Decoding Your Drive: The Essential Car Loan Factors You Absolutely Need to Master

Decoding Your Drive: The Essential Car Loan Factors You Absolutely Need to Master Carloan.Guidemechanic.com

The open road, the fresh scent of a new car, the feeling of independence – owning a vehicle is a significant milestone for many. But before you hit the gas, there’s a crucial journey you need to navigate: securing a car loan. This isn’t just about finding the lowest monthly payment; it’s about understanding the intricate web of car loan factors that determine the true cost of your vehicle and your financial commitment.

As an expert blogger with years of experience dissecting personal finance, I’ve seen countless individuals make common mistakes that cost them thousands. My mission today is to equip you with the in-depth knowledge needed to approach car financing with confidence. We’ll explore every critical element, transforming you from a hopeful buyer into a savvy borrower.

Decoding Your Drive: The Essential Car Loan Factors You Absolutely Need to Master

This comprehensive guide will demystify the complex world of auto loans, ensuring you make informed decisions that benefit your wallet in the long run. Let’s buckle up and dive deep into the essential car loan factors that will shape your next automotive adventure.

Understanding the Road Ahead: Essential Car Loan Factors You Can’t Ignore

Securing a car loan involves more than just picking a car and signing on the dotted line. It’s a strategic financial decision influenced by a multitude of interconnected variables. Each of these car loan factors plays a pivotal role in determining whether your loan application is approved, what interest rate you’ll receive, and ultimately, how much you’ll pay over the life of the loan.

Ignoring any of these elements can lead to higher costs, unfavorable terms, or even rejection. By understanding these factors proactively, you gain leverage. You can improve your financial standing, negotiate better deals, and ensure your car purchase aligns perfectly with your budget.

This isn’t just theory; it’s practical knowledge designed to save you money and stress. Let’s break down each key factor one by one, revealing how they impact your car buying experience.

1. The Power of Your Credit Score: Your Financial Passport

Your credit score is arguably the single most influential car loan factor. It acts as a financial report card, telling lenders how reliably you’ve managed debt in the past. A higher score signals less risk, while a lower score suggests a greater chance of default.

What is a Credit Score and Why Does it Matter?

A credit score is a three-digit number, typically ranging from 300 to 850 (FICO and VantageScore are the most common models). It’s calculated based on your credit history, including payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use this score to quickly assess your creditworthiness.

A good or excellent credit score (generally 700+) can unlock the best interest rates, saving you thousands over the life of your loan. Conversely, a poor score might lead to higher interest rates, stricter terms, or even outright loan denial. Based on my experience, a higher credit score is like having a VIP pass to the best financing deals available.

How Your Credit Score Directly Impacts Your Car Loan

The correlation between your credit score and the interest rate you receive is direct and profound. For example, a borrower with an excellent credit score might qualify for an APR of 3-5%, while someone with a fair score could face rates of 8-12% or even higher. This difference, compounded over several years, translates into a significant disparity in the total amount you pay for the same car.

Even a percentage point or two can drastically alter your total cost. Therefore, understanding your credit score and working to improve it before applying for an auto loan is one of the smartest moves you can make. It truly is a cornerstone among all car loan factors.

Pro Tips for Boosting Your Credit Score Before You Buy

- Check Your Credit Report: Obtain free copies of your credit report from AnnualCreditReport.com. Look for errors and dispute any inaccuracies immediately.

- Pay Bills On Time: This is the most crucial factor. Set up reminders or automatic payments to avoid missing due dates.

- Reduce Debt: Lowering your credit utilization ratio (the amount of credit you use compared to your total available credit) can positively impact your score.

- Avoid New Credit Applications: Limit opening new credit accounts in the months leading up to your car loan application, as each inquiry can temporarily dip your score.

2. The Mighty Down Payment: Laying a Strong Foundation

Your down payment is the cash you pay upfront toward the purchase price of the vehicle. It’s another critical car loan factor that directly influences the size of your loan, your monthly payments, and the total interest you’ll accrue.

Why a Larger Down Payment Makes a Big Difference

A substantial down payment offers several significant advantages. Firstly, it reduces the amount you need to borrow, which in turn lowers your monthly payments. Secondly, because you’re borrowing less, you’ll pay less interest over the life of the loan. This can lead to substantial savings.

Furthermore, a larger down payment demonstrates financial stability to lenders, potentially making you eligible for better interest rates. It also helps reduce your loan-to-value (LTV) ratio, which is the amount of the loan compared to the car’s value. A lower LTV is less risky for lenders.

How Much is Ideal?

While there’s no universal magic number, a common recommendation is to put down at least 10-20% for a new car and often more for a used car. For example, on a $30,000 car, a 20% down payment would be $6,000. This significantly reduces your principal, making your loan more manageable.

Consider your budget and how much you can comfortably afford upfront without depleting your emergency savings. Striking the right balance here is key to managing this important car loan factor.

Leveraging Your Current Vehicle: The Trade-In

If you have an existing vehicle, trading it in can act just like a down payment. The value of your trade-in is applied directly to the purchase price of your new car, reducing the amount you need to finance.

Pro tips from us: Do your research before heading to the dealership. Get an independent appraisal of your car’s value from sources like Kelley Blue Book or Edmunds. This knowledge empowers you to negotiate a fair trade-in value and ensures you’re getting the most out of your old vehicle.

3. Unpacking Interest Rates and APR: The True Cost of Your Car Loan

Beyond the sticker price, the interest rate is perhaps the most impactful car loan factor determining the total cost of your vehicle. It’s the fee you pay to the lender for borrowing money.

What is an Interest Rate and What Influences It?

The interest rate is expressed as a percentage of the principal loan amount. It’s how lenders make a profit. Several elements influence the interest rate you’re offered:

- Your Credit Score: As discussed, a higher score typically leads to lower rates.

- Loan Term: Shorter loan terms often come with lower interest rates because the lender’s risk is reduced.

- Lender: Different banks, credit unions, and dealerships offer varying rates. Shopping around is crucial.

- Economic Conditions: Broader economic factors, like the Federal Reserve’s interest rate policies, can influence auto loan rates across the board.

- Vehicle Type: New cars often qualify for lower rates than used cars due to their predictable value and lower risk of mechanical issues.

Fixed vs. Variable Interest Rates

Most auto loans come with a fixed interest rate, meaning your rate and monthly payment remain the same throughout the loan term. This provides stability and predictability. While less common for car loans, some lenders might offer variable rates, which can fluctuate with market conditions. For the sake of financial predictability, fixed rates are generally preferred for car loans.

Pro Tip: Don’t just look at the monthly payment. While it’s important for budgeting, always consider the total interest you’ll pay over the life of the loan. A slightly higher monthly payment on a shorter term with a lower rate can save you thousands in the long run.

APR vs. Interest Rate: Knowing the Whole Picture

While often used interchangeably, the Annual Percentage Rate (APR) is a more comprehensive measure of your loan’s cost than the interest rate alone. The APR includes the interest rate plus any additional fees charged by the lender, such as origination fees or closing costs, spread out over the loan term.

Comparing APRs from different lenders provides a more accurate apples-to-apples comparison of the true cost of borrowing. A loan with a slightly lower interest rate but higher fees might actually have a higher APR than a loan with a slightly higher interest rate but no fees. Always ask for the APR to fully understand this critical car loan factor.

For a deeper dive into understanding APR and its components, you can refer to this helpful guide from a trusted external source: Investopedia’s Explanation of APR

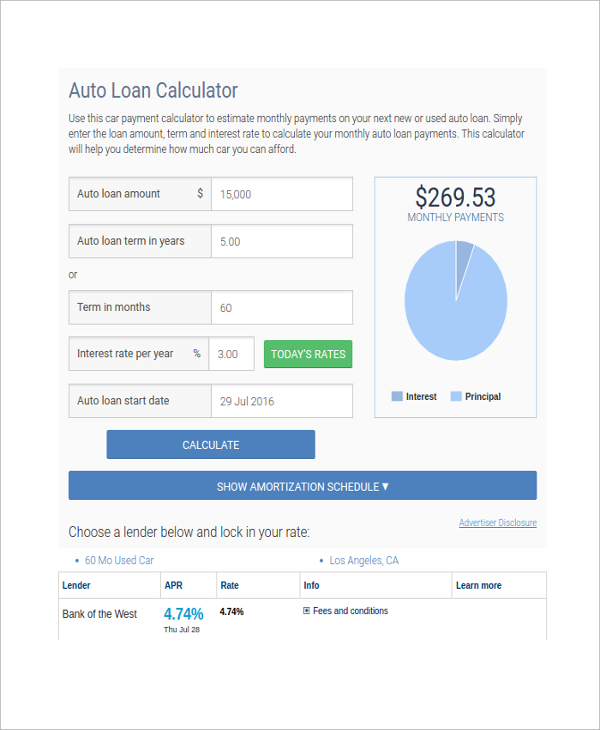

4. The Loan Term: Balancing Monthly Payments and Total Cost

The loan term, or the length of time you have to repay the loan, is another pivotal car loan factor that directly impacts both your monthly payment and the total amount of interest you’ll pay. Common terms range from 36 to 84 months, with 60 or 72 months being very popular.

Shorter Term: Less Interest, Higher Payments

Choosing a shorter loan term, such as 36 or 48 months, means you’ll pay off your car faster. Because the principal is repaid more quickly, the lender charges interest for a shorter period, resulting in significantly less total interest paid over the life of the loan. However, this comes with the trade-off of higher monthly payments.

If your budget can comfortably accommodate the higher payments, a shorter term is often the most financially savvy choice. It minimizes the total cost of ownership and helps you build equity in your car faster.

Longer Term: Lower Payments, More Interest

Conversely, opting for a longer loan term, like 72 or 84 months, will reduce your monthly payments. This can make a more expensive car seem more affordable on a month-to-month basis. However, the extended repayment period means you’ll pay substantially more in total interest.

Common mistakes to avoid are automatically opting for the longest term just to get the lowest possible monthly payment without considering the overall cost. While it might seem manageable now, you could end up paying thousands more for the same vehicle. Additionally, a longer term increases the risk of being "upside down" on your loan, where you owe more than the car is worth, especially with rapid depreciation.

Finding Your Sweet Spot

The ideal loan term balances affordability with the total cost. Consider your budget carefully. What’s the highest monthly payment you can comfortably afford without straining your finances? Then, compare how different loan terms impact the total interest paid.

For a more detailed look at budgeting for your car loan and understanding monthly payments, check out our article: . Understanding these trade-offs is crucial for mastering the various car loan factors.

5. Your Debt-to-Income Ratio: A Lender’s View of Your Capacity

Beyond your credit score, lenders also scrutinize your debt-to-income (DTI) ratio. This important car loan factor offers a clear picture of your financial capacity to take on new debt.

What is the Debt-to-Income Ratio?

Your DTI ratio is a percentage that compares your total monthly debt payments to your gross monthly income (before taxes and deductions). For example, if your monthly debt payments (rent/mortgage, credit cards, student loans, existing car loans) total $1,500 and your gross monthly income is $4,000, your DTI is 37.5% ($1,500 / $4,000 = 0.375).

Why Lenders Care About Your DTI

Lenders use your DTI to assess your ability to manage additional debt. A high DTI indicates that a significant portion of your income is already committed to existing obligations, making you a higher risk for a new loan. They want to ensure you have enough disposable income to comfortably make your car loan payments.

While ideal DTI ratios can vary slightly by lender, most prefer a DTI of 36% or less, though some might go up to 43% for well-qualified borrowers. A lower DTI strengthens your loan application and can lead to better terms.

Beyond the Loan: True Affordability and Hidden Costs

When considering your capacity, it’s vital to look beyond just the loan payment. A car comes with numerous ongoing expenses that must fit into your overall budget. These hidden costs can quickly turn an "affordable" monthly payment into a financial burden if not properly planned for.

These include:

- Car Insurance: Premiums vary widely based on your vehicle, driving record, age, and location.

- Fuel Costs: Consider your daily commute and current gas prices.

- Maintenance and Repairs: All cars need regular servicing, and older cars might require more frequent repairs.

- Registration and Licensing Fees: Annual costs imposed by your state.

- Parking Fees/Tolls: If applicable to your routine.

Pro Tip: Create a comprehensive budget that includes all potential car ownership costs, not just the loan payment. This holistic approach ensures you truly understand your affordability and manage this crucial car loan factor. For more on these often-overlooked expenses, check out our guide: .

6. The Vehicle Itself: New vs. Used, Make and Model

The specific vehicle you choose also plays a significant role in the car loan factors equation. Lenders assess the risk associated with the car itself.

New vs. Used Car Loans

- New Cars: Generally considered lower risk by lenders. They have a predictable value, come with warranties, and are less likely to have immediate mechanical issues. This often translates to lower interest rates and longer loan terms for new vehicles.

- Used Cars: Can be perceived as higher risk due to potential mechanical problems, unknown history, and more rapid depreciation. Interest rates for used car loans are typically higher, and loan terms might be shorter, especially for older models.

However, used cars are usually more affordable upfront and depreciate less rapidly than new cars once purchased. The key is to find a balance between the car’s price, its reliability, and the associated loan terms.

Make, Model, and Loan-to-Value (LTV)

The specific make and model of the car also matter. Some vehicles hold their value better than others, which is attractive to lenders. A car with strong resale value reduces the lender’s risk if they ever need to repossess and sell it.

The loan-to-value (LTV) ratio is particularly important here. This is the ratio of the loan amount to the car’s actual market value. If you borrow more than the car is worth (e.g., due to negative equity from a trade-in or excessive add-ons financed into the loan), your LTV will be high. Lenders prefer a lower LTV as it means they are lending less relative to the asset’s value, which reduces their exposure. This is why a down payment is so effective in improving your loan terms.

7. The Lender’s Role: Banks, Credit Unions, and Dealerships

Finally, the institution providing your loan is a critical car loan factor. Where you choose to borrow can significantly impact the terms and rates you receive.

Exploring Your Lender Options

- Banks: Traditional banks are a popular choice. They offer competitive rates, a wide range of loan products, and often have online application processes.

- Credit Unions: These member-owned financial cooperatives are known for often offering some of the lowest interest rates on auto loans. Membership is usually required but is often easy to obtain.

- Dealership Financing: Dealerships offer convenience, allowing you to arrange financing directly at the point of sale. They often work with multiple lenders to find you a deal. However, their rates may not always be the most competitive, and there can be markups. They also sometimes offer special manufacturer incentives (0% APR) which can be excellent but often require top-tier credit.

The Power of Pre-Approval

Pro Tip: Always get pre-approved for a loan before you step foot on a dealership lot. Pre-approval gives you a firm offer from a lender, outlining the maximum amount you can borrow and the interest rate you qualify for. This empowers you to negotiate with the dealership as a cash buyer, knowing exactly what financing you can secure independently.

Comparing offers from multiple lenders – banks, credit unions, and even online lenders – is crucial. Don’t settle for the first offer you receive. Shopping around can reveal significant differences in interest rates and fees, saving you a substantial amount of money over the life of the loan.

Conclusion: Driving Away with Confidence

Navigating the world of car loans can seem daunting, but by thoroughly understanding these essential car loan factors, you empower yourself to make intelligent, cost-effective decisions. From your credit score to the loan term, your down payment to the specific vehicle you choose, each element plays a vital role in shaping your financial commitment.

Remember, a car loan isn’t just about the monthly payment; it’s about the total cost of ownership. By diligently researching, preparing your finances, and shopping around for the best terms, you can significantly reduce the overall expense of your vehicle. Don’t let excitement overshadow prudence.

Armed with this in-depth knowledge, you’re now ready to approach the car buying process with confidence and clarity. Drive away not just with a new car, but with the peace of mind that comes from mastering the car loan factors and securing a deal that truly works for you. Happy driving!