Decoding Your Credit Score: The Ultimate Guide to Securing a $50,000 Car Loan

Decoding Your Credit Score: The Ultimate Guide to Securing a $50,000 Car Loan Carloan.Guidemechanic.com

Buying a car is often one of the biggest financial decisions we make, and for many, a $50,000 vehicle represents a significant investment in quality, performance, or luxury. Whether you’re eyeing a robust SUV, a sleek electric vehicle, or a high-performance sedan, the path to ownership almost invariably involves a car loan. And when you’re talking about a substantial sum like $50,000, your credit score isn’t just a number – it’s your financial resume, dictating everything from your approval chances to the interest rate you’ll pay.

This comprehensive guide is designed to empower you with the knowledge needed to confidently navigate the world of car loans, specifically focusing on what it takes to secure that $50,000 dream car. We’ll dive deep into credit scores, lender expectations, and the strategies you can employ to put yourself in the strongest possible position. Prepare to transform from an aspiring car owner into an informed, savvy borrower.

Decoding Your Credit Score: The Ultimate Guide to Securing a $50,000 Car Loan

The Significance of a $50,000 Car Loan

A $50,000 car loan isn’t a small commitment; it places you squarely in the market for premium new vehicles or high-end used models. This amount signals to lenders that you’re seeking a substantial line of credit, which naturally comes with higher scrutiny. Lenders view larger loans as carrying greater risk, making your financial stability and history – primarily reflected in your credit score – incredibly important.

The type of car you’re looking at within this price range often influences lender perception as well. A brand-new luxury vehicle might be seen differently than a high-mileage vintage car, even if both cost $50,000. Lenders will assess the collateral, your ability to repay, and the overall risk profile associated with such a significant sum. Understanding this perspective is your first step towards successful loan approval.

Unpacking Your Credit Score: The Key to the Auto Loan Kingdom

Your credit score is a three-digit number that summarizes your creditworthiness based on your financial history. It’s generated by complex algorithms, primarily FICO and VantageScore models, which analyze data from your credit reports. These scores tell potential lenders how likely you are to repay borrowed money on time.

For a significant loan like $50,000, your credit score becomes the single most influential factor. Lenders use it to quickly assess your risk level. A higher score signals lower risk, potentially unlocking lower interest rates and more favorable loan terms. Conversely, a lower score can lead to higher rates, stricter terms, or even outright denial for such a large loan.

What Constitutes a "Good" Credit Score for a $50,000 Car Loan?

While there’s no single magic number, lenders generally categorize credit scores into ranges, each with different implications for a $50,000 car loan. It’s crucial to understand these tiers to set realistic expectations and strategize your approach.

Excellent Credit (780-850)

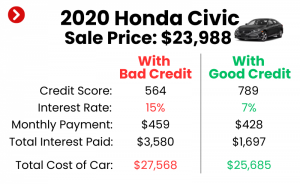

With an excellent credit score, you are a lender’s ideal customer. You represent minimal risk, demonstrating a consistent history of responsible borrowing and repayment. For a $50,000 car loan, this score range virtually guarantees approval at the most competitive interest rates available. You’ll have significant negotiating power and access to the best terms.

Based on my experience, individuals in this category often qualify for rates below 3-4% APR, which can save thousands of dollars over the life of a $50,000 loan. Lenders will actively compete for your business.

Very Good Credit (740-779)

A very good credit score also places you in an excellent position. You’re still considered a low-risk borrower and will likely qualify for highly favorable interest rates. While perhaps not the absolute lowest rates reserved for the "excellent" tier, you’ll still secure highly competitive terms for your $50,000 loan.

Lenders will be confident in your ability to repay. You should still shop around, as even a slight difference in APR can impact your monthly payments significantly on a loan of this size.

Good Credit (670-739)

This is where the majority of consumers fall, and it’s generally considered a solid credit score. For a $50,000 car loan, a good credit score means you’re likely to be approved, but the interest rates might be slightly higher than those with excellent or very good credit. You’ll still receive reasonable terms, but you might not get the absolute best offers.

It’s particularly important for those in this range to focus on a strong down payment and a stable income to strengthen their application. Your good credit shows a responsible history, but lenders might seek additional assurances for a $50,000 sum.

Fair Credit (580-669)

If your credit score falls into the fair range, securing a $50,000 car loan becomes more challenging. Approval is still possible, but you should expect higher interest rates and potentially less flexible loan terms. Lenders perceive a higher risk with fair credit, so they compensate by charging more for the loan.

Pro tips from us: If your score is in this range, consider making a larger down payment. This reduces the loan amount and signals to the lender that you’re committed, potentially improving your chances and lowering your rate. You might also explore lenders specializing in less-than-perfect credit.

Poor Credit (Under 580)

With a poor credit score, obtaining a $50,000 car loan from traditional lenders will be very difficult, if not impossible. The risk is considered too high for such a large amount, and if approved, the interest rates would be exorbitant, making the loan extremely expensive.

In this scenario, it’s generally advisable to focus on credit improvement before applying for such a large loan. Alternatively, you might need to consider a significantly less expensive vehicle, a substantial down payment, or exploring options like a co-signer.

Beyond the Score: Other Critical Factors Lenders Evaluate

While your credit score is paramount, it’s not the only piece of the puzzle. Lenders consider a holistic view of your financial situation, especially for a $50,000 car loan. Overlooking these factors can derail even an application with a decent credit score.

1. Debt-to-Income Ratio (DTI)

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, typically below 36%, though some auto lenders may accept slightly higher. A high DTI indicates that a significant portion of your income is already committed to other debts, making you a higher risk for taking on an additional $50,000 loan.

They want to see that you have enough disposable income to comfortably afford the new car payment without financial strain. Even with excellent credit, an excessively high DTI can be a red flag.

2. Income Stability and Employment History

Lenders want assurance that you have a consistent and reliable source of income to make your monthly payments. A steady employment history, ideally with the same employer for several years, speaks volumes about your financial stability. Recent job changes or gaps in employment might raise questions.

Self-employed individuals or those with commission-based income might need to provide more extensive documentation, such as tax returns for the past two years, to prove income consistency.

3. Down Payment Amount

A substantial down payment significantly strengthens your application for a $50,000 car loan. It reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment and ability to save.

Common mistakes to avoid are underestimating the power of a down payment. Even an extra few thousand dollars can move you into a better interest rate tier, saving you far more in the long run. Aim for at least 10-20% of the vehicle’s price, or more if your credit is not stellar.

4. Loan Term

The loan term refers to the length of time you have to repay the loan. While longer terms (e.g., 72 or 84 months) offer lower monthly payments, they often come with higher interest rates and mean you’ll pay more interest over the life of the loan. Lenders also perceive longer terms as slightly riskier due to the extended period of potential default.

For a $50,000 loan, try to keep the term as short as you can comfortably afford to minimize interest costs and accelerate equity buildup.

5. Vehicle Age and Type

The car itself acts as collateral for the loan. Lenders assess its value, age, and type. New cars generally secure better rates because they hold their value better initially and are less prone to immediate mechanical issues. Older or very high-mileage vehicles might be harder to finance for a $50,000 loan, or come with higher rates, as their depreciated value makes them riskier collateral.

Luxury or specialty vehicles might also be subject to different lending criteria due to their specific market and depreciation patterns.

6. Co-Signer

If your credit score is fair or poor, or if your DTI is a concern, a co-signer with excellent credit can significantly improve your chances of approval for a $50,000 car loan. A co-signer essentially guarantees the loan, promising to make payments if you default.

However, a co-signer takes on equal responsibility, so this decision should be made with extreme care and clear understanding between both parties.

Strategies to Boost Your Credit Score for a $50,000 Car Loan

If your credit score isn’t quite where you want it to be, don’t despair. There are actionable steps you can take to improve it, sometimes quicker than you might think. Building good credit is a marathon, not a sprint, but consistent effort pays off.

1. Pay Your Bills On Time, Every Time

Payment history is the single most important factor in your credit score, accounting for about 35% of your FICO score. Late payments can severely damage your score. Set up automatic payments or reminders to ensure you never miss a due date on credit cards, existing loans, or utility bills.

Even a single 30-day late payment can drop your score by dozens of points, making a $50,000 loan much harder to secure. Consistency is key.

2. Reduce Your Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’re using compared to your total available credit. For example, if you have a $10,000 credit limit and a $3,000 balance, your utilization is 30%. Experts recommend keeping this ratio below 30%, with lower being better (ideally under 10%).

Paying down credit card balances can rapidly improve this ratio, which accounts for about 30% of your FICO score. This shows lenders you’re not over-reliant on credit.

3. Address Negative Items on Your Credit Report

Regularly check your credit reports from all three major bureaus (Experian, Equifax, TransUnion) for errors. You can get a free report annually from AnnualCreditReport.com. If you find inaccuracies, dispute them immediately. Removing erroneous negative marks can boost your score.

For legitimate negative items like collections or charge-offs, consider negotiating a "pay-for-delete" if possible, or at least settling the debt to show good faith.

4. Avoid New Credit Inquiries

Each time you apply for new credit (like another credit card or loan), a hard inquiry appears on your credit report, which can slightly lower your score for a short period. Before applying for a $50,000 car loan, avoid opening any new credit accounts for at least 6-12 months.

Multiple hard inquiries in a short period signal to lenders that you might be desperate for credit, which is a risk factor.

5. Diversify Your Credit Mix (Responsibly)

Having a mix of credit types (e.g., credit cards, installment loans like student loans or mortgages) can positively impact your score, showing you can manage different forms of credit. However, only take on new credit if you genuinely need it and can afford it.

Opening new accounts solely for credit mix purposes can backfire if you can’t manage the payments.

6. Consider a Secured Credit Card or Credit-Builder Loan

If your credit history is thin or severely damaged, a secured credit card or a credit-builder loan can be excellent tools. A secured card requires a cash deposit as collateral, while a credit-builder loan essentially involves you making payments to yourself into a savings account, which is then released to you.

Both options allow you to demonstrate responsible payment behavior, which is reported to credit bureaus and helps build your score over time.

Navigating the Application Process for a $50,000 Car Loan

Once you’ve optimized your credit and financial profile, it’s time to approach the application process strategically.

1. Get Pre-Approved

This is a crucial step. Pre-approval involves applying for a loan before you even step foot in a dealership. It gives you a firm offer for a loan amount and interest rate, providing significant leverage. With pre-approval, you know exactly what you can afford and can focus on negotiating the car’s price, not the financing.

Many banks, credit unions, and online lenders offer pre-approval with only a soft credit inquiry, which doesn’t harm your score.

2. Shop Around for Rates

Don’t settle for the first offer you receive. Apply to several different lenders – banks, credit unions, and online auto loan providers. Each lender has different criteria and risk assessment models, so rates can vary significantly.

Based on my experience, taking the time to compare multiple offers, even for just a few days, can lead to substantial savings on a $50,000 loan. All hard inquiries for auto loans within a 14-45 day window (depending on the scoring model) are typically treated as a single inquiry, so rate shopping won’t unduly harm your score.

3. Gather All Necessary Documentation

Be prepared. Lenders will typically ask for proof of income (pay stubs, tax returns), proof of residence (utility bills, lease agreement), identification (driver’s license), and potentially bank statements. Having these documents ready will streamline the application process.

For a $50,000 loan, expect thorough verification of your financial claims.

4. Negotiate the Best Deal

With your pre-approval in hand, you’re a cash buyer to the dealership. This gives you power. Negotiate the car price separately from the financing. If the dealer offers a lower rate than your pre-approval, great! But always have your external offer as a fallback.

Remember that dealerships often make money on financing, so they might try to steer you towards their in-house options.

5. Understand the Fine Print

Before signing anything, meticulously read the entire loan agreement. Understand the interest rate (APR), the total loan amount, the monthly payment, any fees, and the repayment schedule. Ask questions if anything is unclear.

Pro tips from us: Pay close attention to any add-ons or extended warranties that might be rolled into the loan, as they can significantly increase your total cost.

What If Your Credit Score Isn’t Perfect? Alternative Avenues

Even if your credit score isn’t in the excellent range, securing a $50,000 car loan isn’t necessarily out of reach. You might just need to adjust your strategy or explore different options.

1. Make a Larger Down Payment

As mentioned, a substantial down payment mitigates lender risk. If you can put down 25-30% or more, it significantly reduces the amount you need to finance and can open doors to better rates even with a fair credit score. This is one of the most effective ways to compensate for a less-than-ideal credit profile.

2. Consider a Co-Signer

A co-signer with excellent credit can be your ticket to approval and better rates. Their creditworthiness effectively backs your loan, providing the lender with the security they need. Ensure both you and your co-signer fully understand the responsibilities involved.

This is a serious commitment for the co-signer, as their credit will also be impacted by your payment history.

3. Explore Credit Unions

Credit unions are non-profit organizations that often have more flexible lending criteria and competitive rates compared to large commercial banks, especially for members. If you qualify for membership (often based on location, employer, or association), it’s definitely worth checking their auto loan offerings.

Their member-focused approach can be beneficial for those with good to fair credit seeking a $50,000 loan.

4. Work with Online Lenders Specializing in Various Credit Tiers

Several online lenders specialize in different credit profiles, some even catering to those with fair or challenged credit. Companies like Capital One Auto Finance, LightStream, or PenFed Credit Union (which also operates like a credit union but has broad membership criteria) are good places to start your research.

They often have streamlined application processes and can provide quick pre-approvals.

5. Opt for a Less Expensive Vehicle (Initially)

If a $50,000 car loan proves too challenging with your current credit, consider buying a more affordable vehicle, diligently making payments to build your credit, and then upgrading in a few years. This is a pragmatic approach to achieving your long-term car ownership goals while strengthening your financial foundation.

Maintaining Your Credit After the Loan

Securing your $50,000 car loan is a significant achievement, but the journey doesn’t end there. How you manage this loan will have a lasting impact on your credit score and future financial opportunities.

1. Timely Payments are Paramount

Continue the habit of making all your payments on time, every single month. Your auto loan payments will be reported to the credit bureaus, and a perfect payment history for such a large loan will significantly boost your credit score over time.

Conversely, late payments will severely damage the very score you worked so hard to improve.

2. Don’t Let Other Credit Suffer

While focusing on your car loan, don’t neglect your other financial obligations. Keep paying credit card bills, student loans, and other debts on time. Your entire credit profile contributes to your score.

A strong overall credit history is essential for maintaining a high score.

3. Avoid Taking on Excessive New Debt

While you’re repaying your $50,000 car loan, be mindful of taking on too much additional debt. A high debt-to-income ratio, even with timely payments, can still be a concern for future lenders. Prioritize paying down existing debts.

This demonstrates financial prudence and responsibility.

Conclusion: Drive Towards Your Dream Car with Confidence

Securing a $50,000 car loan is a significant financial undertaking, and your credit score is undeniably the most powerful tool in your arsenal. From understanding the nuances of different credit score ranges to strategically improving your financial profile, this guide has provided you with a comprehensive roadmap.

Remember, preparation is key. By knowing what lenders look for, actively working to improve your credit, and diligently comparing offers, you can position yourself for the best possible interest rates and terms. Don’t let the idea of a large loan intimidate you. With the right knowledge and a proactive approach, your dream car, financed on favorable terms, is well within reach. Drive smart, drive informed, and enjoy the journey!