Decoding Your Drive: The Ultimate Guide to Car Loan Interest Percentage

Decoding Your Drive: The Ultimate Guide to Car Loan Interest Percentage Carloan.Guidemechanic.com

The dream of a new car often comes with the reality of a car loan. While the excitement of a shiny new (or new-to-you) vehicle is palpable, understanding the financial engine behind it – your car loan interest percentage – is crucial. This isn’t just a number on a contract; it’s a significant factor that determines the total cost of your vehicle and your financial well-being for years to come.

As an expert blogger and professional SEO content writer who has navigated countless financial landscapes, I’ve seen firsthand how a lack of understanding about interest rates can cost consumers thousands. This comprehensive guide will demystify car loan interest, providing you with the knowledge and strategies to secure the best possible rates and drive away with confidence.

Decoding Your Drive: The Ultimate Guide to Car Loan Interest Percentage

What Exactly is Car Loan Interest Percentage?

At its core, the car loan interest percentage is the cost of borrowing money from a lender to purchase a vehicle. Think of it as the fee the bank or financial institution charges you for allowing you to use their capital. This percentage is typically expressed as an annual rate, meaning it represents the cost over one year.

When you take out a car loan, you agree to repay the principal amount (the original cost of the car) plus this interest. The higher the interest rate, the more you pay over the life of the loan. Understanding this fundamental concept is the first step towards making smart financial decisions.

APR vs. Interest Rate: Why the Difference Matters

Many people use "interest rate" and "APR" interchangeably, but this is a critical mistake. While the interest rate is indeed a component, the Annual Percentage Rate (APR) is the true and more comprehensive measure of your borrowing cost.

Based on my experience, focusing solely on the nominal interest rate can be misleading. The APR includes not just the interest rate, but also any additional fees associated with the loan, such as origination fees, processing fees, or discount points. It provides a holistic view of the total cost of borrowing. Always compare APRs when shopping for a loan, not just the quoted interest rates. This transparency helps you avoid hidden costs.

How Car Loan Interest Works: A Simple Explanation

When you secure a car loan, the lender provides you with a lump sum to buy the car. In return, you agree to make regular payments (usually monthly) over a set period, known as the loan term. Each payment you make consists of two parts: a portion that goes towards reducing the principal balance and a portion that covers the accrued interest.

Early in the loan term, a larger percentage of your payment typically goes towards interest. As you continue to make payments and reduce the principal, a greater portion of each subsequent payment is applied to the principal. This gradual reduction of the principal balance over time is how you eventually pay off the loan.

Key Factors Influencing Your Car Loan Interest Rate

Several variables come into play when lenders determine your specific car loan interest percentage. Understanding these factors can empower you to improve your chances of securing a favorable rate.

1. Your Credit Score: The Ultimate Game Changer

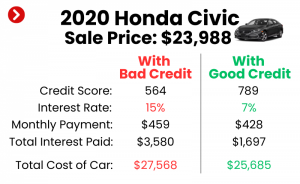

Without a doubt, your credit score is the single most influential factor in determining your car loan interest rate. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your debts. A higher credit score signals a lower risk to lenders.

Individuals with excellent credit (typically 750+) often qualify for the lowest advertised rates, sometimes even 0% APR promotions. Conversely, those with poor credit scores (below 600) can expect significantly higher interest rates, as lenders perceive them as a greater risk. Proactively checking and improving your credit score before applying for a loan is a top priority.

2. The Loan Term: Short vs. Long

The length of your loan, also known as the loan term, plays a crucial role. Shorter loan terms (e.g., 36 or 48 months) generally come with lower interest rates. This is because the lender is exposed to risk for a shorter period. While your monthly payments will be higher with a shorter term, you’ll pay less interest overall.

Longer loan terms (e.g., 60 or 72 months, or even 84 months) typically have higher interest rates. This is due to the increased risk for the lender over an extended period. Although longer terms mean lower monthly payments, you’ll end up paying significantly more in total interest over the life of the loan. It’s a trade-off between affordability now and total cost later.

3. Your Down Payment Amount

Making a substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. Lenders view a larger down payment favorably, as it demonstrates your financial commitment to the purchase. This reduced risk often translates into a lower interest rate for you.

A significant down payment also helps you avoid being "upside down" on your loan, where you owe more than the car is worth. Based on my experience, aiming for at least 20% down on a new car and 10% on a used car is a solid financial strategy.

4. Your Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another metric lenders scrutinize. It compares your total monthly debt payments to your gross monthly income. A low DTI ratio indicates that you have plenty of income left over after paying your debts, making you a less risky borrower.

A high DTI ratio, on the other hand, suggests that you might be stretched thin financially, potentially making it harder to manage additional debt. Lenders prefer borrowers with a DTI ratio below 36%, though some may approve loans with higher ratios depending on other factors. Keeping your DTI in check can positively impact your interest rate.

5. Vehicle Type: New vs. Used Car

The type of vehicle you’re financing can also influence your interest rate. New cars generally come with lower interest rates compared to used cars. This is because new cars hold their value better initially, and lenders perceive them as less risky collateral. They also often come with manufacturer-backed financing incentives that offer very low rates.

Used cars, especially older models, tend to have higher interest rates. This is due to several factors: they depreciate faster, their reliability can be less predictable, and their resale value is often lower. Lenders factor in these increased risks when setting interest rates for pre-owned vehicles.

6. Market Conditions and Economic Climate

The broader economic environment also plays a role in car loan interest percentages. When the Federal Reserve raises or lowers its benchmark interest rates, it ripples through the entire lending market. During periods of economic expansion, interest rates might be higher, while during recessions, rates might drop to stimulate borrowing.

Additionally, the competitive landscape among lenders can affect rates. If there’s a surge in demand for car loans, or if lenders are aggressively competing for market share, you might find more favorable rates. Keeping an eye on financial news can provide insights into current market trends.

7. Lender Type: Where You Borrow From

Where you choose to get your loan can also impact the interest rate. Different types of lenders have different business models and risk appetites.

- Banks: Traditional banks often offer competitive rates, especially to customers with strong credit and existing relationships.

- Credit Unions: These member-owned institutions are known for offering some of the lowest interest rates because they are non-profit and pass savings back to their members.

- Dealership Financing: While convenient, dealership financing (often through captive finance companies like Toyota Financial Services or Ford Credit) can sometimes have higher rates, though they also offer promotional rates (like 0% APR) to attract buyers.

- Online Lenders: A growing number of online lenders specialize in car loans, offering quick approvals and competitive rates, particularly for those with good credit.

Shopping around with various lender types is crucial. Pro tips from us: Always get pre-approved from at least two or three different lenders before stepping foot in a dealership.

8. Co-signer: The Boost You Might Need

If you have a limited credit history or a less-than-stellar credit score, adding a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment.

However, a co-signer relationship should be entered into with caution. If you fail to make payments, your co-signer’s credit will also be negatively impacted. It’s a serious commitment for both parties.

Fixed vs. Variable Interest Rates: Which is Right for You?

Car loans typically come with either a fixed or a variable interest rate. Understanding the difference is vital for long-term financial planning.

- Fixed Interest Rate: This is the most common type for car loans. With a fixed rate, your interest percentage remains the same throughout the entire loan term. This means your monthly payment for principal and interest will also stay consistent, providing predictability and making budgeting easier. Based on my experience, most consumers prefer fixed rates for the peace of mind they offer.

- Variable Interest Rate: Less common for standard car loans, a variable rate fluctuates over the loan term based on an underlying benchmark interest rate (like the prime rate). While it might start lower than a fixed rate, your monthly payments could increase or decrease if the benchmark rate changes. This introduces an element of uncertainty, making budgeting more challenging.

For the vast majority of car buyers, a fixed interest rate is the safer and more predictable option.

Calculating Your Car Loan Interest: A Quick Overview

While lenders handle the complex calculations, understanding the basic principle can help you evaluate loan offers. Most car loans use simple interest, meaning interest is calculated only on the principal amount outstanding.

A simple way to estimate your total interest paid is to use an online car loan calculator. You input the loan amount, interest rate, and term, and it will show you your estimated monthly payment and the total interest you’ll pay over the life of the loan. This tool is invaluable for comparing different loan scenarios.

For example, a $25,000 loan at 5% APR over 60 months will have a lower total interest cost than the same loan at 7% APR over 72 months, even if the monthly payments feel similar initially.

Strategies to Secure the Best Car Loan Interest Percentage

Don’t just accept the first offer you receive. With a bit of strategic planning, you can significantly reduce the interest you pay.

1. Prioritize Improving Your Credit Score

Before you even start car shopping, pull your credit reports from Equifax, Experian, and TransUnion. Dispute any errors. Then, focus on reducing existing debt, paying bills on time, and avoiding new credit applications. A few months of diligent effort can boost your score and save you thousands.

2. Save for a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and signals financial stability to lenders. Aim to save at least 10-20% of the vehicle’s price. This not only lowers your interest rate but also reduces your monthly payments and lessens the risk of being underwater on your loan.

3. Shop Around and Get Multiple Quotes

This is perhaps the most crucial advice. Never settle for the first loan offer. Contact banks, credit unions, and online lenders to get pre-approved loan offers. Compare their APRs, not just the interest rates. This competition among lenders can drive down your rate.

4. Get Pre-Approved Before Visiting the Dealership

Armed with a pre-approval letter from an outside lender, you enter the dealership as a cash buyer. This puts you in a much stronger negotiating position. You’ll know the best rate you qualify for, and the dealership will have to beat it to earn your business. This strategy often results in a better overall deal.

5. Negotiate the Interest Rate (and the Car Price)

While the car’s price is often the focus, remember that the interest rate is also negotiable, especially if you have competing offers. Don’t be afraid to ask the dealer to beat your pre-approved rate. Every fraction of a percentage point can save you money over the loan term.

6. Consider a Shorter Loan Term If Possible

If your budget allows for higher monthly payments, opt for a shorter loan term. You’ll likely secure a lower interest rate, and you’ll pay off the car faster, saving a substantial amount in total interest.

7. Refinance Your Car Loan (If Rates Drop or Your Credit Improves)

If you’ve already purchased a car and interest rates have dropped, or if your credit score has significantly improved since you took out the original loan, consider refinancing. Refinancing replaces your current loan with a new one, ideally at a lower interest rate, reducing your monthly payments or total interest paid. Our article, "When to Refinance Your Car Loan: A Smart Financial Move," delves deeper into this topic.

Common Mistakes to Avoid When Getting a Car Loan

Based on my experience in the financial blogging world, I’ve seen recurring errors that cost people money. Avoid these pitfalls:

- Not checking your credit score: Going in blind means you don’t know what rates you truly qualify for.

- Focusing only on the monthly payment: A low monthly payment might sound appealing, but it often means a longer loan term and a much higher total interest paid. Always look at the total cost of the loan.

- Not understanding the full loan terms: Read the fine print! Understand all fees, prepayment penalties (rare for car loans but worth checking), and exactly what you’re agreeing to.

- Skipping pre-approval: This robs you of your negotiating power and makes you susceptible to higher dealer-offered rates.

- Ignoring additional fees: The APR includes these, but be aware of them. Documentation fees, tag and title fees, and extended warranties can inflate the total cost.

- Rolling negative equity into a new loan: If you’re trading in a car you owe more on than it’s worth, avoid adding that negative equity to your new car loan. This means paying interest on money for a car you no longer own.

The Long-Term Impact of Interest Rates

The difference of just a few percentage points on your car loan interest percentage might seem small initially, but its long-term impact is significant. Over a 5-7 year loan term, a higher interest rate can add thousands of dollars to the total cost of your vehicle. This extra money could have been used for savings, investments, or other important financial goals.

Moreover, a manageable interest rate contributes to overall financial health by keeping your monthly payments affordable and reducing financial stress. It’s not just about the car; it’s about your future financial flexibility. For more tips on managing your vehicle finances, you might find our guide, "Maximizing Your Car’s Value: Tips for Smart Ownership," helpful.

Pro Tips from Us: Your Expert Blogger’s Checklist

To summarize the most impactful advice:

- Know Your Credit: Get your credit score and reports in order well before you apply.

- Save, Save, Save: A larger down payment is your secret weapon for lower rates.

- Shop Smart: Get pre-approved by multiple lenders (banks, credit unions, online) before you step into a dealership.

- Compare APRs: Always look at the Annual Percentage Rate, not just the interest rate.

- Negotiate Everything: The car price and the interest rate are both on the table.

- Read the Fine Print: Understand every single detail of your loan agreement.

By following these strategies, you empower yourself to make informed decisions and secure the most favorable car loan interest percentage possible. This due diligence ensures that you not only drive away in the car you want but also with a loan that aligns with your financial goals.

Conclusion: Drive Away with Confidence

Understanding your car loan interest percentage is more than just financial literacy; it’s a critical component of smart car ownership. It’s about being an informed consumer, ready to navigate the complexities of lending with confidence and strategic insight. By mastering the factors that influence your rate, employing smart shopping tactics, and avoiding common mistakes, you can significantly reduce the total cost of your vehicle.

Remember, the goal isn’t just to get approved for a car loan, but to secure one that makes financial sense for you in the long run. Take the time to prepare, compare, and negotiate, and you’ll be well on your way to a financially sound journey on the open road. For further reliable information on car financing, you can consult resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.