Decoding Your Drive: How Long Can You Get A Car Loan For? Your Ultimate Guide to Smart Auto Financing

Decoding Your Drive: How Long Can You Get A Car Loan For? Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, beneath the gleam of fresh paint and the allure of advanced features lies a critical financial decision: How long can you get a car loan for? This seemingly simple question opens up a world of complex variables that directly impact your monthly budget, the total cost of your car, and your overall financial well-being.

As an expert blogger and professional SEO content writer, I’ve seen firsthand how understanding car loan terms can make or break a buyer’s experience. Many people focus solely on the monthly payment, overlooking the profound implications of the loan duration. This comprehensive guide is designed to be your definitive resource, helping you navigate the intricacies of auto financing with confidence and clarity. We’ll dive deep into every aspect, ensuring you make an informed decision that perfectly aligns with your financial goals.

Decoding Your Drive: How Long Can You Get A Car Loan For? Your Ultimate Guide to Smart Auto Financing

Understanding the Fundamentals: What is a Car Loan Term?

Before we delve into the "how long," let’s establish a clear understanding of what a "car loan term" actually means. Simply put, the loan term refers to the duration over which you agree to repay the borrowed amount for your vehicle, typically expressed in months. Common car loan lengths range from 36 months (3 years) to 84 months (7 years), with some lenders even offering extended terms up to 96 months (8 years) or, in rare cases, even longer.

This duration is not just a number; it’s a pivotal factor that dictates the size of your monthly payments and the total amount of interest you’ll pay over the life of the loan. A shorter term generally means higher monthly payments but less total interest, while a longer term offers lower monthly payments but accrues more interest over time. Making the right choice here is fundamental to responsible auto financing.

The Interplay: Loan Term, Monthly Payments, and Total Interest

The relationship between your car loan term, your monthly payment, and the total interest you pay is a delicate balance. Understanding this dynamic is crucial for making a financially sound decision. Let’s break down the advantages and disadvantages of different loan durations.

The Appeal of Shorter Car Loan Terms (e.g., 36-60 months)

Opting for a shorter car loan term, typically between 3 to 5 years, comes with several compelling benefits, particularly for those who prioritize debt freedom and minimizing costs. While the monthly payments will be higher, the long-term financial advantages are often significant.

Pros of Shorter Loan Terms:

- Lower Total Interest Paid: This is arguably the biggest advantage. Because you’re paying off the principal amount faster, the lender has less time to charge you interest. Over the life of the loan, this can translate into substantial savings, leaving more money in your pocket.

- Faster Debt Freedom: Imagine the relief of knowing your car is paid off in just a few years. Shorter terms mean you’ll be debt-free sooner, freeing up a significant portion of your monthly budget for other financial goals, such as saving for a home, investing, or simply enjoying more disposable income.

- Build Equity Quicker: Your car begins to depreciate the moment you drive it off the lot. With a shorter loan term, you’re paying down the principal faster than the car depreciates, allowing you to build equity more quickly. This reduces the risk of being "upside down" on your loan, where you owe more than the car is worth.

- Less Risk of Negative Equity: Building on the previous point, rapid equity accumulation significantly lowers your exposure to negative equity, especially in the event of an accident or if you decide to trade in your vehicle earlier than planned. This financial safety net is invaluable.

- Motivates Financial Discipline: Based on my experience, committing to a shorter term often encourages better financial discipline. Knowing you have a higher monthly payment can motivate you to stick to your budget and avoid unnecessary spending, fostering healthier financial habits in the long run.

Cons of Shorter Loan Terms:

- Higher Monthly Payments: The most obvious drawback is the larger chunk of your income that will go towards your car payment each month. This can strain tighter budgets and leave less room for other expenses or savings.

- Potentially Harder to Qualify: Lenders assess your ability to comfortably afford the monthly payments. If the higher payment of a short-term loan pushes your debt-to-income ratio too high, you might find it more challenging to get approved, especially if your credit score isn’t stellar.

Exploring Longer Car Loan Terms (e.g., 72-84+ months)

In recent years, longer car loan terms, stretching to 6 or 7 years, have become increasingly common, primarily due to the rising costs of vehicles. These extended durations offer a different set of financial trade-offs.

Pros of Longer Loan Terms:

- Lower Monthly Payments: This is the primary driver for many consumers choosing longer terms. Spreading the cost over more months significantly reduces the amount you pay each month, making higher-priced vehicles more "affordable" on a day-to-day basis.

- Easier Budget Management: For individuals with tight budgets or those who want more flexibility with their monthly cash flow, lower payments can be a huge relief. It leaves more money available for other necessities, emergencies, or discretionary spending.

- Potentially Easier to Qualify (for the monthly payment): While the total loan amount remains the same, the lower monthly payment can make it easier to meet a lender’s debt-to-income ratio requirements, potentially broadening your approval chances for a desired vehicle.

Cons of Longer Loan Terms:

- Significantly Higher Total Interest Paid: This is the critical trade-off. Over a longer period, even a slightly lower interest rate can accumulate into thousands of dollars more in total interest compared to a shorter term. You’re paying for the convenience of lower monthly payments.

- Slower Equity Build-Up (Increased Negative Equity Risk): With a longer term, your principal balance decreases at a slower rate. Given that cars depreciate rapidly, you’re at a much higher risk of owing more than your car is worth for a significant portion of the loan. Pro tips from us: Always be aware of your car’s market value versus your outstanding loan balance, especially if you’re considering a trade-in or if your car is totaled in an accident.

- Longer Period of Debt: Committing to a car loan for 6, 7, or even 8 years means a substantial portion of your financial life is tied to this debt. This can limit your flexibility for other major financial decisions, such as buying a home, starting a business, or saving for retirement.

- Vehicle Reliability Concerns: As your loan stretches longer, your vehicle ages. There’s a higher chance that your car will start requiring significant maintenance or repairs while you’re still making payments. This can lead to the frustrating situation of paying for a car that’s becoming unreliable.

- Warranty Expiration: Most manufacturer warranties expire after 3-5 years. If your loan term extends beyond this, you’ll be solely responsible for all repair costs while still paying off the original purchase.

Factors Influencing Your Car Loan Term Eligibility

Lenders don’t just hand out money; they assess risk. Several key factors determine not only if you’ll be approved for a car loan but also the specific terms, including the length, that will be offered to you. Understanding these elements can help you prepare and secure the best possible deal.

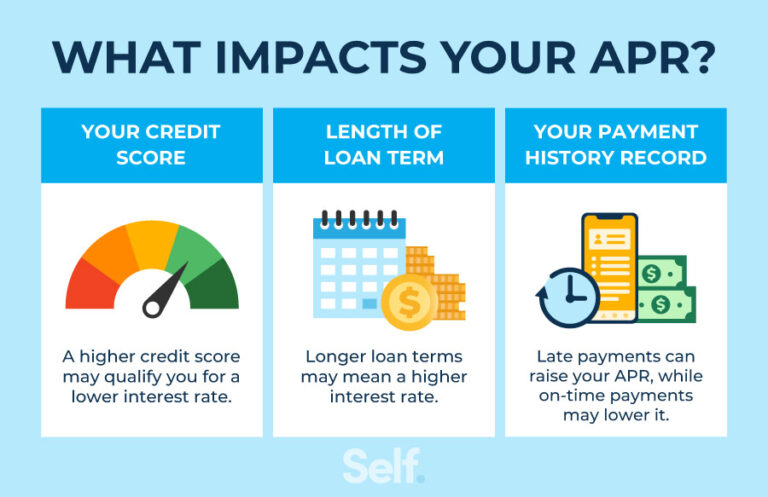

1. Your Credit Score

Your credit score is perhaps the single most influential factor in securing favorable car loan terms. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt.

- High Credit Score (700+): With excellent credit, you’re considered a low-risk borrower. Lenders will be more eager to offer you the lowest interest rates and the widest range of loan terms, including the flexibility to choose shorter durations with attractive rates.

- Fair Credit Score (600-699): If your credit falls into this range, you’ll likely still qualify for a loan, but the interest rates will be higher, and the available loan terms might be slightly more restrictive. Lenders may prefer to offer longer terms to make the monthly payments more manageable, albeit at a higher overall cost.

- Poor Credit Score (Below 600): Securing a car loan with bad credit is challenging. If approved, you’ll face significantly higher interest rates and potentially limited term options. Lenders might gravitate towards shorter terms to reduce their risk or require a larger down payment. Common mistakes to avoid are applying to too many lenders at once if you have a low score, as this can further damage your credit. Focus on improving your score before applying, if possible.

2. Debt-to-Income (DTI) Ratio

Your DTI ratio is a crucial metric lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments (including the proposed car payment) by your gross monthly income.

- Lenders prefer a low DTI, typically below 40%, indicating you have sufficient income to cover your debts. A high DTI suggests you’re already stretched thin, making a lender hesitant to offer a large loan or a term that results in a high monthly payment. A lower DTI can open doors to more flexible terms.

3. Down Payment Amount

A down payment is the initial amount of money you pay upfront for the car, reducing the amount you need to borrow. This has a direct impact on your loan terms.

- Larger Down Payment: A substantial down payment reduces the loan-to-value (LTV) ratio, which is the amount financed relative to the car’s value. A lower LTV signals less risk to the lender, often resulting in better interest rates and more flexible term options. It also helps you build equity faster and reduces your monthly payments.

- No Down Payment: While zero-down loans are appealing, they mean you’re financing the entire cost of the car. This increases your monthly payment, the total interest paid, and puts you at a higher risk of negative equity from day one. Lenders might offer fewer term choices or higher rates for these loans.

4. Age and Type of Vehicle

The car itself plays a role in determining eligible loan terms.

- New Cars: Lenders are often more willing to offer longer terms (up to 72 or 84 months) for new vehicles due to their predictable value, longer lifespan, and higher resale value compared to used cars.

- Used Cars: For used vehicles, particularly older models, lenders typically impose shorter term limits. This is because older cars have higher depreciation rates and a greater likelihood of mechanical issues, which increases the lender’s risk. You might find it hard to get an 84-month loan on a 7-year-old car.

- Luxury vs. Economy: High-end luxury vehicles might also be subject to different terms, sometimes shorter, due to their rapid depreciation and the specialized market for their resale.

5. Lender Policies and Promotions

Every financial institution has its own set of lending criteria, risk tolerance, and promotional offers.

- Banks, Credit Unions, Dealerships, Online Lenders: Each type of lender has varying strengths. Credit unions often offer competitive rates and more flexible terms to their members. Dealerships might have special financing offers from manufacturer-backed lenders, sometimes including extended terms at attractive rates for specific models.

- Promotional Terms: Keep an eye out for special financing deals, such as 0% APR for a limited term, which can significantly impact your decision. However, these are usually reserved for buyers with excellent credit on new vehicles.

The "Sweet Spot" for Car Loan Length: Is There One?

Given the wide range of options and influencing factors, many buyers wonder if there’s a universally "best" car loan term. The truth is, there isn’t a single sweet spot that applies to everyone. The ideal loan length is highly individual, determined by a careful balance of your financial situation, personal preferences, and the specific car you’re purchasing.

For many years, 60 months (5 years) was considered a standard and often recommended term. It provided a reasonable balance between manageable monthly payments and a lower total interest burden. However, with the rising average cost of new vehicles, 72-month (6-year) loans have become increasingly popular, allowing buyers to afford more expensive cars with lower monthly outflows.

Based on my experience, the "sweet spot" is the longest term you can comfortably afford while still paying the least amount of interest possible, ideally without entering a negative equity situation. This often means aiming for the shortest term whose monthly payment fits comfortably within your budget without causing financial strain. For some, this might be 36 months, for others, 72 months might be the practical limit. The key is to run the numbers and find your personal equilibrium.

Potential Pitfalls of Extended Car Loan Terms (72+ Months)

While longer loan terms offer the immediate gratification of lower monthly payments, they come with significant long-term risks that many buyers overlook. Being aware of these potential pitfalls is crucial for making a responsible financial decision.

1. The Peril of Negative Equity (Being "Upside Down")

This is perhaps the most dangerous aspect of extended car loan terms. Negative equity, often called being "upside down" or "underwater," occurs when you owe more on your car loan than the car is currently worth.

- How it Happens: Cars depreciate rapidly, especially in the first few years. If your loan term is long, your principal balance decreases slowly. The car’s value can drop faster than you pay off the loan, leaving you in a negative equity position.

- The Risks: If your car is totaled in an accident, your insurance payout might only cover the car’s actual cash value, leaving you responsible for the remaining loan balance. Similarly, if you want to trade in your car, you’ll have to pay the difference between your outstanding loan and the trade-in value, or roll that negative equity into a new loan, digging an even deeper financial hole. This scenario is a common trap for buyers who consistently opt for long terms and low down payments.

2. Significantly Increased Total Interest

This cannot be stressed enough. The longer you take to repay a loan, the more interest you’ll accrue. Even a seemingly small increase in interest rate or a few extra months can add up to thousands of dollars over the life of the loan.

- Example (Conceptual): Imagine financing $30,000 at 5% APR. Over 60 months, your total interest might be around $3,900. Extend that to 84 months, and your total interest could jump to over $5,500 – an extra $1,600 simply for the convenience of lower monthly payments. These numbers illustrate the principle; actual figures depend on specific rates.

3. Loan Fatigue and Financial Burden

Committing to a car payment for six, seven, or even eight years can lead to "loan fatigue." The novelty of the new car wears off, but the monthly obligation persists.

- Impact on Financial Flexibility: This long-term debt can hinder your ability to save for other significant life events, invest, or simply enjoy financial freedom. It becomes a persistent drain on your budget, potentially for longer than you even own the car.

4. Outliving Your Warranty

Most new car manufacturer warranties typically last for 3 years/36,000 miles or 5 years/60,000 miles. If you finance your car for 72 or 84 months, you will likely be making payments on a vehicle that is no longer covered by its original warranty for a significant portion of the loan term.

- The Cost of Repairs: This means any major mechanical issues that arise in the later years of your loan will come directly out of your pocket, adding to your financial burden while you’re still paying off the initial purchase.

Strategies for Choosing the Right Car Loan Term

Making an informed decision about your car loan length requires careful planning and a realistic assessment of your financial situation. Here are actionable strategies to help you choose the term that’s best for you:

1. Assess Your Budget Honestly

Before you even start looking at cars, take a hard look at your finances. Determine how much you can truly afford to pay each month without stretching yourself thin.

- Calculate All Costs: Remember to factor in not just the loan payment but also insurance, fuel, maintenance, and potential parking fees. A comprehensive budget review will prevent you from being "car poor."

2. Consider the Car’s Lifespan and Your Ownership Plans

Think about how long you realistically plan to keep the car.

- Match Term to Ownership: Ideally, you want to pay off your car before you plan to replace it or before it becomes prone to major repairs. If you typically trade in your car every 3-5 years, a 7-year loan is likely not the best fit.

3. Shop Around for Lenders and Compare Offers

Don’t settle for the first loan offer you receive, especially at the dealership. Different lenders will have different rates and terms based on their specific criteria.

- Get Multiple Quotes: Contact banks, credit unions, and online lenders to compare interest rates and available loan terms. can provide an in-depth guide on this process. This due diligence can save you thousands over the life of the loan.

4. Make a Significant Down Payment

As discussed, a larger down payment reduces the amount you need to borrow, lowers your monthly payments, and mitigates the risk of negative equity.

- Aim for 20%: While not always feasible, aiming for a 20% down payment on a new car (or 10% on a used car) is a good target to minimize your financial exposure and potentially secure better loan terms.

5. Run the Numbers Thoroughly

Utilize online car loan calculators to model different scenarios. See how changing the loan term affects both your monthly payment and the total interest paid.

- Visualize the Impact: This visual aid can clearly demonstrate the long-term cost implications of choosing a longer term for a lower monthly payment. can provide excellent tools for this.

6. Get Pre-Approved Before Visiting the Dealership

Pre-approval from a bank or credit union gives you a solid understanding of the loan amount, interest rate, and terms you qualify for before you even step foot on a car lot.

- Empower Your Negotiation: This puts you in a stronger negotiating position at the dealership, as you’ll already have a competitive offer in hand. for more detailed information.

Refinancing Your Car Loan: A Second Chance

What if you’ve already taken out a car loan and now realize the term isn’t ideal, or your financial situation has changed? Refinancing your car loan can offer a valuable opportunity to adjust your terms.

- When to Consider Refinancing:

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan, you might qualify for a lower interest rate, which can lead to substantial savings.

- Lower Interest Rates: If market interest rates have dropped since your initial loan, refinancing can lock you into a more favorable rate.

- Reduce Monthly Payments: By extending your loan term (though be mindful of increased total interest), you can lower your monthly payments for better budget management.

- Shorten Loan Term: If your financial situation has improved, you might want to refinance to a shorter term to pay off the car faster and save on interest.

- How it Works: Refinancing involves taking out a new loan to pay off your existing car loan. The new loan will come with new terms, including a new interest rate and a new loan duration. Pro tips from us: Always calculate the total cost savings (or increased cost) of refinancing. Ensure the fees associated with the new loan don’t outweigh the benefits.

Conclusion: Your Informed Decision is Key

The question of "How long can you get a car loan for?" is far more nuanced than it appears on the surface. There’s no single right answer, as the ideal car loan length is deeply personal, influenced by your credit health, financial capacity, the vehicle itself, and your long-term goals.

As an expert in the auto financing space, my ultimate advice is to prioritize financial wisdom over immediate gratification. While lower monthly payments offered by longer terms can be tempting, always weigh them against the significant increase in total interest paid and the heightened risk of negative equity. Conversely, shorter terms, though demanding higher monthly outflows, offer the fastest path to debt freedom and substantial savings.

By thoroughly understanding the interplay of loan terms, interest rates, and your personal finances, and by employing the strategies outlined in this guide, you empower yourself to make a truly informed decision. Choose a car loan term that not only gets you into the car you desire but also supports your overall financial health, ensuring a smooth and stress-free journey down the road. Drive smart, not just far!