Decoding Your Drive: How Your Credit Score Directly Impacts Your Car Loan APR

Decoding Your Drive: How Your Credit Score Directly Impacts Your Car Loan APR Carloan.Guidemechanic.com

The open road, the scent of a new car, the thrill of freedom – buying a car is an exciting milestone for many. However, beneath the gleaming paint and the powerful engine lies a crucial financial decision: securing a car loan. And when it comes to financing, few things are as impactful on your wallet as your Car Loan APR By Credit Score.

Understanding the intricate relationship between your creditworthiness and the Annual Percentage Rate (APR) you’re offered can save you thousands of dollars over the life of your loan. This isn’t just about getting approved; it’s about getting the best deal possible. As expert bloggers and professional SEO content writers, our mission is to empower you with the knowledge to navigate this complex landscape, turning potential pitfalls into stepping stones for a smarter financial future.

Decoding Your Drive: How Your Credit Score Directly Impacts Your Car Loan APR

In this super comprehensive guide, we’ll peel back the layers of car financing, demystifying APR, breaking down credit score ranges, and equipping you with actionable strategies to secure the most favorable terms. Get ready to transform your car buying experience from confusing to confident.

What Exactly is APR and Why Does It Matter So Much?

Before we dive into credit scores, let’s clarify a fundamental concept: APR. Many people confuse APR with a simple interest rate, but they are distinct, and understanding the difference is paramount for any borrower.

The Annual Percentage Rate (APR) represents the true annual cost of borrowing money. It’s not just the interest rate; it also includes any additional fees or charges associated with the loan, such as administrative fees, origination fees, or discount points, spread out over the loan term. This comprehensive figure provides a more accurate picture of what you’ll pay each year.

The interest rate, on the other hand, is simply the percentage charged by the lender for borrowing the principal amount. While the interest rate is a significant component of the APR, it doesn’t encompass all the potential costs. Think of the interest rate as the core cost of borrowing, and the APR as that core cost plus any extra charges rolled into one annual percentage.

Why does this distinction matter? Because a seemingly low interest rate might hide high fees that push the overall APR much higher than you initially expected. Always focus on the APR when comparing loan offers, as it gives you the most complete cost analysis. A lower APR means a lower total cost for your car loan over time, directly impacting your monthly payments and overall financial burden.

The Credit Score Conundrum: Your Financial Report Card

At the heart of every lending decision, especially for a car loan, lies your credit score. This three-digit number is essentially your financial report card, a snapshot of your creditworthiness that lenders use to assess the risk of lending money to you. A higher score signals lower risk, while a lower score suggests a higher risk.

The most commonly used credit scoring models are FICO Score and VantageScore. While they use slightly different methodologies, both evaluate similar factors: your payment history, amounts owed, length of credit history, new credit, and credit mix. Each of these components contributes to the final score that dictates your financial reputation.

Lenders rely heavily on your credit score because it predicts the likelihood of you repaying your loan on time. It’s their primary tool for risk assessment. Based on your score, they determine not only whether to approve your loan but also the terms they’re willing to offer, with the APR being the most significant variable.

Car Loan APR By Credit Score: A Detailed Breakdown

Now, let’s get to the core of the matter: how your credit score directly translates into the APR you can expect for your car loan. We’ll break this down by common credit score ranges, offering insights and expectations for each.

Excellent Credit (780-850 FICO Score)

If your credit score falls into this top-tier range, congratulations! You are considered an exceptionally low-risk borrower. Lenders are eager to do business with you, leading to the most competitive rates and favorable terms.

Typical APR Range: For new cars, you could see APRs as low as 0% to 3.5%. For used cars, rates might be slightly higher, typically ranging from 2.5% to 5%. These figures are highly dependent on market conditions and specific lender promotions.

Benefits: With excellent credit, you’ll enjoy the absolute lowest interest rates, which translates to the smallest total cost for your vehicle. You’ll also have the widest selection of lenders, allowing you to shop around for the best deal with ease. Additionally, lenders may offer more flexible repayment terms, larger loan amounts, and fewer requirements for down payments or co-signers.

Pro tips from us: Even with excellent credit, don’t just accept the first offer. Shop around aggressively. Get pre-approved from several banks and credit unions before stepping into a dealership. This competitive environment ensures you leverage your strong credit to its maximum potential. You might also qualify for special manufacturer incentives, which can often be combined with low APR offers.

Good Credit (670-739 FICO Score)

Borrowers with good credit are still viewed as reliable and responsible. While you might not qualify for the absolute lowest rates reserved for excellent credit, you’ll still receive very competitive offers.

Typical APR Range: For new cars, you can expect APRs generally between 3.5% and 6%. For used cars, this range might be 4.5% to 8%. Again, these are averages and can fluctuate based on economic factors.

Opportunities: With a good credit score, you’re in a strong position, but there’s always room for improvement. Focus on maintaining timely payments and reducing any outstanding debt to push your score into the excellent category before your next big purchase. This range often offers a sweet spot where rates are manageable, and options are still plentiful.

Based on my experience, individuals in this range can significantly benefit from comparing pre-approvals. While dealerships might offer decent rates, a local credit union or an online lender might surprise you with an even better offer. Don’t leave money on the table by only checking one source.

Fair Credit (580-669 FICO Score)

If your credit score falls into the fair range, lenders perceive you as a moderate risk. You might have some blemishes on your credit history, such as late payments or higher debt utilization, which will result in higher APRs.

Typical APR Range: Expect new car APRs to be in the range of 6% to 12%, and used car APRs from 8% to 15% or even higher. The difference in total cost compared to good or excellent credit becomes quite significant here.

Challenges and Strategies: Securing a loan with fair credit is certainly possible, but it requires more diligence. Shopping around becomes even more critical, as rates can vary widely between lenders. Be wary of predatory lenders who might offer seemingly easy approvals with exorbitant rates. Consider working with a credit union, which often has more flexible lending criteria.

Common mistakes to avoid are settling for the first loan offer without exploring alternatives. Also, avoid extending the loan term excessively to lower monthly payments, as this dramatically increases the total interest paid. A larger down payment can also significantly help your chances and lower your APR in this range.

Poor/Bad Credit (300-579 FICO Score)

This range indicates a higher risk for lenders due to a history of missed payments, defaults, or high debt. While getting a car loan is still possible, it comes with the highest APRs and more restrictive terms.

Typical APR Range: New car APRs can start at 10% and go upwards of 20%, while used car APRs can easily exceed 15% and climb past 25% or even higher. These rates can add thousands of dollars to the total cost of your car.

Navigating the Landscape: Getting a car loan with bad credit is challenging, but not impossible. You’ll likely need to focus on specific "subprime" lenders who specialize in higher-risk loans. Be incredibly cautious and scrutinize every detail of the loan agreement to avoid unfavorable terms or hidden fees.

Alternative Options:

- Co-signer: A creditworthy co-signer can significantly improve your chances of approval and help you secure a lower APR. Their credit history essentially backs your loan.

- Secured Loans: Some lenders offer secured car loans, where the car itself serves as collateral. This can reduce the perceived risk for the lender.

- Larger Down Payment: A substantial down payment reduces the loan amount, making you a less risky borrower and potentially qualifying you for a better rate.

- Improve Your Credit First: If possible, consider delaying your car purchase and dedicating time to improving your credit score. Even a few points can make a difference.

Based on my experience, rushing into a bad credit car loan without exploring all options can lead to financial regret. It’s often better to save up for a larger down payment or work on credit repair for a few months if immediate transportation isn’t a dire emergency.

Factors Beyond Credit Score That Influence Your APR

While your credit score is the primary determinant of your Car Loan APR By Credit Score, it’s not the only factor. Several other variables play a significant role in the final rate you’re offered.

- Loan Term: The length of your repayment period directly impacts your APR. Shorter loan terms (e.g., 36 or 48 months) typically come with lower APRs because the lender’s risk is spread over a shorter period. Longer terms (e.g., 60 or 72 months) often have higher APRs, despite offering lower monthly payments, because the lender is taking on risk for a longer duration.

- Loan Amount: The total amount you borrow can also influence the rate. Very small loans might have slightly higher rates due to fixed administrative costs, while very large loans might also see slight adjustments based on the lender’s portfolio risk.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, meaning you’re borrowing less relative to the car’s value. This makes you a less risky borrower and can often lead to a lower APR. Lenders appreciate your commitment when you put more money down upfront.

- Vehicle Type (New vs. Used): New cars typically qualify for lower APRs than used cars. This is because new cars hold their value better initially, are less likely to have unforeseen mechanical issues, and often come with manufacturer incentives that include low-interest financing. Used cars are considered higher risk due to depreciation and potential maintenance issues.

- Lender Type: Different types of lenders have different risk appetites and rate structures.

- Banks: Offer competitive rates, especially for borrowers with good to excellent credit.

- Credit Unions: Often known for offering slightly better rates than traditional banks, particularly for members, and may be more flexible with fair credit borrowers.

- Dealerships: While convenient, their financing (often through captive finance companies or third-party lenders) may not always be the best. They often mark up rates from what you could get elsewhere.

- Online Lenders: Can be very competitive and offer quick pre-approvals.

- Current Interest Rate Environment: Macroeconomic factors, such as the federal funds rate set by the central bank, influence interest rates across the board. When the federal funds rate is low, overall loan rates tend to be lower, and vice-versa. This is beyond your control but can significantly affect your APR.

Strategies to Secure the Best Car Loan APR

Regardless of your current credit standing, there are proactive steps you can take to improve your chances of securing the most favorable Car Loan APR By Credit Score.

1. Improve Your Credit Score

This is arguably the most impactful strategy. Even a small improvement can shift you into a better credit tier.

- Pay Bills on Time, Every Time: Payment history is the most significant factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Existing Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can quickly boost your score. Aim to keep this below 30%.

- Check Your Credit Report for Errors:

Regularly review your credit reports from all three major bureaus (Experian, Equifax, TransUnion). Dispute any inaccuracies, as they can negatively impact your score. You can get free copies annually. - Don’t Open Too Many New Credit Lines: Each new credit application can result in a hard inquiry, which temporarily dings your score. Only apply for credit when absolutely necessary.

- Become an Authorized User: If someone with excellent credit adds you as an authorized user on their credit card, their good payment history can positively reflect on your report (provided they use it responsibly).

2. Shop Around Aggressively for Pre-Approval

Never rely on the first loan offer you receive, especially from a dealership. Get pre-approved from multiple lenders – banks, credit unions, and online lenders – before you visit the car lot.

Pro tips from us: Most credit scoring models treat multiple hard inquiries for the same type of loan (like an auto loan) within a 14-45 day window as a single inquiry. This allows you to rate shop without further damaging your score. This strategy empowers you with concrete loan offers, giving you strong negotiating power at the dealership.

3. Make a Larger Down Payment

As discussed, a substantial down payment reduces the amount you need to borrow and improves your loan-to-value ratio. This makes you a less risky borrower in the eyes of lenders, often resulting in a lower APR. Aim for at least 20% if possible, especially for used cars.

4. Consider a Co-signer (If Needed)

If you have fair or poor credit, a co-signer with an excellent credit history can be your secret weapon. Their creditworthiness offsets your risk, helping you qualify for a much lower APR than you would on your own. However, remember that the co-signer is equally responsible for the loan, so choose someone you trust and who understands the commitment.

5. Choose a Shorter Loan Term

While a longer loan term offers lower monthly payments, it invariably leads to a higher total cost due to increased interest and often a higher APR. If your budget allows, opt for the shortest loan term you can comfortably afford. This will significantly reduce the overall interest you pay and get you out of debt faster.

6. Negotiate More Than Just the Price

Once you have your pre-approvals in hand, you’re in a strong position. Don’t just negotiate the car’s price; use your pre-approved rates to negotiate the financing offered by the dealership. They may be willing to match or even beat your external offers to close the sale.

The Pre-Approval Process: Your Secret Weapon

The pre-approval process is a powerful tool in your car-buying arsenal. It means a lender has reviewed your credit history and financial situation and determined how much they are willing to lend you, along with an estimated APR.

Benefits:

- Know Your Budget: You’ll know exactly how much car you can afford before you start shopping, preventing you from falling in love with a vehicle outside your price range.

- Negotiating Power: Armed with a pre-approval, you walk into the dealership as a cash buyer. You can focus on negotiating the car’s price, not just the monthly payment, and then compare the dealer’s financing offer against your pre-approval.

- Reduced Stress: The financial heavy lifting is done upfront, allowing you to enjoy the car shopping experience more.

Soft vs. Hard Inquiries: Most pre-approvals involve a "soft inquiry" on your credit report, which doesn’t affect your score. Once you decide to proceed with a specific lender, they’ll conduct a "hard inquiry," which can temporarily lower your score by a few points. However, as mentioned, multiple hard inquiries for the same type of loan within a short period are usually grouped into one.

Common Mistakes to Avoid When Financing a Car

Even savvy buyers can fall into common traps. Being aware of these can save you from costly errors.

- Focusing Only on Monthly Payments: Dealerships love to talk about low monthly payments. However, a low monthly payment can hide a very long loan term or a high APR, leading to a much higher total cost. Always look at the total cost of the loan, including interest.

- Not Understanding the Full Loan Terms: Before signing, read every single line of your loan agreement. Understand the APR, loan term, any prepayment penalties, and all associated fees. Don’t be afraid to ask questions.

- Accepting Dealer Financing Without Comparison: While convenient, dealer financing isn’t always the best deal. Always compare their offer with pre-approvals you’ve secured from other lenders.

- Ignoring the Total Cost of the Loan: Add up the principal, interest, and any fees. This is the real price you’re paying for the car, and it’s often significantly higher than the sticker price.

- Not Checking Your Credit Score Beforehand: Going into the car buying process blind to your credit score puts you at a severe disadvantage. You won’t know what kind of APR to expect or how to negotiate effectively.

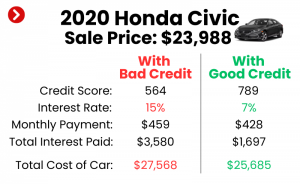

Real-World Scenarios: APR in Action

Let’s illustrate how drastically Car Loan APR By Credit Score impacts your total cost with a hypothetical scenario:

Imagine you’re buying a $30,000 car and making a $5,000 down payment, so you’re financing $25,000 over 60 months.

- Excellent Credit (e.g., 3.5% APR):

- Monthly Payment: Approximately $454

- Total Interest Paid: Approximately $2,240

- Good Credit (e.g., 6.0% APR):

- Monthly Payment: Approximately $483

- Total Interest Paid: Approximately $3,980

- Fair Credit (e.g., 10.0% APR):

- Monthly Payment: Approximately $531

- Total Interest Paid: Approximately $6,860

- Bad Credit (e.g., 20.0% APR):

- Monthly Payment: Approximately $662

- Total Interest Paid: Approximately $14,720

As you can see, the difference between an excellent credit APR and a bad credit APR on the same $25,000 loan over 60 months is over $12,000 in interest alone! This stark contrast underscores why understanding and optimizing your credit score is so crucial.

Conclusion: Your Road to a Better Car Loan Starts Here

Navigating the world of car loans can feel overwhelming, but armed with a thorough understanding of Car Loan APR By Credit Score, you are now in a powerful position. Your credit score is not just a number; it’s a direct determinant of how much you’ll ultimately pay for your vehicle. From years of observing car buyers, I can confidently say that the most successful ones are those who do their homework.

Remember, a lower APR isn’t just a minor saving; it’s thousands of dollars that stay in your pocket, not a lender’s. By actively working to improve your credit, diligently shopping around for pre-approvals, making a smart down payment, and understanding all the factors at play, you can transform a potentially costly transaction into a financially sound decision.

Don’t let the excitement of a new car overshadow the importance of smart financing. Take control of your car loan journey, understand your credit, and drive away not just with a new car, but with the peace of mind that comes from securing the best possible Car Loan APR By Credit Score. Your wallet will thank you.