Decoding Your Drive: The Ultimate Guide to Amortization of a Car Loan

Decoding Your Drive: The Ultimate Guide to Amortization of a Car Loan Carloan.Guidemechanic.com

Buying a car is an exciting milestone, often marking a new chapter of independence and adventure. For most of us, this significant purchase involves financing, meaning we take out a car loan. While the monthly payment amount is often the primary focus, there’s a powerful underlying mechanism at play that dictates how your money is actually being allocated: amortization of a car loan.

Understanding car loan amortization isn’t just about knowing a financial term; it’s about gaining control over one of your largest recurring expenses. It’s the key to saving money, paying off your debt faster, and making smarter financial decisions for years to come. In this comprehensive guide, we’ll peel back the layers of car loan amortization, empowering you with the knowledge to navigate your auto financing with confidence.

Decoding Your Drive: The Ultimate Guide to Amortization of a Car Loan

What Exactly Is Amortization? (And Why It Matters for Your Car Loan)

At its core, amortization refers to the process of gradually paying off a debt over a set period through regular, fixed payments. Each payment you make on your car loan isn’t just a lump sum; it’s carefully divided between two critical components: the principal and the interest. The principal is the original amount of money you borrowed, while the interest is the cost of borrowing that money.

For car loans, this process follows a specific pattern, often described as an amortization schedule. This schedule acts like a financial roadmap, detailing how much of each payment goes towards reducing your loan balance (principal) and how much goes to the lender as their fee (interest). Ignoring this roadmap can lead to paying far more than necessary over the life of your loan.

The Anatomy of a Car Loan Payment: Principal vs. Interest

One of the most crucial aspects of car loan amortization is understanding how the principal and interest portions of your payment shift over time. When you first start paying off your car loan, a disproportionately large percentage of your monthly payment goes towards interest. This is a standard practice in lending, often referred to as "front-loading" the interest.

As your loan matures and you make more payments, this allocation gradually reverses. The interest portion of your payment decreases, and a larger share of your payment begins to chip away at the principal balance. This shift means that in the early stages, your equity in the car grows slowly, but it accelerates significantly towards the end of the loan term.

Factors That Influence Your Car Loan Amortization Schedule

Several key variables play a pivotal role in shaping your car loan amortization schedule and, consequently, the total amount you’ll pay. Being aware of these factors allows you to make informed choices before you even sign on the dotted line.

Firstly, the loan amount directly impacts everything. A larger principal balance means more interest will accrue over the life of the loan, simply because there’s more money being borrowed. This is a straightforward relationship: borrow more, pay more.

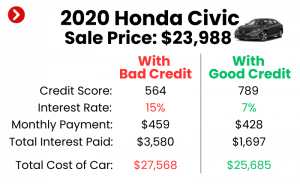

Secondly, the interest rate (APR) is perhaps the most significant influencer. The Annual Percentage Rate (APR) is the true cost of borrowing, expressed as a yearly percentage. A higher APR means a larger portion of each payment goes to interest, increasing your total cost and slowing down your principal reduction. Always strive for the lowest possible APR.

Thirdly, the loan term, or the duration of your loan, has a profound effect. While a longer term (e.g., 72 or 84 months) offers the allure of lower monthly payments, it comes at a steep price. Stretching out your payments means you’ll pay interest for a much longer period, significantly increasing the overall interest paid on the loan. Shorter terms, conversely, mean higher monthly payments but substantially lower total interest.

Lastly, your down payment also plays a critical role. A larger down payment reduces the principal amount you need to borrow from day one. This immediately lowers your monthly payments and, more importantly, reduces the total interest you’ll pay over the life of the loan. It’s a powerful tool for taking control of your amortization from the very beginning.

How to Create and Understand Your Car Loan Amortization Schedule

An amortization schedule is an invaluable tool for any car owner with a loan. It’s a detailed table that breaks down every single payment you’ll make over the life of your loan. Each row typically shows the payment number, the date it’s due, the total payment amount, how much of that payment goes to interest, how much goes to principal, and your remaining loan balance.

You don’t need to be a math wizard to create one. Many online calculators are readily available that can generate a full amortization schedule for you. Simply input your loan amount, interest rate, and loan term, and the calculator will do the rest. Link to a reputable external source like Consumer Financial Protection Bureau for an example calculator: CFPB Auto Loan Calculator

Based on my experience, reviewing this schedule provides immense clarity. It allows you to visualize exactly how your debt is being retired and highlights the "front-loading" of interest we discussed earlier. This transparency is key to effective financial planning and understanding the true cost of your vehicle.

The Power of Early Payments: Accelerating Your Car Loan Payoff

Understanding amortization unlocks a powerful strategy for saving money: making extra payments directly towards your principal. Since interest is calculated on your remaining principal balance, every dollar you reduce from that principal means less interest will accrue in the future. This is where the magic happens.

There are several effective ways to leverage this. One common approach is simply making an extra principal-only payment whenever you have spare cash. Clearly designate these payments to go directly to the principal, not future interest. Another strategy involves making bi-weekly payments instead of monthly. By paying half your monthly payment every two weeks, you effectively make one extra full payment per year, significantly shortening your loan term and reducing total interest.

Pro tips from us include rounding up your monthly payment. If your payment is $375, consider paying $400. That extra $25 might seem small, but consistently applied, it can shave months off your loan. Additionally, consider refinancing your car loan if interest rates have dropped or your credit score has significantly improved. A lower interest rate means more of your payment goes to principal from the start.

Common Mistakes to Avoid When Managing Your Car Loan

While the concept of amortization might seem straightforward, many borrowers fall into common traps that can cost them dearly. Being aware of these pitfalls is the first step to avoiding them.

One of the most prevalent mistakes is only paying the minimum required amount. While this keeps you current on your loan, it fully embraces the front-loaded interest structure, ensuring you pay the maximum possible interest over the loan term. It offers no financial advantage beyond meeting your obligation.

Another common error is ignoring the interest rate during the negotiation phase. A difference of just one or two percentage points in your APR can translate into hundreds, even thousands, of dollars in extra interest over the life of the loan. Always shop around for the best rate before committing.

Extending the loan term unnecessarily is another frequent misstep. Lured by lower monthly payments, many borrowers opt for 72 or even 84-month loans. While the immediate relief is tempting, the long-term financial burden of increased interest paid often far outweighs the benefit of a slightly reduced monthly bill.

Finally, a critical mistake is failing to check for prepayment penalties in your loan agreement. While most car loans today don’t have them, some lenders still include clauses that charge you a fee for paying off your loan early. Always read the fine print before making extra payments to ensure you’re not incurring unexpected costs.

Beyond the Basics: Amortization and Your Financial Future

Understanding car loan amortization extends far beyond just saving money on a single vehicle. It’s a foundational concept that empowers you to build a stronger financial future. By strategically reducing your principal, you build equity in your car faster, which can be beneficial if you decide to sell or trade in your vehicle.

Freeing up cash flow is another significant benefit. Once your car loan is paid off, the money previously allocated to that payment can be redirected towards other financial goals, such as saving for a down payment on a home, investing, or accelerating other debt payments. This creates a powerful snowball effect for your personal finances.

Moreover, managing your car loan effectively by understanding amortization positively impacts your credit score. Consistent, on-time payments, especially when combined with responsible principal reduction, demonstrate financial discipline. This strengthens your credit profile, potentially leading to better rates on future loans and credit products.

Pro Tips for Mastering Your Car Loan Amortization

To truly master the art of managing your car loan and leveraging amortization to your advantage, consider these expert tips:

Firstly, always shop for the best APR. Don’t just accept the first offer from the dealership. Get pre-approved by banks, credit unions, and online lenders before you even step foot on the lot. This gives you negotiating power and ensures you secure the most favorable interest rate.

Secondly, thoroughly understand your loan agreement. Before signing, read every clause. Pay particular attention to the interest rate, loan term, any fees, and specifically check for prepayment penalties. If anything is unclear, ask questions until you fully comprehend the terms.

Thirdly, regularly review your amortization schedule. Use it as a living document. As you make extra payments, you can update your schedule (or use an online calculator) to see the immediate impact on your total interest paid and your remaining loan term. This provides motivation and keeps you on track.

Finally, consider refinancing if market rates drop or your credit improves significantly. Even a small reduction in your interest rate can save you a substantial amount of money over the remaining life of the loan. This strategy is especially powerful if you’ve had your loan for a while and have built a strong payment history.

Conclusion: Take Control of Your Car Loan Today

The amortization of a car loan is more than just a complex financial term; it’s the operational blueprint of your auto financing. By understanding how your payments are allocated between principal and interest, and by recognizing the factors that influence this process, you gain an immense advantage. You move from being a passive borrower to an active manager of your debt.

Armed with this knowledge, you can make informed decisions that save you thousands of dollars, accelerate your path to debt freedom, and strengthen your overall financial health. Don’t let your car loan drive you; take the wheel, understand its amortization, and steer your finances towards a brighter future.