Decoding Your Drive: Understanding the Average Car Loan Amount and How to Secure Your Best Deal

Decoding Your Drive: Understanding the Average Car Loan Amount and How to Secure Your Best Deal Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. However, for most of us, this dream hinges on securing a car loan. Understanding the financial landscape, particularly the average car loan amount, is not just an academic exercise; it’s a crucial step towards making an informed and financially sound decision. This comprehensive guide will peel back the layers of auto financing, helping you navigate the complexities of car loans with confidence and clarity.

We’ll dive deep into what truly influences these averages, how they’ve shifted over time, and most importantly, what these figures mean for your personal budget. Our goal is to equip you with the knowledge to not just understand the average, but to beat it by securing the best possible terms for your next vehicle. Let’s hit the road!

Decoding Your Drive: Understanding the Average Car Loan Amount and How to Secure Your Best Deal

Unpacking the Numbers: What is the Average Car Loan Amount Today?

When we talk about the average car loan amount, we’re looking at a dynamic figure that reflects current economic conditions, consumer behavior, and the ever-evolving automotive market. These averages provide a benchmark, a point of reference for where most buyers stand. However, it’s vital to remember that an average is just that – an average – and your specific situation might differ.

Based on my experience tracking auto finance trends, the average car loan amount has steadily climbed over the past decade. This rise is largely driven by increasing vehicle prices, both for new and used models, coupled with a preference for longer loan terms. Consumers are often opting for more feature-rich vehicles, pushing sticker prices higher.

Let’s break down the current landscape into two key categories:

The Average New Car Loan Amount

For those dreaming of a brand-new vehicle, the loan amount tends to be significantly higher. These figures typically reflect the purchase of a vehicle fresh off the lot, often with the latest technology and safety features. Factors like the brand, model, trim level, and any added packages all contribute to this higher price tag.

Historically, new car loan averages have pushed well into the tens of thousands of dollars, often reflecting the MSRP of popular sedans, SUVs, and trucks. This substantial investment means that even small differences in interest rates or loan terms can have a profound impact on the total cost over the life of the loan. Understanding this average helps you gauge if your desired new car aligns with typical financing benchmarks.

The Average Used Car Loan Amount

Opting for a used car can often present a more budget-friendly alternative, and this is reflected in the average used car loan amount. While generally lower than new car loans, these figures have also seen an upward trend. The demand for reliable used vehicles, coupled with supply chain challenges impacting new car production, has kept used car prices relatively robust.

The age, mileage, condition, and make of a used vehicle all play a significant role in its final price and, consequently, the loan amount. Buyers often find that securing a used car loan can be a bit more complex due to varying vehicle conditions and potential lender perceptions of risk. Nevertheless, for many, a used car loan offers an accessible path to vehicle ownership.

Beyond the Benchmark: Key Factors That Influence Your Specific Car Loan Amount

While the average provides a general idea, your personal car loan amount will be sculpted by several critical factors. Understanding these elements is paramount to not only securing a loan but also ensuring it’s one that fits comfortably within your financial framework. Don’t just look at the average; consider how these variables apply to you.

Let’s explore each of these influential factors in detail:

1. The Vehicle’s Price (MSRP or Negotiated Price)

This might seem obvious, but the sticker price of the car you choose is the foundational element of your loan. Whether it’s the Manufacturer’s Suggested Retail Price (MSRP) for a new car or the negotiated price for a used one, this figure directly determines how much you need to borrow. A higher vehicle price naturally translates to a larger loan amount.

It’s crucial to remember that the listed price isn’t always the final price you pay. Dealerships often add additional fees, and you might negotiate the price down. Focusing on the total "out-the-door" price is more important than just the initial sticker price when calculating your potential loan amount.

2. New vs. Used Car Choice

The distinction between a new and used car goes beyond aesthetics; it profoundly impacts your loan. New cars generally command higher prices, leading to larger loan amounts and often longer loan terms to keep monthly payments manageable. They also tend to have lower interest rates for well-qualified buyers due to their perceived reliability and collateral value.

Used cars, while cheaper upfront, might come with slightly higher interest rates, especially for older models, as lenders perceive a greater risk. However, the overall lower principal amount often results in more affordable monthly payments and a quicker path to ownership. Your choice here significantly dictates the initial loan figure.

3. Your Down Payment

A down payment is the cash you pay upfront, reducing the total amount you need to finance. This is one of the most powerful tools you have to control your loan amount and, consequently, your monthly payments and total interest paid. A larger down payment directly lowers the principal of your loan.

Based on my experience, a substantial down payment signals financial stability to lenders and can sometimes even help you qualify for better interest rates. Pro tips from us: Aim for at least 10-20% of the vehicle’s price, if possible. This not only shrinks your loan but also helps protect you from being "upside down" on your loan, where you owe more than the car is worth.

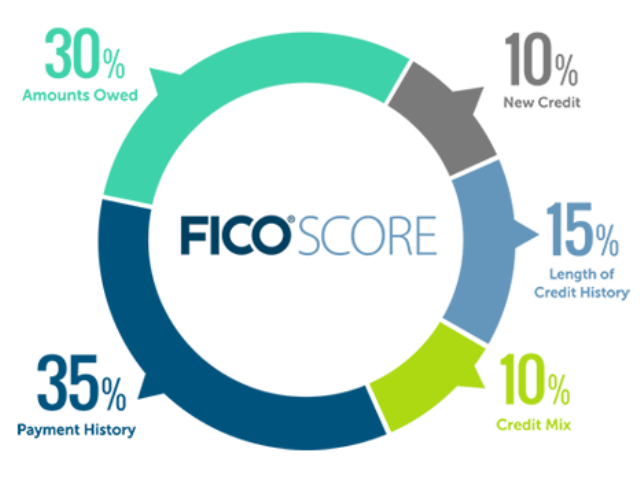

4. Your Credit Score

Your credit score is arguably the single most important factor determining your interest rate and, indirectly, your loan amount. Lenders use this three-digit number to assess your creditworthiness – your likelihood of repaying the loan. A higher credit score (typically 700+) indicates lower risk to lenders.

Excellent credit can unlock the lowest interest rates, significantly reducing the total cost of your loan. Conversely, a poor credit score will result in higher interest rates, meaning you pay more in interest over the life of the loan. This higher interest effectively increases the "cost" of borrowing, even if the principal loan amount remains the same. For more tips on improving your credit score, check out our guide on .

5. The Loan Term (Length of the Loan)

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 60 months, 72 months). While a longer loan term will result in lower monthly payments, it also means you’ll pay more in total interest over the life of the loan. This is because the interest accrues for a longer period.

Common mistakes to avoid are extending the loan term solely to achieve a lower monthly payment without considering the increased total cost. Shorter loan terms, while having higher monthly payments, save you a substantial amount in interest and allow you to pay off your vehicle faster.

6. The Interest Rate (Annual Percentage Rate – APR)

The interest rate, expressed as an Annual Percentage Rate (APR), is the cost of borrowing money. It’s the percentage of the principal loan amount that you pay back to the lender in addition to the principal itself. This rate is heavily influenced by your credit score, the loan term, and current market conditions.

Even a small difference in APR can translate into hundreds or thousands of dollars over the life of a car loan. For instance, a 1% difference on a $30,000 loan over 60 months can easily add over a thousand dollars to your total repayment. Always shop around for the best APR, as it directly impacts your overall loan cost.

7. Trade-in Value

If you’re trading in your current vehicle, its value acts much like a down payment. The trade-in value is deducted from the purchase price of your new car, reducing the amount you need to finance. A higher trade-in value means a lower principal loan amount.

It’s wise to research your car’s trade-in value before heading to the dealership. This empowers you to negotiate effectively and ensures you’re getting a fair deal, further reducing your financing needs.

8. Additional Costs, Fees, and Add-ons

Beyond the vehicle’s price, several other costs can be rolled into your loan, increasing the total amount you finance. These include:

- Sales Tax: Varies by state and significantly adds to the total.

- Registration and Licensing Fees: Required by your state’s DMV.

- Documentation Fees: Charged by dealerships for processing paperwork.

- Extended Warranties: Optional service contracts that can be expensive.

- GAP Insurance: Covers the difference between what you owe and what your car is worth if it’s totaled.

While some of these are mandatory, others are optional. Pro tips from us: Carefully scrutinize any add-ons. While some might offer peace of mind, they also inflate your loan amount and accrue interest. Only finance what you truly need and understand.

Beyond the Average: What You Should Afford – A Personal Approach

Understanding the average car loan amount is one thing, but knowing what you can comfortably afford is entirely another. The average might be far more than your budget allows, or perhaps less than you’re capable of managing. It’s crucial to shift your focus from industry averages to your personal financial reality.

Buying more car than you can afford is a common mistake that can lead to financial strain down the road. Let’s delve into how to determine your personal affordability.

Budgeting for Your Car Loan: The 20/4/10 Rule

A widely recognized guideline for car affordability is the "20/4/10" rule. This framework provides a solid starting point for evaluating what you can reasonably spend:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price. This reduces your loan amount, lowers monthly payments, and helps prevent you from owing more than the car is worth.

- 4-Year Loan Term (48 Months): Keep your loan term to no more than four years. While longer terms offer lower monthly payments, they dramatically increase the total interest paid and extend the period you’re financially tied to the vehicle.

- 10% of Gross Income: Your total monthly car expenses (loan payment, insurance, fuel, maintenance) should not exceed 10% of your gross (pre-tax) monthly income. This ensures your car doesn’t become a disproportionate drain on your finances.

While this is a general rule, it’s a powerful tool for self-assessment. Adjust it based on your specific financial situation and priorities.

Understanding Your Debt-to-Income (DTI) Ratio

Lenders often look at your Debt-to-Income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to manage new debt, making you a less risky borrower. Most lenders prefer a DTI ratio below 43%, though it can vary.

A high DTI ratio, even with a good credit score, might limit the amount a lender is willing to offer you or result in less favorable terms. It’s a key indicator of your overall financial health and capacity to take on new debt.

The Hidden Costs of Car Ownership

Many buyers fixate solely on the monthly loan payment, forgetting that a car comes with a host of other ongoing expenses. These "hidden costs" can quickly erode your budget if not accounted for:

- Car Insurance: Premiums vary significantly based on your age, driving record, location, and the car you choose. A more expensive car generally means higher insurance costs.

- Fuel: Gas prices fluctuate, and fuel efficiency varies greatly between vehicles. Factor in your estimated mileage and current fuel costs.

- Maintenance and Repairs: Even new cars require routine maintenance (oil changes, tire rotations). Older used cars might demand more frequent or costly repairs.

- Registration and Inspection Fees: Annual or biennial costs mandated by your state.

- Parking Fees/Tolls: If applicable to your daily commute or lifestyle.

Common mistakes to avoid are underestimating these recurring expenses. They can easily add several hundred dollars to your monthly outlay. If you’re wondering about the true cost of ownership, our article on has you covered.

Strategies to Secure a Favorable Car Loan

Now that you understand the factors at play and how to assess your own affordability, let’s talk about proactive strategies to ensure you don’t just get a car loan, but the best car loan for your situation. These pro tips, honed over years in the automotive finance industry, can save you thousands.

1. Shop Around for Rates (Get Pre-approved)

Don’t wait until you’re at the dealership to think about financing. Pro tips from us: Start by getting pre-approved for a loan from multiple lenders – banks, credit unions, and online lenders. This process gives you a concrete interest rate and maximum loan amount before you even set foot on a car lot.

Having a pre-approval in hand empowers you to negotiate with confidence. You’ll know what a competitive rate looks like, and you won’t be solely reliant on the dealer’s financing options, which may not always be the most competitive.

2. Improve Your Credit Score Before Applying

Since your credit score is such a major determinant of your interest rate, taking steps to improve it before applying for a loan can pay significant dividends. Pay down existing debts, make all payments on time, and avoid opening new credit accounts in the months leading up to your car purchase. Even a small bump in your score can lead to a noticeably lower APR.

3. Negotiate the Car Price, Not Just the Monthly Payment

This is a critical distinction. Dealers often try to focus buyers on the monthly payment, which can mask a higher overall price or an extended loan term. Always negotiate the total purchase price of the vehicle first, before discussing financing.

Once you’ve agreed on a fair price, then you can discuss the loan terms (APR, length). This approach ensures you’re getting a good deal on the car itself, separate from the financing.

4. Make a Substantial Down Payment

As discussed, a larger down payment directly reduces the amount you need to borrow, cutting down on interest paid and lowering your monthly payments. It also provides a buffer against depreciation, reducing the risk of being upside down on your loan.

5. Consider a Shorter Loan Term

While longer terms offer lower monthly payments, they come at the cost of significantly more interest paid over time. If your budget allows, opt for the shortest loan term you can comfortably afford. This strategy minimizes your total cost of ownership and gets you to debt-free ownership faster.

6. Refinance Your Loan (If Applicable)

If you’ve already secured a car loan and your credit score has improved, or if interest rates have dropped, consider refinancing. Refinancing allows you to replace your existing loan with a new one, potentially at a lower interest rate or with a more favorable term. This can significantly reduce your monthly payments or the total amount of interest you pay.

Conclusion: Driving Towards Smart Financial Decisions

Understanding the average car loan amount is more than just knowing a statistic; it’s about gaining insight into the broader market and positioning yourself for a financially savvy vehicle purchase. We’ve explored the factors that influence these averages, the critical variables that determine your specific loan, and crucial strategies to secure the best possible deal.

Remember, the goal isn’t just to get a car loan, but to secure one that aligns perfectly with your financial health and future goals. By focusing on your affordability, improving your credit, shopping around for rates, and negotiating wisely, you empower yourself to drive away with not just a great car, but a smart financial decision. Don’t let the average define your loan; let your informed choices lead the way.

Now that you’re armed with this comprehensive knowledge, take the first step towards your next vehicle purchase with confidence and clarity. Your wallet will thank you!

External Resource: For up-to-date national auto loan statistics and consumer finance advice, you might find valuable information from the Consumer Financial Protection Bureau (CFPB) or trusted financial news outlets like NerdWallet or Experian. (Note: As an AI, I cannot provide a real-time, specific external link. Please replace this with a current, reputable source.)