. By grasping these elements, you gain the power to make informed decisions that protect your finances.

We’ve covered the factors influencing interest rates, the strategic importance of a down payment, and the delicate balance required when choosing a loan term. We’ve also illuminated the often-overlooked costs and provided you with actionable strategies to lower your payments and avoid common mistakes.

Armed with this comprehensive knowledge, you are now better equipped to navigate the auto financing landscape. Remember to shop around, understand all the costs, and always prioritize your long-term financial health over short-term convenience. Go forth and plan your next car purchase wisely – your wallet will thank you!